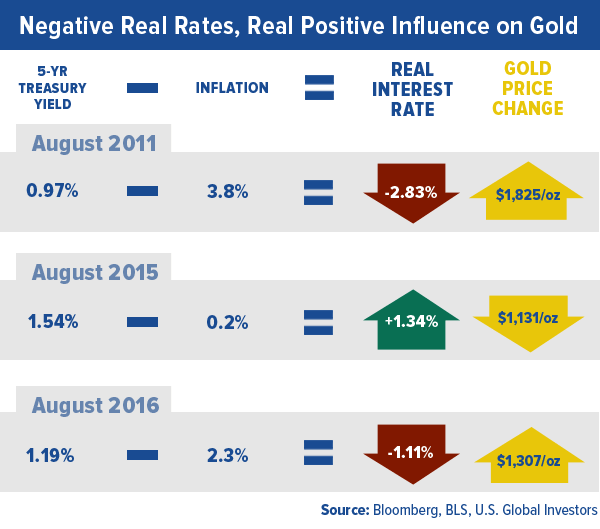

Today the consumer price index (CPI), a measure of inflation, came in hotter than expected, registering 2.3 percent year-over-year in August on expectations of 2.0 percent. With the five-year Treasury yielding 1.19 percent, government bond investors are now receiving a negative real rate of return (because 2.3 minus 1.19 comes out to negative 1.11 percent).

This is highly constructive for the price of gold. As I’ve discussed many times before, the yellow metal has benefited when real rates have fallen below zero. This was the case in September 2011 when gold hit its all-time high of $1,900 per ounce. And last year around this time, the opposite was true—positive real rates were a drag on gold.

Although gold sunk to a two-week low today on a strong U.S. dollar and fears over next week’s Federal Reserve meeting, the drivers are firmly in place to push prices higher.

| LEARN MORE ABOUT WHAT’S DRIVING GOLD |

|

Maybe you’ve heard that a new book out right now is lending its propaganda voice in the war on cash. In “The Curse of Cash,” Harvard economics professor Kenneth Rogoff makes the case that nixing paper money—at the very least, larger-denominated bills—“could help more than you might think” in combating criminal activities such as drug trafficking, corruption, extortion and money laundering. It could even prevent the spread of terrorism and discourage illegal immigration, Rogoff argues.

It gets even worse. Central banks, he adds, should have the latitude to drop interest rates below zero during recessions to spur spending. If the Federal Reserve tried this now, of course, many people would likely convert their savings into paper—which at least yields 0 percent—and hoard it in bedroom safes. This is precisely what many Germans have reportedly done, prompting safe manufacturers to scramble to meet demand

But in a world where nothing larger than a $10 bill exists, hoarding cash would be highly impractical. Better to buy that new boat you don’t need!

While we all agree that corruption and terrorism are things that should be stopped, killing cash is the absolute wrong way to go about it.

Instead, perhaps Rogoff should consider “The Curse of No Cash.” Does he not recall what happened in Cyprus just three years ago? The government ransacked citizens’ bank accounts to “fix” its own mistakes and mismanagement. In example after example, people’s rights to save and freely hold cash have been disrupted, with tragic results.

I’ve written about this topic before. In a cashless society, your economic liberty is forever at risk. Every transaction could be monitored, taxed and charged a fee. Capital controls would be crippling, assets could be seized. Just ask the Colombians and Venezuelans

I find Google helpful in gauging the spin and general opinions on a theme by scanning headlines. I’m not the only one who disagrees with the ideas in Rogoff’s polemic against money. As of this writing, nearly three quarters of Amazon customers have given the book a rating of two or fewer stars. And in a scathing Wall Street Journal op-ed, respected financial writer James Grant strips away the book’s “technical pretense” to uncover its true motive. Rogoff, he writes, “wants the government to control your money,” which is the extreme form of Keynesian economics.

Gold Has Shined Brightly During Currency Crises

There’s one area where Rogoff and I both agree, though. “As paper currency is phased out,” he writes, “gold prices will rise.” Were cash eliminated and interest rates plunged underwater, gold’s role as a store of value would become even more apparent and demand for the yellow metal would turn red hot, despite its price appreciation.

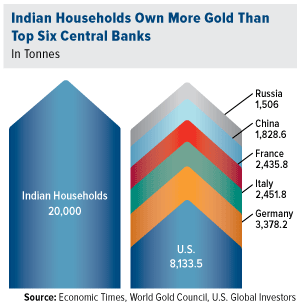

This has been the case in countless past examples. Rogoff himself cites Indians’ longstanding love of and cultural affinity to gold jewelry as protection against currency uncertainty. For centuries, inhabitants of the Indian subcontinent saw continuous regime change, not to mention imperialist rule by various European forces. During all this time, the one stable and widely accepted currency was gold.

|

The tradition carries on today, as I’ve written about many times before. A third of Indian gold jewelry demand comes from rural farmers, who annually convert a portion of their crop revenues into the yellow metal. Whether this gold is stored or given to a female family member, perhaps a daughter, before her wedding day, its purpose is twofold: one, as a beautiful heirloom to be worn and passed down to the next generation, and two, as a form of financial security.

It’s estimated that Indian households currently hold more than 20,000 tonnes of gold. To put that in perspective, 20,000 tonnes is more than the official gold holdings of the U.S., Germany, Italy, France, China and Russia combined.

With speculation strong that a rupee devaluation is imminent, it makes just as much sense now as ever for Indians to have at least some of their wealth in gold. When the rupee unexpectedly dipped to record lows in August 2013, the wealth that prudent Indians had placed in the precious metal was, for the time being, safe.

Although there’s little fear right now that the U.S. dollar is in trouble, I still recommend that investors maintain a 10 percent weighting to gold—5 percent in gold stocks, 5 percent in gold coins and jewelry.

Is Chicago Next to Declare Bankruptcy?

|

It’s not just Indian investors who should be aware of currency fluctuations and imbalances in monetary and fiscal policy. These can happen right here in our own backyards, and investors who aren’t paying attention—specifically municipal bond investors—could pay a steep price. When we go hunting for tax-free bonds, we stay away from irresponsible government policy.

In the past few years, we’ve seen how financial mismanagement can bring calamity to state and local economies, the most notable example being Detroit’s $18 billion bankruptcy in July 2013, the largest in U.S. history. Right now, the U.S. territory of Puerto Rico is in dire financial straits, owing some $70 billion, more than any state government except California and New York.

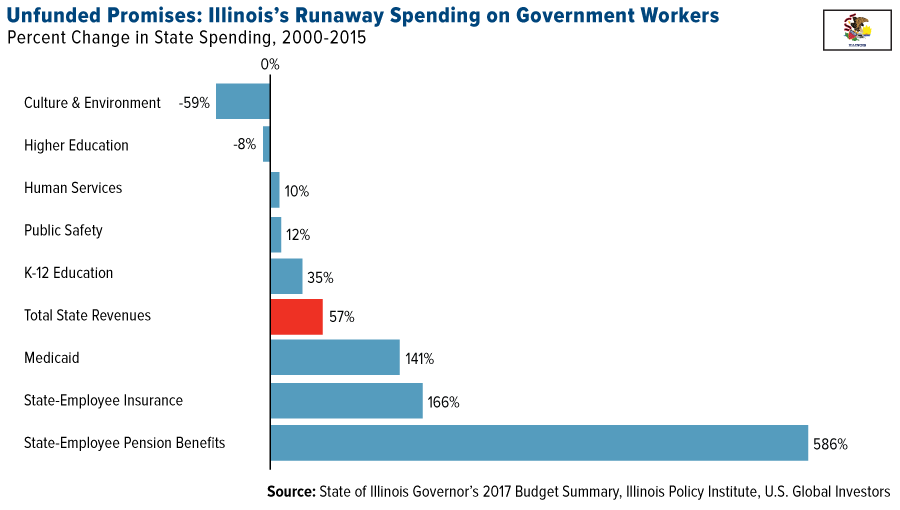

And then there’s Chicago, which is looking at $170 billion in unfunded pensions and other costs.

This came to my attention earlier this month when I visited Chicago to attend the Morningstar ETF Conference. While there, I had the opportunity to speak to several locals, who shared with me their frustration of high local tax rates—some of the highest in the country.

Taxes are high, they said, mainly because of outrageous pensions for public and union workers. Entitlement spending has exploded. Now, Chicago, which has the lowest credit rating of any major U.S. city, is edging scarily close to bankruptcy.

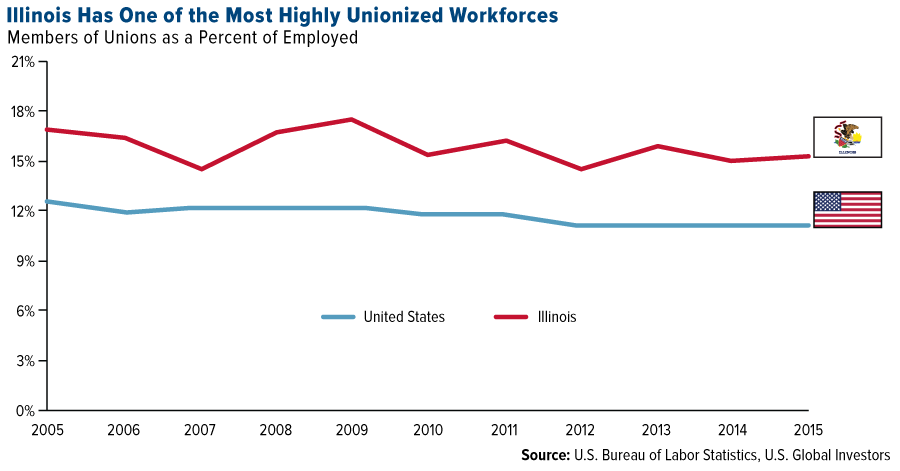

Unfortunately, it isn’t hard to see why. For starters, the state has one of the most highly unionized workforces in the country, compared to the national average.

And instead of reining in costs, state and city officials continue to add to the pile of debt. The Land of Lincoln already has the least funded retirement system in the country, according to Bloomberg, and is on track to end the year $7.8 billion in the hole.

Lawmakers and other government workers are among the highest paid in the nation and enjoy “Cadillac” health care benefits and pensions. It’s not uncommon for them to retire in their 50s. The Illinois Policy Institute estimates that the total annual operating cost for each state lawmaker—including salary, insurance and the like—stands at more than $100,000, with private taxpayers footing most of the bill.

“It’s like we work for the government,” one Chicagoan told me. “Everything we make goes to their pensions.”

Conveniently, the state constitution includes a clause that forbids any reduction of public pensions.

For these reasons, Illinois is saddled with some of the highest income and corporate taxes in the United States. Chicago’s sales tax is the highest of any major U.S. city. Despite the revenue this generates, it doesn’t come close to touching what’s been promised.

Look at the chart below. Between 2000 and 2015, Illinois tax revenue increased 57 percent. That’s a significant jump. But over the same period, state-employee insurance and pension benefits skyrocketed—166 and 586 percent respectively—while essential services such as higher education suffered.

What this means is very little of taxpayers’ money is going toward anything tangible—new schools, new hospitals, new wastewater treatment plants. Nothing that provides jobs or has a multiple effect is being produced.

We’re already seeing serious consequences as a result of the state and city’s fiscal woes. In a recent study of jobs market competitiveness, CareerBuilder found that Chicago is the least competitive metropolitan area in the U.S. in terms of jobs growth. Between 2014 and 2015, the Windy City’s rate of adding jobs was far short of the national average.

Because of this—among other reasons, including crime, unemployment and political infighting—Chicago had the largest population loss of any metro in the U.S last year (6,263). Meanwhile, Illinois was one of only seven states to see a net decline (22,194).

And where are these people going? Where the jobs are, of course. I always say that money flows where it’s most respected. People behave the same way.

It’s no wonder, then, that the state that attracts the most Illinois expats is Texas, according to the Chicago Tribune. This falls in line with what I wrote just a couple of weeks ago. Between 2014 and 2015, Texas added more residents than any other state because of its strong economy, abundance of jobs and low taxes. CareerBuilder’s jobs study, I should point out, rated Dallas as the most competitive city. And within the next eight to 10 years, Houston is expected to surpass Chicago to become the nation’s third largest city by population.

I’m not saying this to beat up on Chicago, but to emphasize my earlier point about being aware and prepared—especially, in this case, when it comes to municipal bond investing. Many passive muni funds might hold Chicago debt because it’s high-yielding. But those yields could come at a huge cost. Three years ago, bondholders of Detroit’s bad debt learned the hard way that, in the event of a default, pensioners get paid first, investors last—or worse, not at all.

As active managers we’re well aware of this. We sincerely hope Chicago can straighten out its balance sheet, but in the meantime, we feel it’s not a space to be a buyer right now. Instead, we seek to invest primarily in high-quality, short-term munis.

| LEARN MORE ABOUT SHORT-TERM MUNIS |

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 0.21 percent. The S&P 500 Stock Index rose 0.53 percent, while the Nasdaq Composite climbed 2.31 percent. The Russell 2000 small capitalization index gained 0.46 percent this week.

- The Hang Seng Composite lost 3.17 percent this week; while Taiwan was down 2.87 percent and the KOSPI fell 1.89 percent.

- The 10-year Treasury bond yield rose 1 basis point to 1.69 percent.

Domestic Equity Market

Strengths

- Information technology was the best performing sector for the week, increasing by 3.03 percent versus an overall increase of 0.53 percent for the S&P 500.

- Skyworks Solutions was the best performing stock for the week, increasing 13.95 percent.

- The biggest M&A deal of 2016 was announced Wednesday when Bayer announced a deal to acquire Monsanto for $128 in a $66 billion deal. This deal ends several months of discussions between the two sides on a deal.

Weaknesses

- Energy was the worst performing sector for the week, falling by -2.91 percent versus an overall increase of 0.53 percent for the S&P 500.

- Range Resources was the worst performing stock for the week, falling -11.51 percent.

- Deutsche Bank had a disastrous day. The German bank saw its stock fall nearly 10 percent in trading on Friday after reports that the Department of Justice was going to settle with the company for $14 billion over financial crisis-era mortgage-backed securities.

Opportunities

- The iPhone 7 hits stores on Friday. Apple stores will open at 8am, earlier than usual, for the occasion. Additionally, Apple says it's sold out of the initial batch of iPhone 7 Plus. The phone is sold out in all colors, and while customers won't be able to get the phone Friday, when it is officially released, they will still be able to order it online, Reuters says. Analysts are tuned in to see how the upgraded phone model sales progress.

- Trivago is getting ready to go public. Expedia has chosen JP Morgan, Goldman Sachs and Morgan Stanley to coordinate the Nasdaq-based initial public offering for its travel search site, Trivago, Reuters reports.

- Some of the biggest hedge fund managers in the world presented their best ideas this week. Ray Dalio, Paul Singer, Jim Chanos and more presented at CNBC's Delivering Alpha conference. Their ideas included shorting Tesla (a long-time Chanos position) and going long the S&P 500.

Threats

- Technical analysis out of UBS published Wednesday indicates that at least for the month of September the stock market may have hit its highs. "With breakdown last Friday, we are changing our tactical bias towards a more cautious stance since we see the risk of an 8 percent to 10 percent correction into late October/early November, where we have our next bigger tactical low projection for a classic year end bounce/rally," the firm wrote.

- Americans are ditching giant chain restaurants. According to data from Bank of America Merrill Lynch, restaurant spending has risen at a slower pace over the last 18 months, though spending at large chains — as opposed to smaller chains or local restaurants — has borne the brunt of this decline. "We find that sales of the big chain restaurants, which make up 18 percent of the aggregate, have been decidedly slower than the rest of the composite," the firm writes. "This is indicative of a market shift away from large chain restaurants."

- Oracle missed on earnings. The software company reported earnings per share of $0.55 against expectations of $0.58 from analysts on Friday morning. The stock fell a bit more than 2.5 percent in trading.

September 13, 20165 Reasons Why Active Management Works |

September 12, 2016Look to Chindia for Gold’s Love Trade |

September 8, 2016Use This Tip to Help You Avoid Taxes Like the Top 1 Percent |

The Economy and Bond Market

Strengths

- The median household income in America increased for the first time since 2007. A report released by the U.S. Census Bureau on Tuesday showed that median real household income increased by 5.2 percent for all American families in 2015. This is the first increase since the financial crisis.

- Inflation came in higher than expected. The Consumer Price Index grew 0.2 percent from the prior month, higher than the 0.1 percent increase expected by economists. The biggest contributors to the gain were health care services and increased housing costs.

- Consumer confidence stayed steady, but disappointed. The University of Michigan's consumer confidence index stayed steady at 89.8, but fell short of economist's expectations of 90.6. Nonetheless, consumer confidence remains strong.

Weaknesses

- Retail sales fell more than expected. U.S. retail sales fell 0.3 percent in August according to the Commerce Department, more than the 0.1 percent decline forecast by economists. Consumers have become key to the U.S. economy, so the disappointing number is concerning.

- Fed rate hike odds keep sliding. The market is pricing in just an 18 percent chance the U.S. Federal Reserve will raise rates at its September meeting, according to data compiled by Bloomberg. Additionally, the market sees just a 49.7 percent probability of a Fed rate hike before the end of 2016.

- Industrial production slumped. Industrial production fell 0.4 percent in August, according to the Federal Reserve, coming in weaker than the 0.2 percent decline that economists had forecast.

Opportunities

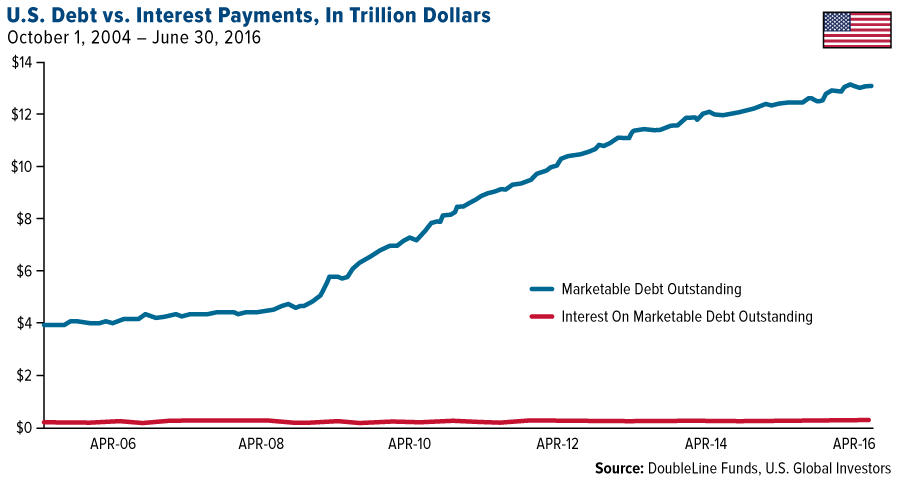

- According to Jeffrey Gundlach, political conditions are indicative of a pending surge in fiscal spending. Both leading candidates – Clinton and Trump – have advocated for large increases in federal spending on infrastructure projects. Such spending can be justified by data on the deficit and debt. The average interest rate paid by the federal government has been coming down since 2004. Debt has gone up “massively” since 2008, but interest payments have been frozen. Gundlach predicted that Americans will be shown versions of the chart below, as politicians attempt to justify the ability of the government to borrow as a means to support additional spending. Massive infrastructure spending would create jobs and stimulate the economy.

- China's economy got some good news. Industrial production, fixed-asset investment and retail sales all topped expectations..

- Apart from the Federal Open Market Committee (FOMC) meeting, important U.S. data releases include the National Association of Home Builders (NAHB) survey (Monday), housing starts (Tuesday), leading indicators (Thursday) and Manufacturing Purchasing Managers’ Index (PMI) (Friday). Positive signals from these indicators will greatly influence the market's rate hike expectations.

Threats

- The bond market is “sniffing out” an unfriendly change in the direction of interest rates, according to Jeffrey Gundlach. Rates are going up, he said, and investors should position their bond portfolios defensively for a long-term secular rise in rates.

- The International Energy Agency (IEA) says the oil glut will continue into 2017. “Global oil demand growth is slowing at a faster pace than initially predicted,” the IEA’s most recent oil report said, predicting that the oil glut would persist into at least the first half of 2017.

- Central bank meetings will take center stage next week. The Fed and the Bank of Japan will kick off proceedings early in the week followed by the Reserve Bank of New Zealand. Any unexpected policy moves could cause turmoil in markets.

Gold Market

This week spot gold closed at $1,310.11, down $17.82 per ounce, or 1.34 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, however, ended the week lower by 2.60 percent. Junior miners outperformed seniors for the week, as the S&P/TSX Venture Index fell 2.97 percent. The U.S. Trade-Weighted Dollar Index finished higher by 0.76 percent.

|

Date |

Event |

Survey |

Actual |

Prior |

|

Sep-16 |

CPI YoY |

1.0% |

1.1% |

0.8% |

|

Sep-20 |

Housing Starts |

1190k |

-- |

1211k |

|

Sep-21 |

FOMC Rate Decision |

0.50% |

-- |

0.50% |

|

Sep-22 |

Initial Jobless Claims |

260k |

-- |

260k |

Strengths

- The best-performing precious metal for the week was palladium, down slightly by 0.41 percent. In an overall down week for the precious metals sector, palladium remained flattish.

- Following the release of disappointing U.S. economic data Friday morning, which reduces the chance of a rate hike next week, gold rebounded from near two-week lows (although still on track for its first weekly loss in three), reports Reuters. “Once past the FOMC, gold may find a better environment to move higher,” said Michael Armbruster, principal and co-founder at Altavest. “In the big picture, even if the Fed raises rates twice more a total of 50 [basis points], real interest rates will remain negative—a very bullish environment for gold.”

- Copper posted the biggest gain in nearly three months, reports Bloomberg, as strong economic data from China fueled speculation that demand will strengthen in the country. Factory output, investment and retail sales all exceeded analyst estimates in the Asian nation. On the London Metals Exchange copper for delivery in three months rose 2.6 percent mid-week, the biggest increase since June 15, the article continues.

Weaknesses

- The worst-performing precious metal for the week was platinum, down 4.18 percent. According to Bloomberg, platinum experienced a seventh week of losses (the longest run since 2013). John Meyer, an analyst at SP Angel Corporate Finance LLP, says investors are losing interest in both platinum and palladium on concern that the popularity of electric cars, which use less platinum and palladium than gasoline-fueled cars, will cut into demand.

- Reports that U.S. inflation pressures are rising, with a rise in monthly inflation seeing its biggest jump since February, sent the U.S. dollar higher on Friday. Gold, which has an inverse relationship with the greenback, drifted lower on the news. “This continues the tennis match between bulls and bears, hawks and doves over whether or not the Fed will raise interest rates next week,” said Colin Cieszynski, chief market strategist at CMBC Markets.

- Although 2016 started with a bang for commodities, the year could end with a whimper, reports Bloomberg. The Bloomberg Commodity Index is heading for a third-quarter slump after posting consecutive gains for the first two periods, the article continues. Investors pulled $791 million out of ETFs tracking commodities over the past month and hedge funds have cut their combined wagers on a rally for raw materials in nine of the past 11 weeks.

Opportunities

- David Mazza, head of ETF and mutual fund research at State Street Global, doesn’t believe a rate hike in the U.S. will spoil investors’ appetite for gold, reports Bloomberg. “We’re still going to be in an environment where rates in the U.S. are still very low,” Mazza said. In fact, holdings in gold-backed ETFs are heading for a third quarterly gain, the longest streak since 2012, despite the rising odds of a rate increase, according to data compiled by Bloomberg.

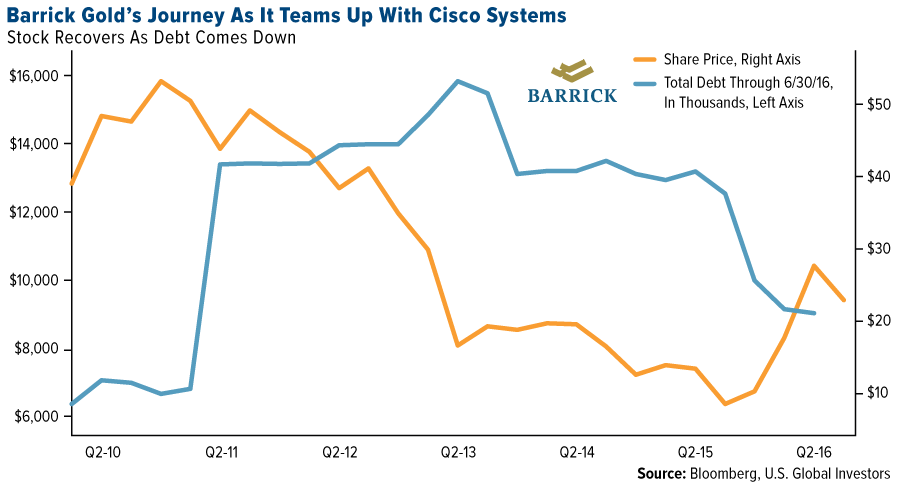

- Barrick Gold Corp. has turned to tech giant Cisco Systems Inc. to help digitize its global mining operations, reports Bloomberg. “We mean to create value and push the boundaries of our industry in entirely new ways,” Barrick Executive Chair John Thornton said. A flow of real-time data should help cut costs and wring additional value out of its existing mines. As seen in the chart below, Barrick’s debt is down 43 percent to $9 billion from a 2013 peak, with most of the heavy lifting done by Thornton, Bloomberg continues.

- Klondex Mines announced this week its decision to put its underground True North Gold Mine in Manitoba, Canada, back into full production, reports Mining.com. This will be Klondex’s third operational mine and President and CEO Paul Huet sees it delivering “significant value” to shareholders. The positive production decisions estimates annual production at True North at 45,000 to 65,000 ounces of gold.

Threats

- With the Federal Reserve’s interest rate decision due next week, some gold investors are getting a bit nervous, reports Bloomberg. Cohen & Steers Capital Management, for example, was overweight in the yellow metal until last week when it decided to pare its gold allocation. In fact, over the past week, investors pulled $698 million from SPDR Gold Shares (taking holdings to the lowest since June), the article continues.

- Barrick Gold Corp. announced temporary suspension of operations at its Veladero mine in Argentina on Thursday, pending further inspections of the mine’s heap leach area. A new spill was confirmed in the area, but Barrick reported that no solution from the damaged pipe had reached any water diversion channels or watercourses. The impacted area has now been remediated. The company does not expect the incident to have a material effect on its 2016 operating guidance for the mine.

- In South Africa, one of the biggest producers of gold, 60 mining deaths this year (through August) were reported, according to the Chamber of Mines, up 20 percent from the same period last year. Finding minerals is becoming more and more deadly in the country, reports Bloomberg. The annual tally is heading for its first increase in nine years, the biggest in at least two decades.

Energy and Natural Resources Market

Strengths

- Gasoline demand posted the strongest weekly increase for four months, VTB reports. Demand was up 4.2 percent in the past four weeks, an encouraging sign leading into the fourth quarter. Average gasoline demand in the past four weeks remains just 2.5 percent below the peak summer driving season and strong enough to minimize normal seasonal inventory growth.

- The best performing sector for the week was the S&P 500 Oil & Gas Refining & Marketing Index. The index rose 2.7 percent after weekly inventories showed gasoline demand rose at the highest rate in four months. The rally in gasoline pulled the 321 crack spread above its 200-day moving average.

- Tesoro Corp, a major U.S. refiner, was the best performing stock in the broader natural resource space for the week. The stock gained 3.6 percent for the week after crack spreads rebounded in response to weakening oil prices and rising gasoline demand.

Weaknesses

- Oil prices fell 5.8 percent to multi-week lows on Friday as rising Iranian exports and returning supplies from Libya and Nigeria fueled concerns that a global glut would persist. As Reuters reports, Libya has lifted force majeure at some of its main ports and is resuming oil exports, while ExxonMobil was making preparations to load a cargo of Qua Iboe crude from Nigeria, its first since it imposed force majeure in July.

- The worst performing sector for the week was the S&P/TSX Oil and Gas Exploration and Production Index. The index of Canadian producers dropped 5.7 percent for the week tracking the weakness in oil prices.

- The worst performing stock for the week in the broader natural resource space was Novolipetsk Steel PJSC. The Russian steelmaker dropped 11 percent as investors feared China’s output may place downward pressure on steel prices. China’s August steel production rose 2.4 percent, the strongest monthly increase in two years.

Opportunities

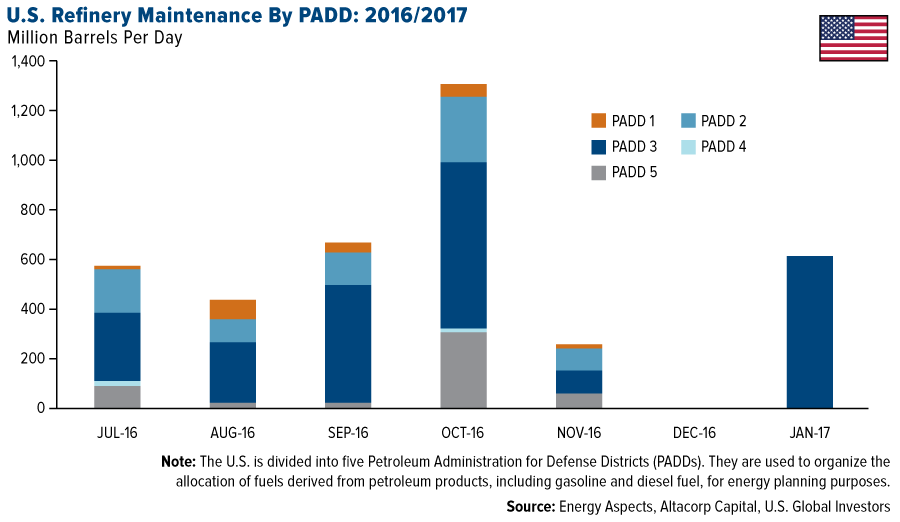

- The major refining maintenance season is likely to boost profit estimates for refiners. As Altacorp reports, with the driving season now over, we are heading into the fall refining maintenance season, with planned outages expected to increase to 1.3 million barrels per day in October. Goldman Sachs’ analysts expect margins to stay strong in September given these outages, adding that they expect upward pressure to consensus third-quarter earnings’ forecasts.

- A surprising inflation print may spur a new bid for gold. Consumer prices as measured by core inflation rose 2.3 percent in August over the last year, topping analysts’ expectations and sending real yields deeper into negative territory. The August reading is the highest since September 2008, and the tenth straight reading above the Fed’s 2 percent target.

- China August data beat expectations across the board. Industrial production rose 6.3 percent year-on-year in August, while retail sales also bested expectations with a growth of 10.6 percent. In addition, fixed asset investment, a proxy for longer-term spending, grew 8.1 percent year-on-year. With beats across industrial and consumer data, coupled with expansionary fiscal and monetary policies, Chinese demand may rebound into year end.

Threats

- The crude oil glut is likely to extend into late 2017, says the International Energy Agency lowering its demand forecasts. Consumption growth sagged to a two-year low in the third quarter as demand faltered in China and India, while record output from OPEC’s Gulf members is compounding the glut, according to the IEA. The group trimmed projections for global oil demand next year by 200,000 barrels a day and reduced growth estimates for this year by 100,000 barrels a day, citing a deceleration in China and India as well as weaker growth in developed economies.

- The met coal rally has left its first casualty; iron ore prices. A recent UBS report that its channel checks suggest higher steelmaking coal prices are pressuring steel mill margins, and in turn forcing cuts to iron ore prices. Moreover, industry operators are reportedly growing increasingly concerned about declining steel prices, as it suggests peak seasonal September/October demand is not holding up.

- The global iron ore surplus will continue to deteriorate and prices should correct, according to HSBC. With supply topping demand through at least 2019 on rising mine production in Australia, Brazil and India, prices are forecast to drop to $42 a metric ton next year and $41 in 2018, the bank said in a report. Iron ore for delivery in China was last at $56 a ton.

China Region

Strengths

- China’s economy is showing multiple signs of a rebound in August. Factory output, fixed-asset investment and retail sales all beat analysts’ expectations, coming in respectively up 6.3 percent year-over-year, 8.1 percent year-over-year, and 10.6 percent year-over-year. “The government should be comfortable with the figures,” Chief Economist at Australia & New Zealand Banking Group Raymond Yeung said, according to Bloomberg. “The PBOC can now focus on structural reforms such as interest rate liberalization and simply maintain an accommodative environment in the money market.”

- New yuan loans and aggregate financing (CNY) both came in higher than expected. New yuan loans came in at just under 949 billion for the August period, better than expectations of a gain of only 750 billion, and aggregate financing came in at 1.47 trillion yuan, up from July and well ahead of expectations for a reading of 900 billion.

- Parkson Retail Group Ltd. (3368 HK) jumped almost 30 percent this week after the Hong Kong-based department store operator agreed to sell its Beijing property for 1.67 billion yuan.

Weaknesses

- Unemployment in South Korea ticked up in August to 3.8 percent, missing analysts’ expectations for a steady print of 3.6 percent, which would have been in line with July’s reading.

- The South Korean city of Gyeongju suffered an earthquake (5.8 on the Richter scale) this week, with continuing aftershocks. Aftershocks of a different variety continue as the country continues its attempt to push the international community toward higher sanctions for North Korea, following the isolated nation’s nuclear test last week.

- Energy was the worst-performing sector in the Hang Seng Composite Index for the week, mirroring losses reflected in crude and other global indices, and falling 4.45 percent. Energy respectively edged out second- and third-worst-performing sectors, properties & construction and telecommunications.

Opportunities

- CLSA hosts its signature Investors’ Forum event in Hong Kong next week, providing investors with an opportunity to partake in unique insights into strategic issues in the region and globally.

- JPMorgan Chase’s asset management unit has chosen to focus on Shanghai’s free-trade zone for its China expansion, reports Bloomberg. The company set up China’s first wholly owned foreign money manager last month, providing the platform for the group’s future development in the Asian nation and becoming the parent for potential legal entities to be set up there. Country head Desiree Wang expects to see rising cross-border investment flows.

- China is rebalancing its economy away from labor-intensive production, reports Bloomberg, providing an opportunity for Indonesia to benefit. “Low wages give countries such as Indonesia an advantage in attracting investment,” said Shang-Jin Wei, chief economist at the ADB. “India, Bangladesh, and Indonesia all want to pick up some of the things that China will be leaving behind.”

- Ikea Group announced plans to accelerate its expansion in China and open its first store in India, reports Bloomberg. The furniture retailer has a revenue goal of 50 billion euros by 2020, and the expansion in China and India, could help Ikea achieve this target as sales growth stalls in Russia, the article continues.

Threats

- Philippine leader Rodrigo Duerte has vowed to end cooperation with the U.S. military, in both fighting terrorism and patrolling the South China Sea, reports Bloomberg. Now he’s moved to boost both economic and defense ties with China and Russia. “Duerte’s foreign policy may dramatically shift the geostrategic picture of the region, leaving China in an advantageous position versus the United States,” said Zhang Baohui, director of the Center for Asian Pacific Studies at Lingnan University in Hong Kong.

- Typhoon Meranti caused China to issue the highest storm warning as the storm made landfall this week, reports Bloomberg, leaving at least one dead and 38 injured in Taiwan. Another storm is heading toward Taiwan, according to Taiwan’s Central Weather Bureau. Financial markets in China are shut for the remainder of the week for the Mid-Autumn Festival holiday.

- Yuan loan rates in Hong Kong jumped the most in seven months on Monday, reports Bloomberg, highlighting concern over China’s equity market. According to Bocom International Holdings, higher funding costs will weigh on the nation’s shares as the PBOC seeks to squeeze bears betting against the yuan amid rising odds of a U.S. interest-rate increase, the article continues.

Emerging Europe

Strengths

- Ukraine was the best performing country this week, gaining 16 basis points. The International Monetary Fund (IMF) approved the release of a $1 billion loan tranche after a year’s delay. Ukraine is moving forward with reforms. A new system was implemented to monitor the income and asset declarations of public officials, but political uncertainty and a challenging reform agenda may delay future disbursements from the IMF.

- The Ukrainian hryvnia was the best performing currency this week, gaining 3.3 percent against the U.S. dollar. The Ukrainian stock exchange and the country’s currency were supported by the disbursement of IMF funds. Out of $17.5 billion pledged, $7.62 billion has been distributed. Also, this week the Ukraine government approved a budget for 2017, assuming 3 percent growth.

- The health care sector was the best performing sector among Eastern European markets this week.

Weaknesses

- Russia was the worst performing market this week, losing 2.3 percent. The Moscow stock exchange was pulled lower by a selloff in Brent crude oil, down 4.3 percent. As expected, the central bank of Russia lowered its benchmark rate by 50 basis points to 10 percent on the back of easing inflationary pressure. Governor Elvira Nabiullina commented that another decrease this year is extremely unlikely, but the rate cuts could continue next year.

- The Romanian lue was the worst performing currency this week, losing 77 basis points against the U.S. dollar. Industrial sales and industrial output for July came in much weaker, which may suggest weaker economic expansion.

- The telecommunication service sector was the worst performing sector among Eastern European markets this week.

Opportunities

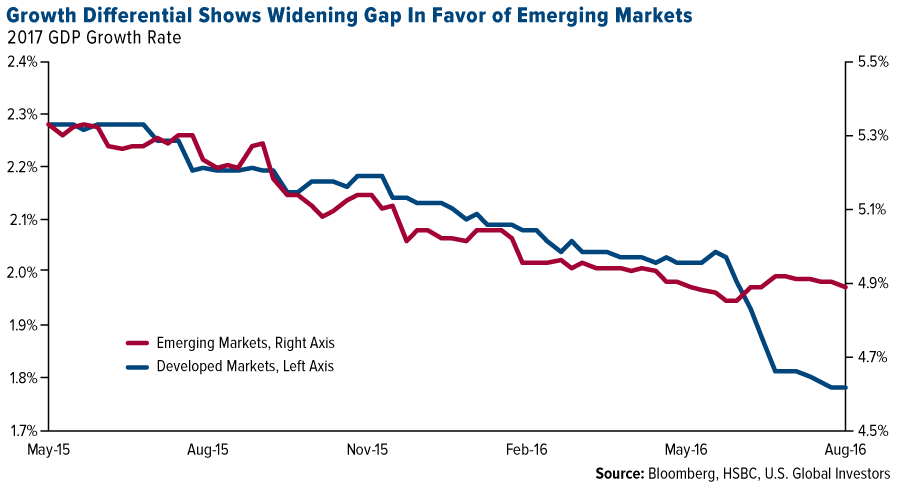

- HSBC’s global emerging market team expects the emerging market equity rally to continue, and they recommend to overweight Russia and Turkey. Leading indicators for EM growth continue to show ongoing stabilization/acceleration in the third quarter of 2016, thanks to improving domestic demand which is supported by previous rate cuts and helpful financial conditions. The chart below shows the widening gap in growth expectations in favor of emerging markets.

- According to Wood & Company, Greek banks are cheap and may present opportunity for investors who like higher risk combined with higher returns. The risk of new capital issues for the Greek banks is rather small and NPL coverage levels are currently some of the highest within the eurozone, despite the larger NLP stockpiles. Greek banks trade at a price-to-book value of 0.2 for 2016, at a discount of 50 percent for the South European banks, and nearly 80 percent discount to the emerging European banks. The average CET1 ratio among the banks that participated in the 2016 eurozone banking stress test was 12.5 percent, while the CET1 ratio for the Greek banks stood at 16.3 percent as of June 2016. The Greek banks are guiding for a profitable 2016.

- Emerging market yields continue to be attractive to investors looking beyond low and negative rates. Romania’s government is preparing to sell about 750 million euros in bonds to meet its 3 billion euro target for 2016. Romania’s yields declined along with other emerging markets as record low interest rates in developed nations drive investors towards more risky assets. At the beginning of the year government bonds due by 2025 were yielding 2.6 percent and are now about 1.7 percent, which is still an attractive positive yield compared to developed markets.

Threats

- Eurozone industrial production declined in July followed by the U.K.’s decision in June to leave the European Union. Industrial production declined by 1.1 percent month-over-month and 0.5 percent on a year-over-year basis. The largest declines were recorded by manufacturers of capital goods as investment spending slowed in the three months to June. The July drop in industrial output indicates that growth is weak and may put further pressure on the eurozone’s GDP.

- The EU agreed to increase spending on refugees. This will help manage migration flows, spur growth and cut funds destined for the least developed regions of the bloc. Eastern European countries will see a fall in 2017 payments by nearly 24 percent year-on-year. Hungary and Poland are the biggest beneficiaries of EU funds. According to Berenberg’s analysis, central emerging Europe countries (CEE4) receive around 2 to 2.5 percent of GDP worth of EU funds every year.

- Turkey’s Justice Ministry formally requested that the U.S. provisionally arrest Fethullah Gulen, who the government in Turkey claims is responsible for organizing the failed July 15 coup attempt. Tension between both countries may continue as Gulen lives in Pennsylvania, and Erdogan wants him to be prosecuted.

© US Global Investors