Remain calm and allow the world to shape itself - The I Ching

Takeaways

· Cutting through a thick fog of uncertainty, stock and bond markets rebounded smartly in 2Q16 on the back of plentiful central bank liquidity.

· Limited upside lies ahead for stocks in the face of downgraded growth prospects, extended valuations, and political uncertainty.

· Though buffeted by declining profits growth and vulnerable to pullbacks, U.S. equities are still the asset class of choice, but emerging markets and commodities are worthy of increased exposure.

· The rally in global bonds has generally run its course, but bond prices can stay firm in the face of easy central bank policies, tepid economic conditions, and restrained price inflation.

· The dollar continues range-bound against the yen and the euro, but some slippage is possible in the wake of no action by the Fed and sluggish growth in 2H16. In the wake of Brexit, the sterling weakens further versus the dollar as the economy struggles to avoid recession.

· Cutting back modestly overweight positions in global equities, while raising slightly exposure to bonds, especially emerging markets in global portfolios.

Surf’s Up – The July Rally

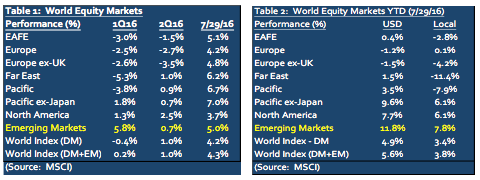

The tsunami of liquidity provided by unprecedented central bank policies has helped repair the market reaction to the 25 bps rise in the fed funds rate last December, the failed Turkish putsch, terrorist attacks in the U.S. and Europe, and the expected fallout from Brexit. The bounce back in asset prices picked up in July (see Table 1), despite a serious setback in U.S. growth reflected in the new and revised GDP data released in late July, and further downgrades in world economic prospects by the IMF and the OECD. The risk-on attitude, coupled with a drop in U.S. Treasury yields and a softer dollar, gave a second wind to the battered emerging markets. When measured in dollar terms, emerging markets have been clear winners this year (see Table 2).

Speed Bumps Ahead

The enthusiasm for equities is likely to lose some froth in the period ahead, undermined by tepid growth, earnings disappointments and ongoing policy uncertainties. In the U.S., despite climbing to record levels, the stock market remains largely unloved, especially by institutional investors as they try to de-risk their portfolios and/or step up exposure to alternatives. Foreign investors have also cut back on purchases of U.S. stocks. On the face of these outflows, share buybacks and merger and acquisition activity by U.S. companies have been a major prop to stock prices, albeit by adding a hefty load of debt on corporate balance sheets. Such activity is not sustainable against the backdrop of feeble revenue growth and declining profits.

Added support from further aggressive easing by central banks cannot be counted on to reinforce risk-on appetite for stocks. Despite weak headline real GDP growth in 2Q16, with the U.S. Presidential campaign in the home stretch, the Federal Reserve is likely to stay on the sidelines at least until December mindful of not undermining its independence already under threat in the Republican Congress.

Similarly, beyond some tweaking, the European Central Bank (ECB) and the Bank of Japan (BOJ) stayed put in July, implying that they are running low on unorthodox measures, and that it is fiscal policy’s turn to pick up the slack. This is especially true in Japan, where Prime Mister Abe just announced a massive $265 billion fiscal package to jump start the moribund economy. Action by the Bank of England (BOE) to drop interest rates for the first time since 2009 and expand quantitative easing is an effort to cushion the economy in the wake of increased uncertainty following Brexit. Whether the ECB or the BOJ will follow suit will depend on incoming data in the period ahead.

Decision Economics, Inc. (DE) Asset Allocation Shifts in Global Equities

Against this muddle-through backdrop and policy uncertainty, DE is cutting back overall exposure to equities in global portfolios for dollar-based investors.

U.S. stocks retain their position as the asset class of choice supported by economic growth that chugs along. But the stock market is vulnerable to pullbacks brought on by declining profits, pressure on margins and more importantly by the dystopian Presidential election campaign. Other indicators suggesting a bumpy road ahead include continuing weakness in small caps, rotation out of cyclicals and into defensive sectors such as utilities and consumer staples, and the market’s narrow footprint as a result of the ongoing concentration on large caps with strong balance sheets.

European markets have been under pressure as the economy grapples with the aftermath of austere fiscal policies, weakened exports, limited credit growth, the fallout from Brexit, and a weak banking system. By comparison, Pacific ex-Japan has turned in a strong performance supported by some recovery in commodities and a semblance of stability in China.

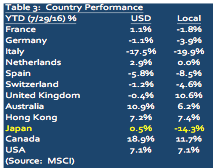

Despite a massive buying spree by the BOJ – the central bank now owns about 55% of Japanese ETFs, making it indirectly a Top-Ten holder of 90% of the Nikkei 225 Index – and a tail wind for USD-based investors thanks to a sharp rise in the yen, Japanese stocks have been the worst performing market YTD among major markets as the economy struggles to get traction, while foreign investors in a show of no confidence in Abenomics have gone MIA (see Table 3).

Attractive valuations notwithstanding, the three other factors that support raising further the already significant exposure to emerging markets include 1) the rebound in oil and other commodity prices, 2) the drop in USD interest rates and 3) the softening of the dollar. Among the regions, Latin America has shown the strongest results, rising 32% YTD as of July 30, led by an explosive 61% rise by Chile and nearly matched by Brazil’s 58% rise, as both are heavy commodity producers. Nevertheless, emerging markets are not a monolith and exposure should take into account pro-growth government policies and positive external balances.

Bonds Away – Searching for Yield

This unconventional investment landscape dominated by ZIRP and NIRP has produced some odd attitudes. Investors seem to be looking to stocks for yield – over 50% of stocks in the S&P 500 Index now yield more than the 10-Year U.S. Treasury bond yield – while investing in bonds for capital appreciation. The demand for capital preservation has driven bond yields to historic low levels. Amazingly, about $13 trillion of global sovereign debt now carries negative interest rates, while the entire Swiss government yield curve all the way out to 50 years is in negative territory. Though the rally in global bonds has generally run its course as investors regrouped following the Brexit fallout, the modest backup in Treasury yields from record lows does not foretell a further steep rise ahead. Below par growth is expected to continue, Federal Reserve action on rates will be on hold until December, and inflation expectations remain well anchored.

Similarly, the recent sell-off in JGBs was more of a reaction to the BOJ decision to stay put. And with BOJ buying all new government bond issues and then some, it would be hard for a further rise in yields to be sustained. Meanwhile in the Eurozone, Sig Draghi stands ready to do “whatever it takes” to keep markets calm. This backdrop of easy central bank policies, tepid economic growth and restrained inflation, calls for range-bound yields for U.S. 10-year Treasuries between 1.3% and 2% for the rest of this year. An upward drift is likely in 2017 in the backwash of some pickup in growth and an expanding federal budget deficit.

Against the backdrop of fairly stable yields, DE has raised the weight of bonds in global portfolios, focusing on U.S. Treasuries (also because of their safe haven protection against geopolitical risks), high-grade corporates, and dollar and non-dollar sovereign bonds.

There is no infallible GPS to guide investors through this uncharted investment landscape. But the opening quote, “Remain calm and allow the world to shape itself,” underscores our global investment strategy for now. DE’s Baseline Scenario (60% probability) calls for a 2-3/4% U.S. real growth in the rest of 2016 driven by the consumer, and about the same on average in 2017. Also, a turnaround in U.S. earnings, helped along by some improvement in overseas economic growth as a source of earnings is expected next year. Going forward, DE maintains a constructive overall posture on equities, while also recognizing that this is a challenging investment world, stuck in a relatively slow growth trajectory with significant downside risks and limited upside potential. Global diversification across all major asset classes represents the safest way for investors to preserve capital.