Seasoned readers are familiar with our use of point-and-figure charts as a tool in our investment process to both 1. find ideas in our Knowledge Leaders universe that bear further analysis and 2. give us a clear signal when a position begins to underperform, warranting a sale.

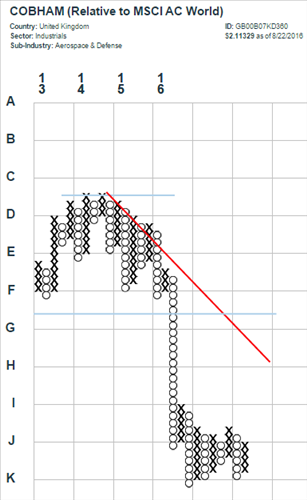

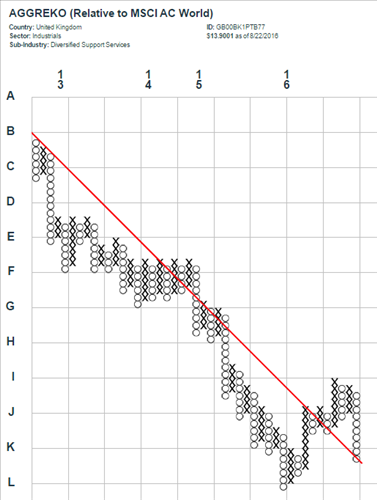

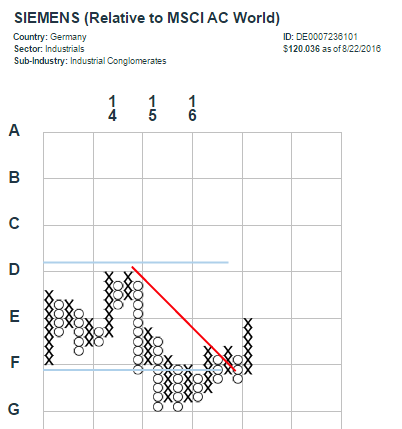

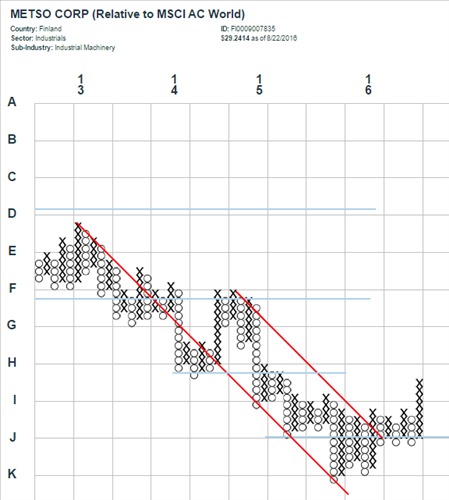

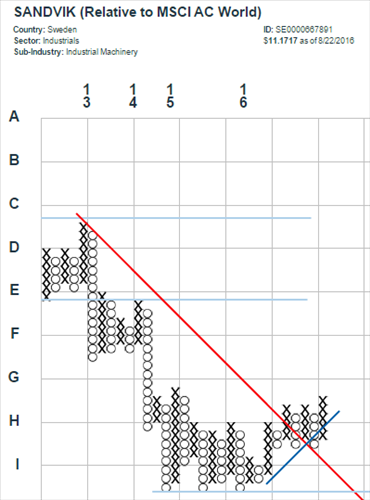

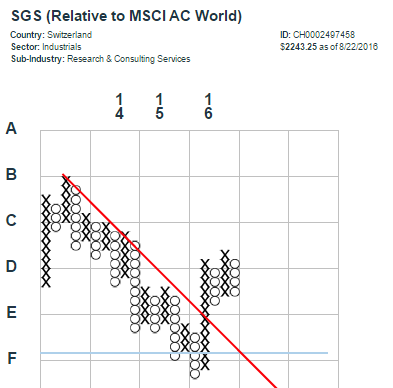

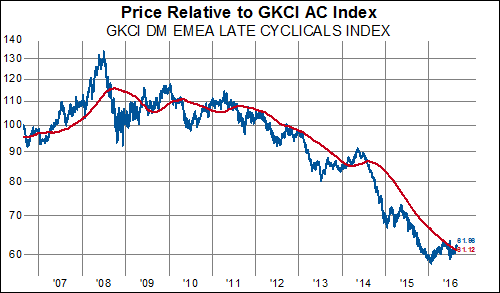

More recently, this review of our Knowledge Leaders has yielded a somewhat unexpected result: the relative outperformance of DM EMEA Late Cyclicals, particularly those in the Industrials sector. Say what?? To be sure, there is no shortage of relative strength charts like this one:

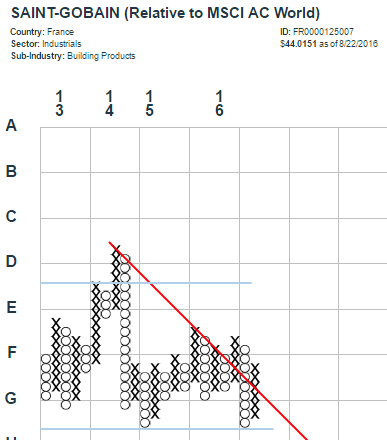

However, there seem to be increasing numbers of charts that suggest the opportunity for a turn for the better.

EMEA Industrials

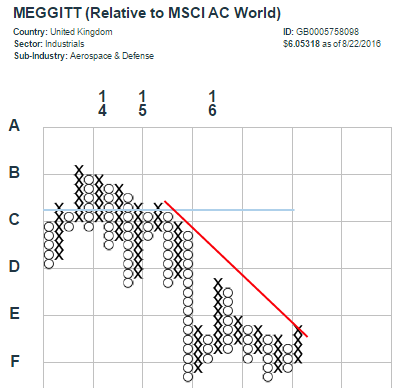

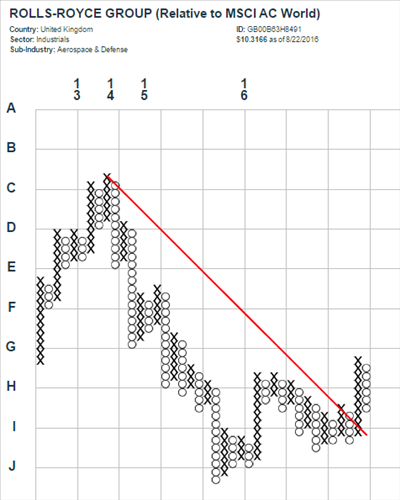

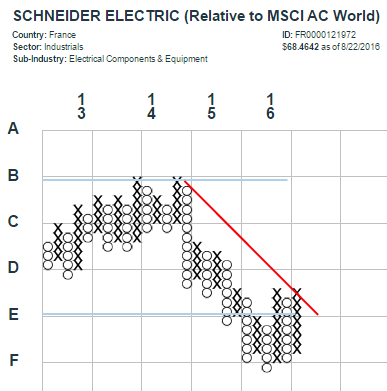

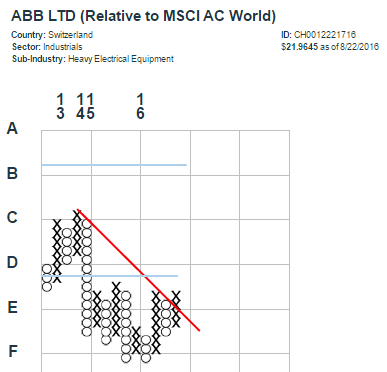

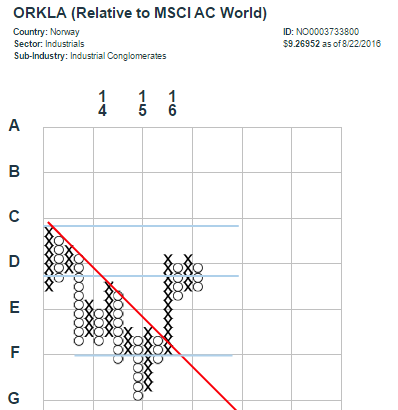

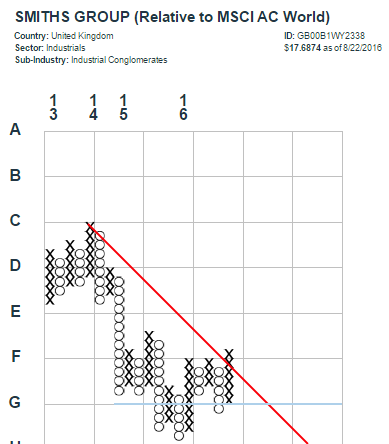

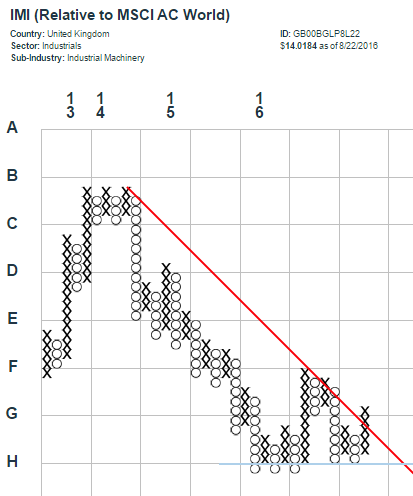

Some of these names have managed to more definitively break through their respective downtrend resistance (red) lines (here’s looking at you Rolls-Royce, Orkla, Siemens, Sandvik, SGS) while others have yet to confirm a major change in trend (Meggitt, Schneider, ABB, Smiths, IMI). Since important changes in market leadership are typically marked by widespread participation of group members, it is not unreasonable to assume this positive relative outperformance will continue for DM EMEA Industrials.

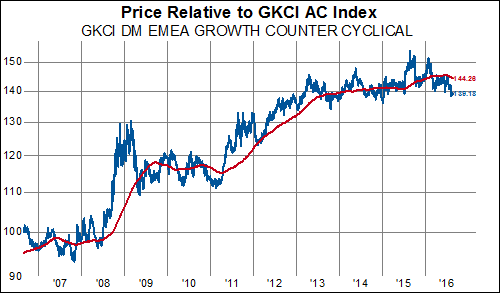

Indeed, the growth counter-cyclical groups that have lead this bull market (Consumer Staples and Health Care stocks) appear to be taking a breather after achieving a 50% gain relative to the GKCI All Country Index over the last decade:

All while DM EMEA Late Cyclicals (Industrials, Materials, Energy) seem to have found some support at the beginning this year, following a decade-long relative underperformance of 40%:

Seems clear enough, you might be saying to yourself. Is it really, though?

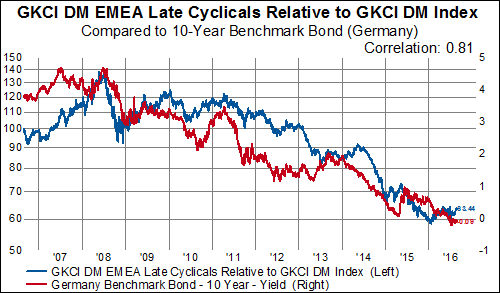

Consider, for a moment, the relationships and correlations that would seem to have to shift dramatically in order to confirm a true change in leadership. Falling rates and DM EMEA Late Cyclicals underperformance have an 80%+ correlation over the last ten years. Either that relationship breaks down or rates would have to rise in order to be consistent with a rebound in Late Cyclical stocks.

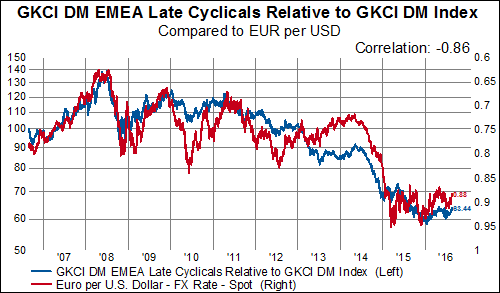

Similarly, there is an 80%+ correlation between the underperformance of DM EMEA Late Cyclicals and weakening EURUSD. If you are confident the USD is poised to fall significantly versus the euro, then it is reasonable to bet on a turnaround for the group.

So how do we square the very clear bounce in these DM EMEA Late Cyclicals with the somewhat dubious proposition that decade-long relationships are about to breakdown completely (or rates are going to rise consistently as the dollar embarks on a weakening trend)? One of the most simple explanations is investors’ hunt for yield.

While DM EMEA Growth Counter-Cyclicals have dominated consistent dividend increases over the last decade…

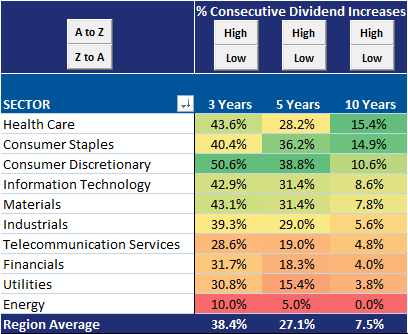

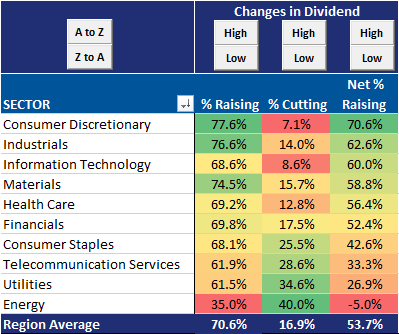

The groups increasing dividends more recently are concentrated in Cyclical sectors:

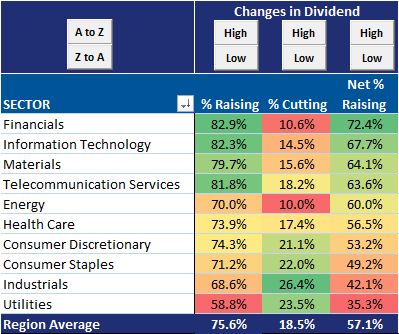

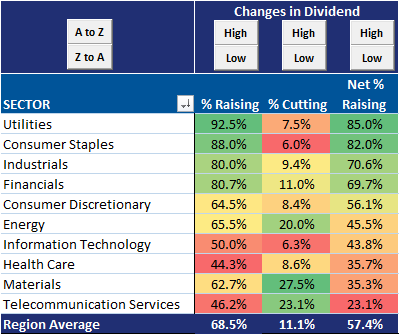

More than 75% of DM EMEA Industrials companies are raising their dividend. When we compare the sectoral distribution to other regions, we find a somewhat different picture as dividend increases in DM Asia are dominated by Hyper Cyclicals (Financials and Information Technology) while those in DM Americas are concentrated in defensive sectors like Utilities and Consumer Staples.

DM Asia

DM Americas

Bottom line, DM EMEA Industrials look interesting BUT we need to remain mindful of the driving forces behind their improved relative performance.