The term “alternative investment” only makes sense in relation to some other type of investment—that is, a set of non-alternative core asset classes. The implication is that the non-alternative investments are more traditional or more generally accepted than the alternative investment.

This article utilizes the terms “core asset class” and “diversifier asset class,” which are meant to be understood as being different from alternative asset classes.

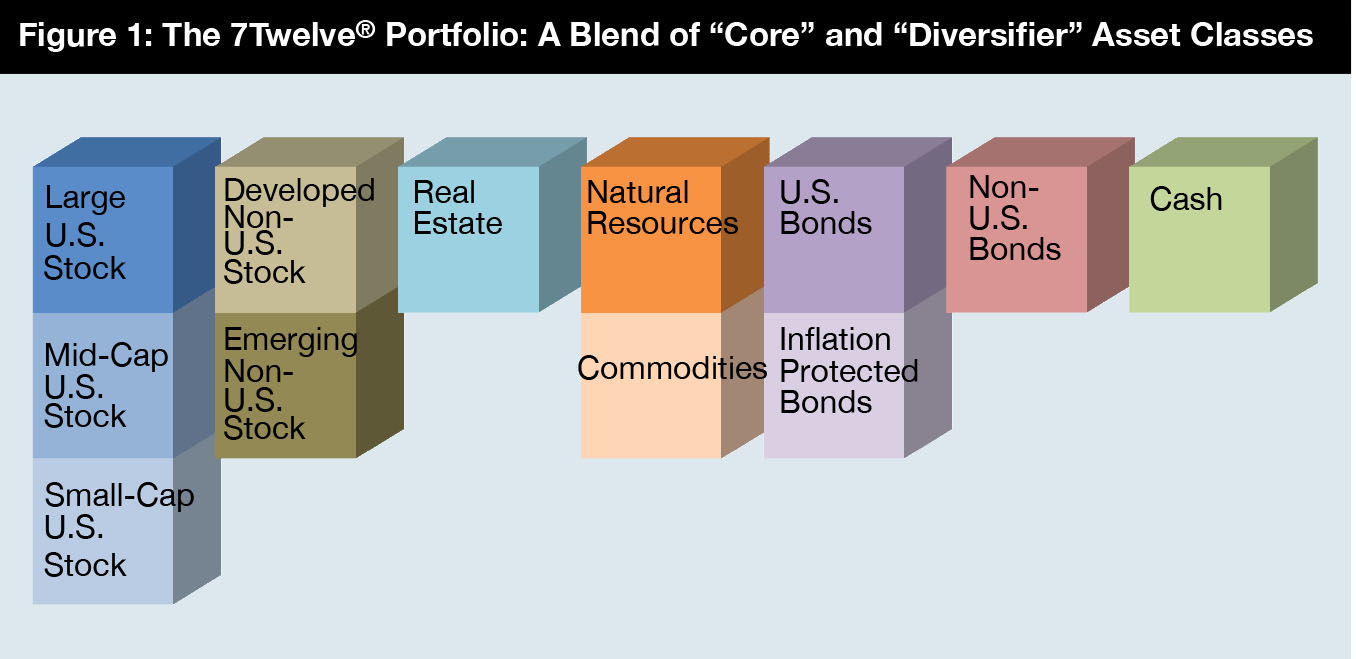

The core asset classes in this study include U.S. equity (large, mid, small), non-U.S. equity (developed), U.S. bonds, and cash. The diversifier asset classes in this study include emerging stock, real estate, natural resources, commodities, Treasury inflation-protected securities (TIPS), and non-U.S. bonds.

The alternative asset classes included in this study were defined as such by Lipper and include: active extension, credit focus, currency strategies, equity market neutral, event driven, global macro, long/short equity, managed futures, and multi-strategy.

An important premise of this study is that core and diversifier asset classes should be present in any well-diversified portfolio, and that alternative asset classes might be used selectively as satellite positions around the diversified core.

Core Asset Classes

Large-cap U.S. stock is a traditional and widely accepted investment asset. The S&P 500 Index is the most common representation of large-cap U.S. stock. Thus, including large-cap U.S. stock in a portfolio is considered a core or fundamental starting point for most portfolios that include an equity allocation.

The next most fundamental or core equity asset classes in a portfolio typically might include small-cap U.S. stock and non-U.S. stock. Typical indexes representing these two asset classes would be the Russell 2000 Index and the Morgan Stanley Capital International EAFE (Europe, Australasia, and Far East) Index.

These three equity asset classes (large-cap U.S. stock, small-cap U.S. stock, and non-U.S. developed market stock) typically are available in most 401(k) menus—suggesting that they are viewed as core equity asset classes. Mid-cap U.S. stock likely also would be considered a core asset class. A representative index would be the S&P MidCap 400 Index. U.S. bonds and U.S. cash are virtually always present in a 401(k) menu suggesting that they are also core asset classes. Representative indexes would be the Barclays Capital Aggregate Bond Index and the three-month U.S. Treasury bill (or essentially a typical money market mutual fund).

Diversifier Asset Classes

What would be the diversifiers to these six core equity asset classes? As already noted, the diversifier asset classes (and representative indexes) include the following: emerging stock (MSCI EM Index), real estate (DJ US Select REIT Index), natural resources (S&P North American Natural Resources Sector Index), commodities (Deutsche Bank Liquid Commodity Index), TIPS (Barclays US TIPS Index), and non-U.S. bonds (Barclays Global Treasury ex-US Index).

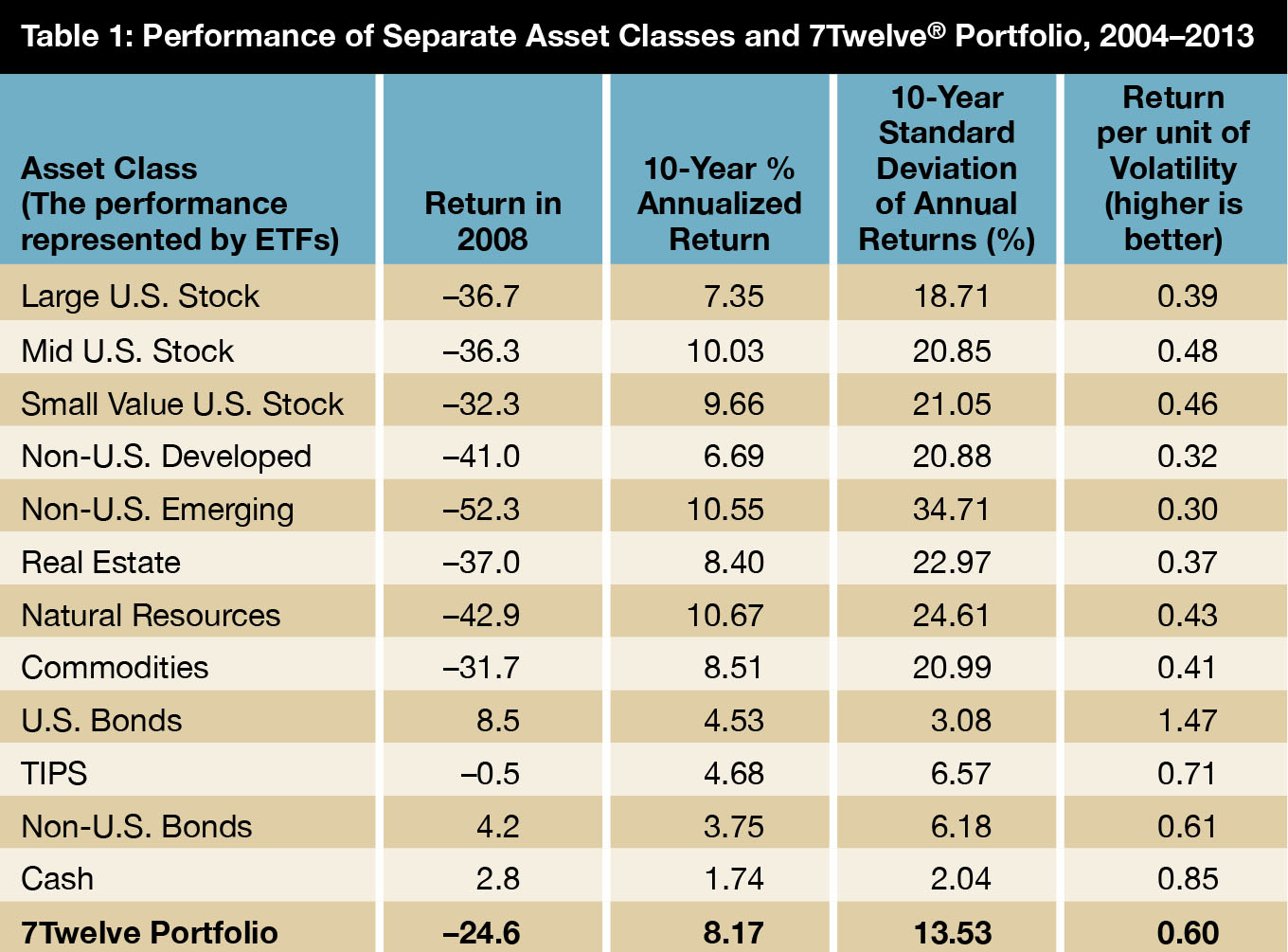

The combination of these six core asset classes with these six diversifier asset classes is known as the 7Twelve® Portfolio (www.7TwelvePortfolio.com) (full disclosure: the author is the designer of the 7Twelve Portfolio). The 7Twelve model is depicted in figure 1. Each of the 12 asset classes is equally weighted at 8.33 percent and is rebalanced annually. Performance of the 7Twelve Portfolio in addition to all the separate ingredients is reported in table 1. (Return per unit of volatility is calculated by dividing the 10-year annualized return by the 10-year standard deviation of annual returns—the higher the number the better).

Putting It All Together

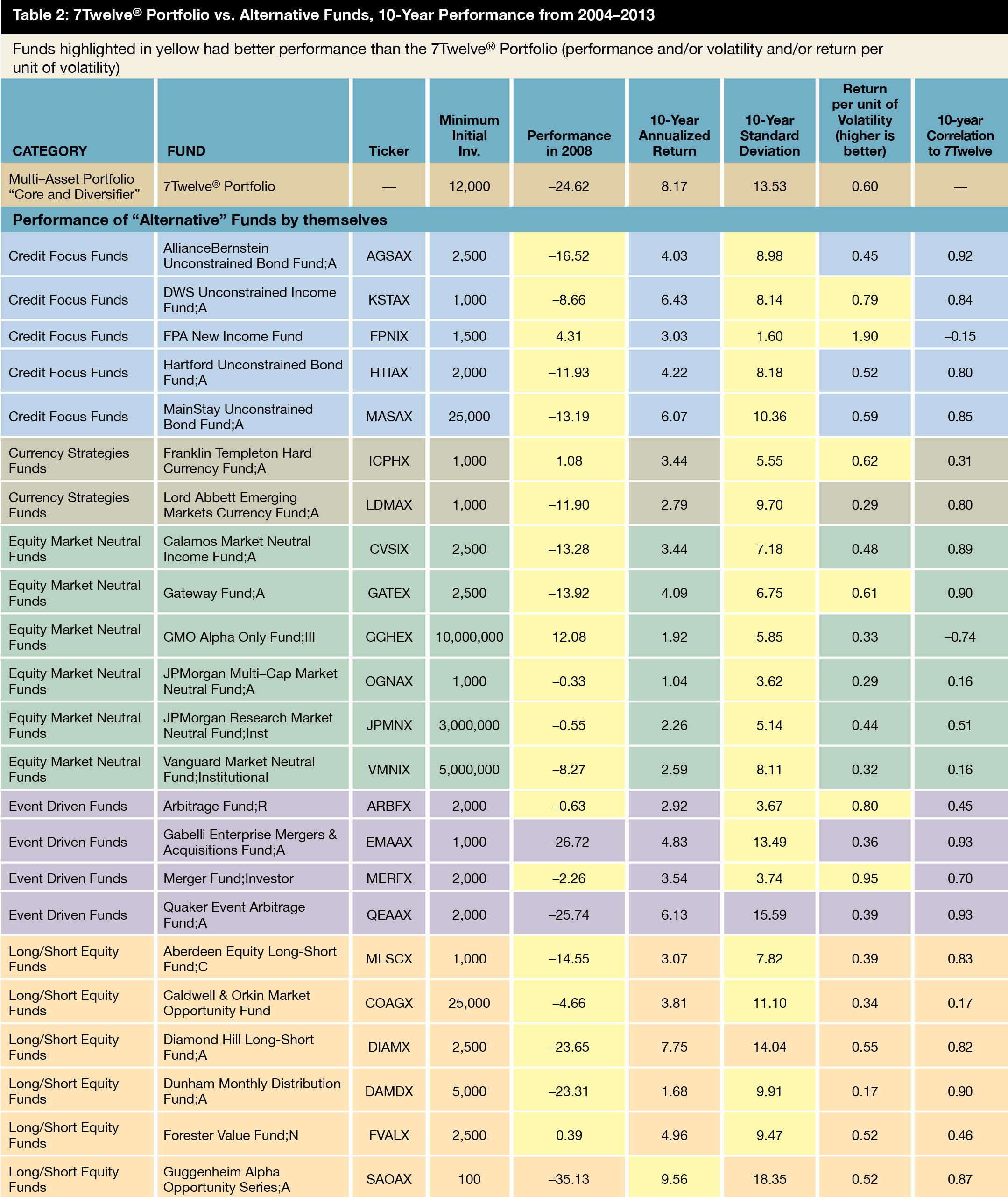

The key information included for each alternative fund is its category, fund name, ticker symbol, minimum initial investment, performance in 2008, 10-year average annualized return as of December 31, 2013, 10-year standard deviation of annual returns, and 10-year return per unit of volatility. Finally, the 10-year correlation of each alternative fund to the 7Twelve Portfolio was calculated and is shown. The minimum initial investment of $12,000 for the 7Twelve Portfolio assumes a $1,000 investment into each exchange-traded fund (ETF) representing the 12 asset classes.

The boxes in table 2 that are highlighted in yellow indicate outperformance in comparison to the 7Twelve portfolio. For example, all but five of the alternative funds performed better in 2008. Only two of the alternative funds had a superior 10-year annualized return. Twenty-five of the 31 alternative funds had lower standard deviation than the 7Twelve Portfolio. Six of the alternative funds had a more favorable return per unit of volatility.

Continue reading this article now.

Craig Israelsen, PhD, is an executive-in-residence in the Financial Planning Program at Utah Valley University. His research interests include analysis of mutual funds and design of investment portfolios. He earned a PhD in family resource management from Brigham Young University, and a BS in agribusiness and MS in agricultural economics from Utah State University. Contact him at [email protected].

© Investment Management Consultant Association (IMCA)