Come April 2017, many financial professionals will find themselves acting as an ERISA-like fiduciary. The new rule broadens the definition of “investment advice” to impose ERISA-like fiduciary obligations on all advisors to qualified retirement plans as well as IRAs and other tax-deferred accounts, such as Health Savings Accounts.

As an employee benefits professional, it is difficult to avoid talk about the Department of Labor’s (DOL) new Conflict of Interest Rule (also called the fiduciary rule). Much of the discussion has focused on the impact to financial professionals because the rule will hold more advisors to an ERISA-like fiduciary standard. But retirement advisors are not the only benefits professionals who will be impacted by the regulatory changes. Sponsors can expect to see changes as a result of the new rules too:

Your retirement plan advisor will be a fiduciary.

Today

Your retirement plan advisor or consultant may call themselves a fiduciary, or they may not. ERISA has always held financial professionals who receive compensation for providing investment advice to a retirement plan or plan participant to a fiduciary standard, but “investment advice” was narrowly defined. The narrow definition of investment advice allowed retirement plan advisors to choose whether they would accept fiduciary status or not.

April 10, 2017

Your retirement plan advisor or consultant will likely be a co-fiduciary to the plan. The new rule substantially broadens the definition of investment advice, making it almost impossible for a financial professional to help guide an employer on their organization’s retirement plan without becoming an ERISA fiduciary. Having a co-fiduciary helps manage a sponsor’s fiduciary risk, but does not replace a sponsor’s fiduciary liability. The plan sponsor is also a fiduciary and will always be responsible for ensuring that the selected co-fiduciary advisor is in the best interest of plan participants.

TIP: Talk to your advisor about their services and if they are changing in response to the new regulation. Specifically, ask your advisor—and ensure proper documentation for—when they are acting in a fiduciary capacity, what services they will provide, and how much compensation they will receive for their services.

Fee arrangements with your service providers may change.

Today

Fiduciaries are prohibited from paying service providers more than a reasonable fee. Regulators and litigators have suggested factors that may make a fee unreasonable, but there is no clear definition for reasonableness and there are a variety of fee structures in the marketplace. Although service providers give sponsors detailed fee disclosures, many sponsors and participants are still unclear about what fees they pay or what they receive in return.

April 10, 2017

The DOL believes that level fees (a fixed percentage of assets) help avoid conflicts of interest and provide greater transparency and clarity to sponsors and participants. As a result, the new rule incentivizes service providers to use level fee arrangements but stops short of requiring it. Regardless of whether the fee is level or variable, fiduciaries are required to ensure that the fee is reasonable.

TIP: Fee arrangements can be complex. Make sure you understand what your providers are paid and ask them to benchmark their services. Talk to each of your plan providers about their services and document whether they are taking a fiduciary role for any of their plan recommendations.

Participant education resources may change.

Today

Your retirement plan and Health Savings Account (HSA) providers offering administration services, participant education and decision-making resources are not likely fiduciaries. The DOL distinguishes participant education (not a fiduciary action) from ERISA investment advice (fiduciary action). In addition, brokers providing investment advice to Individual Retirement Account (IRA) owners and HSA owners may not be subject to an ERISA-like fiduciary standard.

April 10, 2017

Your retirement plan and HSA providers may be fiduciaries. The new rule narrows the definition of investment education and broadens the definition of investment advice, making it more difficult to provide non-fiduciary education. The new rule also applies to financial professionals providing investment advice to IRA or HSA owners for a fee.

TIP: Talk to your retirement plan and HSA advisors and consultants, recordkeeper, TPAs, and other service providers if their services—particularly HSA resources offered to employees and IRA rollover resources offered to terminated employees—are changing in response to the new regulation. Specifically, ask your service providers and document when they are acting in a fiduciary capacity, what services they will provide, and how much compensation they will receive for their services.

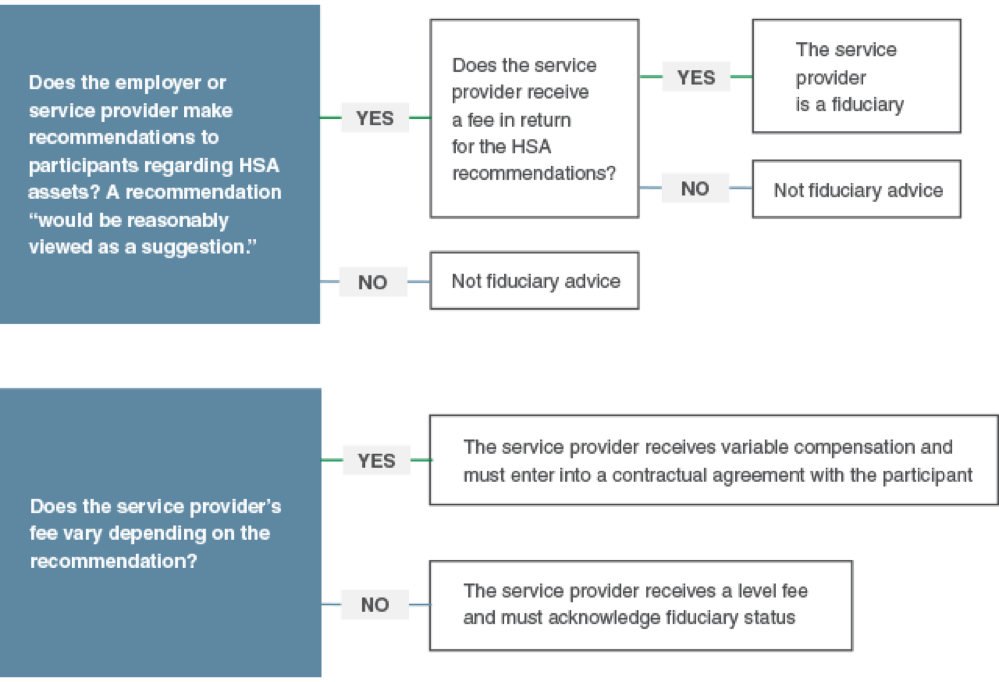

IN FOCUS: ERISA, FIDUCIARIES AND HSAS

Even before the new rule, ERISA’s application to high deductible health plans and Health Savings Accounts caused confusion for many. Group health plans (also called welfare plans), including high deductible health plans, are generally ERISA plans. However, HSAs are individually owned bank accounts and generally not subject to ERISA requirements as long as certain conditions are met. The same is true under the new rule. However, the new rule does impose ERISA-like fiduciary requirements on those who provide participants investment advice regarding their HSA assets. Many questions remain about the new rule’s application, the following decision tree can be a helpful starting point for determining if there are fiduciary obligations under the new rule:

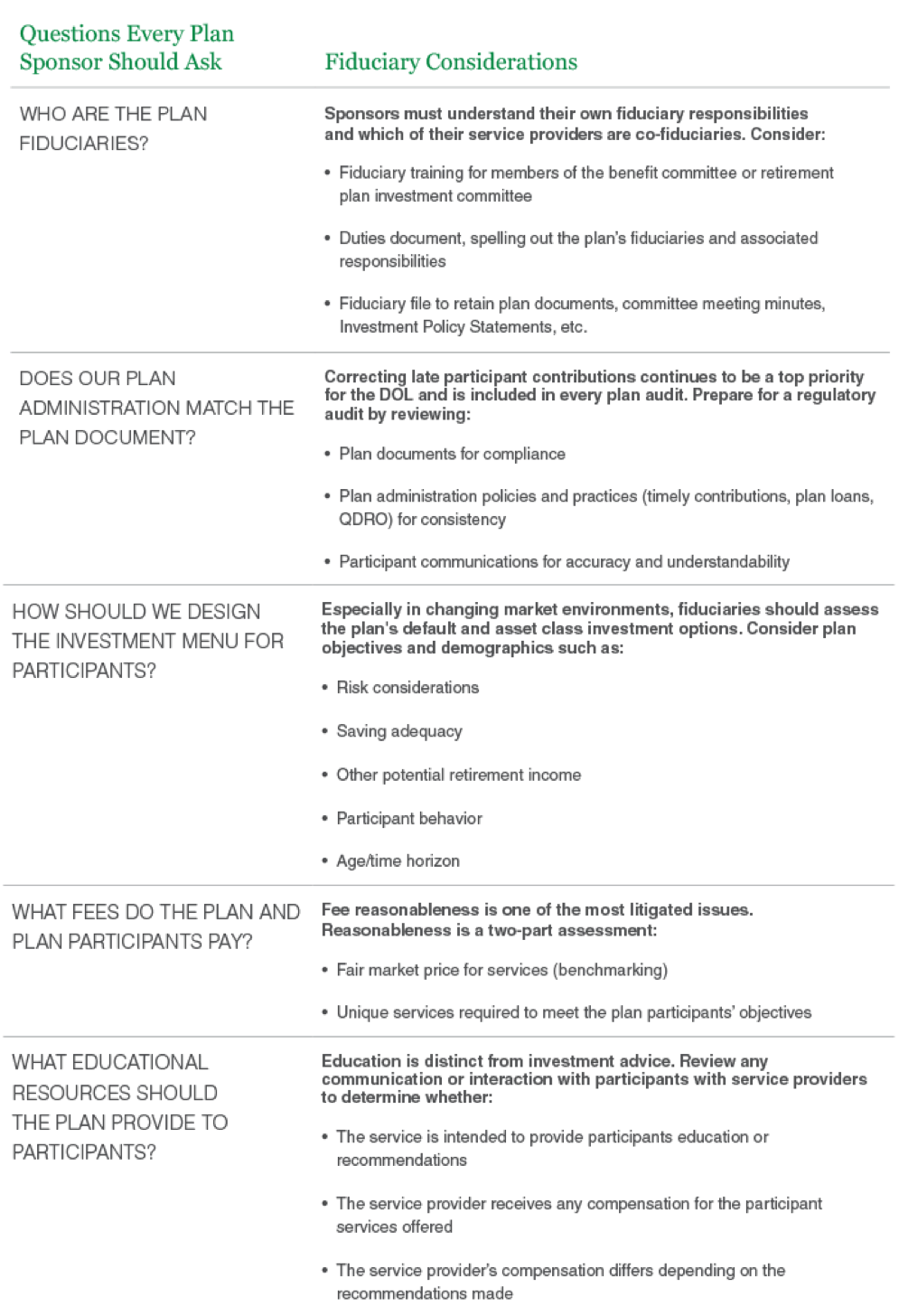

Effective communication among the retirement plan team—the employer, plan advisor, service providers—is critical to successfully navigating the changing regulatory environment. Together the retirement plan team should be able to confidently answer the following five questions with consistency and clarity: