While prospects at the start of 2016 seemed rather dour for emerging markets, resilience has been the story in the asset class for the first half of the year. What’s behind the improvement in emerging-market equities? Here are some general themes I will briefly touch on:

- Growth in emerging markets continues to outpace that of developed markets

- Improved investor sentiment and attractive valuations have helped drive asset flows

- China’s market/economy hasn’t imploded as many had feared at the start of the year

- Political, economic and structural changes have been taking place in many markets

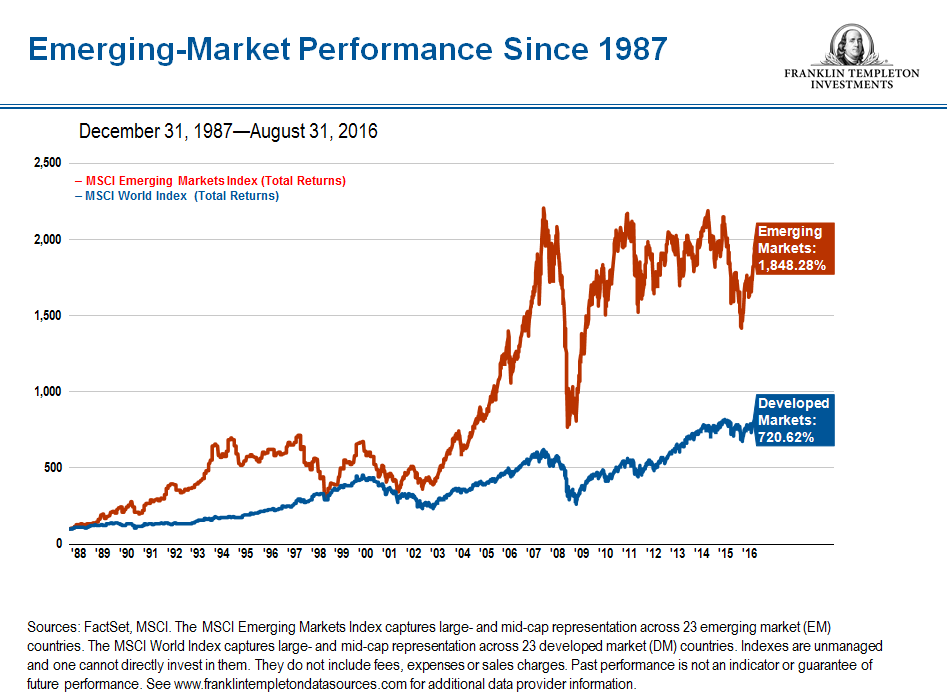

Year-to-date, emerging-market equities have outperformed developed markets in US dollar terms, with the MSCI Emerging Markets Index up 14.5%, while the MSCI World Index is up 2.7%.1 Growth rates in emerging markets also continue to outpace those of developed markets; the International Monetary Fund estimates gross domestic product growth of 1.8% in 2016 and 2017 for advanced economies, and growth of 4.1% and 4.6%, respectively, in emerging/developing economies.2 In August, Moody’s ratings agency revised its outlook on the world’s largest emerging-market economies upward for 2016 and 2017, with the expectation that these economies have stabilized.3

While the year is not yet over, we see brighter prospects for investors in emerging markets compared with last year, and the long-term performance of emerging-market equities compares favorably to that of developed markets.

The asset class received strong inflows this summer as investors continued to search for higher yields, helping to drive outperformance.4 A rebound in commodity prices this year led by oil has further shifted investor sentiment in favor of emerging-market equities. At the same time, many emerging-market countries have moved to lessen their dependence on commodities as drivers of growth and have diversified their economies into other areas, including information technology and other service-based sectors.

The US dollar has stabilized, and this has largely benefited emerging markets as it reduces the threat of a US dollar-denominated debt; many companies in emerging markets have issued debt in US dollars, making it harder to repay when their economies are weak at the same time the US dollar is very strong. In addition, given challenges surrounding the global economy, including the United Kingdom’s referendum vote to leave the European Union, several major central banks have taken a dovish stance on interest rates, which we think bodes positively for emerging markets’ growth and assets. At the same time, the US Federal Reserve (Fed) has been very cautious in terms of tightening this year. We think emerging markets should be able to weather small and gradual increases in US interest rates, which seems to be the path Fed policymakers have indicated.

In addition, many emerging-market countries are making meaningful progress on structural reforms to stimulate growth and their respective share markets. For example, India recently passed a national bankruptcy law, and a goods-and-services tax (GST) bill, and has relaxed foreign direct investment rules to further stimulate economic growth.

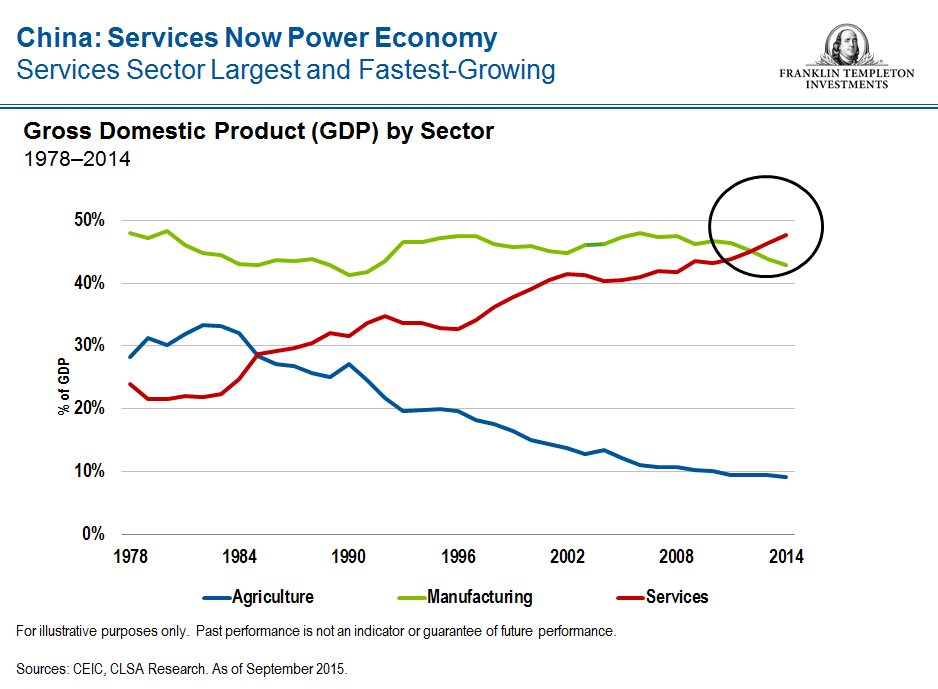

Perhaps the biggest catalyst of investor sentiment has been China. In 2015, events in China were a driver of a substantial sell-off that affected all emerging markets. The devaluation of China’s currency had prompted alarm bells among global investors on fears the weaker currency could ignite competitive currency volatility and potentially destabilize the economies of China’s neighbors. Weak economic data from China had added to the uncertain market mood, causing the Shanghai Composite Index to decline approximately 40% from its peak in mid-June of 2015. While China’s market has recovered a bit since then, undoubtedly, the Chinese economy still has many ailments, including an oversupply of housing, excess capacity in many industries, a slowing manufacturing sector and considerable debt issues. However, there are also many strengths fostered by China’s economic rebalancing, including growth in consumption driven by rising wages, an expanding services sector and new infrastructure initiatives launched by the central government.

So perhaps more importantly, signs of stability in China’s economy have been a key factor in boosting overall sentiment in emerging markets this year. Recently, Chinese authorities have taken a step forward in opening up domestic equity markets with the long-awaited approval of Shenzhen-Hong Kong Connect, which allows trading between mainland domestic shares (A shares) and the market in Hong Kong (H shares). Heavier southbound flows are to be expected as domestic Chinese investors are likely to try to reap the benefits of enhanced H-share liquidity and cheaper H-share valuations versus those of the domestic A-shares market. In our view, the fundamentals in China still look very good. The country remains one of the fastest-growing economies in the world despite a decelerated growth rate from decades past, and we remain confident in the government’s efforts to effect a broad economic rebalancing away from an export-driven model and toward one that is more domestic-oriented.

Elsewhere, Latin American equities have seen positive performances overall this year. Sentiment improved amid sweeping political changes and reform efforts in Brazil, culminating with the formal impeachment of former President Dilma Rousseff in August. Peru’s market has also benefited from business-friendly Pedro Pablo Kuczynski’s victory in the recent presidential election. In Argentina, a new government eliminated most capital controls and reached a deal with creditors.

These are just a few factors behind the resilience we have seen in emerging markets this year. We also see many positive long-term trends continuing, including favorable demographics and a rise in purchasing power and consumption in many of emerging economies—and the story is far from over. As such, we believe the long-term investment case for emerging markets remains positive. In our view, economic growth rates in emerging-market countries are likely to continue to outpace those of many developed-market economies, due to the reasons discussed. While emerging markets remain sensitive to macroeconomic indicators and global monetary policy—which means volatility is likely to persist for some time—equity markets appear to have begun to readjust. We see signs confidence is returning to emerging markets and believe it is likely to continue.

The comments, opinions and analyses expressed herein are personal views and are intended to be for informational purposes and general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. The information provided in this material is rendered as at publication date and may change without notice, and it is not intended as a complete analysis of every material fact regarding any country, region market or investment.

Important Legal Information

All investments involve risks, including the possible loss of principal. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions.

____________________________________________________

1 Source: MSCI, year-to-date through September 9, 2016. The MSCI Emerging Markets Index captures large- and mid-cap representation across 23 emerging market (EM) countries. The MSCI World Index captures large- and mid-cap representation across 23 developed market (DM) countries. Indexes are unmanaged, and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or a guarantee of future performance. See www.franklintempletondatasources.com for additional data provider information.

2 Source: IMF World Economic Outlook Update, July 2016. There is no assurance that any estimate, projection or forecast will be realized.

3 Source: Moody’s Investors Service announcement, August 17, 2016.

4 Past performance is not an indicator or a guarantee of future performance.

© Franklin Templeton Investments