“We believe that investors chasing yield might be missing the big picture.” – Kapish Bhutani, CFA

The most important and the most difficult question in investment management is, “What to buy?” A stock well bought, like any other merchandise, is half sold. In the current low interest rate environment, investors looking for higher yields have gravitated to dividend-paying consumer staples stocks because they are similar to bonds in their low volatility and reliability of income. These stocks are now trading at a significant premium to their historical averages and to their fundamental characteristics. This overvaluation makes it difficult for value investors, like Diamond Hill, to find investment opportunities with a meaningful margin of safety.

We believe that investors chasing yield might be missing the big picture, as what ultimately matters is total return, not dividend yield. In other words, it is not prudent for investors to overemphasize dividend income at the risk of long-term loss of principal from a market correction. In this piece, I will look into the sources of overvaluation in the consumer staples sector and discuss the investment principles that have guided our response to the all-important question of what to buy in this environment.

Valuation Analysis

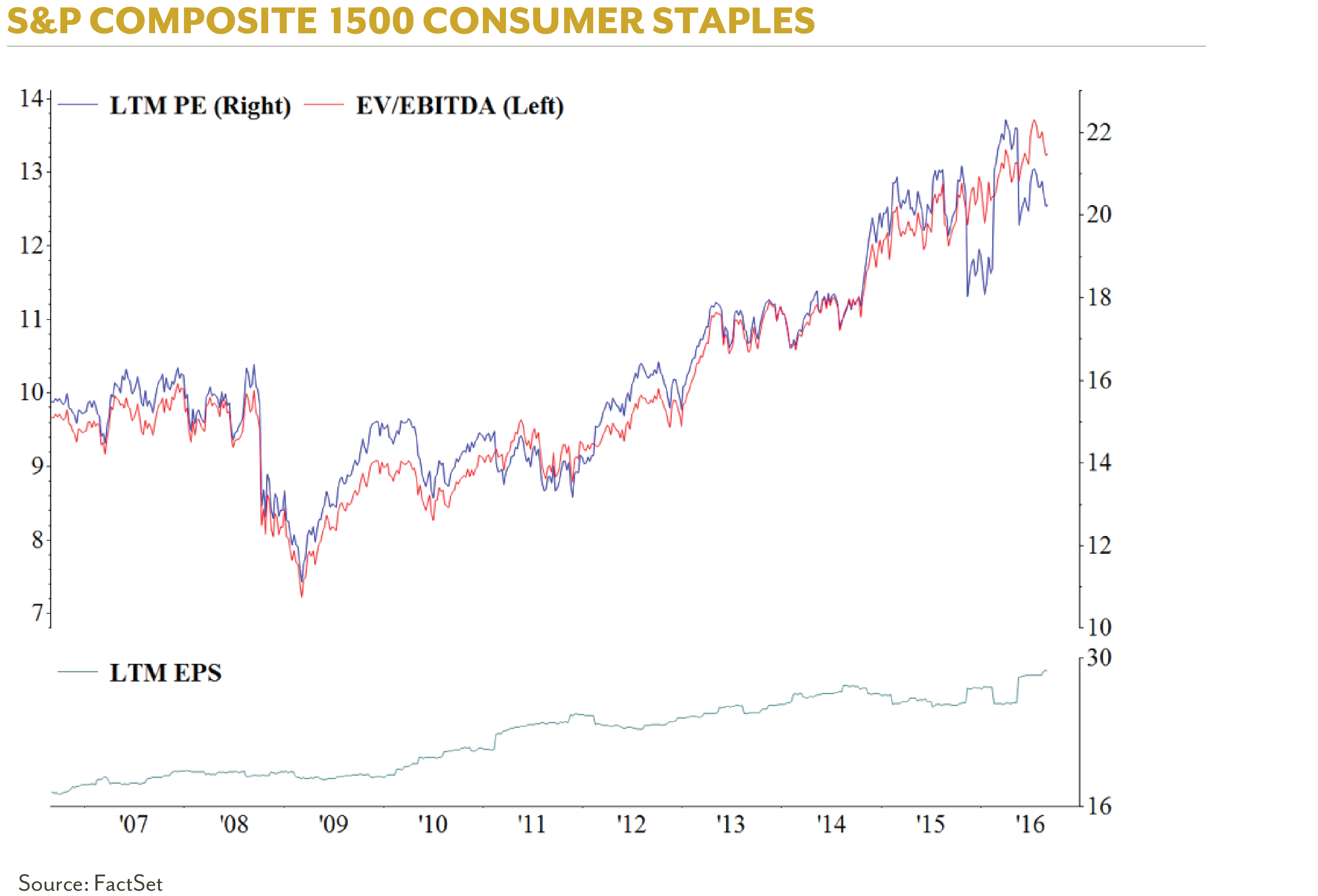

Consumer staples companies, operating in packaged food, beverages, and household and personal care industries, are defensive in nature as consumer demand for these products is less affected by cyclical changes in the broad economy. Many of these companies also enjoy strong competitive advantages from brand loyalty and distribution networks. As a result, the durability and return on capital for these businesses is among the best. That said, however attractive a business or its prospects might be, at some price it ceases to be an attractive investment. Over the last three years, the average price-to-earnings ratio for consumer staples stocks has gone from 16.9x to 20.2x, while the average EV/EBITDA (enterprise value-to-earnings before interest, taxes, depreciation and amortization) ratio has risen from 10.6x to 13.2x1 even as there has been little change in growth or return profile for the overall sector (see chart below).

Source: Factset

Over the trailing ten-year period, the yield on the 10-Year U.S. Treasury bond has fallen by roughly two-thirds from 4.7% to 1.6%1 and now compares unfavorably to the 2.5% dividend yield on consumer staples stocks. Earnings per share for the sector have grown at a 5% rate1 with limited volatility. Add the 2.5% dividend yield to this earnings growth rate and 7.5% total return looks like a bargain in today’s world.

The main problem with this conclusion is that it assumes that valuations will stay where they are. However, it is pretty hard to make that point given high absolute valuation levels relative to history. Moreover, if interest rates rise, then our estimates of intrinsic value are likely to come down as future cash flows would be less valuable at a higher discount rate, and the interest costs will rise for debt refinanced at a higher rate. It is also conceivable that some consumer staples companies will be forced to cut dividends or investments for future growth or stock buy backs to support these higher interest payments.

The other problem with the inference above is that investors expect a continuation of the past earnings growth rate in a very different economic environment. Consumer staples companies, while relatively less affected by macro-economic changes, are not completely insulated. Current levels of overvaluation exist partly because investors expect earnings to grow at a faster rate than in the past, but expect interest rates, which are lower to reflect a less favorable macro-economic situation, to remain low. This anomaly has resulted in future earnings being more highly valued than they should be. We believe it is more appropriate to assume lower earnings growth and lower interest rates, or vice versa, either of which would result in a correction in earnings multiples.

Investment Strategy

It is fairly obvious that lofty consumer staples valuation levels have more to do with external market factors, such as interest rates, and less to do with the stocks’ fundamental characteristics. That said, interest rates are a critical input for determining the intrinsic value of a business. We can neither totally ignore them nor can we extrapolate current rates for many years into the future.

As bottom-up investors, predicting the course of interest rates is outside our circle of competence. Our goal in economic analysis is to protect our clients’ portfolios from adverse outcomes, not to take advantage of economic trends. The ability to perfectly foresee the future is impossible for anyone, but we can be more certain about understanding business strengths and assessing management potential. This is precisely where we have chosen to focus our energies when looking for new ideas in the current environment. Below are some of the key principles that have guided our thinking in recent times.