This week’s calendar features yet another light week for data, a lot of politics, and slow summer trading. Something has to fill all of that air time! This week the punditry gets their favorite topic – the Fed. Chair Yellen’s speech on Friday may set the tone for post-election monetary policy. Sometimes there is also a presentation from a non-Fed economist that challenges current policy. Will there be a showdown at Jackson Hole?

Last Week

The important economic news was positive. Despite the impending options expiration, the big story was the lack of action. There has not been a daily 1% move since early July. This is much lower than the normal August volatility. (LPL)

Theme Recap

In my last WTWA, I predicted discussion about whether the oil price/stock price relationship was at an end. My claim is that there was never a solid basis for the correlation, despite the intense focus by traders. It was a good guess about a topic in a quiet week. (A typical example). Both TV and print journalists kept citing oil prices as influences on daily trading. The real story was the lack of volatility. Last week the dead air was filled with a sandwich promotion. This week the news was about a reported theft from athletes at the Olympics. I understand why this story is important for athletics, the host country, the Olympic rules, endorsements and other angles. It has little importance for financial markets. The attention it got highlights the lack of other news.

The Story in One Chart Short

I always start my personal review of the week by looking at this great chart from Doug Short. The overall range is very narrow, with stocks remaining near record highs. Doug has a special knack for pulling together all of the relevant information. His charts save more than a thousand words! Read his entire post where he adds analysis and several other charts providing long-term perspective.

The News

Each week I break down events into good and bad. Often there is an “ugly” and on rare occasion something really good. My working definition of “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

The Good

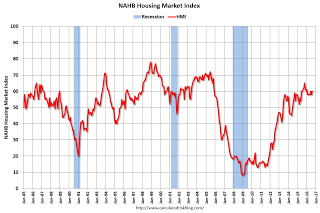

- Homebuilder sentiment was strong again at 60, an increase over 58 in July.

- Initial jobless claims fell 4000 to 262K. Claims have now been below 300K for 76 weeks. (Jeffry Bartash, MarketWatch).

- The first post-Brexit news is positive, as UK employment is stronger than expected (FT).

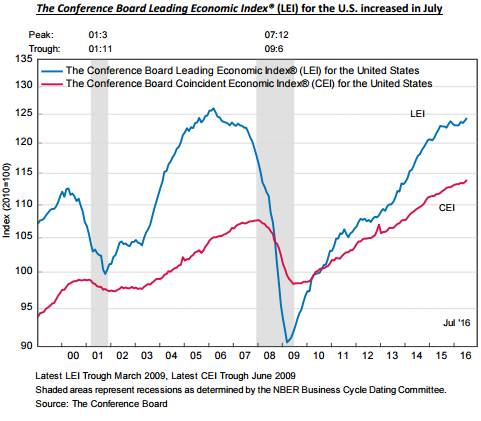

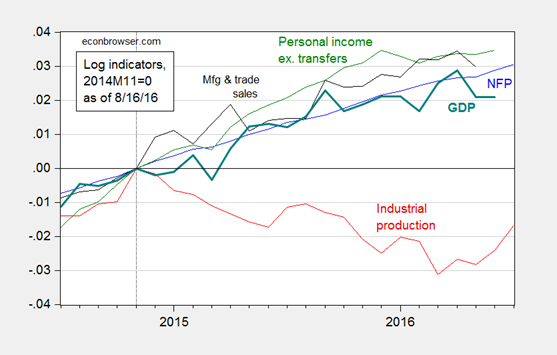

- Leading Economic Indicators rose 0.4 percent. This signals continuing slow growth for the next six months. Steven Hansen provides analysis and this chart:

- Industrial production continued the recent rebound, up 0.7% in July. Calculated Risk has the story.

- July housing starts – another “solid report” via (Calculated Risk).

The Bad

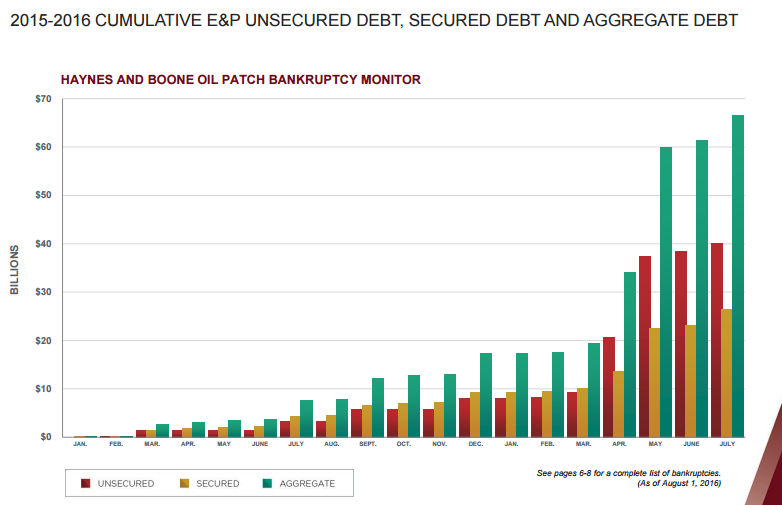

- Oil bankruptcies increased. Rupert Hargreaves provides the relevant data, including this chart.

- Fed Facebook page. Undaunted by the prior efforts at transparency, the Fed has launched a Facebook page. This will not end well.

The Ugly

Serious consequences from bad information. Here are two quite different examples.

- The government believes you to be dead and your benefits are ended. What next?

- Airline passengers, conditioned by recent events, hear something perceived as a shot. An incredible stampede at JFK results.

The Silver Bullet

I occasionally give the Silver Bullet award to someone who takes up an unpopular or thankless cause, doing the real work to demonstrate the facts. No award this week. Nominations always welcome! For ideas, go to your favorite conspiracy site and look for people doing data mining and/or poets writing about economics.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react. That is the purpose of considering possible themes for the week ahead. You can make your own predictions in the comments.

The Calendar

We have another rather slow week for economic data, but plenty of impending big news. While personally I watch everything on the calendar, I highlight only the most important items in WTWA. Focus is essential.

The “A” List

- New Home Sales (T). A good read on an important sector.

- Michigan Sentiment (F). The only concurrent data on job creation and spending.

- Durable Goods Orders (Th). Volatile July data is relevant to confirm the industrial rebound.

- Initial claims (Th). The best concurrent indicator for employment trends.

The “B” List

- Existing home sales (W). Not as important as new homes, but a solid indicator for the overall market.

- GDP – 2nd estimate for Q2 (F). Old news, but it will be the base for evaluating the rest of the year.

- Crude inventories (W). Often has a significant impact on oil markets, a focal point for traders of everything.

The big news will be the Yellen presentation at Jackson Hole. Markets will get a hint when the specific topics are announced on Thursday.

Next Week’s Theme

This week’s quiet trading might end with a bang. The Kansas City Fed’s annual Jackson Hole conference attracts economists and central bankers from around the world. There may be exploration of new policy ideas or hints at new policy directions. This is especially true when the Fed Chair is speaking. It is not a single, unified message. Some presentations may well feature dissenting viewpoints. While it provides food for the punditry, many market participants would prefer a clear policy statement from a single voice. Instead, everyone will be wondering: Will there be a showdown at Jackson Hole?

Several viewpoints have already emerged.

- The conference generally has little market impact, even when the Fed Chair speaks.

- Too many voices mean there will be no clear message.

- The presentations will be too theoretical to be meaningful.

- Sometimes the Conference highlights the start of new plans – Bernanke’s hints about Quantitative Easing come to mind.

- A spirited discussion will sharpen opinions on all sides.

- The odds on near-term rate increases will be better understood.

There are many proponents for each. Feel free to add your own thoughts in the comments, including anything I have missed.

As always, I’ll have a few ideas of my own in the conclusion.

Quant Corner

We follow some regular great sources and also the best insights from each week.

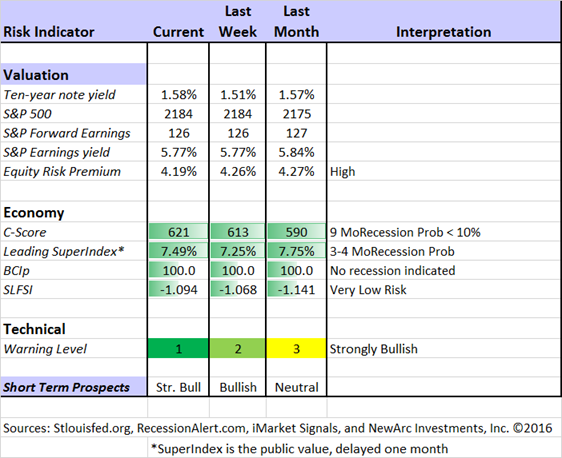

Risk Analysis

Whether you are a trader or an investor, you need to understand risk. Risk first, rewards second. I monitor many quantitative reports and highlight the best methods in this weekly update.

The Indicator Snapshot

The Featured Sources:

Brian Gilmartin: Analysis of expected earnings for the overall market as well as coverage of many individual companies. This week he expresses more confidence about growth in earnings.

Bob Dieli: The “C Score” which is a weekly estimate of his Enhanced Aggregate Spread (the most accurate real-time recession forecasting method over the last few decades). His subscribers get Monthly reports including both an economic overview of the economy and employment.

The recession odds (in nine months) have nudged closer to 10%.

Holmes: Our cautious and clever watchdog, who sniffs out opportunity like a great detective, but emphasizes guarding assets.

Doug Short: The Big Four Update, the World Markets Weekend Update (and much more).

The ECRI has been dropped from our weekly update. It was not so much because of the bad call in 2011, but the stubborn adherence to this position despite plenty of evidence to the contrary. Those interested can still follow them via Doug Short and Jill Mislinski. The ECRI commentary remains relentlessly bearish despite the upturn in their own index.

Georg Vrba: The Business Cycle Indicator, and much more. Check out his site for an array of interesting methods. Georg regularly analyzes Bob Dieli’s enhanced aggregate spread, considering when it might first give a recession signal. Georg thinks it is still a year away. It is interesting to watch this approach along with our weekly monitoring of the C-Score.

RecessionAlert: Many strong quantitative indicators for both economic and market analysis. While we feature his recession analysis, Dwaine also has a number of interesting approaches to asset allocation.

In addition to my first-rate collection of recession watchers – selected as the best in my 2011 analysis – I always monitor other ideas. Here are some key viewpoints:

- The St. Louis Fed (via GEI, which does a great job of highlighting relevant Fed sources) has a balanced analysis, taking note of the recent weakness in GDP. Examining and rejecting the possibility of a current business cycle peak (the official start of a recession), they conclude: “…(T)he available evidence suggests that the economy, though exhibiting stubbornly weak real GDP growth, continued to expand heading into the second half of 2016.”

- Menzie Chinn updates his version of the Big Four indicators used by the NBER for recession dating. He notes the improvement in industrial production, and the impact on the overall assessment.

- Bill McBride, who has had an excellent record through the financial crisis and recovery, still sees no recession through the next half of 2017, in line with our own experts.

How to Use WTWA

In this series I share my preparation for the coming week. I write each post as if I were speaking directly to one of my clients. For most readers, they can just “listen in.” If you are unhappy with your current investment approach, we will be happy to talk with you. I start with a specific assessment of your personal situation. There is no rush. Each client is different, so I have six different programs ranging from very conservative bond ladders to very aggressive trading programs. A key question:

Are you preserving wealth, or like most of us, do you need to create more wealth?

My objective is to help all readers, so I provide a number of free resources. Just write to info at newarc dot com. We will send whatever you request. We never share your email address with others, and send only what you seek. (Like you, we hate spam!) Free reports include the following:

- Understanding Risk – what we all should know.

- Income investing – better yield than the standard dividend portfolio, and also less risk.

- Holmes – the top artificial intelligence techniques in action.

- Why 2016 could be the Year for Value Stocks – finding cheap stocks based on long-term earnings.

You can also check out my website for Tips for Individual Investors, and a discussion of the biggest market fears. (I welcome questions or suggestions for new topics.)

Best Advice for the Week Ahead

The right move often depends on your time horizon. Are you a trader or an investor?

Insight for Traders

We consider both our models and also the best advice from sources we follow.

Felix and Holmes

We have moved to a strongly bullish market forecast. Felix is fully invested, including several aggressive sectors. The more cautious Holmes is now also fully invested.

Top Trading Advice

Should aspiring traders start with “paper trades.” Tadas Viskanta explains why it is better to have some money on the line – even if it is a small amount.

You can appreciate such an experience by watching Adam H. Grimes and the “reality show” involving a beginning trader.

Have traditional market signals lost their value? (Conor Sen)

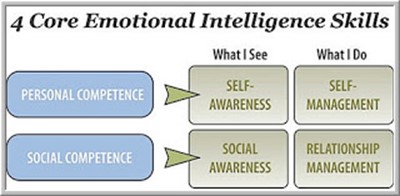

Dr. Brett Steenbarger had a great week of posts. They are all worth reading and all have ideas you are unlikely to see elsewhere. Two of my favorites:

- Do you have talent for trading? Here is how to awaken it?

- Do you understand emotionally intelligent trading?

Insight for Investors

Investors have a longer time horizon. The best moves frequently involve taking advantage of trading volatility!

Best of the Week

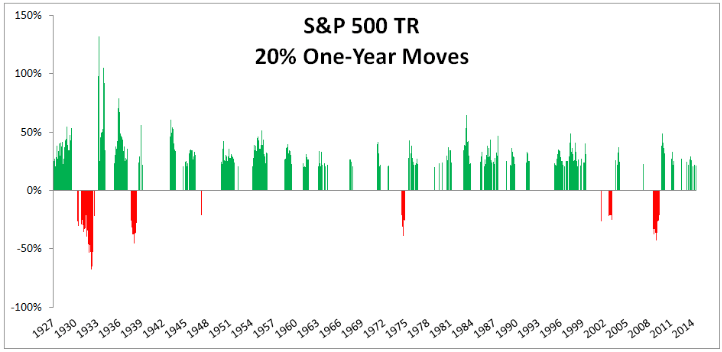

If I had to pick a single most important source for investors to read this week it would be Ben Carlson’s advice about How to Survive a Melt Up. He observes that most investors are focused on the risks, giving little thought to the possible upside.

But there’s another risk in the markets that most investors don’t spend too much time worrying about — a melt-up in prices.

It would seem to me that all of the ingredients are in place for a potential U.S. equity bubble. Interest rates are extremely low, central banks around the globe are almost accommodative across the board, there is a substantial need for returns from pensions and retirees and a general lack of alternatives elsewhere to invest. That doesn’t mean it has to happen, but the pieces are in place for upside volatility, something very few investors believe could occur these days.

In fact, if you look back historically at how stock markets have generally performed, they are much more likely to rise substantially than fall substantially in a given year.

Take a look at the odds.

Stock Ideas

Chuck Carnevale notes the problem with finding good dividend stocks: Very high valuations. He nurses out an interesting candidate, Kroger, while teaching how to be selective.

The biotech stock rebound might be just getting started (See It Market).

Holmes will begin contributing an idea each week, a stock we bought for clients a few days ago. I will mention it here and Holmes will also post it each Friday at Scutify.com. While we cannot verify the suitability of specific stocks for everyone who is a reader, the ideas may be a starting point for your own research. Holmes may exit a position at any time, and I am not going to do a special post on each occasion. If you want this information, just sign up via holmes at newarc dot com and you will get email updates about exits. This week’s Holmes pick is Hartford Financial Services (HIG).

Personal Finance

Professional investors and traders have been making Abnormal Returns a daily stop for over ten years. The average investor should make time (even if not able to read AR every day as I do) for a weekly trip on Wednesday. Tadas always has first-rate links for investors in his weekly special edition. There are several great choices worth reading, but my favorite is Carl Richards’ take on a Freaknomics theory. People are too cautious about making big changes in their lives. Is it enough to flip a mental coin?

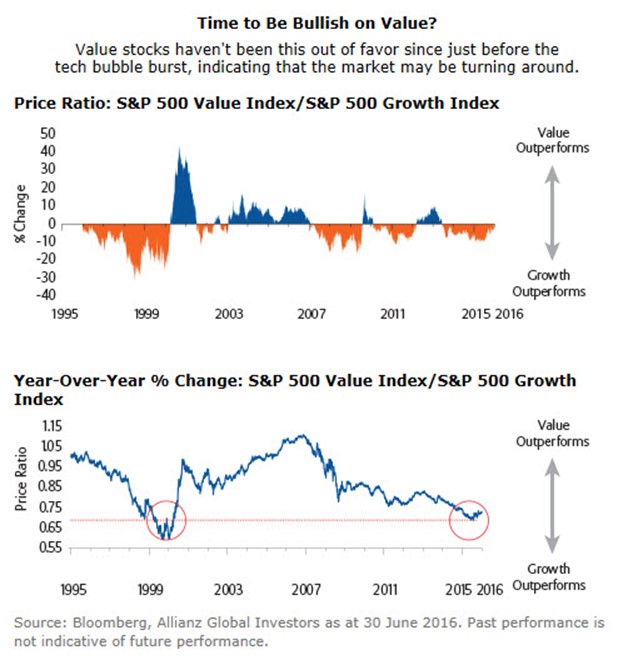

Value Stocks

This approach, successful in the long run, has been out of favor for the last few years. Ben Fischer (Allianz) describes the factors suggesting a change in the recent trend. He also includes this chart in the mean-reverting series:

If you missed my special post on this topic, addressing the “value trap” question, please take a look.

Watch out for….

Tax scams. There is no such thing as a “student tax” and your kids will not be kicked out of school if you do not pay it. The IRS does not seek money or charge card numbers for telephone payments. And they certainly do not take iTunes gift certificates! Sheesh! While my audience at WTWA would not fall for any of these scams, you might be able to help a friend.

And definitely do not fall for bogus citations from Warren Buffett! David Merkel explains.

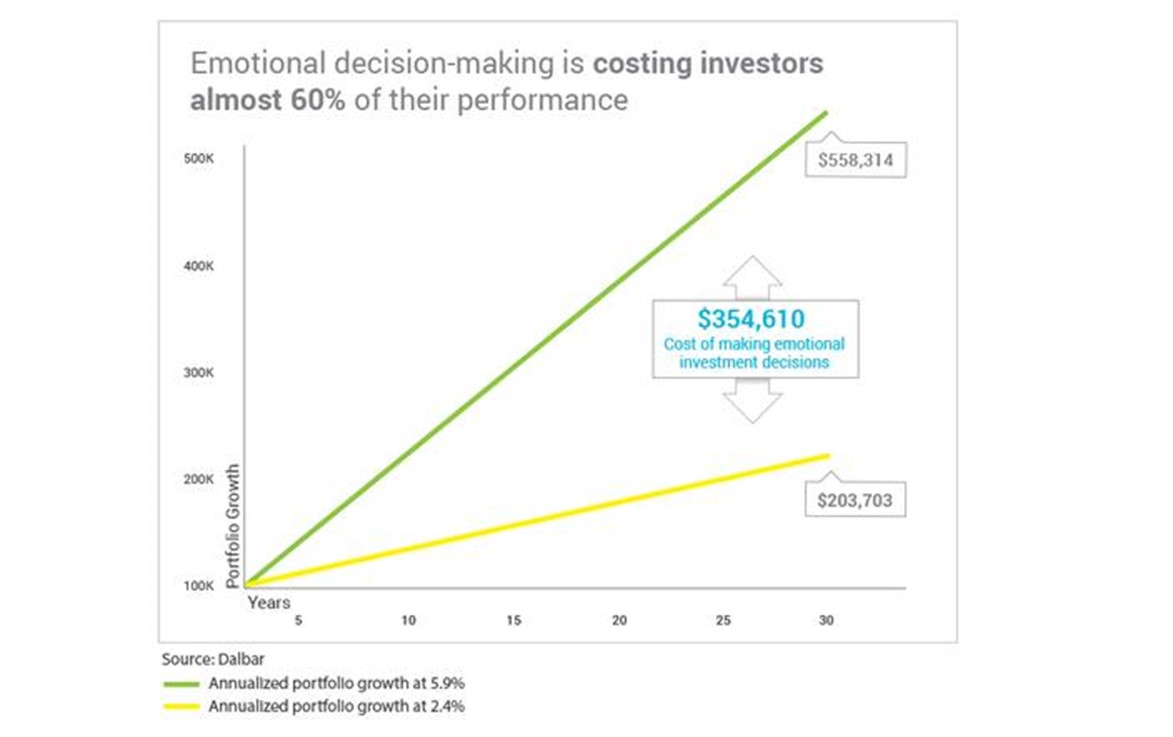

Emotional decision making is costly. Eric Crittenden Cio writes as follows and provides a supporting chart:

Investors have an addiction. Many of us feel like we can’t help it: we buy high and sell low even though it’s more logical to do the exact opposite. This addictive behavior is dooming us to a rocky investment experience and underperforming portfolios.

Final Thoughts

The continuing laments about the Fed seem concentrated among those who have done a poor job of predicting both the policy and the effects. The most recent variant is the complaint that there is not a unified message, and Fed members are not elected.

If the Fed had (even more) political accountability, rates would never increase! Politicians love low rates. The Committee currently includes a group of appointed officials with Congressional ratification, just as we have for the FDA, SEC, FCC, and other regulatory agencies. It is the nature of committees that the members will disagree, discuss, and compromise.

Instead of complaining about a very normal process of the U.S. style of government, it is more profitable to pay attention and to accept the diversity.

If the underlying data do not do not send a clear message, why should we expect the Fed to declare an unwavering policy? I expect interest rate increases sooner than the market currently believes, and that it will reflect economic improvement.