Apple Gets a Shakedown from the EU. Is Ireland Next to Bail?

“Total political crap.”

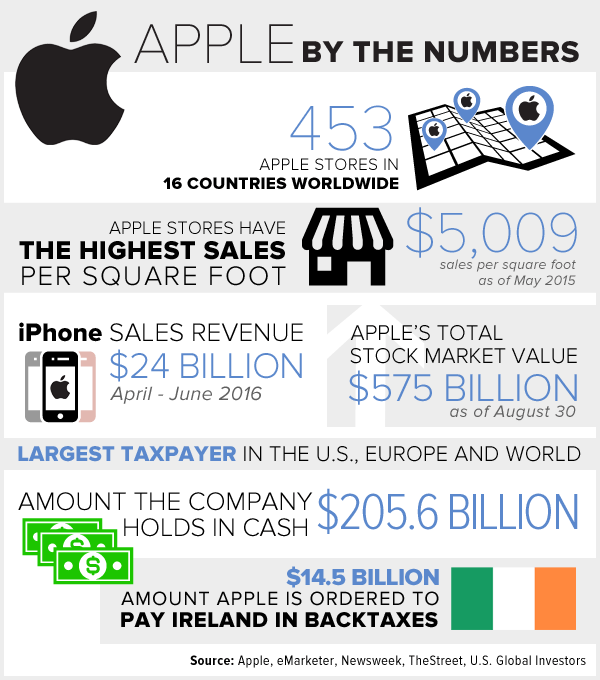

That’s how Apple CEO Tim Cook described the European Commission’s ruling that the iPhone maker must pay 13 billion euros ($14.5 billion), plus interest, in back taxes to Ireland, its longtime European host. Meanwhile, the island-nation is being accused of giving Apple an “illegal” sweetheart deal in exchange for jobs.

Political crap, indeed. I hate to say it, but I told you so.

June’s Brexit referendum, I’ve argued, was about so much more than immigration. U.K. citizens and businesses are fed up with mountains of rules and regulations from unelected bureaucrats in Brussels, controlled by French and German socialists, that trample on basic personal freedom. There are ludicrous laws on the books legislating everything from the kind of lightbulbs you can use to the wattage of your vacuum cleaner to the curve and length of your bananas and cucumbers to the color of your olives.

Now, Ireland is learning a similarly hard lesson on Brussels’ policies of envy.

It’s a plotline that should be reserved for the Theater of the Absurd: Party A is forced by Party B to pay Party C, in a transaction that neither Party A nor Party C had a hand in creating.

Apple insists it has no outstanding taxes. “We never asked for, nor did we receive, special deals,” Tim Cook wrote in an open letter this week. And yet an authoritarian, nontransparent “Commissioner of Competition” is ordering the company to shell out an arbitrarily exorbitant amount to the government of Ireland—which doesn’t even want Apple’s money.

And why would it? As you might imagine, Ireland fears risking a stain on its tax advantaged status that has succeeded in attracting hundreds of billions in foreign direct investment.

Eurocrats Envious of Ireland’s Competitive Advantage and America’s Ingenuity

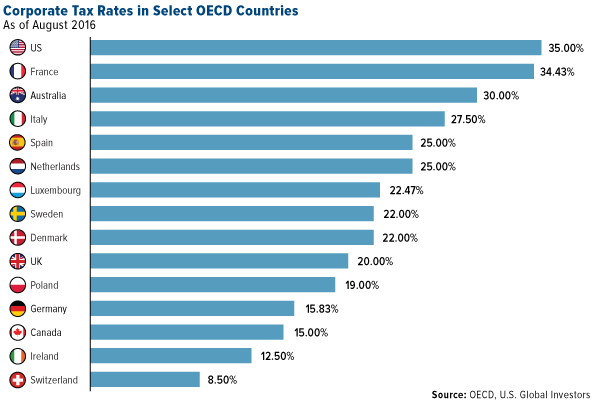

Over the last 50 years, the country has carved out a reputation as a prime destination for multinationals seeking a competitive corporate tax rate. At 12.5 percent, Ireland’s rate is much more attractive than the U.S. rate, 35 percent, one of the highest in the world. (Other countries with similarly high rates include Argentina, Brazil and Venezuela—not exactly model examples of business-friendly regimes.)

Consider what Ireland has achieved: PricewaterhouseCoopers (PwC) ranks it “the most effective country in the EU in which to pay business taxes.” For five years in a row, the country has topped IBM’s Global Location Trends report for its “continued ability to attract high-value investment projects in key areas.” The most recent IMD World Competitiveness Yearbook names Ireland first in the world for “investment incentives” and “financial skills.” According to the World Economic Forum, it’s the fastest growing European economy (followed by Romania, which I wrote about in July). The list goes on.

For these reasons and more, nine out of the top 10 global information and communications technology (ICT) companies have locations in Ireland, not to mention nine out of the top 10 global pharmaceutical companies and nine out of the top 10 global software companies, according to Ireland’s Industrial Development Agency.

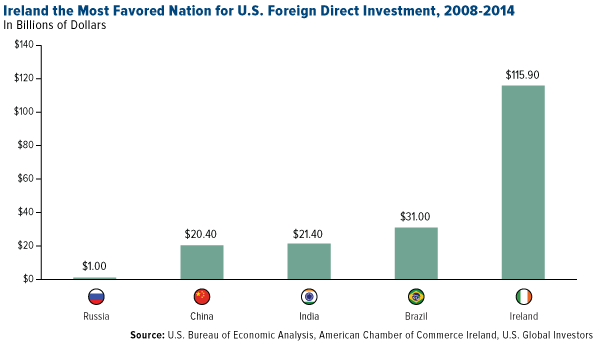

The country’s relationship with American-based companies has been particularly beneficial to its economy and workforce. U.S. companies account for three quarters of Ireland’s inward investment, which totaled nearly $116 billion in the years from 2008 to 2014. That’s more than U.S. investment in the four BRIC countries combined over the same period. About a fifth of all private sector jobs in Ireland are in some way linked to American multinationals. Apple alone employs 6,000 Irish citizens, most of them in Cork, where Steve Jobs originally opened an Apple factory in 1980.

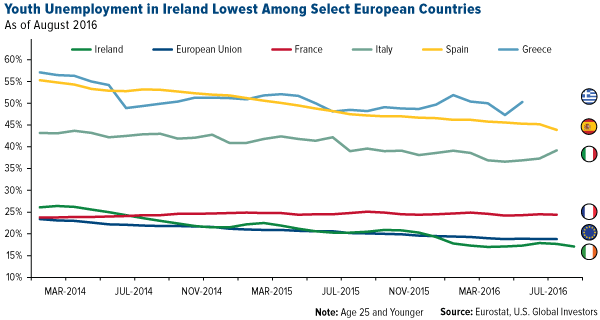

Thanks to low corporate taxes that attract big multinationals, youth unemployment in Ireland is today among the lowest in the EU. Restrictive, labyrinthine labor laws elsewhere in the 28-member bloc have immobilized the jobs market, especially for young people, many of whom have little choice but to seek work abroad. In May, the Financial Times reported that the number of EU nationals working in the U.K. had climbed to 2.1 million, accounting for close to 7 percent of its workforce—a new high.

Both Apple and Ireland vow to appeal the European Commission’s ruling, a process that will likely take years.

Next Up: Irexit?

The real question now is whether the Apple incident will motivate Ireland to follow the U.K.’s lead and pursue its own “Irexit” from the European Union. In June, I asked if we’re nearing the end of the EU experiment. If officials continue to oppose competition and restrict member states from conducting business on their own terms, entrepreneurial countries such as Ireland will increasingly feel the pressure to file for divorce

Remember, Britain will soon be free to do what it pleases to attract foreign investment—possibly away from Ireland. London already sees an opening with Apple following the tax ruling. On Tuesday, Prime Minister Theresa May’s spokesman said the tech giant is welcome to relocate to the U.K. if things don’t work out between Ireland and the EU.

This would be a high price for Ireland to pay to retain its EU membership status.

Apple Just the Beginning

American multinationals are likewise in a difficult position, as they face mounting pressure from EU regulators and tax officials. Europe doesn’t have its own versions of Apple, Facebook and others, so its only course of action is to legislate them into being noncompetitive.

I previously shared with you the European Commission’s proposal to require streaming services such as Netflix and Amazon Prime Video to meet a content quota. Under the plan, at least 20 percent of all programs offered in their libraries would need to be produced in Europe.

Like Apple, Starbucks was ordered in October 2015 to pay up to $33 million in back taxes to the Netherlands, a ruling the Dutch government has already appealed. McDonald’s and Amazon’s tax arrangements in Luxembourg are also being scrutinized, and Google could be added to the list.

Speaking of Google, its Madrid office was raided in June by Spanish tax inspectors, who are accusing the search giant of tax avoidance.

In yet another case, Google and Facebook could both end up having to pay licensing fees to European newspapers, magazines and other publications every time their content ends up in their search results.

WhatsApp, the most-used messaging app in the world, and its parent company, Facebook, are both currently being investigated by EU privacy regulators.

This is just a sampling of what American companies must put up with in order to do business in Europe.

The question stands: Instead of attacking American innovation and ingenuity, why don’t Europeans develop their own competitive alternatives?

Index Summary

- The major market indices finished up slightly this week. The Dow Jones Industrial Average gained 0.52 percent. The S&P 500 Stock Index rose 0.50 percent, while the Nasdaq Composite climbed 0.59 percent. The Russell 2000 small capitalization index gained 1.11 percent this week.

- The Hang Seng Composite gained 1.47 percent this week; while Taiwan was down 1.58 percent and the KOSPI rose 0.04 percent.

- The 10-year Treasury bond yield fell 3basis points to 1.6 percent.

Domestic Equity Market

Strengths

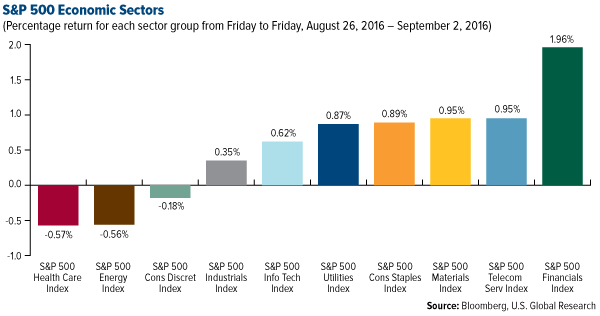

- Financials was the best performing sector for the week, increasing by 1.96 percent versus an overall increase of 0.49 percent for the S&P 500.

- United Continental was the best performing stock for the week, increasing 9 percent. The stock rose after the airline announced it had lured American Airlines executive Scott Kirby to be its president. The move comes in response to concerns about succession planning after the exit of former CEO Jeff Smisek left investors wondering whether United had deep enough of a support team to sustain positive momentum in the event of a leadership change.

- Infoblox Inc. spiked to a 52-week high Wednesday after a report that it was accepting acquisition bids. The security-software company also beat expectations in its earnings report.

Weaknesses

- Health care was the worst performing sector for the week, falling by -0.57 percent versus an overall increase of 0.49 percent for the S&P 500.

- Diamond Offshore Drilling was the worst performing stock for the week, falling -13.40 percent. The company’s stock fell the most in nearly half a year after Petroleo Brasileiro SA canceled a drilling contract for a deep-water rig two years early as it cuts costs to survive the crude market downturn.

- Lululemon's same-store sales missed. The athletic-apparel retailer posted in-line earnings and revenue, but same-store sales including direct-to-consumer, but excluding FX adjustments were light, coming in at 5 percent versus expectations for a 5.9 percent increase. Lululemon shares lost 8.5 percent in after-hours trade.

Opportunities

- Smith & Wesson sees a ton of gun sales in the future. The gun maker crushed analyst estimates on the top and bottom lines, and it raised its full-year earnings-per-share guidance to a range of $2.38 to $2.48, up from a range of $1.83 to $2.03.

- Historically, a flat yield curve has signaled that monetary policy is too tight and that an economic downturn loomed. An inverted yield curve accurately predicted the major U.S. equity market tops in 2000 and 2007, as well as the shorter but sharp declines in 1990 and 1998. The yield curve continues to narrow as the Fed lowers its terminal rate forecast and the insatiable global search for yield persists. It will not take many Fed rate hikes for the yield curve to completely flatten or invert. As such, BCA’s U.S. equity strategists continue to de-emphasize the overall financial sector, preferring its less cyclical components such as REITs and insurance, which stand a better chance of outperforming as the curve flattens further.

- BCA's U.S. and global strategists have become cautious on the near-term outlook for U.S. and global equities. Renewed hawkishness from the Fed and/or earnings disappointments could trigger a correction in the coming weeks. However, they see any such correction as unlikely to be the start of a cyclical bear market just yet.

Threats

- Ford says U.S. auto sales have peaked. All of the so-called “Big Three” missed analysts' expectations for August sales. Only Fiat Chrysler reported a positive month, while Ford and GM posted declines. Ford said it no longer sees the pent-up demand experienced after the financial crisis, and that has led to the peak. Overall, sales rose at a seasonally adjusted annual rate of 16.98 million, missing expectations, according to Autodata.

- The Department of Justice filed an anti-trust lawsuit against Deere's planned purchase of Monsanto's Precision Planting business. The government's suit in Chicago Federal Court said the deal would remove competition and raise costs for farmers, Bloomberg reported. Deere, the largest maker of agricultural machinery, agreed to buy the unit in November to give farmers real-time planting data.

- The European Union ordered Apple to pay up to a record 13 billion euro ($14.5 billion) in taxes to Ireland. The EU's competition commissioner said the country gave Apple "illegal tax benefits." Apple said the decision will harm investment and job creation in Europe. It is appealing the judgement.

![[thumb]](/images/content_image/data/4e/4e1085c38f52347e120a6483975f4838.jpg)

August 30, 201611 Reasons Why Everyone Wants to Move to Texas |

![[thumb]](/images/content_image/data/e0/e01270ecc32b78fd6b99b8373efecb5b.jpg)

August 29, 2016The Real Truth About Millennial Investors |

![[thumb]](/images/content_image/data/f1/f18d98814b62a08114b207c535d0d0da.jpg)

August 22, 2016These Olympian Gold Royalty Companies Are Insanely Attractive |

The Economy and Bond Market

Strengths

- The 4.3 percent jump in second quarter unit labor costs (upward revision from 2 percent) illustrates tightening labor markets and some wage growth.

- The Conference Board's consumer confidence index jumped to 101.1 in August, the highest since last September. The share of people saying jobs were "plentiful" increased from 23 percent to 26 percent, the highest since January 2008.

- Personal spending was up 0.3 percent month-over-month (MoM) in July. Prices were also flat, leaving real personal spending up 0.3 percent MoM. June's real spending was revised up to 0.4 percent.

Weaknesses

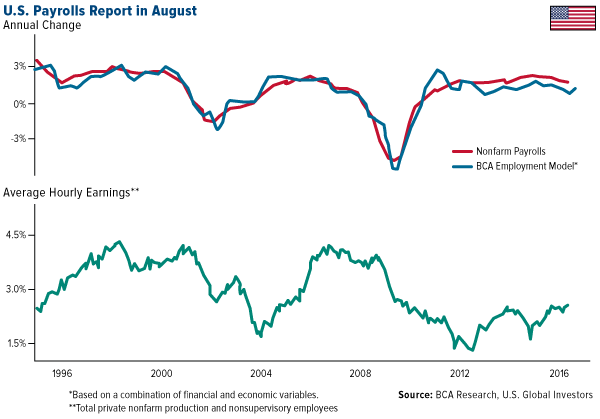

- The August employment report was soft, shifting expectations for the Fed rate hike to December. Nonfarm payrolls expanded by only 151,000, below the expectation of 180,000. Aside from the headline number, there were two areas of softness. First, average hourly earnings rose by only 0.1 percent MoM. The annual wage inflation rate fell to 2.4 percent from 2.7 percent. Soft wages confirm that labor demand is not outstripping supply. Second, the average work week was down. As a consequence, aggregate hours worked, a measure of total labor inputs, fell 0.2 percent MoM.

- Manufacturing slumped back into contraction in August, according to the Institute of Supply Management. The purchasing managers’ index was 49.4, missing the forecast for 52. A plunge in new orders led declines among all the measures that make up the index. Production, order backlogs, and employment also shrank. This indicates the first contraction in manufacturing activity in six months.

- Second quarter productivity fell by 0.6 percent, the third negative quarterly reading and the longest streak of productivity declines in more than 35 years.

Opportunities

- No change in European Central Bank (ECB) policy is expected on Thursday, but President Draghi's press conference could provide insight to whether the ECB is considering any additional easing for the future.

- Thus far the U.K. economy has proven surprisingly resilient following the Brexit vote. Next week's services PMI, industrial production, Halifax house prices, RICS survey and NEISR's monthly GDP estimate will tell whether this resilience is continuing.

- Given the rising odds of another Fed move before year-end, and the uncertainty that additional easing can be delivered in Europe and Japan, a cautious approach would be to maintain a below-benchmark bond duration stance.

Threats

- The Chicago Purchasing Managers’ Index fell more than expected to 51.5 in August. "Economic activity slowed down into the summer, suggesting June’s momentum was only a temporary revival in activity," said Lorena Castellanos, senior economist at MNI Indicators.

- Following the surprise weakness in the August manufacturing ISM this week, a decline in the nonmanufacturing survey next Tuesday or a pessimistic outlook from the Beige Book on Wednesday will provide confirmation that U.S. GDP growth is losing momentum once again.

- One real-time indicator that investors should monitor for a potential end to the cyclical bull market in stocks is the slope of yield curve. Historically, a very flat or inverted yield curve signaled that monetary policy had become tight and an economic downturn was looming. The U.S. 2/10-year yield curve has been on a flattening trend, but it is it still positively sloped. However, with the curve at about +75 basis points, it is relatively flat and it will not take much for it to completely flatten or invert. Two or three Fed rate hikes and modestly lower, longer term bond yields could cause it to invert.

Gold Market

This week spot gold closed at $1,325.36, up $4.14 per ounce, or 0.31 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, essentially ended the week unchanged. Junior miners outperformed seniors for the week, as the S&P/TSX Venture Index rose 0.67 percent week. The U.S. Trade-Weighted Dollar Index was edged up 0.33 percent.

| Date | Event | Survey | Actual | Prior |

|

Aug-30 |

Germany CPI YoY |

0.5% |

0.4% |

0.4% |

|

Aug-31 |

U.S. Consumer Confidence |

97.0 |

101.1 |

96.7 |

|

Aug-31 |

Eurozone CPI Core YoY |

0.9% |

0.8% |

0.9% |

|

Aug-31 |

ADP Employment Change |

175k |

177k |

194k |

|

Aug-23 |

Caixin China PMI Mfg |

50.1 |

50.0 |

50.6 |

|

Sep-1 |

U.S. Initial Jobless Claims |

265k |

263k |

261k |

|

Sep-1 |

U.S. ISM Manufacturing |

52.0 |

49.4 |

52.6 |

|

Sep-2 |

U.S. Change in Nonfarm Payrols |

185k |

151k |

255k |

|

Sep-2 |

U.S. Durable Goods Orders |

4.4% |

4.4% |

4.4% |

|

Sep-8 |

ECB Main Refinancing Rate |

0.000% |

-- |

0.000% |

|

Sep-8 |

U.S. Initial Jobless Claims |

265k |

-- |

263k |

Strengths

- The best performing precious metal for the week was silver with a surge of 4.18 percent following the poor jobs report.

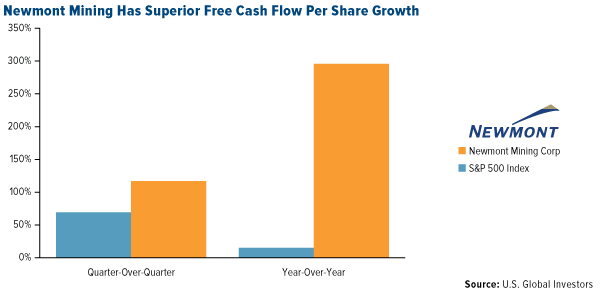

- As seen in the chart below, when comparing the S&P 500 Index and Newmont Mining, the only gold mining stock in that index, on free cash flow per share growth, Newmont has performed significantly better. Both quarter-over-quarter and year-over-year, the mining company beats the broader index on this factor.

- The August unemployment report came in soft on Friday, with payroll expansion of 151,000, reports Bank of America. Consumer confidence surprised to the upside, while the ISM manufacturing index slipped to 49.4. In addition, the Department of Labor reported that second quarter productivity fell by 0.6 percent (the longest streak of declines in more than 35 years). As BofAML notes, when faced with a choice of defending the inflation target or allowing a modest overshoot, the Fed will choose the latter, meaning negative real rates could persist ahead.

- The government in Burkino Faso wants to help mining companies that are already in operation in the nation to lengthen the lives of their mines, reports Bloomberg, and make it easier for new investors to get information about deposits. The supportive policies for wealth creation in the nation are strong. Not only are troops being deployed to secure the mines, but the government is also building seven solar power plants to help deal with an electricity shortage.

Weaknesses

- The worst performing precious metal for the week was palladium with a loss of 1.85 percent. Russia’s state minerals depository noted they do not have any orders to buy platinum or palladium for inventories this year.

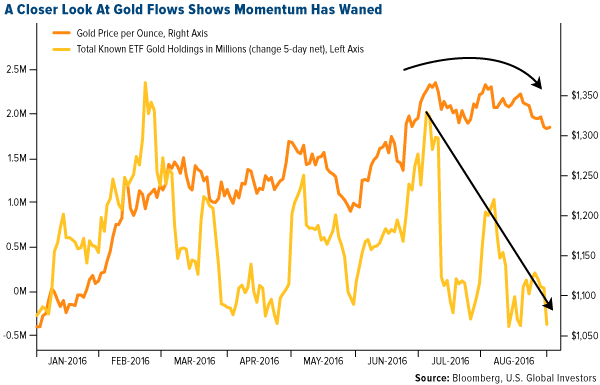

- Gold is in its longest run of declines since May, reports Bloomberg, following speculation from leading central bankers that U.S. interest rates could rise as soon as September, lifting the dollar. “Gold’s rally this year has been pegged back as a rate hike is/was now on the cards,” the article continues. Metal for immediate delivery fell 2.2 percent this month and the momentum of bullion purchases for ETFs slowed.

- During the three months through June, central banks cut their purchases by 40 percent compared to the same time last year, according to data compiled from the World Gold Council. This was the third-straight quarterly drop, reports Bloomberg, making it the longest streak in at least five years. In a similar mood toward the yellow metal, Citi analysts cut their six month stance to bearish, reversing their upgrade of the sector following the Brexit vote.

Opportunities

- In RBC Capital Market’s The Morning Miner report, the group’s traders were noting that the last rate raise by the Fed was in December of 2015, and since then the GDX is up over 100 percent. When looking at spending for the miners, the report shows that a majority of companies have “sustaining capex below 50 percent of full-year guidance.” A Morgan Stanley report also highlighted capex intentions out of Australian companies, noting that fiscal year 2017 capex intentions provide better visibility on an expected -32 percent plunge in resource spend.

- TD Securities released its Precious Metals Second Quarter Recap report this week, noting that overall the quarter was largely in-line with expectations. The group says margins were up slightly as the increase in gold price more than offset modest cost increases. In addition, production was relatively flat quarter-over-quarter, but remains down year-over-year. Lastly, positive free cash flow generation continued during the second quarter, with companies maintaining a tight lid on non-essential spending.

- Despite gold and silver stocks being up over 100 percent in 2016, Sean Williams at Motley Fool says they can still be considered “value stocks,” particularly relative to the S&P 500. His analysis is based on price-to-cash flow per share ratio (P/CFPS). Currently, the S&P 500 is valued at 8.7 times P/CFPS (and generally speaking it is often between 10 and 20). “However, if you look at gold and silver stocks, you’ll find substantially cheaper alternatives on a price-to-cash flow per share basis,” Williams continues. “Especially after this last correction. In many instances, you can find mid-to-high, single-digit P/CFPS among gold and silver miners.”

Threats

- Some of South Africa’s biggest mining companies are opposed to a government proposal that 1 percent of their annual revenue be spent on developing communities associated with their operations, reports Bloomberg. Some have countered with suggestions that they pay a share of profit instead. These companies already pay royalties to the government, differing by commodity. For example, gold producers pay around 3 percent of revenue, says Bloomberg.

- James Rickards recently pointed out the risks of having all of your assets in a digital format versus owning some physical gold. Rickards notes whether that means digital currency deposits, digital gold, digital stocks, etc. According to the Zero Hedge article, Rickards believes these assets are now intermediated by technology which creates counter party risk from the platform, liquidity providers, etc.

- Christopher Louney from RBC Capital Markets writes that the Chinese gold market will continue to grow, according to the group’s analysis on the space. However, he notes that lower net demand and continued supply growth means that the demand shortfall should narrow this year, thus “feeding the dragon” should be easier this year than in those past. The group also reiterates their belief that the gold price will weaken, noting the “investor-only” nature of this year’s gold rally while jewelry sales have stagnated.

Energy and Natural Resources Market

Strengths

- Gold shone again after U.S. employment data disappointed. August payrolls climbed by 151,000 below the median forecast in a Bloomberg survey which called for 180,000. The weak data boosted the metal’s appeal as a haven, paring its weekly decline.

- The best-performing sector for the week was the S&P Supercomposite Paper and Forest Products Index. The index rose 3.6 percent after a number of members reported price hikes for its containerboard products, suggesting demand was stronger than initially anticipated.

- Potash Corp of Saskatchewan Inc., a Canadian major fertilizer and chemicals producer, was the best-performing stock in the broader natural resource space for the week. The stock gained 12.2 percent after it disclosed to be in talks with peer Agrium Inc. about a potential merger.

Weaknesses

- Global manufacturing purchasing managers’ index (PMI) edges lower again in August. As VTB Capital reports, the unexpectedly sharp fall in the U.S. ISM manufacturing composite index to 49.4 (vs 52.6 in July) weighed on the JP Morgan Global Manufacturing PMI which declined 0.2 to 50.8. The PMIs are reflective of sluggish new orders in most regions.

- The worst performing sector for the week was the FTSE 350 Mining Index. The index of major global diversified miners dropped 4.2 percent for the week, as global commodities weakened as a result of dovish commentary out of Jackson Hole over the weekend, which propelled the U.S. dollar to a 4-week high.

- The worst performing stock for the week in the broader natural resource space was First Quantum Minerals Ltd. The major Canadian copper miner dropped 5.7 percent after tracking the weakness in global miners. In addition, news releases suggested the company reported power issues at one of its operations in Zambia.

Opportunities

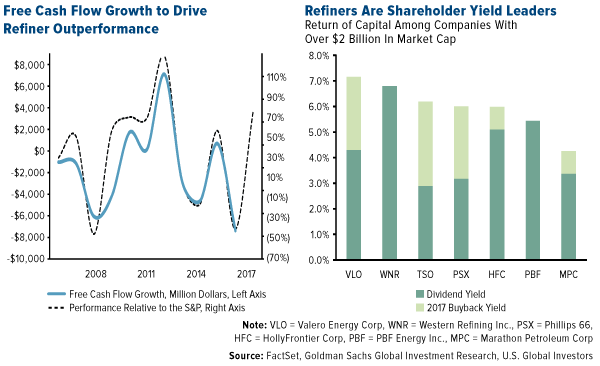

- Refiners may be on the edge of a breakout. A recent Goldman Sachs report suggests refiners may outperform the S&P 500 by as much as 50 percent in 2017 as free cash flow generation rebounds strongly. In addition, the bank’s analysts highlight refiners as shareholder yield leaders, with dividends and buybacks expected to yield 4 to 7 percent in 2017.

- Oil discoveries at a 70-year low signal a supply shortfall ahead, according to Bloomberg. Following the collapse in crude prices, explorers and producers have curtailed exploration spending, resulting in the smallest amount of crude discovered since 1947, according to Wood Mackenzie Ltd. The article suggests that producers lose an average 5 percent of production per year due to natural declines, and as a result, the industry may find itself unable to meet demand growth in the next decade.

- Chinese house prices re-accelerated in August. A private survey of 100 large cities by China Index Academy showed house prices up 2.17 percent in August, the strongest monthly increase so far in the current property cycle and a sharp rebound from the recent pullback to 1.32 percent in June, reports VTB Capital. The China Index Academy data also showed renewed pick-up in the three leading cities of Beijing, Shanghai and Shenzhen, which had previously slowed as credit conditions tightened.

Threats

- OPEC members pumped record crude in August. OPEC’s production increased by 40,000 barrels per day in August to 33.5 million barrels per day, setting a fresh output record, according to OilPrice.com. The unexpected increase from July’s record levels continues to jeopardize the stabilization of crude prices, and suggests that the global crude market remains oversupplied.

- Oil supermajors’ dividends are at ‘Massive Risk,’ according to Macro Risk Advisors. The world’s biggest oil and gas producers pay more than $40 billion in annual dividends to investors, and as the worst crude collapse in a generation stretches into a third year, these supermajors may find themselves unable to honor their commitments.

- Global metals and mining stocks have outrun the fundamentals and may be due for correction, says Citi. The bank slashed its stance on the global metals and mining industry to bearish, reversing an upgrade following the Brexit vote, as strong dollar concerns and inflated valuations suggest the sector may be overdue for a correction.

China Region

Strengths

- South Korea was the best performing country in the region this week, gaining 40 basis points.

- Official Manufacturing PMI in China came in much better than expected. China’s expansionary August print of 50.4 beat analysts’ expectations for a contractionary drop to 49.8, and marks a jump from July’s reading of 49.9 to one of the gauge’s highest readings in two years. The Caixin China Manufacturing PMI came in right at 50.0, just behind expectations for 50.1, and official Non-manufacturing PMI came in above 53. We don’t get Caixin’s Services PMI reading until next week.

- The Hong Kong dollar was the strongest currency in the region this week.

Weaknesses

- Malaysia was the worst performing country this week and the Malaysian ringgit was the weakest currency in the region, down -2.2 percent and -1.74 percent respectively.

- The Nikkei Malaysia Manufacturing PMI continues to languish in contractionary territory, dropping from a July print of 48.1 to an August reading of only 47.4. The Malaysian economy has received no great help from relatively lower energy prices over the last couple of years.

- The Nikkei Philippines Manufacturing PMI moderated slightly from its recent highs above 56 to a 55.3 reading for the August period.

Opportunities

- After dipping below 50 into contractionary territory in July, the Nikkei Indonesia Manufacturing PMI rose back into expansionary territory at a 50.4 print for the August period. Investors and locals alike continue to await progress in the recently-announced Tax Amnesty Scheme, designed to spur on infrastructural and domestic development while making up for Indonesia’s large but anticipated budget shortfall.

- China once again has an opportunity to showcase some of its infrastructural development at the G20 meeting in Hangzhou, China this weekend.

- Taiwan announced that it will allow broader Chinese investor access to local Taiwanese mutual funds. The move, announced by Financial Supervisory Commission Vice Chairman Kuei Hsien-nug and reported by Blooomberg News, follows recently-elected Taiwanese President Tsai Ing-wen’s cool but pragmatic initial stance toward the Chinese mainland, whose One-China policy she refuses to endorse.

Threats

- The on-shore Chinese renminbi continued to remain relatively stable this week ahead of China’s hosting of the G20 meeting this weekend. However, there is wide speculation that the intervening PBOC seeks to keep the weaker yuan out of focus at the meeting to the greatest extent possible.

- The Nikkei South Korea Manufacturing PMI fell in August to a contractionary 48.6, down from July’s reading of an expansionary 50.1. South Korea’s largest container-shipping company Hanjin Shipping Co. also filed for court protection this week, worrying retailers and raising supply chain questions even as Korean exports rose for the first time in twenty months.

- Emerging markets and emerging market currencies rallied as data showing slower than forecasted U.S. employment growth reduced the odds that the Federal Reserve will move quickly to raise interest rates, propping up demand for riskier assets.

Emerging Europe

Strengths

- Czech Republic was the best-performing country this week, gaining 2.6 percent. Bloomberg’s economist survey showed that the Czech Central Bank will only be able to remove its three-year-old exchange cap, which has kept the koruna from appreciating much above 27 per euro, in the fourth quarter of 2017 at the earliest. GDP growth was reported at 2.6 percent, above the prior 2.5 percent. The Czech state budget surplus grew to over 81 billion koruna in August, the best result ever, on the back of better tax revenues.

- The Romanian leu was the best relative currency this week, losing 15 basis points against the dollar. Romania is among the fastest growers in emerging Europe. Second-quarter GDP will be released next week, and economists expect 6 percent growth on year-over-year basis. The country’s unemployment rate stands at 6 percent, and retail sales growth at 16 percent.

- The health care sector was the best performing sector among Eastern European markets this week.

Weaknesses

- Turkey was the worst performing market this week, losing 31 basis points. After the failed coup attempt, President Recep Erdogan continues to fire government employees and jail people who he believes are followers of the Gulen movement. The Financial Times published an article saying that Turkey is on track to surpass China this year as the country that jails the most journalists.

- The Ukrainian hryvnia was the worst-performing currency this week, losing 4.5 percent against the dollar. Ukraine’s bonds are the worst performers this month among eastern European debt with 1 percent loss. According to the Ukrainian central bank, current hryvnia volatility is caused by seasonal increase in demand for foreign currency, a dip in grain prices, and escalation of the Crimean situation in eastern Ukraine.

- The industrial sector was the worst-performing sector among Eastern European markets this week.

Opportunities

- Kazim Andac from Deutsche Bank sees favorable risk/return reward in selected Turkish banks despite top-down risk. Turkish banks are still 12 percent below their pre-coup levels, trading at 37 discount based on price to book value – one of the widest discounts since December 2009. Current valuations may provide opportunity to own those banks that are of better quality with stronger capitalization, efficiency and asset quality.

- According to Bloomberg, the debt reduction push is one of the reasons emerging market stocks have soared this year. The average debt of Russian companies in the MSCI Emerging Markets Index fell to $8.9 billion in the second quarter from $10.3 billion a year earlier as international sanctions prevented many from issuing debt. The more than 800 companies in MSCI’s Emerging Markets Index posted average growth in earning per share of 47 percent in the latest quarter, while profits for members of the Standard & Poor’s 500 Index fell.

- Russia’s government lifted a ban on charter flights to Turkey, which officially opens the Russian travel market to Turkey once more. Some 13 percent of Turkey’s GDP is derived from travel and tourism and Russians are among the more faithful visitors, along with the British. Latest data showed tourist arrivals into Turkey declined by 37 percent on a year-over-year basis. The high travel season is over this year but next year it could see improvement.

Threats

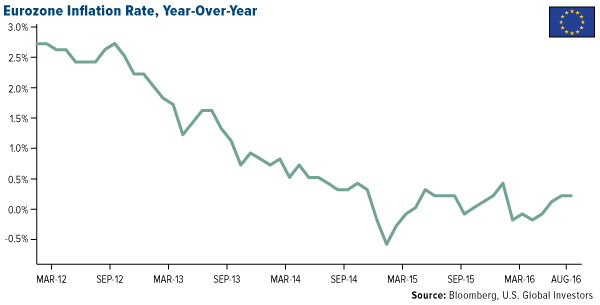

- Euro-area inflation failed to accelerate in August. Consumer prices rose 0.2 percent, versus a consensus estimate for 0.3 percent. In March, the European Central Bank (ECB) cut the main interest rate from 0.05 percent to zero, and its bank deposit rate from minus 0.3 percent to minus 0.4 percent. Later in the year the ECB has increased its program of quantitative easing, and is now buying 80 billion euros a month. Despite these stimulus measures the inflation rate still remains well below the bank’s target of 2 percent.

- Investment in Poland accounted for just 16.7 percent of GDP in the second quarter, down from 18.1 percent a year ago, the biggest contraction in investment for almost four years. Political uncertainty discouraged firms from spending due to concerns over increasing government interventions in the economy and a constitutional crisis.

- After the recent Janet Yellen speech the probability of a hike in September has risen to about a 35 percent chance with a December rate rise now seen as a 60 percent probability. The rate hike in the U.S. may mean a stronger dollar and weaker emerging currencies. If the U.S. economic data remain strong, it may be tough to make a decision not to raise rates sooner than later.

(c) US Global Investors