Divided Fed Inches Closer To Rate Rise As Fundamental State of US Economy Remains Positive

The Fed delivered a broadly positive assessment of the state of the US economy at its September meeting, but judged that there was no immediate need to increase US interest rates, with inflation remaining short of the Fed’s 2% target. However, the decision by the Federal Open Market Committee was far from unanimous, as three members voted in favor of a quarter-point rise, leading to increased speculation that a rate hike would be announced at December’s meeting—a decision in November being widely discounted due to the US presidential election. Also noteworthy was a lowering of the Fed’s current and longer-term growth and inflation forecasts, which was accompanied by a trimming of projections for the federal funds rate, as policymakers judged a lower level of interest rates would be required to keep the economy on track.

The Fed’s decision to keep rates on hold came as little surprise after US economic data had turned somewhat softer moving into September, though financial markets remained relatively quiet after the traditional holiday lull in trading volumes. Part of the reason for August’s inactivity was anticipation of Fed Chair Janet Yellen’s speech at the Jackson Hole symposium of central bankers, as investors looked to parse her comments for hints about the future path for US interest rates. But a muted tick up in yields following her speech was swiftly undermined by some weaker data releases, notably the Institute for Supply Management’s (ISM’s) August purchasing managers’ indexes (PMIs) for services and manufacturing, both of which came in well below consensus expectations.

Nevertheless, the fundamental state of the US economy appears little changed to us, with forecasts for growth to improve in the second half of the year still looking on track, underpinned by the resilience of data relating to consumers—by far the most significant part of the economy—despite some signs of weakness elsewhere. Though we are not expecting a particularly strong rebound from the sub-trend growth seen in past quarters, we still believe the economy is likely to revert to its longer-term cyclical average of around a 2% expansion rate.

One of the main factors restricting the economy’s growth potential has been a reversal in productivity gains—in other words, workers failing to improve their efficiency—with the annualized change in the second quarter revised even lower to -0.6%. The fall marked the third consecutive quarter in which the measure has declined, the longest such sequence since the 1970s. According to official data, productivity growth has been lower in the current business cycle than during any of the previous 10 periods. Similar drops in productivity have occurred across numerous G20 countries, although the United States has been less affected by an aging of its workforce—another significant headwind for many other economies. Economists have struggled to explain the US productivity slowdown, with the theories advanced including the shift from a manufacturing to a service-based economy, a mismatch between workers’ skills and employers’ needs, and the difficulties of measuring Internet-based business activity. The decline in productivity was probably one factor behind Fed Chair Yellen’s reference in her Jackson Hole speech to the possibility of a lower neutral level for the federal funds rate.

Another factor that may be weighing on the Fed’s thinking has been a rise in interest rates for US dollar LIBOR (London Interbank Offered Rate). These rates are generally closely correlated to the benchmarks set by the Fed, but they have diverged recently due to new regulations affecting US money market funds, which have provided an incentive for the funds to shift away from higher-yielding commercial paper into lower-yielding government securities. As a result of the lower demand for short-term corporate notes, US dollar LIBOR rates have moved close to their highest level since the global financial crisis. The consequent rise in funding costs for corporate issuers could be seen by Fed policymakers as a de facto tightening of credit for the economy as a whole, with the potential to affect their calculations on the future path of official interest rates.

Economic data released from mid-August and into September had little market impact, although retail sales figures for July were weaker than generally expected, and August’s figures posted the first month-on-month (m/m) decline in five months. The August nonfarm payroll report also came in lower than consensus forecasts, showing the economy added 151,000 jobs from the previous month, but the three-month moving average of job gains remained solid at 232,000, holding well above past levels at this stage of the business cycle. Wage data were more disappointing, with average hourly earnings up only 0.1% m/m, leaving the annual rate of increase down 0.3% at 2.4%.

The backdrop of subdued pricing pressures was generally confirmed by inflation data. The Fed’s favored measure, the core personal consumer expenditures price index, was unchanged from the previous reading, rising in July at 0.1% m/m and 1.6% year-on-year (y/y), with the equivalent headline numbers down a notch at 0.0% and 0.8%. Core consumer price inflation figures for the same period told a similar story, slipping to 2.2% y/y, although data for August were stronger, pushing the annual rate back up to 2.3%.

But it was August’s ISM PMIs that really caught the attention of investors. The services index fell to 51.4, a hefty decline from 55.5 the month before, and its lowest level since 2010. The weakness was widespread, with business activity, new orders and inventories all below the 50-point level that signifies contraction. The fall in the service PMI followed the poor showing of the ISM index covering manufacturing, which slipped back below 50 for the first time in five months, as declines in employment and inventories picked up speed. The report underlined the fragility of this area of the economy, which has been hurt by a stronger US dollar, cuts in capital expenditure by energy companies and weaker global demand for US products.

For all the noise around these single data points, we think US consumers remain well supported by a solid labor market, gains in stock and housing prices, and oil prices that are still low compared to past years despite having rebounded somewhat. In coming quarters, we would expect to see these firm underpinnings translate into a stronger overall rate of growth for the economy, although policy measures to tackle structural headwinds such as stagnant productivity are likely to be required to raise the trend growth rate over the longer term.

Doubts About the Efficacy of Monetary Policy Underlined by Latest BOJ Moves

As in the United States, a sense of holiday-induced torpor was apparent across many other economies and markets in August. A paradigm of weak economic growth alongside government bond yields that remained close to historical lows, primarily driven by radical central bank policies, continued to dominate, amid renewed doubts monetary policy by itself could be effective in shifting the global economy onto a more solid footing.

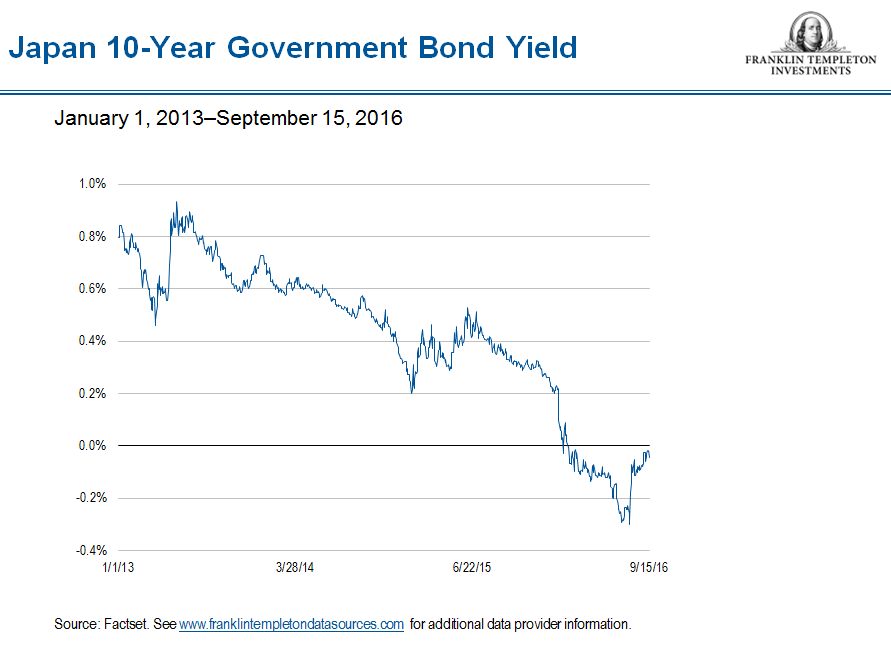

Nowhere was this more apparent than in Japan, where confusion surrounded the BOJ’s intentions ahead of its meeting in late September. The scale of the BOJ’s interventions in the Japanese government bond (JGB) and equity markets has grown ever larger since the central bank embarked on a quantitative easing program in 2013, with its latest commitment in July to raise its annual purchases of ETFs (exchange-traded funds) from ¥3.3 trillion to ¥6 trillion. Both markets have been thoroughly distorted, in our view, with bond market participants often effectively restricted to buying from the government and selling to the BOJ. The central bank has purchased as much as 15% of some companies in the Nikkei 225 Stock Average, the leading Japanese stock market index. Its decision to adopt a negative interest-rate policy in January (after denying such a move was planned only a month earlier) succeeded in pushing down JGB yields across all maturities, but at the cost of simultaneously sparking a counterproductive rise in the Japanese yen.

Yields on 10-year JGBs fell steadily until late July, reaching a record low of -0.30%, but then rebounded sharply as a lack of further action at the BOJ’s July meeting fueled speculation that policymakers might be having second thoughts about pushing interest rates deeper into negative territory. By mid-September, benchmark 10-year yields had risen to a six-month high, even briefly turning positive at one point.

At its September meeting, the BOJ again left interest rates unchanged—although leaving the door open for further cuts—but unveiled two new measures. First, it set a ceiling of 0% on benchmark 10-year JGB yields, which in theory should allow a return to a more conventional sloping yield curve, and thereby ease some of the pressure on banks’ profitability that the flat yield curve so far this year has applied. In a related tweak to its purchasing program, the BOJ also announced plans to buy fewer ultra-long JGBs. Second, the central bank pledged to continue its purchases until inflation had risen above its 2% target and had stabilized above this level.

With the exception of Japanese banking stocks, the immediate market reaction to the new policies was muted, underlining the credibility issue faced by BOJ policymakers. In effect, market participants were demonstrating their lack of belief in the central bank’s ability to reach its inflation target—let alone overshoot it—without the adoption of far more extensive changes to interest rates and the size of its asset purchases.

The BOJ provides perhaps one of the most extreme examples of the repression of interest rates by central banks. In a country with some of the world’s worst debt metrics—most significantly a government debt-to-GDP (gross domestic product) ratio of over 245% according to the International Monetary Fund—government bond yields bear little relation to fundamentals. At some point, Japan—along with other countries that have embarked on such untested monetary policies—may be forced to address the distortions it has imposed upon its markets.

ECB Stays on Hold Amid Eurozone Resilience in Face of Political Uncertainty

The ECB left monetary policy unchanged at its September meeting, and officials refrained from offering any guidance on future moves, disappointing some investors who had hoped for hints on an extension or a widening of the central bank’s bond-purchasing program. The ECB’s decision to remain on hold followed economic data suggesting the eurozone’s fragile recovery had not been affected by the United Kingdom’s vote in June to leave the European Union (EU). The single-currency bloc’s early PMI for August reached its highest level in seven months, with encouraging signs the French economy was likely to bounce back after its stagnant performance in the second quarter, though these figures were later revised downward.

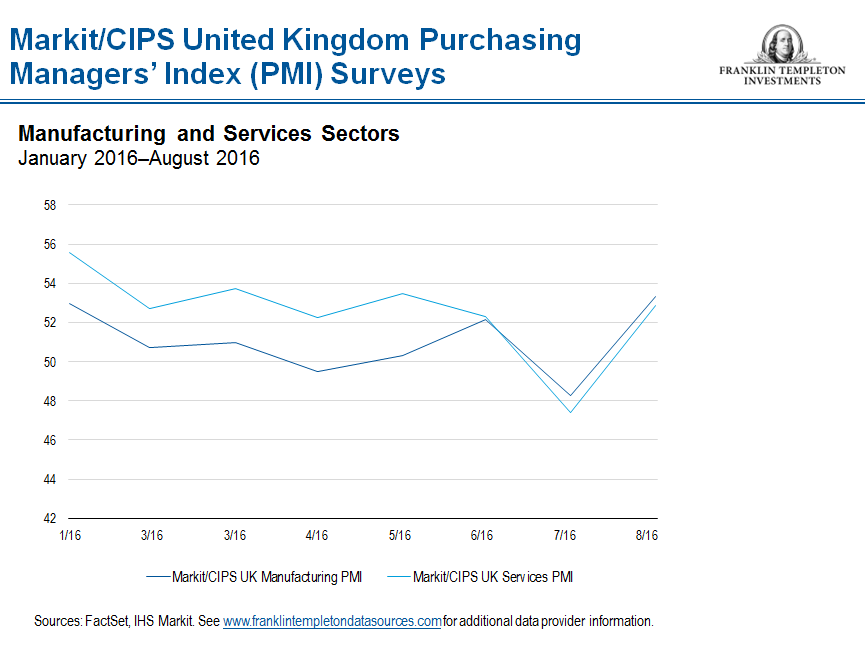

More surprising was the resilience of UK economic data, with both service and manufacturing PMIs rebounding strongly in August from their poor showing in the aftermath of the referendum result. The strength of the data led some market participants to reassess their earlier calls that the United Kingdom was likely to fall into recession in 2017, and led to some criticism that the Bank of England had moved too quickly to ease monetary policy at the start of August. Nevertheless, UK Prime Minister Theresa May was reminded of the difficult path ahead at a meeting of G20 leaders in China, as Japan called on Britain to negotiate a deal with the EU allowing Japanese companies invested in the United Kingdom to maintain their access to the European single market, or else risk seeing them relocate their investments elsewhere in Europe.

The political situation in Spain remained deadlocked, despite a fresh attempt by acting Prime Minister Mariano Rajoy, leader of the conservative Partido Popular (PP) that won around a third of the vote in the last election in June, to end the stalemate. A new pact between the PP and the centrist Ciudadanos party failed to deliver enough support, and an attempt to form a government was rejected by the Spanish parliament. Unless a solution is agreed upon between the four main political groupings within the next two months, which seems unlikely, the caretaker administration will remain in place until another election in December.

However, far from suffering from the political gridlock, the Spanish economy has proved remarkably unaffected, growing at 0.8% quarter-on-quarter for each of the past four quarters, with consensus forecasts pointing toward a rate of more than 3% for 2016 as a whole. Part of the reason has been an expanded fiscal stimulus that has moved well above the EU ceiling of 3%, though the fact that other countries like France and Portugal have also exceeded this threshold has saved Spain from any retaliatory measures from Brussels. As many tourists have avoided countries affected by terrorism and flocked to Spain instead, revenues have boomed, adding nearly one percentage point to growth according to some estimates. Moreover, Spain’s unemployment rate fell below 20% in June and July, down from a peak of more than 26% in 2013.

And yet neither the political deadlock nor the economy’s strength has had any effect on the direction of Spanish government bond yields. Benchmark 10-year yields, which peaked at over 7% at the height of the eurozone crisis in 2012, have steadily declined ever since, falling below 1% for the first time in August. With investors seemingly convinced the ECB’s bond-purchasing program will underpin the market for the foreseeable future, Spanish bonds have long since decoupled from local political or economic developments. In broad terms, non-core eurozone sovereign debt such as Spain’s has proved attractive to investors seeking a way to boost potential returns, in a wider European environment where negative yields are a common occurrence.

The clouds that have hung over the European banking system cleared a little in August, as financial stocks enjoyed a late summer bounce. The sector was one of the hardest hit by the shock of the UK referendum result, and it has therefore been one of the main beneficiaries of the subsequently calmer tone in markets. Recent results from European banks have been mostly solid, with a notable lack of resulting downgrades, in contrast to previous earnings seasons. Within the sector, market speculation about a potential merger between two major German banks was quashed by the chief executive officer of one of them. However, sentiment regarding the troubled Italian banking sector improved after Italian Prime Minister Matteo Renzi’s announcement that he would not call elections before 2018, whatever the result of the country’s upcoming referendu Templetonm on constitutional reform.

Overall, considering the short-term volatility that the United Kingdom’s referendum result unleashed in financial markets, it is remarkable how little the wider picture appears to have changed in Europe since the vote. The UK government clearly has no desire to be hurried into spelling out the compromises required to redefine the country’s relationship with the EU. With French and German leadership elections due in 2017, the likelihood of another Spanish poll and Italy’s forthcoming referendum—and the potential for a populist backlash similar to the UK vote to occur in one or more of these countries—an extended era of political uncertainty for Europe looks almost assured. Such a backdrop in turn seems likely to hold back a stronger regional recovery, leaving the ECB with little alternative other than to keep monetary policy extremely accommodative for some time.

© Franklin Templeton

http://us.beyondbullsandbears.com

© Franklin Templeton Investments