Key Points

-

Conflicting comments by myriad Fed officials were blamed for Friday's rout; but one official's speech on Monday was credited with Monday's rebound.

-

It's human nature to find an explanation for every market move; but investor sentiment may have been the biggest factor.

-

Sighs of relief are natural; but a pick-up in volatility is likely here to stay for a while.

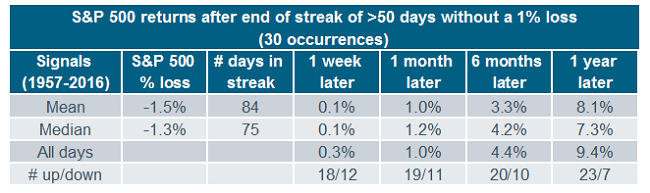

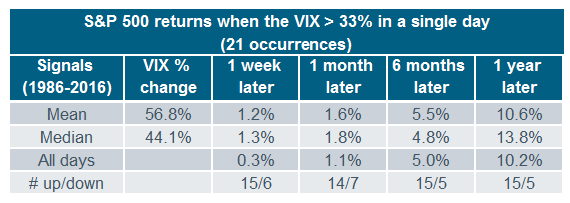

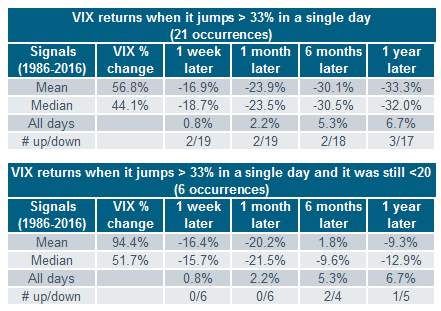

After a 51-day streak of days without the S&P 500 experiencing at least a 1% decline, the market hit a wall on Friday and was down 2.5% on a 40% jump in the volatility index (VIX). It was the worst single-day market decline since the aftermath of Britain’s vote to leave the European Union (Brexit) in June. But you lose some, you win some, and stocks staged an impressive 1.5% rebound on Monday.

Blame game

In terms of blame for Friday, fingers were pointed squarely at a variety of Federal Reserve officials. Conflicting comments from Federal Reserve Governor Daniel Tarullo and Boston Fed President Eric Rosengren likely contributed to investor skittishness. On Friday, Tarullo reiterated his caution about the economy and his dovish stance on rate increases. Rosengren suggested there was a reasonable case for a rate increase at the Fed meeting later this month. San Francisco Fed President John Williams, meanwhile, called for raising rates "sooner rather than later."

Outside the United States, the European Central Bank (ECB) opted last Thursday for no new easing moves and Japanese bond yields continued to rise. These two events sent a message to the markets that perhaps quantitative easing (QE) may have lost some efficacy and will not continue indefinitely.

And then there's Fed Governor Lael Brainard. She is being credited by some as contributing to both Friday's rout and Monday's rally. On Friday, there was a surprise announcement of the speech she gave on Monday. Having been considered a dove, some were worried her quickly setting up a speech a day prior to the Fed's quiet period suggested she was changing her tune. Instead she expressed concerns about the continued impact global stresses will have on the U.S. economy. Brainard mentioned that still-muted inflation and global uncertainty "counsels prudence in the removal of policy accommodation."

Third tantrum?

Many were worried Friday was setting up a third "tantrum"—the first being the "taper tantrum" in 2013, and the second being the tantrum which followed the Federal Reserve's initial rate hike last December. Monday's action eased those concerns…for now.

As you can see in the chart below, since the Fed's July meeting, expectations for a September rate hike have ranged from a low of 16% to a more recent high of 42% (settling in at 22% as of Monday's close). Unless the market begins to price in a higher likelihood of a rate hike in September, the Fed is unlikely to buck the market's expectations.

Source: Bloomberg, as of September 12, 2016.

Sentiment's setup

The media, more than most, persistently look for a narrative to explain every daily move in the market. It's rarely that simple. I believe the set up for the summer rally and this latest bout of weakness had as least as much to do with investor sentiment as it did with Fed policy uncertainty. In the immediate aftermath of the Brexit vote, investor pessimism hit historical extremes. Often at these extremes, not much of a catalyst is needed to boost stocks given the ample liquidity typically parked on the sidelines during an extreme phase of pessimism. That the world didn't immediately fall apart post-Brexit may have been all the market needed to launch its summer rally.

Fast-forward to the period leading into Friday's rout: sentiment had done an about-face and many measures had moved to extreme optimism. As I highlighted in my most recent report titled “All Summer Long,” complacency at best and frothy optimism at worst meant even a minor catalyst could trip up stocks. Whether Friday was it, it's too soon to tell; but I am keeping a close eye on sentiment conditions.