In 2015, the State of Rhode Island selected Ascensus College Savings as the program manager and Invesco as the investment manager for the state’s 529 college savings plan, which is available to investors nationwide. In this role, we at Invesco created a suite of investment options specifically designed to meet the unique needs of college savers, who face fast-growing college costs and a limited time to save.

Our plan has three tiers:

- A menu of individual fund options for investors to build their own custom portfolios

- Three fixed, target risk portfolios (conservative, moderate and growth)

- Eleven age-based portfolios designed to align with a child’s expected year of college enrollment

In this blog, I’m going to focus on the construction of the age-based portfolios, which many investors like for their “set it and forget it” nature — once you choose a portfolio for your child, the asset allocation among stocks, bonds and cash automatically adjusts over time. The allocation is tailored to pursue growth when the child is younger and become more conservative as college bills become closer.

Addressing the unique needs of college savers

Our research indicated that many college savings plans offered by the industry are quite similar in design to retirement savings plans. However, we believe that college savers face specific goals and constraints that should be considered and which we factored into our portfolio design:

- Distinct investment goal. While retirement savers may be focused on maximizing their total returns, college savers are focused on capital preservation and specifically outperforming the rising cost of education. Over the past several decades, education-related costs, as measured by the Higher Education Price Index (HEPI), have significantly outpaced general price inflation, as measured by the Consumer Price Index (CPI). For example, $100 indexed to the CPI in 1962 would have resulted in $789.50 at the end of 2014. But indexed to the HEPI, $100 would have resulted in $1,201.20 over the same period. With that in mind, the return goal for CollegeBound 529 is defined in terms of risk-adjusted returns needed to outpace college inflation as measured by the HEPI.

- Limited investment horizon. College savers have a relatively short investment horizon, generally up to 18 years, to meet their objective, with limited flexibility to significantly extend it. On the other hand, retirement savers could have 30 to 40 years to save, and can often be more flexible with their retirement dates and give themselves a few extra years to save, if needed.

- Rigid costs. The ability of college savers to set or control the cost of a college education is basically limited to a choice between public and private institutions. Compare this with retirement savers who have the flexibility to spend differently, if needed, should they fall short of meeting their retirement goals.

Given these limitations and concerns, we approached the development of CollegeBound 529 focused on the need for a lower-risk savings plan designed to seek capital preservation and outstrip the cost of education.

Seeking to minimize shortfalls along the glide path

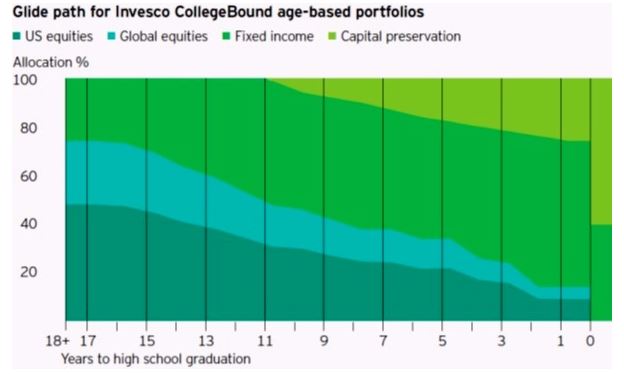

Age-based portfolios are designed to evolve over time — to transition from a heavier weight in equities when children are younger to a more conservative investment in fixed income and cash as a student approaches college age. This change in asset allocation over time is known in the industry as a “glide path.”

The glide path underpinning the CollegeBound 529 age-based portfolios seeks to minimize “portfolio shortfall” — the risk of underperforming college inflation. That risk increases as the investment time horizon shrinks as there’s less time to recoup any potential losses, and with larger allocations to equity, particularly with five years or fewer remaining until college.

The resulting glide path consists of 11 individual portfolios designed to align with the child’s expected year of college enrollment. Based on our research, we believe that offering portfolios in two-year increments (as compared with the industry standard three to four years) would more closely align the allocation to the optimal portfolio for the child’s age. The asset allocations are adjusted quarterly, seeking a smoother transition from capital accumulation to capital preservation.

Robust approach to diversification

Age-based portfolios seek to offer college savers the benefits of diversification through multiple asset classes that are automatically reallocated as the child grows older. In CollegeBound 529, our approach to diversification extended to our investments within each asset class, incorporating different types of investment vehicles and choosing investments from various portfolio management teams.

- Equities – Because college costs are paid for in US dollars, our portfolios include a core allocation to US equities (approximately two-thirds of the total equity allocation). We also include exposure to additional sources of return potential in the form of small-cap, international developed, and emerging market equities.

- Fixed income – In addition to core fixed income, our portfolios include asset classes like bank loans and short-term bonds to help mitigate duration risk (which becomes a concern when interest rates rise). In addition, in the later stages of the glide path, fixed income classes like Treasury Inflation-Protected Securities (TIPS) serve as an inflation-sensitive replacement for riskier equities.

- Capital preservation – In addition to money market funds and short duration TIPS, the investment team made an allocation to stable value, which offers a similar volatility profile to traditional money market funds, but historically with higher yield.

CollegeBound 529 also provides college savers with access to investments from across Invesco’s broad product lineup, including fundamental-based active strategies and factor-based smart beta approaches. Combining these vehicles in a single portfolio enhances our ability to access different asset classes and to harvest the benefits of active management while seeking to lower costs in pursuit of better risk-adjusted returns.

Conclusion

CollegeBound 529 age-based portfolios are specifically designed to help college savers meet their financial goals through a comprehensive and disciplined process that focuses on:

- Accurately capturing the goals of college savers in the form of outpacing the rising cost of education.

- Following a prudent glide path that seeks to meet investor goals while assuming less risk.

- Populating the glide path with thoughtful portfolios that were constructed to maximize the benefits of diversification.

- Developing a low-cost architecture that pairs actively managed funds with passive smart beta offerings to help minimize drag on returns.

To learn more about our age-based portfolios and how they may help you reach your college savings goals, talk to your advisor and visit CollegeBound529.com.

Important information

The Higher Education Price Index (HEPI) measures a basket of goods and services most relevant to the increases in the cost of tuition.

Smart beta is an alternative, index-based selection methodology that may outperform a market-cap-weighted benchmark or mitigate portfolio risk, or both, through active or passive vehicles. Smart beta funds may underperform cap-weighted benchmarks and increase portfolio risk. There is no assurance that an investment strategy will outperform or achieve its investment objectives.

The consumer price index (CPI) measures change in consumer prices as determined by the US Bureau of Labor Statistics.

Diversification does not guarantee a profit or eliminate the risk of loss.

Before investing, consider whether your or the beneficiary’s home state offers any state tax or other benefits that are only available for investments in that state’s qualified tuition program.

For more information about CollegeBound 529 call 877 615 4116 or visit CollegeBound529.com to obtain a Program Description, which includes investment objectives, risks, charges, expenses and other important information; read and consider it carefully before investing. Invesco Distributors, Inc. is the distributor of CollegeBound 529.

An investment in the portfolios is subject to risks, including: investment risks of the portfolios, which are described in the Program Description; the risk (a) of losing money over short or even long periods, (b) of changes to CollegeBound 529, including changes in fees, © of federal or state tax law changes, and (d) that contributions to CollegeBound 529 may adversely affect the eligibility of the beneficiary or the account owner for financial aid or other benefits. For a detailed description of the risks associated with CollegeBound 529 and the risks associated with the portfolios and the underlying funds, please refer to the Program Description.

CollegeBound 529 is administered by the Rhode Island Office of the General Treasurer and the Rhode Island State Investment Commission. Ascensus College Savings Recordkeeping Services, LLC, the program manager, and its affiliates have overall responsibility for the day-to-day operations of CollegeBound 529, including recordkeeping and administrative services. Invesco Advisors, Inc. serves as the investment manager. Invesco Distributors, Inc. markets and distributes CollegeBound 529.

©2016 Invesco Ltd. All rights reserved.

Designing an investment plan specifically for college savers by Invesco