The global markets have encountered an era of financial repression since the beginning of 2009—a period of low interest rates and risk-encouragement that has led to a blissful time for growth investing. The market has awarded a scarcity premium to companies that can grow in this environment of limited economic expansion prospects. At the same time, the market has paid less attention to traditional value factors like price-to-earnings (P/E) ratios and dividend yields—despite the fact that these factors have provided sizable return premiums over the long term.

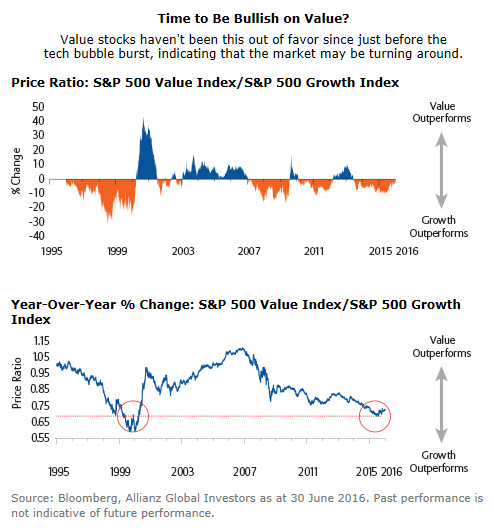

Clearly, everything has its season, and it is fair to say that it has been a long, cold winter for value investors who are committed to the style. Indeed, value has not been this out of favor since the high-flying days of the tech bubble in the late 1990s.

It is important to remember, however, that growth/value cycles tend to be mean-reverting and, on average, have lasted between seven and 10 years from trough to peak. With the growth style now in its ninth year of relative outperformance, the current phase of this cycle may be drawing to a close, and we may soon be likely to enter an environment that once again favors value investing.

Once this shift in the market occurs, as shown in the accompanying charts, yesterday's laggards could become tomorrow's leaders—and investors may want to be positioned accordingly. Of course, no one has a crystal ball that says exactly when the cycle will flip, but there are some signs that a shift may already be occurring, including:

1 Higher US interest rates. History shows that shortly after an initial rate hike, value stocks have outperformed in a persistent and pervasive manner. It is worth noting that “liftoff” for the current rate-hike cycle occurred in December 2015.

2 A weakening US dollar. Value indexes are skewed toward market segments like energy, industrials, and “old tech”, which derive significant revenue abroad. The US dollar has been losing value, which may provide these companies with an earnings tailwind.

3 A recovery in the high-yield bond markets. Value is inversely correlated with US high-yield spreads. These spreads are currently falling thanks to better credit conditions which signal that the worst may be behind us.

4 Strengthening commodity markets. Value outperformance is positively correlated with rising commodity prices. Given today’s market conditions, it seems prudent to keep exposure to value-oriented investments focused on income from dividends and low-valuation P/E multiples.

Given today’s market conditions, it seems prudent to keep exposure to value-oriented investments focused on income from dividends and low-valuation P/E multiples.

Contributing Authors: Baxter Hines, CFA; Garth Reilly

About the Author

Ben Fischer, CFA, is a portfolio manager, an analyst, a managing director and CIO of NFJ, an Allianz Global Investors company. Before founding NFJ in 1989, he was chief investment officer, and a senior vice president and a senior portfolio manager at NationsBank. Before that, Mr. Fischer was a securities analyst at Chase Manhattan Bank and Clark Dodge Asset Management. He has a B.A. in economics and a J.D. from The University of Oklahoma, and an M.B.A. from New York University, Leonard N. Stern School of Business.

Follow Us on Twitter

For more investment insights and market perspectives from our global research network, follow @AllianzGI_US on Twitter or visit us.allianzgi.com.

Important Information

The material contains the current opinions of the author, which are subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Forecasts and estimates have certain inherent limitations, and are not intended to be relied upon as advice or interpreted as a recommendation.

Past performance of the markets is no guarantee of future results. This is not an offer or solicitation for the purchase or sale of any financial instrument. It is presented only to provide information on investment strategies and opportunities.

Allianz Global Investors Distributors LLC, 1633 Broadway, New York NY, 10019-7585, us.allianzgi.com, 1 800 926 4456.

AGI-2016-08-17-16144