Many people don’t have an investment allocation to real estate investment trusts (“REITs”) because they believe they already have “enough” exposure to “real estate” through ownership of their home.REITs and your home are very different asset classes with very different characteristics. REITs invest primarily in commercial real estate, which is any non-residential property used for commercial profit-making purposes. Your home is an investment in residential real estate, which is a type of property, containing either a single-family or multifamily structure, which is available for occupation and non-business purposes.

Performance

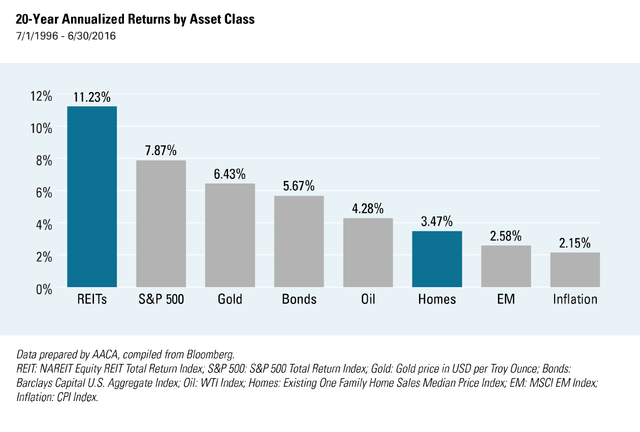

Over the past 20 years publicly-traded REITs have returned an annualized 11.23% total return and homes have returned 3.47%, or just a little more than inflation. Over these 20 years, REITs returned more than 7x (740%) while homes didn’t quite double (98%). Publicly-traded REITs have been one of the top performing asset classes and homes have been one of the worst over the past 20 years.

There are many differences between REITs and your home that contribute to this notable difference in performance. The largest contributor is that commercial real estate can generate positive cash flows but the residential home you live in cannot. By living in your home, you are effectively consuming the market rate rent that your home might have procured. If you forgo rent, as you do by living in your home, the return profile changes to be basically little more than an inflation hedge. Performance of real estate follows the following formula: Total Return = price change + rent collected

Diversification

With your home, 100% of the asset is in one property type and in one geographic market – this is concentration in its purist form, the opposite of diversification. On the other hand, with publicly-traded REITs, investors can choose from dozens of property types (including, but not limited to, specialized real estate sectors such as data centers, cell phone towers, casinos, medical research labs, infrastructure, prisons, ski areas, etc.) across any market in the U.S. and most major markets in the world. The opportunity for diversification in publicly-traded REITs vastly exceeds that of a single home.

Liquidity

Homes are relatively illiquid compared to public REITs that can be traded every day the stock market is open and settle to cash virtually immediately. This is in stark contrast to the home market, which may be illiquid for months, seasons, or even years, and can take months to settle to cash.

Transaction Costs

Transacting a home is much more costly than transacting in publicly-traded REITs. When you sell a home, the typical transaction cost is more than 6% of the home’s sale price (for perspective, based on data from the last 20 years as shown in the Total Return chart above, this is equal to about five years’ worth of your home’s price appreciation after inflation). In contrast, it costs little more than pocket change to trade shares of a public REIT ($7.95 per trade at Fidelity[1] and $4.95 per trade at Scottrade[2]).

Flexibility

Home ownership is not flexible. The entry price for a home is typically six-figures and you can’t really buy or sell a percentage of a home – it is binary: either you are in all the way or you are completely out. With publicly-traded REITs you can buy almost any amount you wish in single share increments (typically $20-$50/share) on the stock market. With public REITs you can trim, add or change a position in almost any amount on almost any day.

Supply & Demand

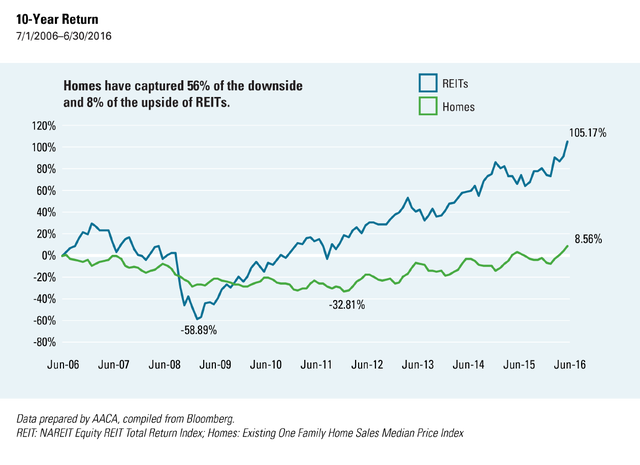

Perhaps the single most impactful factor that undermines home price appreciation is the ability of developers to add new product to the market. In our opinion, homes are the type of real estate most likely to be oversupplied because we believe they are the cheapest, smallest, quickest and least complicated real estate product type to build. AACA also believes that whenever the cost to build new homes is below the current market value of existing homes, builders will build new homes, which could create a price ceiling on the appreciation of your home. Additionally, in recessions, construction costs (materials and labor costs) decrease, which makes building new homes less expensive and creates additional new supply. This combination of factors could dampen your home’s price rebound out of a recession relative to public REITs, as shown in the historical graph below.

Volatility

Let’s look at volatility of publicly-traded REITs and homes. Below is a graph of the past 10 years, which includes the financial crisis. Since public REITs trade on the stock market, the share price of these REITs are subject to fluctuation in the stock market and as such experience volatility. However, we would argue the underlying physical real estate owned by the REITs can’t be much different in volatility than your physical home. The difference is that your home isn’t bought and sold every day and marked to that market price. That being said, in the graph below we see that homes sold off -32.81% and public REITs sold off -58.89% in the financial crisis. However, looking at a longer period of time, homes captured 56% of the downside and 8% of the upside of public REITs over the past 10 years – homes have been asymmetrical to the downside. And public REITs have since gone on to return 105.17% over the past 10 years while homes have returned 8.56% in that same time period.

Final Thoughts

We believe you should think of your home first and foremost as the place you and your family live and second as an inflation hedge for your invested principal – nothing more than that. You should not think of your home as an investment in real estate (as history shows there has been almost no meaningful return after inflation). Publicly-traded REITs and your home are very different asset classes with very different characteristics.

But what if I rent my home out?

But what if I buy a home and rent it out? That would be good, right? Sure, you will grab the warranted rent (assuming you can find a good renter), but you may also be the one grabbing a plunger to fix the toilet on Christmas Eve when your renter calls. Also, you still need a place to live so you will presumably either be buying or renting a home to live in. Additionally, it is probably unlikely that you can rent one house as efficiently as a public REIT that has professional leasing, revenue optimization software, economies of scale, expert experience, market knowledge and real-time industry data. Lastly, if you want to buy a home and rent it out, there are several publicly-traded REITs that do that.

[1] https://www.fidelity.com/trading/commissions-and-margin-rates?s_tnt=76947:8:0