The Russell 1000 Value Index has generally underperformed the Russell 1000 Growth Index for the past decade, on average.1 Naturally, this leads to questions about when the tide may turn back in favor of value. Below, I highlight two of the key factors that I believe will influence performance during the next few years.

Finding opportunity in energy and financials

Historically, energy and financials have been well-represented in the Russell 1000 Value Index, especially when measured against its growth counterpart. In December 2008, financials and energy accounted for 24% and 17.3% of the value index, respectively.1 By comparison, their representation in the Russell 1000 Growth Index was meaningfully lower at 4.4% and 8.4%, respectively.1

Fast forward to June 2016, and the exposures are even more starkly contrasted. As of June 30, 2016, the Russell 1000 Value Index’s respective exposure to financials and energy was approximately 27.4% and 13.4%.1 The Russell 1000 Growth Index’s financial exposure was similar at 4.2%, but its energy exposure was only 0.5%.1 Simplistically, it stands to reason that any recovery in value investing could be led by a recovery in these two important sectors.

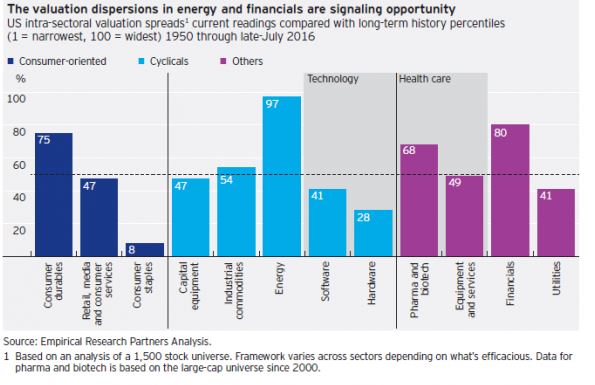

As long-term value investors, one of the trends we track is valuation dispersion — in other words, the difference between the cheapest and most expensive stocks within a sector. When valuation dispersions widen, we see more opportunities to buy undervalued companies. Looking at sectors through that lens, we believe energy and financials have rarely shown more opportunity than they do today. The chart below examines the valuation spread between the cheapest and most expensive stocks within each sector on a monthly basis from 1950 through July 2016. With energy, for example, the bar is at 97%. That means that energy’s valuation dispersion is wider today than it was during 97% of the months in this time frame.

The ‘hedge fund and ETF influence’

The question for investment managers, of course, is why are these sectors trading at wide dispersions and what are the key factors that will determine whether they can revert to more normalized historical valuation levels.

One phenomenon that has been written about recently is the growing influence of hedge funds and exchange-traded funds (ETFs) on the markets. The percentage of investments in ETFs has gone up significantly the last 10 years. Additionally, hedge funds have become a greater percentage of the equity markets as well, and their investments in recent years have moved toward large-cap stocks with strong growth characteristics.

It is our view that all this points to a market that has become even more impatient and short-term focused than it has been in the past. Combine this with the fact that the world suffered through a major financial crisis in 2008, and you have a very nervous investor base that appears to be looking for safety and less willing to take risk. Intuitively it makes sense that this extreme aversion to risk should create periods in which certain stocks and sectors become more undervalued or overvalued than in the past as investors are unwilling to be contrarian. This may create more opportunities for investors who have patience and a long-term focus.

Conclusion

As value investors, we are not here to call the trajectory of the global economy, but only to point out the bottom-up valuation disparities that present themselves today. It’s our belief that even with the unsure global economic backdrop facing governments around the world, they will figure out effective fiscal reform to improve the current, very slow economic growth backdrop, and reversion to the mean will turn out to be alive and well in the equity markets. The question is how long this might take — but we believe the risk/return relationship appears attractive for those who are patient enough to persevere.

1 Source: FactSet Research Systems, as of June 30, 2016

Important information

The Russell 1000® Growth Index, a trademark/service mark of the Frank Russell Co.®, is an unmanaged index considered representative of large-cap growth stocks.

The Russell 1000® Value Index, a trademark/service mark of the Frank Russell Co.®, is an unmanaged index considered representative of large-cap value stocks.

Businesses in the energy sector may be adversely affected by foreign, federal or state regulations governing energy production, distribution and sale as well as supply-and-demand for energy resources. Short-term volatility in energy prices may cause share price fluctuations.

The profitability of businesses in the financial services sector depends on the availability and cost of money and may fluctuate significantly in response to changes in government regulation, interest rates and general economic conditions. These businesses often operate with substantial financial leverage.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. Each entity is an indirect, wholly owned subsidiary of Invesco Ltd. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC, investment adviser. Invesco PowerShares Capital Management LLC (Invesco PowerShares) and Invesco Distributors, Inc., ETF distributor, are indirect, wholly owned subsidiaries of Invesco Ltd.

©2016 Invesco Ltd. All rights reserved.

Energy and financials: The keys to a value resurgence? by Invesco