KEY TAKEAWAYS

- Earnings growth across emerging market (EM) equities has been positive in contrast to the decline in earnings and earnings expectations in developed international markets.

- Valuations in EM have not increased at the same pace as developed international or U.S. markets, creating a more attractive entry point for the asset class.

- Technical weakness in developed foreign markets is coinciding with reductions in earnings expectations.

By nature, emerging markets (EM) have greater risks, but they also have attractive attributes relative to developed foreign markets. For most markets, earnings have been stagnant while valuations—what investors are willing to pay for those earnings—have increased. In contrast, emerging markets are beginning to see earnings actually increase, albeit modestly. Initially, EM earnings growth was driven by commodity related sectors, but has broadened out, most importantly to include financial stocks. Furthermore, valuations in EM have not experienced the same expansion as other markets. As the earnings picture is souring for developed foreign markets, represented by the MSCI EAFE Index, overall, these developments increase the relative attractiveness of EM stocks.International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

IMPROVEMENT FOR EM EARNINGS

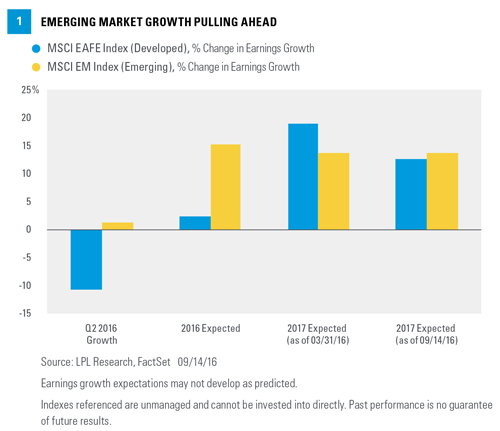

Given that the global financial markets have been in an earnings recession, emerging markets have experienced both earnings growth and improved expectations for future earnings growth. Admittedly, this growth is modest in both respects, but it is in stark contrast to prolonged earnings weakness in Europe[Figure 1]. EM earnings rose 1.3% year over year in the second quarter of 2016, a gain made more significant because at the beginning of the quarter, expectations were for a 6% earnings decline. More importantly, whereas 2017 earnings forecasts for the EAFE Index have declined over the past five months, expectations for EM are essentially unchanged. The fact that EM earnings have grown, and have exceeded expectations, has created greater confidence in forecasts. The poor performance in developed overseas markets has forced the market to lower expectations for the future.

The source of earnings growth is also telling, and shows the contrasts between developed and emerging economies. Earlier in the year, we saw EM earnings growth largely in commodity-related companies, as prices of not only energy, but also copper, iron ore, gold, and other commodities rallied after the sharp decline in late 2015 and early 2016. However, commodities no longer dominate the EM stock universe. In March 2011, commodity stocks represented nearly 40% of the index; today, energy and materials together only comprise 13.4% of the index. However, commodity-related stocks still “punch above their weight” by affecting stocks in other sectors, and entire national economies for countries like Brazil and Russia are heavily tied to commodity prices.

Today, financial stocks are the largest sector in both the MSCI EM and EAFE Indexes, at 26.5% and 19.2%, respectively. As has been well documented, the negative interest rate environment across the developed world has affected earnings and the performance of financial stocks. However, negative rates are a developed market phenomenon only; emerging countries tend to have much higher interest rates. In fact, the farther a country is removed from the global economic mainstream, the higher its interest rates tend to be. For example, export-dependent countries like South Korea and Taiwan have very low, though still positive, rates at 1.25% and 1.375%, respectively; while countries like China and India are at 4.35% and 6.5%. Rates are even higher in less politically stable countries, like Russia, where the central bank just cut rates to 10%, and Brazil, where short-term rates are 14.5%.

We can see the impact of low rates on financial earnings. Second quarter 2016 earnings for the developed world financial sector (defined by the MSCI EAFE Index) declined -11.6%. Equally, if not more important, expectations for earnings for the rest of 2016 and for 2017 have been reduced. At the end of March 2016 (before any first quarter earnings were released), financial sector earnings for the year were expected to be flat. Currently, consensus expectations are for financial sector earnings to decline -9.8% for the year. The outlook for developed market financials has become even gloomier. In contrast, earnings for financial companies in EM actually grew by 2.7% during the second quarter. While not much, it is certainly much better than in developed markets. Furthermore, expectations for financial company earnings for the rest of the year really have not changed from March 31 to today. The market is expecting financial earnings growth of just over 14% for 2016.

VALUATIONS EMERGE AS ATTRACTIVE

Earnings growth is important, but so is what investors are willing to pay for earnings. Low interest rates globally have encouraged investors to buy stocks seeking greater total returns, and increasingly seek income from dividend-paying stocks rather than from bonds. As noted above, EM interest rates have not had the same magnitude of decline; in some markets, rates remain quite high. This is one reason that EM valuations have not expanded as rapidly as the same measures for the U.S. and EAFE [Figure 2]. Globally, we see price-to-earnings ratios (PE) generally follow each other across the regions. This makes sense, despite regional differences; all stock markets operate in a world that became increasingly globalized. However, valuations for both the U.S. and EAFE expanded rapidly, partially because of the cumulative impact of the Fed’s third quantitative easing program that began in September 2012 and further interest rate reductions by the European Central Bank (ECB) in May 2013. Equity markets in the U.S. rallied, but with PE expansion as a significant part of that rally. The reverse happened in EM. Stock prices fell and valuations for the asset class contracted. We believe this divergence may represent an opportunity, but only if earnings continue to increase.

COMBINING FACTORS

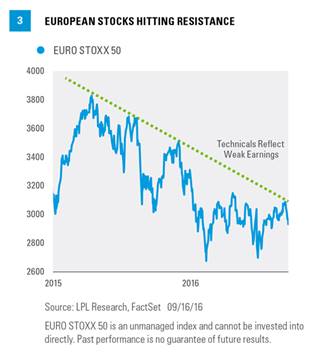

LPL Research uses a combination of fundamentals, like earnings growth, valuations, and technical factors in evaluating investment opportunities. While this commentary focused mostly on EM, several previous commentaries have focused on Europe, which is the primary component of the EAFE Index. We can use the activity in the European markets to show how these factors combine. Valuations have increased in Europe, though not to the same extent as for U.S. equities. Earnings in developed overseas markets have declined and expectations continue to fall. The technicals are telling us that the market has real questions about European fundamentals. Overall, Europe continues to lag, as nearly all European country stock markets are down in 2016, with the Financial Times Stock Exchange (FTSE, the primary U.K. stock market gauge) the surprising outperformer. Technically, the EURO STOXX 50 has been in a downtrend for more than 15 years. Focusing on more recent market activity [Figure 3], the EURO STOXX 50 ran into firm resistance from a trend line going back to the April 2015 peak. We can see in this example how the three components of our process can reinforce each other, and in this case reinforce our caution with respect to Europe and developed international equities in general.

CONCLUSION

Emerging markets have seen earnings increase and future expectations remain stable. This improvement has occurred across many sectors, including the important financial sector. Combined with relatively attractive valuations, we believe opportunities exist in EM for suitable investors, though strength in these markets will likely depend on continued earnings growth. We can see how disappointing earnings can impact performance, and therefore the stock charts and technicals, by looking at recent technical weakness in European stocks.

Thank you to Ryan Detrick for his contributions to this report.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market.

All investing involves risk including loss of principal.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The MSCI EAFE Index is recognized as the pre-eminent benchmark in the United States to measure international equity performance. It comprises the MSCI country indexes that represent developed markets outside of North America: Europe, Australasia, and the Far East.

The MSCI Emerging Markets Index captures large and mid cap representation across 23 emerging markets (EM) countries. With 822 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

The EURO STOXX 50 Index is a blue-chip index for the Eurozone, which covers 50 stocks from 12 Eurozone countries: Austria, Belgium, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, the Netherlands, Portugal, and Spain.

This research material has been prepared by LPL Financial LLC.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial LLC is not an affiliate of and makes no representation with respect to such entity.

Not FDIC or NCUA/NCUSIF Insured | No Bank or Credit Union Guarantee | May Lose Value | Not Guaranteed by Any Government Agency | Not a Bank/Credit Union Deposit

RES 5633 0916 | Tracking #1-536666 (Exp. 09/17)

© LPL Financial