Look to Chindia for Gold’s Love Trade

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsA couple of weeks ago, I shared with you what I brought home from my trip to Toronto, Vancouver and New York City, where I had met with gold fund analysts. The current gold bull run began in January, but as I told you, the general retail investors weren’t buying then. The only people buying that early were quants and huge hedge funds. The question, then, was: What factors or models were the quants using to uncover gold’s meteoric rise this year?

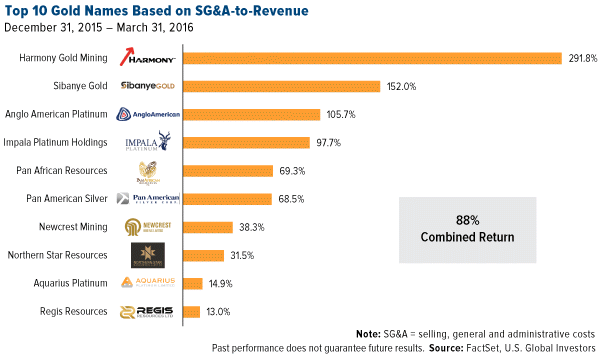

One of the factors they were looking at, I learned, was low SG&A-to-revenue. “SG&A” stands for “selling, general and administrative expenses” and refers to the daily operational costs of running a company that are not related to making a product. It includes everything from shipping fees to salaries to utilities. SG&A-to-revenue is an unusual factor, not typically used among analysts and fund managers, so we were curious to apply it.

Using this information, we looked just at the first quarter to find the mining companies that spent the least amount of money on these daily operations relative to revenue. Mining companies, after all, have had trouble with expense discipline.

What we discovered was nothing short of astonishing. All combined, the top 10 gold companies for the quarter—led by South Africa-based Harmony Gold—returned a spectacular 88 percent. That’s almost double what the Market Vectors Gold Miners ETF (GDX) returned over the same period (45.5 percent).

As early as January, the drivers were in place to fuel gold’s best first half of the year since 1974. The yellow metal is now in position to have its best year overall since 2010, when it rose 29.5 percent.

Upcoming Festivals Could Activate Love Trade

I talk a lot about the differences between gold’s Fear Trade and Love Trade. Loyal readers know that the Fear Trade is associated with negative real interest rates and excessive money supply, which triggers an imbalance of monetary and fiscal policies and macroeconomic uncertainty. Historically, investors in the U.S., Japan, Germany and the U.K. have been the main drivers of the global Fear Trade.

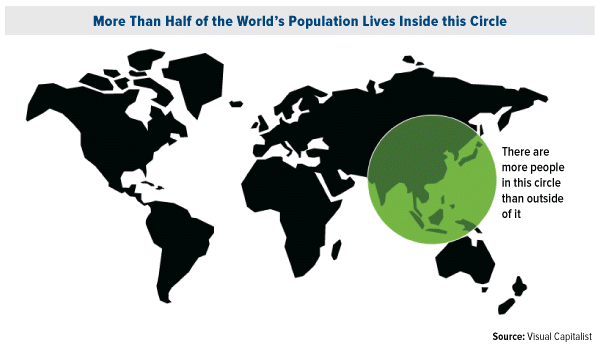

The Love Trade, on the other hand, is all about gold’s powerful allure and its timeless role as a gift without peer. It has two significant benefits: one, as beautiful gold jewelry to be worn, and two, as financial security. Although gold jewelry is often given as a special gift in Western countries, it pales in comparison to what takes place in China and India, or “Chindia”—home to about 40 percent of the world’s population, and the two largest gold importers.

The following image, courtesy of Visual Capitalist, shows emphatically just how enormous this region’s population is. More people live inside the green circle—which covers not just India and China but also Japan and some South China Sea countries—than outside it.

As I shared with you last month, the two Asian countries together accounted for more than half of total global gold jewelry demand in 2015. The U.S., by comparison, represented about 5 percent of demand. All of Europe, even less.

Significant to boosting the metal’s price are important cultural events, from India’s upcoming Diwali festival and fourth-quarter wedding season to the Chinese New Year in January. Going back decades, the yellow metal has tended to perform best in September, when jewelry, coin and bullion dealers restock their inventories in preparation for these celebrations.

Also known as the Festival of Lights, Diwali begins October 30 this year, followed by the wedding season. To give you a sense of scale, as many as 150 million Indian weddings will be held between 2011 and 2021, according to the Government of India. For each wedding, between 0.7 and 70 ounces of gold are typically purchased, which is equivalent to 35 percent to 40 percent of total wedding expenses.

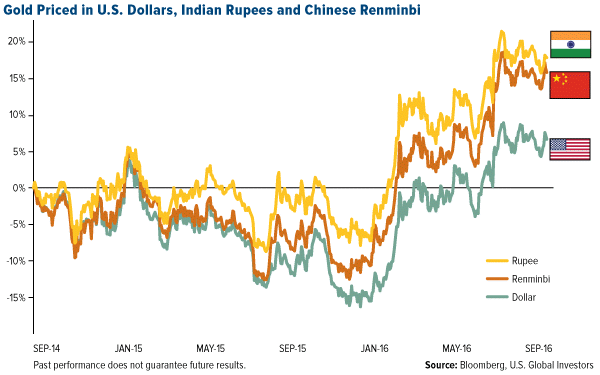

Of course, you can’t convert cash into gold if you don’t have the cash. What’s more, gold priced in Indian rupees and Chinese renminbi has really taken off, making it more expensive to Indian and Chinese consumers than America buyers.

Gold consumption, then, really depends on household income. Fortunately, income growth in Chindia is booming with the rise of the middle class.

Rising Incomes = Golden Opportunity

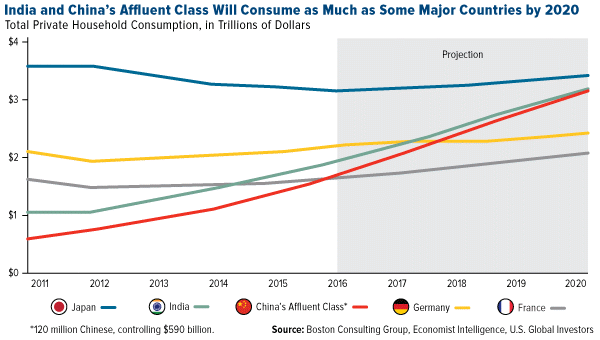

And just how much income growth are we talking about? According to Boston Consulting Group (BCG) data, consumer spending in both China and India will soon overtake spending in Germany and France, and is on a trajectory to match Japan’s level of consumption.

By 2020, the number of “affluent” households in China—those with annual incomes of at least $20,000—will grow to 280 million, equal to 30 percent of the country’s urban population. That’s quite a leap up from today’s 120 million households labeled as “affluent.” It’s also good news for the Love Trade.

As for India, the number of middle class consumers is expected to triple between now and 2025, eventually reaching 89 million people, according to McKinsey & Company.

What I find even more incredible is that by 2030, the economic output of India’s top five cities is expected to reach the size of five middle-income countries today, according to McKinsey. Mumbai’s massive $245 billion economy, for example, could soon exceed the entire country of Malaysia. Likewise, India’s capital city of New Delhi could one day be bigger than the Philippines.

This presents a huge opportunity for the Love Trade to expand even more, as rising incomes and economic momentum have been a tailwind for gold demand.

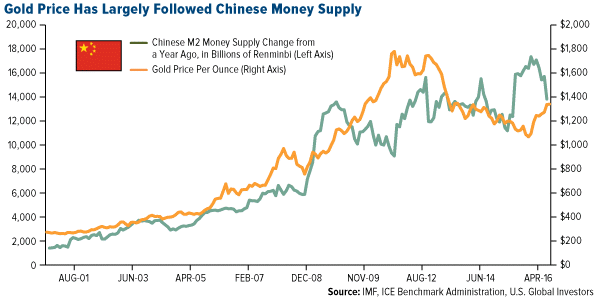

I’ve pointed out before the relationship between M2 money supply growth in China and the price of gold. Money supply isn’t the same as income growth, of course. But it serves as further evidence that the more money that’s available—and the more people who have access to that money—the more it can be converted into gold.

Negative real interest rates play an important role as well, as I’ve discussed many times before. The yellow metal shares an inverse relationship with real rates, which is what you get when you subtract inflation from nominal interest rates.

|

Speaking of which, many investors are wondering if rates will rise this year or not. December is still on the table, but the likelihood of a hike this month seems to have been doused by the August jobs report, which came in below expectations. CNBC reports that Goldman Sachs economists walked back their call for a September rate hike when it was revealed the U.S. economy added only 151,000 jobs, 32 percent fewer than the same month a year ago and a whopping 69 percent decrease from July’s payroll additions.

Be that as it may, markets seem to be betting the end of easy money could arrive sooner rather than later. Stocks sold off today in their worst session since June 24, the day after Brexit.

Last Friday, both gold and silver jumped on the underwhelming jobs numbers. As I told Daniela Cambone during this week’s Gold Game Film, which you can watch here, silver is an important metal to follow because as people develop more confidence in the precious metal area, silver could begin to take center stage.

India Now the Fastest Growing Large Economy

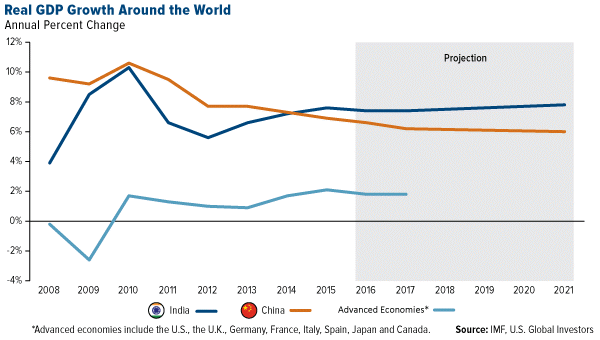

In June, I asked if India is the new China. I think the jury’s still out on that question, but what we do know is that India has pulled ahead of China to become the world’s fastest growing large economy. In its June update to its world economic outlook, the International Monetary Fund (IMF) sees India advancing 7.4 percent this year, compared to China’s 6.6 percent. On a relative basis, these are much stronger growth rates than what we find in advanced economies such as the U.S., European Union and Japan.

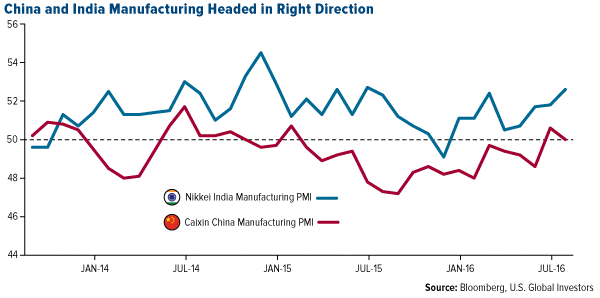

India’s manufacturing sector appears to be growing at a faster clip than China’s, when we compare the two Asian giants’ purchasing manager’s indices (PMI). For the month of August, the India PMI rose to 52.6 from 51.8 in July, indicating healthy sector expansion.

Meanwhile, China logged a neutral 50, indicating neither expansion nor contraction. But as you can see above, the trend is headed in the right direction and making steady improvements from its recent low of 47.2 in September 2015.

For the one-year period, the First Trust ISE Chindia Index Fund (FNI) is up more than 23 percent, as of September 4, suggesting the bad news we’ve been seeing in the media might be over, and the markets in China and India may have reached a bottom. This is good for global growth and the Love Trade.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 2.20 percent. The S&P 500 Stock Index fell 2.39 percent, while the Nasdaq Composite fell 2.36 percent. The Russell 2000 small capitalization index lost 2.61 percent this week.

- The Hang Seng Composite gained 3.85 percent this week; while Taiwan was up 1.97 percent and the KOSPI fell 0.02 percent.

- The 10-year Treasury bond yield rose 7 basis points to 1.68 percent.

Domestic Equity Market

Strengths

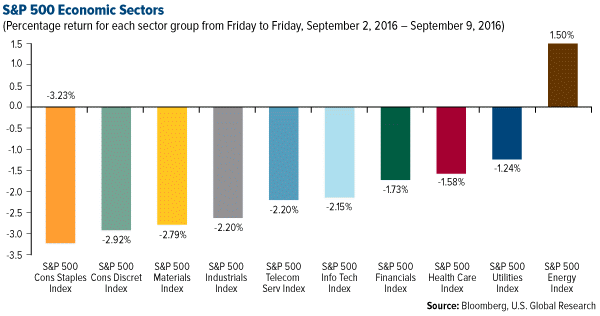

- Energy was the best performing sector for the week, increasing by 1.50 percent versus an overall decrease of -1.98 percent for the S&P 500.

- Chesapeake Energy was the best performing stock for the week, increasing 21.92 percent. It was a strong week for the energy markets, with talks about a Saudi/Russian cooperation and a large drawdown in stockpiles of crude helping spur price gains. Favorable market movements are helpful for Chesapeake, which has taken dramatic action recently to get its capital structure into better shape for the future.

- Hewlett-Packard Enterprise sold its software business. The $8.8 billion deal will give Micro Focus a 50.1 percent stake in the combined company and pay HPE shareholders $2.5 billion in cash.

Weaknesses

- Consumer staples was the worst performing sector for the week, falling by -3.23 percent versus an overall decrease of -1.98 percent for the S&P 500.

- Tractor Supply was the worst performing stock for the week, falling -18.63 percent. The specialty retail chain provided a disappointing business update ahead of its participation in the Goldman Sachs Annual Global Retailing Conference.

- Wells Fargo is paying a $185 million fine to settle a fraud case. The U.S.' largest bank by assets has reached the settlement with Los Angeles prosecutors after it allegedly opened more than 2 million fee-generating accounts that might not have been authorized, Reuters says.

Opportunities

- Liberty Media is buying Formula One for $4.4 billion. F1's biggest shareholder, CVC Capital Partners, and other shareholders, will still own 65 percent of Formula One stock, but have agreed to give up control to Liberty Media, Associated Press reports.

- Bill Ackman has taken a massive stake in Chipotle. Ackman's hedge fund, Pershing Square, disclosed a 9.9 percent stake in the fast casual burrito chain, saying in a 13D filing that the stock is "undervalued and is an attractive investment."

- Lego has a plan to revive U.S. sales growth. The world's largest toy maker says it is building a new plant in China and increasing production elsewhere in an effort to add production capacity to meet growing demand in North America.

Threats

- Elizabeth Warren, Bernie Sanders, and three other U.S. senators are going after Aetna for leaving Obamacare. The senators sent a letter to the company's CEO questioning the motives of the company in its decision to ditch 70 percent of its Affordable Care Act.

- Twitter's stock tanked while its board had a big meeting about the company's future. The stock was down over 6 percent in midday trading on Friday.

- The maker of EpiPen is being investigated for antitrust violations in New York. "A preliminary review by the Office of the Attorney General revealed that Mylan Pharmaceuticals may have inserted potentially

anticompetitive terms into its EpiPen sales contracts with numerous local school systems," New York Attorney General Eric Schneiderman's office said in a statement.

The Economy and Bond Market

Strengths

- Bank of America CEO Brian Moynihan has confidence in the American consumer. "The year-to-date consumers on our debit and credit cards are spending 4.7 percent more than they did last year and the pace is accelerating," he said in an interview with CNBC. "So, the consumer is in very good shape credit-quality wise, spending wise."

- European consumer spending revived in July. Retail sales in the eurozone jumped 1.1 percent in July and 2.9 percent on an annual basis. The solid showing in July pushed retail sales volumes above their prior 2008 peak.

- Initial jobless claims unexpectedly fell to 259,000. "The trend in the data looks pretty good, even though it is not as upbeat as some of the figures reported early in July," said Daniel Silver, an economist at JPMorgan.

Weaknesses

- The most important sector of the U.S. economy grew at its slowest pace in six years. The monthly non-manufacturing purchasing manager's index on the service sector came in at 51.4 for August. That's the lowest reading since February 2010, when the index pulled out of contractionary territory for good following the Great Recession.

- The European Central Bank made no changes to its policy mix, defying market expectations that the ECB Governing Council would extend its bond buying program beyond its scheduled end date in March 2017. Sovereign yields rose broadly after the ECB’s inaction, since a flood of global liquidity has helped boost markets globally. Treasuries were hit hard.

- Euro-area second-quarter GDP grew at 0.3 percent, down from the 0.5 percent that was recorded in the first quarter.

Opportunities

- Consumer confidence is at cyclical highs and incomes/jobs are still growing, albeit somewhat modestly. Furthermore, the wealth effect from residential real estate has been steadily positive for the past few years. This bodes well for consumer spending. U.S. retail sales data are reported on Thursday September 15.

- Key events in the U.S. will begin with Fed Governor Brainard's speech on the economic outlookon Monday. This will be the last, high-level Fed official commenting on the economy ahead of the next FOMC meeting.

- The German ZEW for September (Tuesday) will provide a timely update on the European economy.

Threats

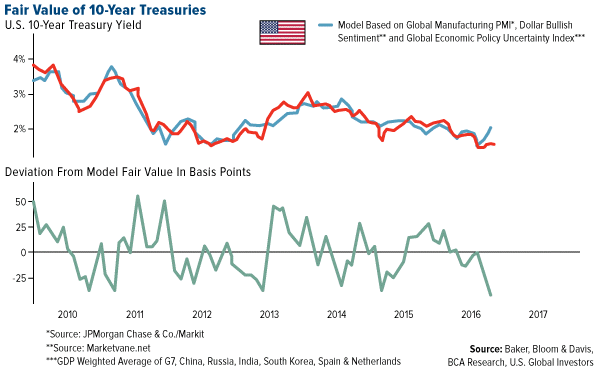

- According to BCA, while the 10-year Treasury yield is in the upper half of the group’s fair value range, it is too low relative to a model based on the global PMI, U.S. dollar sentiment and global policy uncertainty. BCA notes the model has performed reasonably well at tracking changes in the 10-year Treasury yield since 2010 and it currently pegs the fair value at 2.0 percent. BCA’s U.S. bond strategists expect rising expectations of a December Fed rate hike to send the 10-year yield close to the upper end of their fair value range, which is currently 1.88 percent. This would be more consistent with their global PMI model. As such, they maintain a tactical below benchmark duration stance.

- Jeff Gundlach is "defensive on bonds." During his quarterly webcast, Gundlach said he believes interest rates have bottomed and that corporate bonds are "highly overvalued."

- Larry Summers thinks Janet Yellen made a call that could tarnish her legacy at the Fed. "My second reason for disappointment in Jackson Hole was that Federal Reserve Board Chair Janet Yellen, while very thoughtful and analytic, was too complacent to conclude that 'even if average interest rates remain lower than in the past, I believe that monetary policy will, under most conditions, be able to respond effectively.' This statement may rank with former Fed Chairman Ben Bernanke's unfortunate observation that subprime problems would be easily contained," he wrote in a Washington Post piece.

Gold Market

This week spot gold closed at $1,327.93, up $2.86 per ounce, or 0.22 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, however, ended the week lower by 2.67 percent. Junior miners outperformed seniors for the week, as the S&P/TSX Venture Index rose 0.15 percent. The U.S. Trade-Weighted Dollar Index finished lower by 0.52 percent.

|

Date |

Event |

Survey |

Actual |

Prior |

|

Sep-8 |

ECB Main Refinancing Rate |

0.000% |

0.000% |

0.000% |

|

Sep-8 |

U.S. Initial Jobless Claims |

265k |

259k |

263k |

|

Sep-12 |

China Retail Sales YoY |

10.2% |

-- |

10.2% |

|

Sep-13 |

Germany CIP YoY |

0.4% |

-- |

0.4% |

|

Sep-13 |

Germany ZEW Survey Current Situation |

56.0 |

-- |

57.6 |

|

Sep-13 |

Germany ZEW Survey Expectations |

2.5 |

-- |

0.5 |

|

Sep-15 |

Eurozone CPI Core YoY |

0.8% |

-- |

0.8% |

|

Sep-15 |

U.S. Initial Jobless Claims |

265k |

-- |

259k |

|

Sep-15 |

U.S. PPI Final Demand YoY |

0.1% |

-- |

-0.2% |

|

Sep-16 |

U.S. CPI YoY |

1.0% |

-- |

0.8% |

Strengths

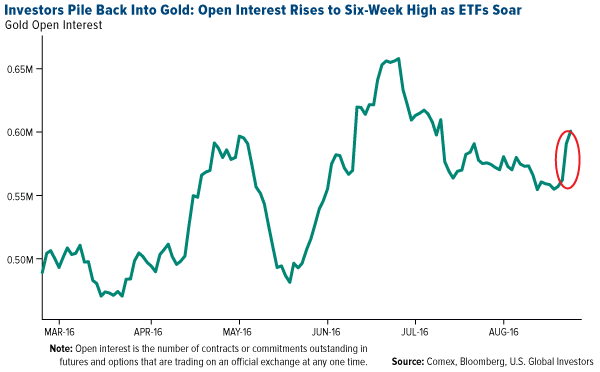

- The best performing precious metal for the week was gold, up 0.22 percent. According to Bloomberg, gold traders and analysts were bullish for the first time in three weeks on the back of the Federal Reserve outlook. In fact, holdings in ETFs backed by the metal climbed by 13.8 metric tons in the first two days of the week, as seen in the chart below.

- On the back of Friday’s jobs numbers, gold and silver have reversed back to the upside and the sector has new buy signals in daily momentum gauges, reports Bloomberg. Stocks related to both gold and silver remain the best area for “new money right now,” according to BMO analyst Russ Visch. BullionVault’s Gold Investor Index agrees with Visch’s analysis—the gauge measuring the balance of client buyers against sellers rose to 56 versus 53.4 in July.

- Pure Gold Mining reported a drill intersect of 50.2 grams per tonne over four meters at its McVeigh Horizon, Madsen Gold Project this week. In addition, mineralization is now extended to a vertical depth of 370 meters. The four drill rig exploration program is designed to expand the high-grade gold resource in close proximity to the existing permitted infrastructure, the company reported.

Weaknesses

- Silver was the worst performing precious metal for the week, down 2.03 percent. Precious metals showed signs of slowing a recent advance, with silver halting a five-day winning streak, reports Bloomberg, and gold trading little changed after the biggest advance since June.

- One of the top gold forecasters, ABN Amro, cut its outlook for gold prices at year-end, reports Bloomberg. The bank lowered its price forecast to $1,325 per ounce compared to a previous estimate of $1,350 per ounce. “We had expected a larger Brexit fallout on financial markets reflected in negative investor sentiment,” ABN Amro analyst Georgette Boele said.

- Gold imports by India slumped in August to the lowest level in five months, reports Bloomberg, as increasing prices reduced spending on the yellow metal. Inbound shipments slumped 85 percent to 21.6 metric tons from a year ago, the article continues, but foreign purchases could recover this month due to festival season.

Opportunities

- Andrew Quail of Goldman Sachs notes that over the past two years, gold miners have adapted well to the new gold price environment. He says companies have executed on the “shrink to profitability” strategy by: 1) lowering operating costs, 2) reducing financial leverage and 3) prudently allocating scarce capital resources. So what now? Quail says the next steps include a focus on productivity, growth and dividends.

- ICBC Standard Bank sees gold rising above $1,400 an ounce in the coming weeks, reports Bloomberg. “There is little prospect that the U.S. Fed will raise rates in September, and most likely not in December either,” the bank said in an email on Thursday.

- The Federal Reserve Bank of Atlanta publishes a special inflation index called, in the words of MarketExclusive.com’s Rafi Farber, the “Sticky-Price CPI.” This index measures prices for goods and services that do not normally experience wild swings. Currently this index is at the highest level since April 2009, which, according to Farber, has “big implications for gold and especially gold mining stocks” because gold usually rises quickly when inflation fears become mainstream. The Sticky-Price CPO has been trending up since 2009, while the flexible CPI has been negative since October 2014. If inflation starts to become obvious—and, according to the Sticky-Price CPI, this could happen soon—Farber writes that “any upside revaluation in the price of gold is likely to be quick and intense.”

Threats

- According to a recent note from BCA Research, the recent “Fedspeak” has hinted strongly at a rate hike later this year. Although a September rate hike is still a possibility, the note goes on to point out the recent batch of disappointing U.S. economic data, combined with lackluster inflation readings and election uncertainty—all suggesting that a December hike is more probable.

- According to the National Australia Bank, the outlook for gold is “mildly bearish” over the rest of 2016. The bank states that central to this outlook are assumptions that the Fed will lift rates in December by 25 basis points and Hillary Clinton will win the U.S. presidential election, reports Bloomberg. The European Central Bank (ECB) can also have an effect on the yellow metal, according to gold traders this week, who saw bullion swing between gains and losses. Investors and traders assessed the outlook for economic stimulus after the ECB president said officials will look at redesigning the quantitative easing program. With no new measures being announced, gold languished for the rest of the week.

- New Gold underperformed as much as 7.6 percent in Canada this week, lagging its gold peers, reports Bloomberg. The drop came after Rainy River capex rose “yet again” by $105 million along with a downgrade of New Gold by Canaccord to hold versus buy. Earlier reports by management have suggested capital requirements would rise by just $35 million due to the need to redesign the tailing containment structures.

Energy and Natural Resources Market

Strengths

- China commodity imports surprised to the upside in August, and signal an increasingly positive outlook according VTB Capital. Headline trade data for August surprised to the upside with imports up 1.5 percent year-on-year, the first such increase since October 2014. Oil, iron ore and coal imports were particularly strong, posting double-digit growth rates as a result of tight domestic availability.

- The best performing sector for the week was the S&P 500 Oil & Gas Exploration and Production Index. The index rose 2.6 percent after crude oil rallied on news that inventories declined by 14 million barrels last week, the largest weekly draw since 1998. Crude production and imports were affected last week as tropical storm Hermine made its way through the Gulf of Mexico.

- South32 Ltd, an Australian major diversified miner was the best performing stock in the broader natural resource space for the week. The stock gained 12.1 percent for the week after coking coal prices rallied to $180 per tonne as a result of tight domestic availability in China.

Weaknesses

- The U.S. dollar continues to recover, hurting commodity prices. The currency cruised back above its 100-day moving average this week as September Fed rate hike odds leapt in spite of weaker U.S. macro data. A number of Fed speakers have appeared more “hawkish” on their public interventions over the last week, suggesting the Fed may want to prepare the market for a hike despite weakening jobs, ISM, and inventory data. As a result, the U.S. dollar regained most of its recent loses, hurting gold, crude and industrial metals in the process.

- The worst performing sector for the week was the S&P 500 Construction Materials Index. The index dropped 5.5 percent for the week as weaker macro data in the U.S. and increasing expectations for a Fed rate hike negatively impacted housing and infrastructure-related stocks.

- The worst performing stock for the week in the broader natural resource space was Vale SA. The major Brazilian miner dropped 7.3 percent as iron ore prices dropped to 11-week lows on news that Australian exports reached record highs in August.

Opportunities

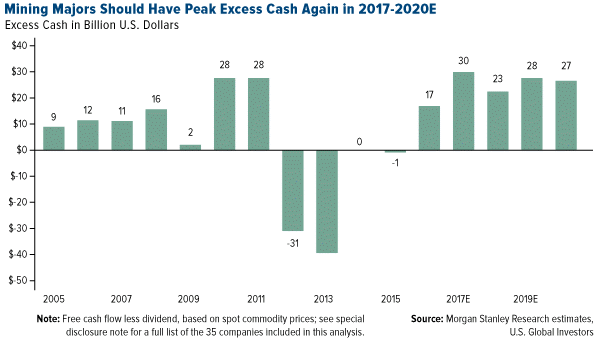

- Major miners should see peak excess cash flows in 2017-2020, according to Morgan Stanley. The bank’s Metals & Mining team shows that at current spot commodity prices, miners’ post-dividend cash flows are on track to be positive in 2016 for the first time in 4 years. By 2019-2020, excess cash will be approaching peak levels of $25-30 billion, implying considerable firepower to increase dividends.

- China may boost fiscal spending to support growth. A recent Chinese State Council meeting held by Premier Li gave a more pro-growth tone with a pledge to enforce more active fiscal policy in China, reports Macquarie. A focus on infrastructure investment was disclosed, with banks being encouraged to increase credit support to investment projects. Already this week, the State Council approved two new civil airports in Jingzhou, Hubei and Chenzhou, Hunan, with investments expected to exceed RMB3.1 billion.

- Investors continue to ignore a looming crisis for oil, according to HSBC. In a recent report, the bank’s analysts argue that the oil glut could soon turn into a largely undersupplied market given the natural decline rates and lack of investment. Among the reasons to substantiate their view, the analysts highlighted that 81 percent of the production of liquid oil is already in decline, while the amount of new oil discoveries was just 5 percent, a record low, and insufficient to replace current declines.

Threats

- Chinese refiners slashing capacity could collapse global oil demand. As reported by Zero Hedge and Bloomberg, refining by China's smaller, "teapot" refiners, may see a steep decline. The reason is that the government is leading a tax crackdown on non-compliant “teapots,” which threatens to constrain this new source of demand from China. At stake are a whopping 1.4 million barrels per day in teapot demand.

- The breathtaking rally in seaborne coal prices may be about to end. Credit Suisse reports that the Chinese government on Thursday agreed to loosen coal production controls that have been in place since the end of March and which have almost single-handedly driven international coal markets higher. The measures are incrementally bearish for seaborne prices as large excess capacity in China may now come back into the market.

- Iron ore prices dropped to 11-week lows as Australian exports climb to record. Bloomberg data shows iron ore shipments from the world’s largest bulk-export terminal in Australia swelled to a record, suggesting strong supply may drive prices lower through year-end.

China Region

Strengths

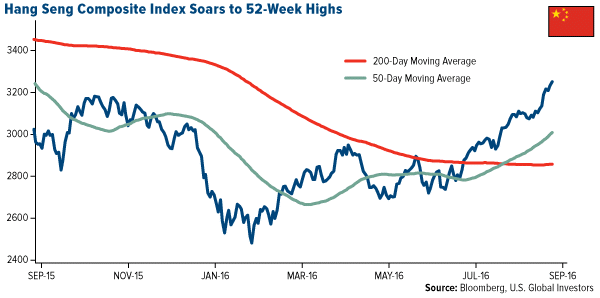

- The Hang Seng Composite Index rose 3.65 percent this week to new year-to-date highs and 52-week highs.

- The Nikkei Singapore Purchasing Manager’s Index (PMI) reading for August rebounded to 52.3 from July’s reading of 50.7

- Year-over-year imports in China rose 1.5 percent for the August period, up from July’s drop of 12.5 percent, marking the first rise in domestic demand in nearly two years. The news comes as Caixin’s China Services PMI also rebounded slightly from a July print of 51.7 to 52.1 for August.

Weaknesses

- While China’s foreign reserves number didn’t come in greatly changed, the August reading of $3.185 trillion nonetheless slightly missed expectations and marks the lowest levels in years. The weaker number may also add credibility to the notion that the People’s Bank of China had been intervening in the market to prevent a weaker yuan ahead of last weekend’s Hangzhou G-20 meeting.

- Thailand’s SET Index tumbled just over 5 percent for the week, underperforming its peers as the baht weakened during a week full of central bank speakers and speculation.

- Malaysia’s year-over-year Industrial Production reading for the July period missed expectations, coming in at 4.1 percent, shy of the 4.5 percent analysts were looking for. The reading marks a drop from a June bounce up to 5.3 percent.

Opportunities

- Passenger vehicle sales in China rose for another consecutive month, as data for the August period reflect a jump of 24.5 percent to 1.8 million units.

- The Nikkei Hong Kong PMI reading for August jumped from a previous print of 47.2 to 49.0, still in contractionary territory but nonetheless at a one-year high, even as Hong Kong shares continue to rebound.

- The China Insurance Regulatory Commission has permitted mainland insurance funds to purchase Hong Kong equities through Shanghai, broadening the potential base of Hong Kong investors and adding additional liquidity to the Hong Kong market.

Threats

- Following the G-20 summit in Hangzhou, and despite what may have been the PBOC’s attempts to stem the weakening of the yuan, capital outflows and renminbi stability remain concerns for China investors. The Hong Kong Interbank Offered Rate (HIBOR) rose this week to multi-month highs, fueling speculation that the PBOC has been intervening to make shorting the yuan more difficult.

- Supply chain concerns continue over South Korean shipper Hanjin Shipping Co.’s vessels, assets and future.

- North Korea conducted another nuclear test this week—its second such test this year—drawing criticism from global leaders, particularly officials in South Korea and the United States. Global leaders once again are left to hope that China—far and away North Korea’s primary and most influential trading partner and ally—will help coax Pyongyang back to broader talks.

Emerging Europe

Strengths

- Russia was the best performing country this week, gaining 1.2 percent. According to the Bank of Russia, inflationary expectations declined substantially in August and lower inflation readings may allow the bank to continue cutting its key rate. A rate decision will be made next week, and Bloomberg’s economists predict a cut of 50 basis points from 10.5 to 10 percent. Brent crude oil gained 2.6 percent.

- The Polish zloty was the best performing currency this week, gaining 1.2 percent against the U.S. dollar. The Central Bank of Poland held its benchmark rate unchanged at a record low 1.5 percent despite deflation being stretched into a third year and economic growth missing forecasts last quarter. Most emerging Europe currencies strengthened after weaker U.S. job data was reported last Friday and prospects of a rate hike in September decreased.

- The health care sector was the best performing sector among Eastern European markets this week.

Weaknesses

- Greece was the worst performing market this week, losing 2.6 percent. The country is due to receive another 2.8 billion euros from the 10.3 billion euro tranche of loans, linked to the successful conclusion of the first review. There have been delays in the process of implementation reforms needed in order for the country to receive additional financial aid from the eurozone.

- The Turkish lira was the worst performing currency this week, losing 60 basis points against the U.S. dollar. Turkish economic growth slowed to 3.1 percent in the second quarter from 4.7 percent in the first quarter on a year-over-year basis. Turkey’s Deputy Prime Minister commented that more economic reforms need to be implemented in order to achieve higher growth.

- The industrial sector was the worst performing sector among Eastern European markets this week.

Opportunities

- Turkey’s central bank lowered its reserve requirement for banks for the third time since July’s attempted coup in order to boost liquidity. The bank also reduced the amount that foreign-exchange and gold lenders must keep as collateral for liabilities.

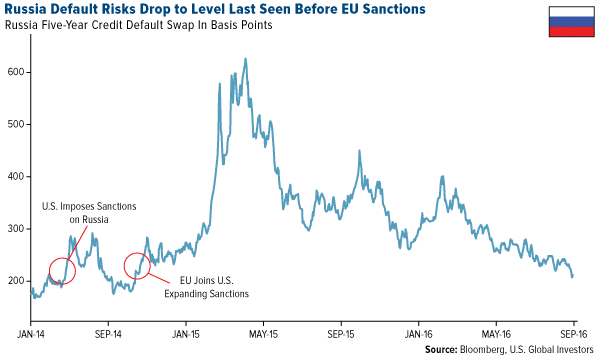

- The cost of insuring Russian debt against default has dropped to levels last seen in July 2014, when the European Union put sanctions on the country for its role in the Ukrainian crisis. Credit default swaps rose in the middle of August this year when Vladimir Putin threatened to respond to what he called “terrorist” tactics by Ukraine. But as his warnings ended and fighting in eastern Ukraine abated, the risk premium fell.

- The Central Bank of the Czech Republic has prevented the koruna from strengthening beyond 27 to the euro since 2013, in order to lift inflation after it cut rates to 0.05 percent in 2012. There are speculations that the central bank may lift the cap on the currency in the second half of 2017. Ceska Sporitelna analysts Jana Urbankova and Roman Sedmera expect capital inflow to intensify through year-end and the central bank will step into the market more vigorously.

Threats

- The European Central Bank left the main refinancing rate at zero, the deposit rate at minus 0.4 percent and asset purchases at 80 billion euros ($90 billion) a month. No additional stimulus was provided to revive the eurozone economy.

- The EU extended part of its sanctions against Russia over Moscow’s annexation of Crimea and its role in the crisis in Ukraine. The EU’s travel bans and asset freezes, which were due to expire on September 15, were extended for six months and cover some 150 people and 37 entities. The U.S. government has expanded its sanctions over Russia’s leading electronics producers. The restrictions introduced by the U.S. might affect possible imports of the U.S. companies’ machinery and technologies.

- The state election in Germany shows that Merkel is falling out of favor. For the first time in post-war history, Merkel’s Christian Democrats finished behind a populist challenger in a state election. Alternative for Germany, a 3-year-old, anti-immigration party defeated the Christian Democratic Union in the German chancellor’s home state. Angela Merkel admitted that the immigration policy hurt party elections. Germany took in more than 1 million refugees in 2015, making it the most open country in Europe to asylum seekers.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| DJIA | 18,085.45 | -406.51 | -2.20% |

| S&P 500 | 2,127.81 | -52.17 | -2.39% |

| S&P Energy | 511.68 | +3.33 | +0.66% |

| S&P Basic Materials | 296.85 | -11.04 | -3.59% |

| Nasdaq | 5,125.91 | -123.99 | -2.36% |

| Russell 2000 | 1,219.21 | -32.62 | -2.61% |

| Hang Seng Composite Index | 3,249.17 | +114.36 | +3.65% |

| Korean KOSPI Index | 2,037.87 | -0.44 | -0.02% |

| S&P/TSX Global Gold Index | 235.81 | -7.68 | -3.15% |

| XAU | 93.46 | -3.17 | -3.28% |

| Gold Futures | 1,331.40 | +4.70 | +0.35% |

| Oil Futures | 45.70 | +1.26 | +2.84% |

| Natural Gas Futures | 2.79 | +0.00 | +0.07% |

| 10-Yr Treasury Bond | 1.68 | +0.07 | +4.55% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| DJIA | 18,085.45 | -410.21 | -2.22% |

| S&P 500 | 2,127.81 | -47.68 | -2.19% |

| S&P Energy | 511.68 | +13.30 | +2.67% |

| S&P Basic Materials | 296.85 | -8.47 | -2.77% |

| Nasdaq | 5,125.91 | -78.68 | -1.51% |

| Russell 2000 | 1,219.21 | -4.07 | -0.33% |

| Hang Seng Composite Index | 3,249.17 | +217.18 | +7.16% |

| Korean KOSPI Index | 2,037.87 | -6.77 | -0.33% |

| S&P/TSX Global Gold Index | 235.81 | -43.84 | -15.68% |

| XAU | 93.46 | -19.27 | -17.09% |

| Gold Futures | 1,331.40 | -20.50 | -1.52% |

| Oil Futures | 45.70 | +3.99 | +9.57% |

| Natural Gas Futures | 2.79 | +0.23 | +9.10% |

| 10-Yr Treasury Bond | 1.68 | +0.17 | +11.14% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| DJIA | 18,085.45 | +220.11 | +1.23% |

| S&P 500 | 2,127.81 | +31.74 | +1.51% |

| S&P Energy | 511.68 | +10.53 | +2.10% |

| S&P Basic Materials | 296.85 | -2.36 | -0.79% |

| Nasdaq | 5,125.91 | +231.36 | +4.73% |

| Russell 2000 | 1,219.21 | +55.28 | +4.75% |

| Hang Seng Composite Index | 3,249.17 | +409.69 | +14.43% |

| Korean KOSPI Index | 2,037.87 | +20.24 | +1.00% |

| S&P/TSX Global Gold Index | 235.81 | +4.05 | +1.75% |

| XAU | 93.46 | +3.07 | +3.40% |

| Gold Futures | 1,331.40 | +49.50 | +3.86% |

| Oil Futures | 45.70 | -3.37 | -6.87% |

| Natural Gas Futures | 2.79 | +0.24 | +9.31% |

| 10-Yr Treasury Bond | 1.68 | +0.04 | +2.13% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of 06/30/2016:

BHP Billiton Ltd

Freeport McMoRan Inc.

Glencore PLC

Lundin Mining Corp

NewGold

Norsk Hydro ASA

Northern Star Resources

Pure Gold Mining

Randgold Resources Ltd.

Regis Resources

Sibanye Gold Ltd

Tractor Supply Co.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.

The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months.

The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.

The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500.

The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500.

The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500.

The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500.

The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500.

The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500.

The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The 35 miners included in the sample and analysis used for the Energy and Natural Resources chart are: Anglo American Plc, BHP Billiton, Glencore PLC, Rio Tinto PLC, Acacia Mining PLC, Antofagasta PLC, Aurubis AG, Boliden AB, CENTAMIN PLC, Eramet SA, Fresnillo PLC, Hochschild Mining PLC, KAZ Minerals PLC, Lundin Mining Corp, Norsk Hydro ASA, Nyrstar NV, Randgold Resources Ltd, China Coal, Coal India, Exxaro, Impats, Jiangxi Copper, SCCO, Shenhua, Vale, Yanzhou Coal, Zijin, Freeport, Teck Resources, South32, Fortescue, Newcrest, Anglo Gold, Gold Fields, Sibanye Gold.

Free Cash Flow (FCF) represents the cash that a company is able to generate after laying out the money required to maintain or expand its asset base.

The Caixin China Manufacturing PMI, released by Markit Economics, is based on data compiled from monthly replies to questionnaires sent to purchasing executives in over 400 private manufacturing sector companies.

The Nikkei India Manufacturing Purchasing Managers’ Index, reported by Markit Economics, measures the performance of the manufacturing sector and is derived from a survey of 500 manufacturing companies.

A basis point, or bp, is a common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01% (0.0001).

The S&P 500 Construction Materials Index is a capitalization-weighted index that tracks the companies in the construction materials industry as a subset of the S&P 500.

The S&P 500 Oil & Gas Exploration & Production Index is a capitalization-weighted Index. The index is comprised of six stocks whose primary function is exploring for natural gas and oil resources on land or at sea.

The ISM New Orders Index is prepared by the Institute of Supply Management and is an indicator of the levels of new orders from customers.

ZEW Germany Expectation of Economic Growth is a survey on the question of economic growth in six months.

The Bullion Vault Gold Investor Index provides a unique window on private-investing sentiment in physical bullion. Using proprietary data from BullionVault, the 24-hour precious metals exchange online, the series show the balance of net buyers over net sellers across the month as a proportion of all owners at the start, rebased to 50.

The Caixin China Services PMI is a composite indicator designed to provide an overall view of activity in the manufacturing sector and acts as an leading indicator for the whole economy.

The Bangkok SET Index is a capitalization-weighted index of all the stocks traded on the Stock Exchange of Thailand.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All