KEY TAKEAWAYS

The Fed holds its sixth of eight FOMC meetings of 2016 this Tuesday andWednesday, September 20–21, 2016.

With a rate hike unlikely, the Fed may begin to prepare the markets for a hike in December.

Fed Chair Yellen’s third post-FOMC meeting press conference of 2016 provides an opportunity for the Fed to add color to its views of the economy, inflation, and financial market volatility, and to dodge questions about politics.

As the sixth of eight Federal Open Market Committee (FOMC) meetings of 2016 approaches later this week, the market and the Federal Reserve (Fed) again remain deeply divided over the timing and pace of Fed rate hikes. In addition, the FOMC itself seems more divided, with many on the committee ready to raise rates now, while others urge patience.

WHAT IS THE SCHEDULE OF EVENTS FOR THE FED THIS WEEK?

The FOMC meeting this Tuesday and Wednesday, September 20–21, will be followed by an FOMC statement at 2:00 p.m. ET on Wednesday, along with the FOMC’s latest economic forecasts for gross domestic product (GDP), the unemployment rate, inflation, and fed funds projections (aka the “dot plots”) for year-end 2016, 2017, 2018, and for the first time, 2019, as well as the “long run.” At 2:30 p.m. ET, Fed Chair Janet Yellen will hold her third post-FOMC press conference of 2016, which is her first public appearance since her speech at Jackson Hole, Wyoming in late August 2016.

HAS THE MARKET PRICED IN A RATE HIKE AT THIS WEEK’S MEETING?

In short, no. As of Monday morning, September 19, the fed funds futures market has priced in just a 20% chance of a 25 basis point (0.25%) rate hike at this week’s meeting. Another good proxy for what the market is pricing in is the yield on the 2-year Treasury note, the Treasury note most sensitive to the Fed’s actions. The 2-year note yield has moved from 0.55% in late July 2016—in the aftermath of the late June Brexit vote and a weak June 2016 employment report (released in early July 2016)—to just under 0.80% here in mid-September 2016. At just 0.80%, the 2-year yield is below where it was (1.0%) when the Fed hiked rates in mid-December 2015[Figure 1].

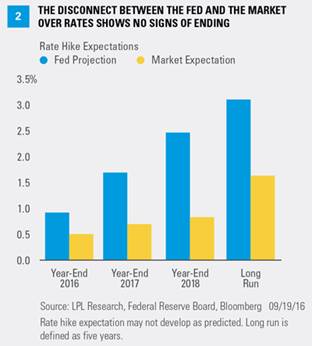

HOW LARGE IS THE DISCONNECT BETWEEN THE FED AND THE MARKET ON RATES?

The FOMC’s latest forecast (June 2016) puts the fed funds rate at 0.875% by the end of 2016. The Fed will provide a new set of dot plots this week. As of September 19, the market (according to fed funds futures) puts the fed funds rate at around 0.50% by the end of 2016 [Figure 2], not fully pricing in even one 25 basis point (0.25%) rate hike this year. The latest dot plots (released in June 2016) had put the fed funds rate at 1.625% at the end of 2017, while the market says it will be less than half of that, at around 0.70%. The Fed’s June 2016 dot plots put the fed funds rate in the long term at 3.0%, down from 3.5%. As noted in Figure 3, the FOMC’s view of the long run fed funds rate has moved substantially lower over the past four years, as both economic growth and inflation have come in below their forecasts. The debate over the proper level for the “neutral” fed funds rate—among FOMC participants, and between the market and the Fed—is likely to persist well beyond this week’s meeting. On balance, we believe the FOMC will continue to lower its “dot plot,” forecasts for 2017, 2018, and perhaps even the “long run” to soften the blow of a rate hike later this year, but not by much.

How that gap closes—between what the market thinks the Fed will do and what the Fed is implying it will do—against the backdrop of what the Fed actually does will continue to be a key source of distraction for markets in 2016.

DOES THE FED CHANGE MONETARY POLICY IN AN ELECTION YEAR?

It often has and may do it again, despite misconceptions the Fed stands down before major elections. Although the Fed often pauses in the month or so prior to the November election, the Fed has changed policy (either raised or lowered rates or stopped or started quantitative easing [QE]) in every election year since at least 1968. We do not expect anything different in 2016, if conditions in the economy and labor force warrant a move. If the data called for a move at this week’s meeting, the Fed would likely act. However, the Fed would likely not raise rates at the November 2 FOMC meeting, which is less than a week ahead of Election Day on November 8. The final FOMC meeting of 2016 is on December 13–14, and our view is that the Fed considers that a “live” meeting; the fed funds futures market agrees, currently pricing in about a 55% chance of a hike at the December 2016 FOMC meeting.