As a “Tex-Can”—born in Canada, lived in Texas the past 26 years—I’m so blessed to call Texas my home. I can’t wait to tell you all the fascinating things I’ve learned that makes the state a truly remarkable place.

But first, you probably heard about the big gold selloff on Wednesday. I just flew in from meeting with gold fund analysts in Toronto, Vancouver and New York, and a lot of our conservations touched on this subject.

Gold has been on a tear so far this year, so what’s the cause of this selloff? Turns out, most of the gold stock buying can be traced back to macro hedge funds like Bridgewater and quant funds. The generalists, in fact, have not been buying. I might have mentioned before that the S&P 500 Index is only 1 percent gold—Newmont Mining being the only name in the high-cap index—so there’s not much general investment in the yellow metal. The Toronto Stock Exchange (TSE) is closer to 8 percent, but most Canadian institutions are substantially underweight. This has been a big drag on performance.

Some of these hedge funds and quantitative-based investment platforms use leverage in their strategies—some are even triple or quadruple leveraged—which can cause the price of gold to react with big fluctuations. Many quant-based traders also track moving averages like the 50-day, and when gold falls below this mark, they quickly sell enough to lower their risk. So the selloff this week—which came ahead of Federal Reserve Chair Janet Yellen’s hawkish remarks from Jackson Hole, Wyoming—has seen gold and gold stocks fall even more.

In the first quarter this year, the top 10 performing gold stocks—selected based on low SG&A (selling, general and administrative costs)-to-revenue—surged 88 percent. Compare that to the Philadelphia Gold and Silver Index (XAU), which jumped 53 percent during the same period. It appears, then, that one of the key factors triggering quant-buying was low SG&A-to-revenue. Quants didn’t care about the mining properties and future gold production, which has historically been the case.

When selloffs such as these occur, it’s often hard not to get emotional. That’s why it’s important to keep in mind Sgt. Joe Friday’s famous saying: “Just the facts, ma’am.”

I still maintain that the gold drivers are in place and am optimistic for the metals’ outlook. Stay tuned!

Having said all that, let’s talk about Texas, home to U.S. Global Investors!

1. Check out Our Mettle

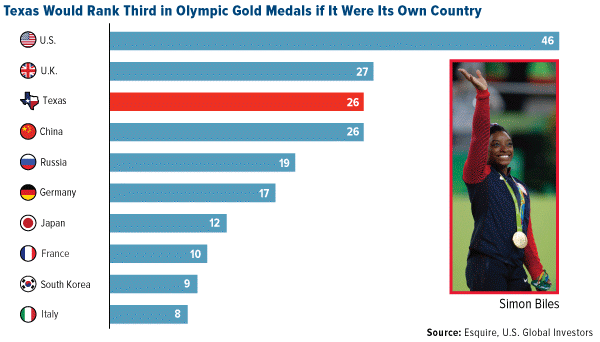

The 2016 Olympics Games in Rio de Janeiro now belongs to history, and by a very wide margin, American competitors walked away with the most medals: 121 altogether. Looking at gold medals, the U.S. still ranked first, with 46 won. But if we took away what Texas collected, the Land of the Free would have fallen to third place, behind the U.K. and China.

Houston was the winningest Texas city. Home to Olympic medalists Simone Biles, Simone Manuel, Kerron Clement and more, H-Town is now 10 gold medals richer.

2. Moneybags

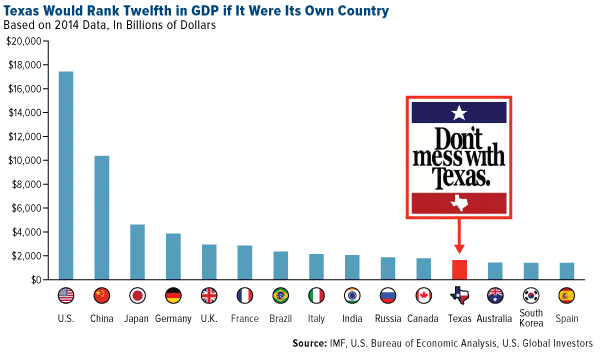

Texas is competitive in more than just Olympic events, of course. The state has the second-largest gross domestic product (GDP) in the Union, following California. If it were its own country, Texas would clock in at number 12 in the world, snuggled in between Canada and Australia.

3. Tex-Can

If Texas were its own nation, in fact, its economy would be about the same size as Canada’s.

4. This Is Oil Country

Another thing Texas has in common with Canada? Black gold. Barrelsful of it.

Last month, Oslo-based Rystad Energy shared a report that shows the U.S. as now having the world’s largest reserve of recoverable oil, with 264 billion barrels in existing fields, unconventional shale and as-yet undiscovered areas. This is the first time such a report has moved the country ahead of both Saudi Arabia and Russia.

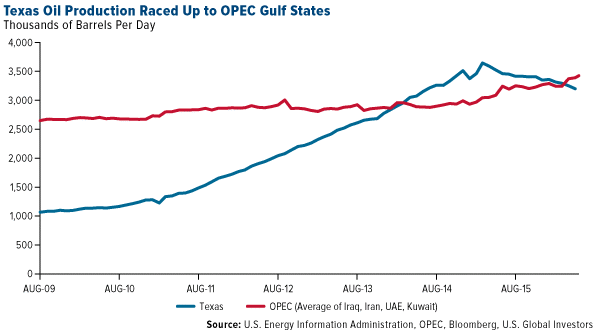

Were it not for the contributions of oil-rich Texas, however, this might not be the case. Thanks in large part to fracking in prolific fields such as the Eagle Ford Formation and Sprayberry Trend, the state leads all others in crude production, annually gushing out more than a third of total U.S. output.

You can see how the fracking boom helped propel the state into the same league as major OPEC nations Iraq, Iran, United Arab Emirates and Kuwait.

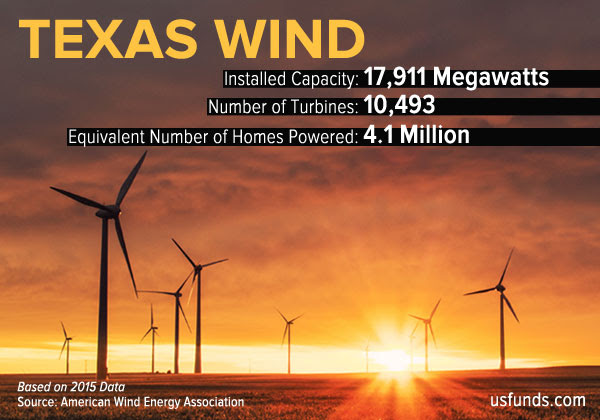

5. A Mighty Wind

Texas is more than oil, of course. The natural-resource-rich state is also known for its natural gas production (it leads the nation), coal, electricity (again, number one in the States) and renewable energy—specifically, wind energy.

Thanks to Competitive Renewable Energy Zones (CREZ) and $33 billion in invested capital, Texas ranks first in the nation for installed wind capacity and the number of megawatts generated by wind. In 2015, close to 10 percent of the state’s electricity production came from wind, according to the American Wind Energy Association.

With an estimated 17,000 Texans already employed in the state’s wind energy industry, Texas is in the process of installing an additional 5,200 megawatts.

6. Men at Work

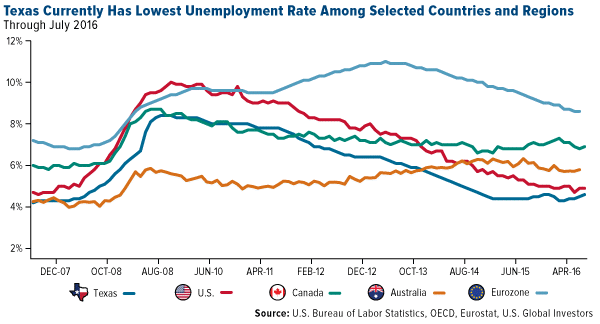

Speaking of employment, that’s something else you can find a lot of in the Lone Star State. The oil industry might have taken a hit from falling crude prices, but the Texas economy has proven resilient. As you can see, the 2007-2008 global financial crisis had much less of an impact on state unemployment rates compared to other major countries and regions such as Canada, Australia, the European Union and United States.

7. All Roads Lead to Texas

Important to keeping business and commerce flowing, as well as helping commuters travel to and from their work, are roads. Texas has them in spades. According to the U.S. Department of Transportation, the state is connected by 313,596 miles of public road, the most of any state. With 18 numbered interstate highways, it also has more interstate miles than any other does.

If it were its own country, Texas would rank 13th by road network size, somewhere between Germany and Sweden.

At only $0.20 per gallon, the Texas gas tax is among the most reasonable in the nation. And because almost that entire amount goes to public transportation—$0.05 is devoted to public education—Texas has some of the best roads in the U.S.

While we’re on the topic of transportation, Texas also boasts the most airports of any state—1,415, according to StateMaster. Two of the four major U.S. carriers, American Airlines and Southwest Airlines, are headquartered in the Lone Star State.

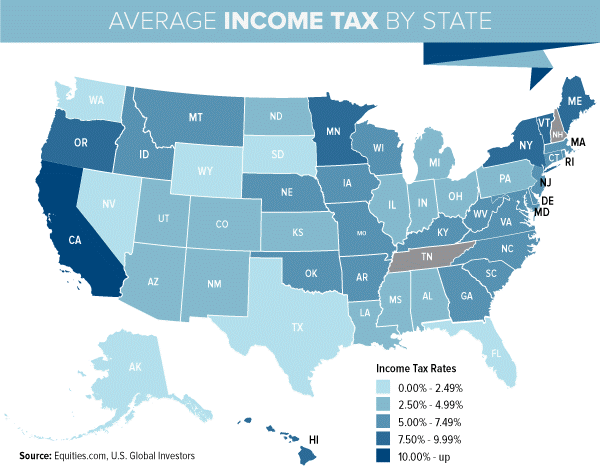

8. No Income Tax

There are only seven states without an income tax, Texas among them. (Alaska, Florida, Nevada, South Dakota, Washington and Wyoming round out the list.)

Neither does the state impose a corporate income tax, and last summer, Governor Gregg Abbott approved $4 billion in tax cuts for businesses and homeowners.

9. Gold Star State

Governor Abbott is also reponsible for what will be a first in the United States. More than a year after he signed a law to repatriate $1 billion in Texas gold bullion from the Federal Reserve, construction will soon begin on the Texas Bullion Depository. Such a state-run gold depository doesn’t currently exist anywhere else in the U.S. It’s hoped that it will help turn Texas into a “financial Mecca,” in the words of one state senator.

10. Population Destination

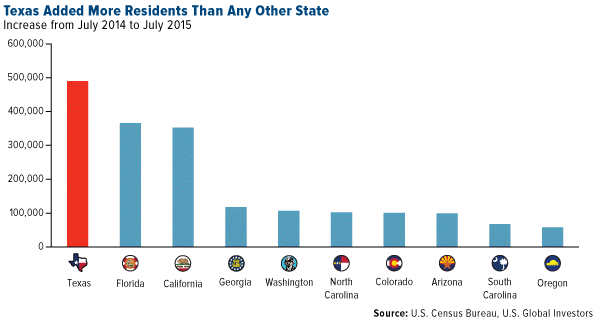

Low taxes are one of the main appeals driving Texas’ rapid population growth. According to the Census Bureau, five of the 11 fastest-growing U.S. cities by population can be found in Texas. Ranking number two in the nation is New Braunfels, a lovely town originally settled by Germans that lies midway between San Antonio and Austin.

Between July 2014 and July 2015, the Lone Star State added 490,036 new residents, the most of any state by a wide margin.

To put this in perspective, the number of new Texas arrivals alone between 2014 and 2015 exceeds the total populations of several countries, including Malta (population: 429,366, as of December 2014), Brunei (411,900, as of July 2014) and Iceland (336,060, as of June 2016).

11. Bet on Tech

It’s not just people moving to Texas, though. Companies are as well—specifically tech companies, and, to get even more granular, Silicon Valley tech companies. The San Francisco Chronicle reports that, in recent years, more than $1 billion in taxable income has flowed from the Bay Area to Texas, as tech firms have sought not just lower taxes but also simpler regulation.

Indeed, the Lone Star State has emerged as a formidable tech hub to rival Silicon Valley. Employing more than 270,000 people, the state’s tech industry supports firms ranging in size from hip Austin startups to massive Fortune 500 companies such as Dell, Texas Instruments and Rackspace Hosting (which just agreed to a $4.3 billion acquisition deal by private equity firm Apollo Global Management).

For the last three years, Texas has led the nation in high-tech exports—everything from semiconductors to communications equipment. Last year, in fact, the state’s total sales amount exceeded California’s by a whopping $6.3 billion.

No wonder so many people are choosing Texas as the place to hang their hat!

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average lost 0.85 percent. The S&P 500 Stock Index fell 0.68 percent, while the Nasdaq Composite fell 0.37 percent. The Russell 2000 small capitalization index gained 0.10 percent this week.

- The Hang Seng Composite dropped 0.25 percent this week; while Taiwan was up 1.08percent and the KOSPI fell 0.91 percent.

- The 10-year Treasury bond yield rose 4 basis points to 1.63 percent.

Domestic Equity Market

Strengths

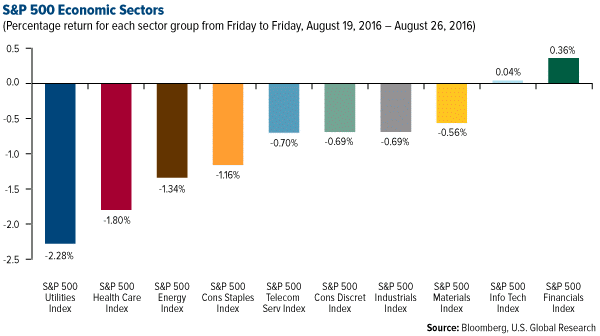

- Financials was the best performing sector for the week, increasing by 0.36 percent versus an overall decrease of -0.68 percent for the S&P 500.

- Best Buy was the best performing stock for the week, increasing 21.14 percent. The company crushed earnings and the stock leaped. Same store sales beat expectations, rising 0.8 percent compared to expectations of a 0.6 percent drop. Earnings per share also beat analysts' forecasts at $0.57 per share against projections of $0.43 per share.

- Toll Brothers, the luxury homebuilder, reported higher home orders, up 18.2 percent to 1,748 units from the year before. It also raised its projection for the average sale price to $840,000 to $850,000 from $820,000 to $850,000.

Weaknesses

- Utilities was the worst performing sector for the week, falling by -2.28 percent versus an overall decrease of -0.68 percent for the S&P 500.

- Dollar General was the worst performing stock for the week, falling -16.90 percent. The company posted revenue that missed analysts' estimates for the 2016 second quarter.

- Retailer Express missed on earnings and the stock dived. Shares fell as much as 25 percent after it posted earnings of $0.13 per share against analyst expectations of $0.17 per share. Sales also fell by 8 percent in stores open for more than one year compared to the same period in the prior year.

Opportunities

- America is driving more than ever. Data released by the Department of Energy shows that vehicles in the U.S. drove a record 1.58 trillion miles in the first half of 2016, up 3.3 percent from the same period last year. This is bullish for auto-parts companies as wear and tear from increased driving will drive higher replacement parts sales.

- Tesla CEO Elon Musk said Tuesday that the Model S and the Model X would offer batteries that will extend their ranges to 315 miles and 289 miles. Additionally, both models will receive an upgrade to their "Ludicrous Mode."

- Amazon is in the planning stages of a subscription music service that would run through its Echo hardware, Recode reports. Amazon is reportedly deciding whether the service will cost $4 or $5 a month.

Threats

- Short seller Carson Block announced a new target and the stock tanked. Block's Muddy Waters Investments said it is now short medical device maker St. Jude's Medical because the company has not spent enough to protect its pacemakers from being hacked and tampered with. The stock fell over 5 percent for the day following the report's release.

- Apple might owe Europe billions of dollars in taxes. The European Commission is expected to impose a judgment against the tech giant in the next few months; Apple is accused of striking a sweetheart tax deal with Ireland, and, per the Financial Times, JPMorgan says the judgment could be as high as $19 billion.

- A new study should have Coke and Pepsi terrified. The American Journal of Public Health found that the sugary-beverage tax of a penny per ounce in Berkeley, California, lowered consumption there by 21 percent.

The Economy and Bond Market

Strengths

- Durable goods orders rose 4.4 percent from the month before, higher than the 3.4 percent increase expected by economists.

- New home sales surged to 654,000, the highest level since October 2007. The number smashed expectations of 580,000 homes sold.

- Initial jobless claims unexpectedly dropped. The number of people requesting unemployment insurance fell to 261,000 from last week's 262,000. This is also lower than economists' expectations of 265,000.

Weaknesses

- Markit flash services PMI came in at 50.9, much lower than expectations of 51.8 and July's print of 51.4. This number is, however, still in expansionary territory.

- Sales of existing homes fell by 3.2 percent in August from the month before, well below economists’ expectations of a mere 0.4 percent drop.

- Japan remains trapped in deflation. Core CPI fell 0.5 percent in July, making for the lowest reading since March 2013.

Opportunities

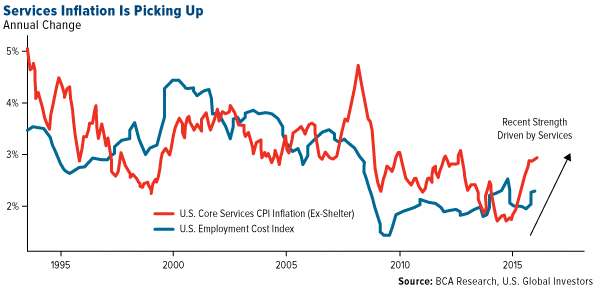

- While inflation remains below the Fed's target, it has also clearly bottomed for the cycle. Importantly, service sector inflation has rebounded sharply toward 3 percent. Given that service sector pricing is driven more clearly by domestic trends, this suggests that wage pressures are beginning to feed through into inflation. Accordingly, the BCA bond team recommends an overweight position in TIPS relative to nominal U.S. Treasuries. TIPS benefit even if the rise in inflation is gradual, but importantly, TIPS breakevens currently appear too low relative to other financial instruments.

- Stanley Fischer, the Federal Reserve vice chairman, says the Fed is nearing its targets. Speaking at a conference in Aspen, Colorado, Janet Yellen's right-hand man thinks the Fed is close to full employment and 2 percent inflation, the two parts of its dual mandate, Reuters reports.

- Next week is an important one for U.S. economic data. Personal consumption and perhaps more crucially, core PCE will be released on Monday.

Threats

- Home prices signaled a "potentially significant market shift." House prices in the U.S. only rose by 0.2 percent in June, below expectations of 0.3 percent, according to the Federal Housing Finance agency. Andrew Leventis, FHFA supervisory economist, said this slowing in house price appreciation was "a much more modest pace of appreciation than we've seen in some time"

- Markit's flash manufacturing PMI fell to 52.1, missing expectations of a 52.7 print. While this is still in expansionary territory and export data looked strong, weak order books during the month signaled a "warning light," according to Markit Chief Business Economist Chris Williamson.

- Saudi Arabia threw cold water on the prospects of a freeze to oil output. Khalid Al-Falih, the Saudi energy minister, told Reuters late Thursday that the kingdom didn't "believe any significant intervention in the market is necessary other than to allow the forces of supply and demand to do the work for us."

Gold Market

This week spot gold closed at $1,321.50, down $19.76 per ounce, or 1.47 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, fell 9.64 percent. Junior miners outperformed seniors for the week, as the S&P/TSX Venture Index fell 3.31 percent week. The U.S. Trade-Weighted Dollar Index was rose 1.00 percent, despite the rally on Friday.

| Date | Event | Survey | Actual | Prior |

|

Aug-23 |

U.S. New Home Sales |

580k |

654k |

582k |

|

Aug-25 |

Hong Kong Exports YoY |

-2.0% |

-5.1% |

-1.0% |

|

Aug-25 |

U.S. Durable Goods Orders |

3.4% |

4.4% |

-4.2% |

|

Aug-25 |

U.S. Initial Jobless Claims |

265k |

261k |

262k |

|

Aug-26 |

U.S. GDP Annualized QoQ |

1.1% |

1.1% |

1.2% |

|

Aug-30 |

Germany CPI YoY |

0.5% |

-- |

0.4% |

|

Aug-31 |

U.S. Consumer Confidence |

97.0 |

-- |

93.7 |

|

Aug-31 |

Eurozone CPI Core YoY |

0.9% |

-- |

0.9% |

|

Aug-31 |

ADP Employment Change |

175k |

-- |

179k |

|

Aug-23 |

Caixin China PMI Mfg |

50.1 |

-- |

50.6 |

|

Sep-1 |

U.S. Initial Jobless Claims |

265k |

-- |

261k |

|

Sep-1 |

U.S. ISM Manufacturing |

52.0 |

-- |

52.6 |

|

Sep-2 |

U.S. Change in Nonfarm Payrols |

185k |

-- |

255k |

|

Sep-2 |

U.S. Durable Goods Orders |

-- |

-- |

4.4% |

Strengths

- The best performing precious metal for the week was gold, down slightly by 1.47 percent. Current market conditions make it the perfect time to invest in gold, according to Heather Ferguson, an analyst at Hargreaves Landsown. “There is a fixed amount of this precious metal in the world so central banks are not able to manipulate the gold market like they can with bonds and cash,” Ferguson explains. “In the current environment of quantitative easing and increasingly extreme monetary policy, gold is highly sought after.”

- UBS says the gold trade is not overcrowded, according to a note this week. The group believes that Federal Reserve policy decisions relative to the metal are not as straightforward in this environment where global yields are under pressure ahead of a rate hike.

- Citigroup is also positive on the metal, raising its forecast for the second half of the year. The group cites elevated levels of U.S. election uncertainty and stickiness of ETF and hedge fund flows into gold products, reports Bloomberg.

Weaknesses

- The worst performing precious metal for the week was platinum with a loss of 3.77 percent. Platinum sold off when precious metals were bear raided on Wednesday, but did not get much of a bounce following Yellen’s speech on Friday.

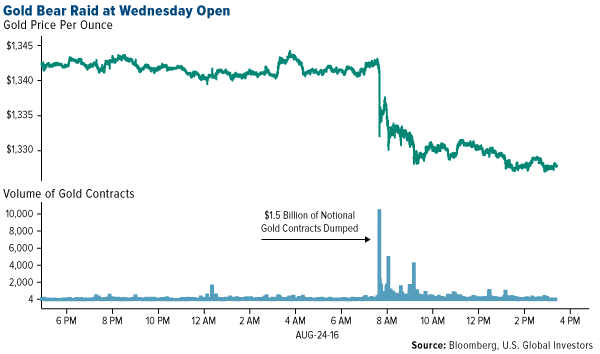

- “The past 48 hours have been an interesting period for gold…” writes Steven Knight of Blackwell Global. “As the metal has again seemingly fallen sharply following the liquidation of a $1.5 billion futures position over the course of 60 seconds.” According to Knight, given the amount of gold derivatives floating around, the fairness of the COMEX exchange likely needs an additional level of scrutiny. In addition, the timing of this “flash crash” could potentially be revealing.

- Goldcorp fell the most in six months, reports Bloomberg, on the back of retreating gold prices and the discovery of a leak at the company’s mine in Mexico. Less-than-stellar news was also reported from Kinross Gold Corp this week, as it suspended operations at a mine in Chile ahead of schedule due to a dispute involving water use (causing 300 workers at the Maricunga mine to be laid off as a result). Lastly, Orezone Gold Corp told investors on Monday that it will likely slash the gold resources at its Bombore project by a staggering 30 percent, reports the National Post.

Opportunities

- When viewed against the aggregate balance sheet of the “big four” global central banks (Fed, ECB, BoJ and PBOC), the argument can be made if we view gold as a currency, that the metal is worth closer to $1,700 an ounce (versus the spot price of $1,326 an ounce USD), says Deutsche Bank. Over the same period that the aggregate central bank balance sheet expanded 300 percent, the bank continues, global above ground stocks grew by 19 percent in tonnage terms.

- More than 500 million people are living in a climate of negative central-bank interest rates, according to a study by Standard & Poor’s cited by HSBC this week. This represents around 25 percent of global GDP and is a clear sign of “economic and policy desperation,” – a bullish factor for gold. Francisco Blanch of Bank of America agrees, stating that central banks “are very scared of hiking rates and that is a very good story for gold.”

- “Although we have seen a significant rally in gold, I think investors should still consider an allocation to the precious metal,” Nick Peters, multi-asset investor at Fidelity, said. He continues by explaining that gold can function as a safe haven during times of market volatility and provide strong countervailing returns to equities.

Threats

- The Reserve Bank announced today that sovereign gold bonds issued in February and March can be traded on stock exchanges starting Monday. Four tranches of the bonds have already been issued, with a fifth likely to be issued next month. Sovereign gold bonds provide an alternative to actual gold investing, offering investors a choice to buy bonds worth 2 grams of gold going up to a maximum of 500 grams. The bonds are denominated in gold and pay 2.75 percent interest in physical gold.

- Are the positive changes in the gold industry sustainable? This was the point of question from Gold Fields CEO Nick Holland during a keynote presentation on Monday, reports Mineweb.com. Holland points out that not only are companies cutting “fat,” but “muscle” as well. Stay-in-business capital (as a percent of operating expenditure) decreased from 46 percent in 2012 on a per ounce basis, to 26 percent in 2015. How can companies do this? “I believe that they have merely deferred capital that is going to come back, because if you want to sustain the business into the future, you need to spend the money,” Holland said. “That for me is a little bit of a concern.” The Industry is going to play catch up, which could yield poor capital allocation decisions, particularly if the industry errors on the side of growing production ounces versus growing profitability.

- In a note from BMO Private Bank this week, Jack Ablin points out that historically, options investors have been able to generate reasonable income by selling options to other investors looking for downside protection and upside opportunity. However, struggling yields have created an “outsized supply of yield-seeking options sellers who collectively outstrip buyers.” The result is that implied volatility has declined. But just because yields are low, doesn’t mean that actual risk has gone away, the note continues.

Energy and Natural Resources Market

Strengths

- Chinese July gold imports rose 20 percent from a year ago. Macquarie Research reports that gold imports were 126 tonnes in July, using data from Chinese Customs. Physical demand rose despite an 18 percent higher gold price, a positive sign for the yellow metal, which has suffered somewhat weak physical demand from India this year.

- The best performing sector for the week was the S&P Supercomposite Paper and Forest Products Index. The index rose 2.6 percent on the back of strong housing data, which showed new home sales reached at a nine-year high.

- Syngenta AG, a Swiss major fertilizer and chemicals producer, was the best performing stock in the broader natural resource space for the week. The stock gained 9.1 percent after a U.S. committee cleared the proposed $44 billion acquisition by ChemChina.

Weaknesses

- Crude inventories continue to rise, suggesting oil market remains oversupplied. This week's petroleum inventories update was bearish relative to consensus. Crude, gasoline, and distillates stockpiles rose by 2.7 million barrels, vs. consensus estimates for a draw of 2.1 million barrels.

- The worst-performing sector for the week was the NYSE Arca Gold Miners Index. The index of major gold producers dropped 9.5 percent for the week, underperforming the commodity which dropped 1.5 percent for the same period. The weakness has been attributed to increasing expectations for a Fed rate hike as the Fed governors gathered in Jackson Hole for their annual symposium.

- The worst performing stock for the week in the broader natural resource space was Goldcorp Inc. The major Canadian gold producer dropped 12.5 percent after tracking the weakness in gold prices. In addition, the company reported operational issues at one of its Mexican mines.

Opportunities

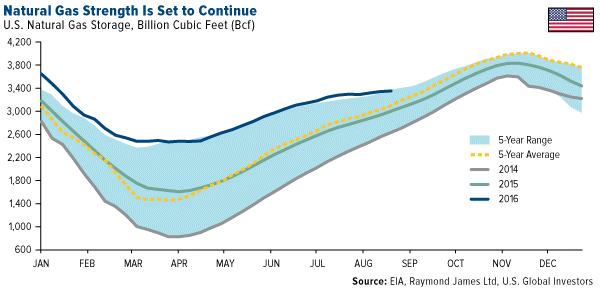

- Natural gas strength is set to continue as inventories have fallen back within normal range. Last week’s 11 billion cubic feet (bcf) build was well below the five-year average of 66 bcf and is the smallest injection for this time of year on record. Raymond James analysts highlighted that the small injection brings total inventories back within their five-year range. In addition, the gas-directed rig count has tumbled to an all time low, with only 81 active rigs, suggesting supply will remain tight.

- China’s trade data for July suggests demand for raw commodities remains healthy. Zinc and copper concentrate imports picked up strongly in July. Coal and ferronickel imports came in better than expected. According to Macquarie commodities analysts, the data suggests the Chinese demand picture seen this year.

- The paper and forest industry may see continued strength from strong housing data. Data out this week shows new home sales surged to the best level since 2007. The Census Bureau reported new home sales rose 12.4 percent in July to 654,000 units, the strongest print since October 2007.

Threats

- Selling pressure in crude intensifies as Saudi Arabia downplays OPEC deal. In an interview with Reuters, Saudi Arabia’s oil minister Khalid al-Falih said that he did not think that intervention in the oil market was necessary, raising questions about the viability of a deal in Algeria next month between OPEC and Russia. As OilPrice.com reports, the comments throw cold water on the chances of a freeze deal.

- The thermal coal strength may fade as weak European data outweighs positive news in China. As Deutsche Bank analysts point out, the decrease in seaborne demand from the UK and Netherlands is being felt by suppliers from Colombia to Russia. European imports are tracking 17.4 million tonnes below last year’s levels, far outweighing the growing demand in China, which is up only 0.7 million tonnes.

- The iron ore rally remains at risk as China takes steps to curtail steel capacity. China Iron & Steel Association argues that steel production in the Asian country will contract this year and shrink further in 2017 as local demand slows. Lower steel output threatens to reduce iron ore demand at a time when Chinese iron ore inventories are near all time highs.

China Region

Strengths

- August Vietnamese trade data beat expectations as exports came in slightly better than anticipated, rising 5.5 percent year-over-year, while imports fell less than expected, dropping only 0.3 percent year-over-year.

- Taiwan’s TAIEX was a top regional performer for the week, rising 1.19 percent over the last five trading days.

- The South Korean won eked out a small total return for the week, among the best regional currencies in a week that saw most regional currencies weaken against the U.S. dollar.

Weaknesses

- In another otherwise quiet week for Chinese data, the Shanghai Composite fell 1.21 percent amid a slew of earnings reports and some difficult comps versus year-ago numbers.

- Year-over-year industrial production in Taiwan missed expectations for a gain of 1.7 percent, declining instead by 0.31 percent.

- The weakest performer in the HSCI Index this week was Zhuzhou CRRC Times Electric Co. Ltd. (3898 HK), which fell more than 17 percent over the last five days after the company reported worse-than-expected earnings and received a number of broker downgrades.

Opportunities

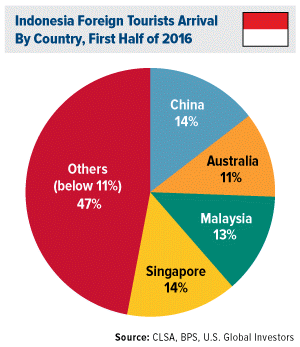

click to enlarge |

- For the first time during the first half of 2016, the number of Chinese tourists to Indonesia surpassed those of any other single nation, CLSA mentioned in a recent report on Indonesian tourism. Chinese visitor arrivals slightly edged out those from Indonesia’s neighboring city-state, Singapore.

- Foreign acquisitions continue to remain relevant for Chinese firms in this record-breaking year, as Jianxi Copper, China’s biggest copper producer, reported that it too will look to M&A overseas after lower metal prices ate into its first-half profits.

- Bloomberg reports that the Shenzhen and Hong Kong stock exchanges plan to seek input from market participants in coming weeks as they finish drafting preliminary rules for the new HK-Shenzhen stock connect program.

Threats

- President Rodrigo Duterte and the Philippines made headlines once again this week after the recently-elected populist president threatened to leave the United Nations over criticisms for his violent crackdown against drugs.

- Bloomberg reported that insurer China Life (2628 HK) suggests it will limit equities exposure in the second half of 2016, attempting instead to boost fixed income and alternative investments while boosting overseas properties.

- Forest fires in Indonesia have led to a state of emergency in six provinces in that island nation. The smoke is also pushing down Singaporean and southern Malaysia’s air quality to unhealthy levels.

Emerging Europe

Strengths

- Russia was the best performing country this week, gaining 1.7 percent. Gains in the Moscow Stock Exchange were led by strong Sberbank performance. Sberbank almost tripled its profits in the second quarter, boosted by a drop in bad loans and signs of an economic recovery. This year’s 61-percent rally in London trading of Sberbank shares has boosted the market capitalization of Russia’s biggest lender to $50.3 billion, surpassing that of Gazprom PJSC’s depository receipts for the first time ever.

- The Hungarian forint was the best relative currency this week, losing 65 basis points against the U.S. dollar. Emerging Europe currencies weakened as the dollar climbed higher on Friday after the Federal Reserve commented that the case for a rate hike has strengthened in recent months.

- The health care sector was the best performing sector among Eastern European markets this week.

Weaknesses

- Turkey was the worst performing market this week, losing 1.3 percent. Fitch revised its outlook to negative from stable on 18 Turkish banks. This is a consequence of the ratings agency’s revision of the outlook on Turkey’s sovereignty to negative from stable on August 19. Political tension after the failed coup attempt and increased military activity puts pressure on equities.

- The Russian ruble was the worst performing currency this week, losing 1.5 percent against the U.S. dollar. Ruble price movement is highly correlated with the price of oil; Brent crude oil lost 2.3 percent during the same period.

- The industrial sector was the worst performing sector among Eastern European markets this week.

Opportunities

- Turkey proposed a national wealth fund, totaling as much as $200 billion, which would finance projects including airports, seaports, roads and railroads across the country. The government planned the wealth fund after a failed coup attempt on July 15. It will include sate-owned companies and lands, as well as proceeds from privatization. Most importantly, it will finance transport projects.

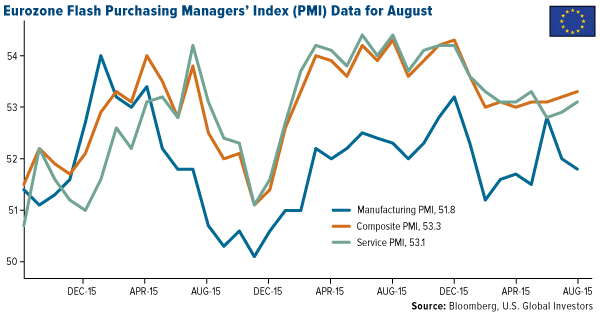

- The August flash purchasing managers’ index (PMI) indicates that the eurozone remains on a steady growth path in the third quarter, with no signs of recovery being derailed by Brexit uncertainty. Eurozone Composite PMI, which gives an overview of the Service and Manufacturing PMI, was reported at 53.3 versus the prior figure of 53.2.

- Poland sold its first bond in yuan currency to reduce its reliance on European investors and seize on growing demand from Asia. The 3 billion yuan ($450 million) notes, due August 2019, were priced to yield at 3.4 percent. The issuance ultimately allows Poland to diversify its funding sources.

Threats

- According to the Russian newspaper Vedomsti, the decision to increase oil and gas sector taxes in 2017 has been made. Details on the additional Mineral Extraction Tax will likely be released in September or October as part of next year’s budget preparation. What is known now is that the government aims to collect extra RUB 200 billion from the oil sectors and RUB 170 billion from Gazprom. Pavel Kushnir from Deutsche Bank comments that the oil sector in Russia remains profitable and cash generative due to positive effects of the ruble devaluation and progressive tax system, although the extra tax will put pressure on revenue.

- Moody’s Investors Service said that Poland’s escalating political crisis threatens investment spending and economic development. The crisis over Poland’s constitutional court is “credit negative” as it escalates tension with the European Union and tempers growth. Moody’s cut its outlook on Poland’s A2 rating to negative in May and is scheduled to review the country’s sovereign rating in two weeks.

- FICO’s Credit Health Index, which measures Russia’s overall credit health based on the number of consumer loans that are overdue by more than 60 days, was at 90 last month, unchanged since July 2015 and the highest since it began compiling data in 2007. Many analysts predict that Russia will return to growth by the end of this year, but the decline in real incomes will continue to put pressure on people’s ability to repay debt, according to Russia’s National Bureau of Credit Histories.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| DJIA | 18,395.40 | -157.17 | -0.85% |

| S&P 500 | 2,169.04 | -14.83 | -0.68% |

| S&P Energy | 511.22 | -6.93 | -1.34% |

| S&P Basic Materials | 305.00 | -1.72 | -0.56% |

| Nasdaq | 5,218.92 | -19.46 | -0.37% |

| Russell 2000 | 1,238.03 | +1.26 | +0.10% |

| Hang Seng Composite Index | 3,089.27 | -7.72 | -0.25% |

| Korean KOSPI Index | 2,037.50 | -18.74 | -0.91% |

| S&P/TSX Global Gold Index | 240.68 | -23.85 | -9.02% |

| XAU | 95.80 | -11.89 | -11.04% |

| Gold Futures | 1,324.40 | -21.80 | -1.62% |

| Oil Futures | 47.38 | -1.14 | -2.35% |

| Natural Gas Futures | 2.86 | +0.27 | +10.53% |

| 10-Yr Treasury Bond | 1.63 | +0.05 | +2.91% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| DJIA | 18,395.40 | -76.77 | -0.42% |

| S&P 500 | 2,169.04 | +2.46 | +0.11% |

| S&P Energy | 511.22 | +11.78 | +2.36% |

| S&P Basic Materials | 305.00 | -2.02 | -0.66% |

| Nasdaq | 5,218.92 | +79.11 | +1.54% |

| Russell 2000 | 1,238.03 | +19.10 | +1.57% |

| Hang Seng Composite Index | 3,089.27 | +109.03 | +3.66% |

| Korean KOSPI Index | 2,037.50 | +12.45 | +0.61% |

| S&P/TSX Global Gold Index | 240.68 | -30.50 | -11.25% |

| XAU | 95.80 | -11.79 | -10.96% |

| Gold Futures | 1,324.40 | -10.10 | -0.76% |

| Oil Futures | 47.38 | +5.46 | +13.02% |

| Natural Gas Futures | 2.86 | +0.18 | +6.89% |

| 10-Yr Treasury Bond | 1.63 | +0.13 | +8.48% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| DJIA | 18,395.40 | +522.18 | +2.92% |

| S&P 500 | 2,169.04 | +69.98 | +3.33% |

| S&P Energy | 511.22 | +11.84 | +2.37% |

| S&P Basic Materials | 305.00 | +9.42 | +3.19% |

| Nasdaq | 5,218.92 | +285.41 | +5.79% |

| Russell 2000 | 1,238.03 | +87.58 | +7.61% |

| Hang Seng Composite Index | 3,089.27 | +300.02 | +10.76% |

| Korean KOSPI Index | 2,037.50 | +68.33 | +3.47% |

| S&P/TSX Global Gold Index | 240.68 | +36.31 | +17.77% |

| XAU | 95.80 | +16.39 | +20.64% |

| Gold Futures | 1,324.40 | +102.40 | +8.38% |

| Oil Futures | 47.38 | -1.95 | -3.95% |

| Natural Gas Futures | 2.86 | +0.69 | +31.67% |

| 10-Yr Treasury Bond | 1.63 | -0.23 | -12.26% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of 06/30/2016:

China Life Insurance Co Ltd/Ta

Gazprom PJSC

Newmont Mining

Sberbank of Russia PJSC

Syngenta AG

American Airlines

Southwest Airlines

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.

The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months.

The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.

The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500.

The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500.

The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500.

The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500.

The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500.

The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500.

The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The "core" PCE price index is defined as personal consumption expenditures (PCE) prices excluding food and energy prices.

The employment cost index (ECI) is a quarterly economic series detailing the changes in the costs of labor for businesses in the United States economy.

The COMEX is a commodity exchange in New York City formed by the merger of four past exchanges. The exchange trades futures in sugar, coffee, petroleum, metals and financial instruments.

FICO’s Credit Health Index measures Russia’s overall credit health based on the number of consumer loans that are overdue by more than 60 days.

The S&P Supercomposite Paper & Forest Products Index is a capitalization-weighted index.

The TAIEX Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The Shanghai Composite Index (SSE) is an index of all stocks that trade on the Shanghai Stock Exchange.