Equity markets have continued to grind higher over the summer months, defying deteriorating company earnings and high profile investors calling for an equity correction. Now U.S. equities are beginning to defy traditionally reliable market indicators, which are undeniably showing that the equity trade has become very crowded. While the phase “this time is different” appears to apply to the current equity rally, at some point, despite central bank policy distortions, the market will eventually fall under its own weight. We have stopped trying to forecast interest rate policy, trying to understand why investors are keen on paying higher prices for falling earnings, trying to fathom the widely accepted doctrine that central banks will be capable of supporting equity prices come what may, and trying to interpret why both good and bad macroeconomic data cause equities to rise. All these miscomprehensions (or anomalies for us), are suggestive of the bubblish behaviour of the current markets. Our next Weekly Commentary, “Bubbology 101” (to be published during the week of August 15), will look at the causes, characteristics, and consequences of past equity bubbles and indicate which segments of the market we judge to be in a bubble.

As for this week, we review numerous market data sourced indicators. While the Federal Reserve, European Central Bank, and Bank of Japan’s “go-for-broke” policy actions are ensuring that “this time IS different”, we must never forget a favourite market truism: “trees never grow to the sky, and their root never descend to hell”. Investors can debate whether or not prices are already at sky high levels today. Given that central banks have placed us in uncharted territory, we have few points of reference to judge when the equity rally will end, and can not be sure if the next move is +20% to the upside or -40% to the downside. The best we can do today is to fall back on our market indicators to get some insight into today’s risk/reward trade-off. We go through several market indicators, beginning with the just-released short interest numbers for the close of July.

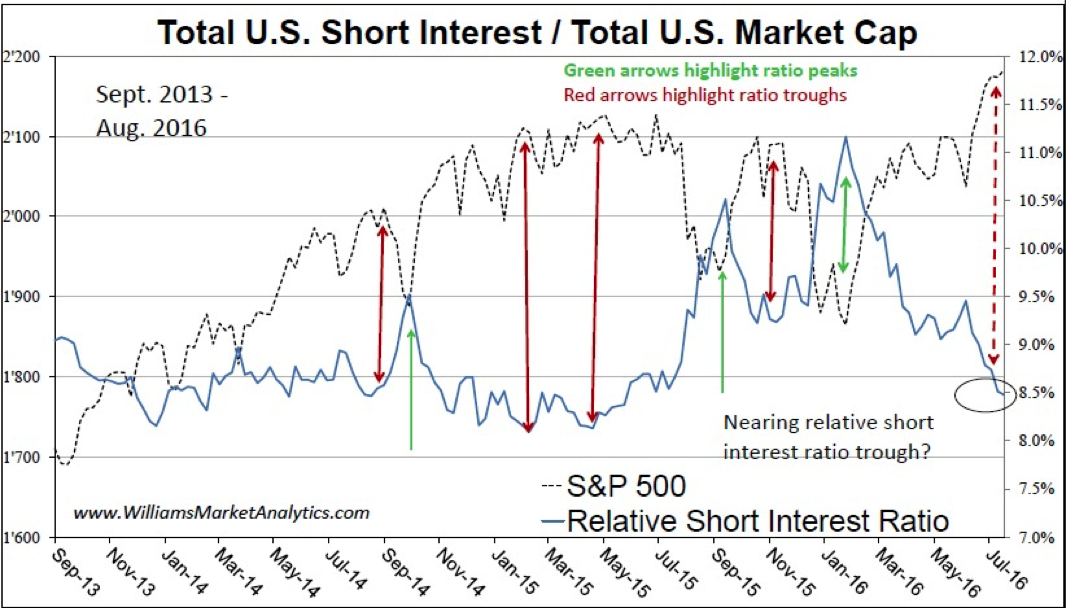

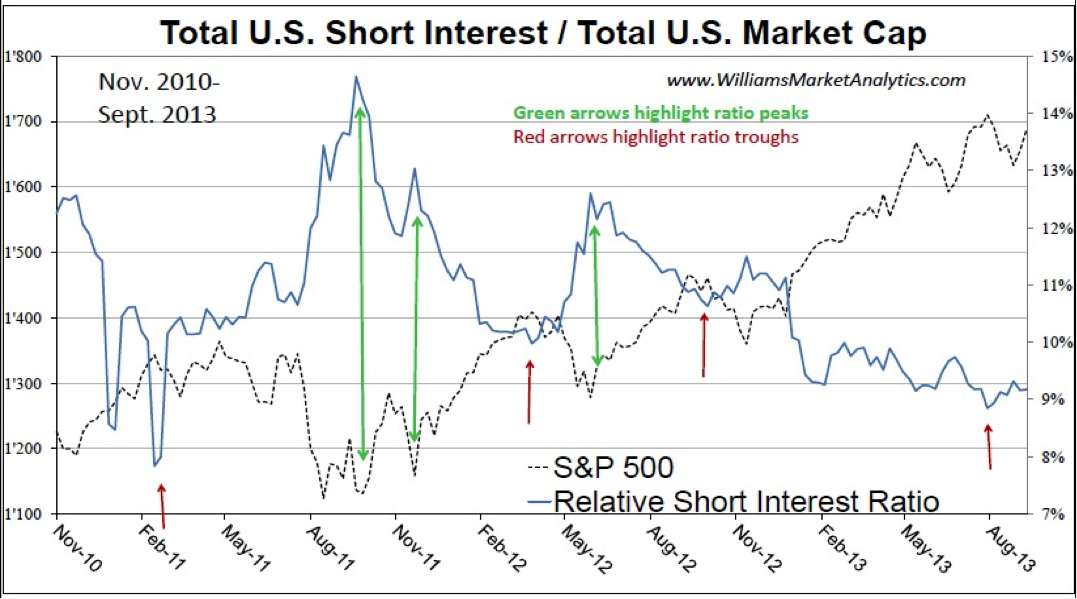

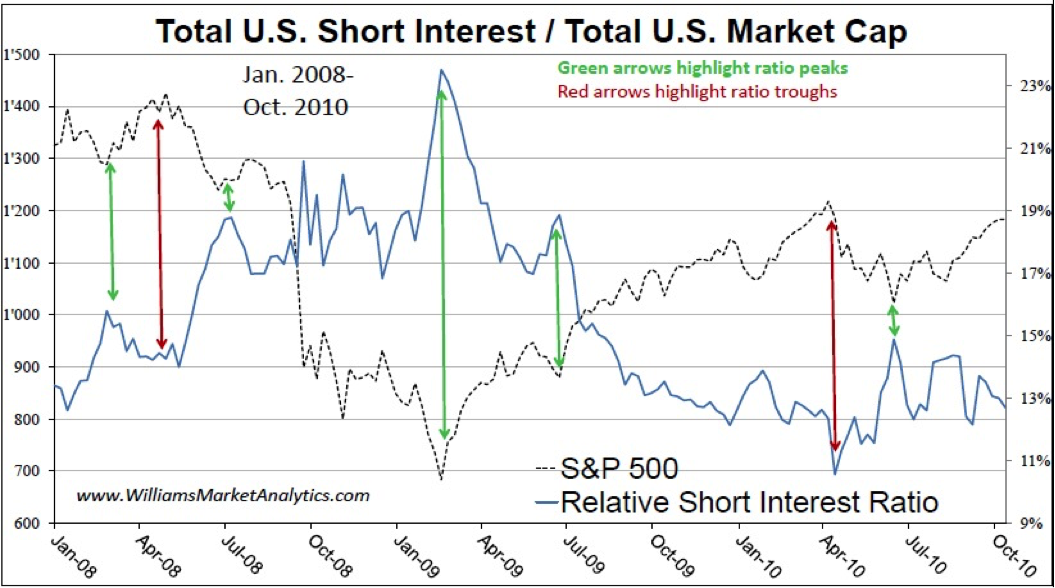

Short Interest

The total market U.S. short interest data, released bi-monthly by the exchanges, aggregates short interest from the NYSE, Nasdaq, and AMEX. We like to look at total short positions relative to total U.S. market capitalization to normalize the data. To better see the historical behaviour, we broke the short interest data from 2008 into three time frames (shown in the next three charts) and overlaid the S&P 500. Unsurprisingly, falling relative short interest is equity-positive, for a while. However when the short interest curve begin to form a trough at low levels, we invariably see a peak on the S&P 500.

Today short interest is neutral, at best. With the short interest ratio below 8.5%, near the record low of February 2011, those calling for another 10%-15% upside right away on the S&P 500 are betting “this time is different”.

One can really see the mirror image relationship between short interest and equity prices.

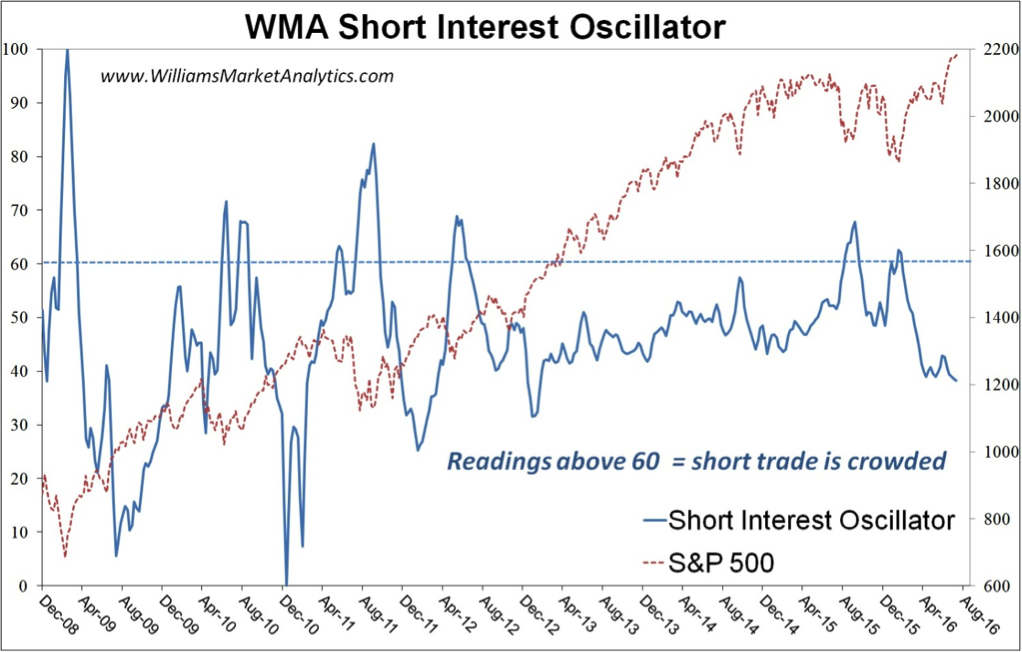

Our short interest oscillator (below), based on the size and direction of total short positions in the market relative to market capitalization, pretty much confirms that shorts have left the building. Low oscillator readings are like a “tornado watch” for a market sell-off: conditions are favourable for one to develop, but nothing in sight for the moment.

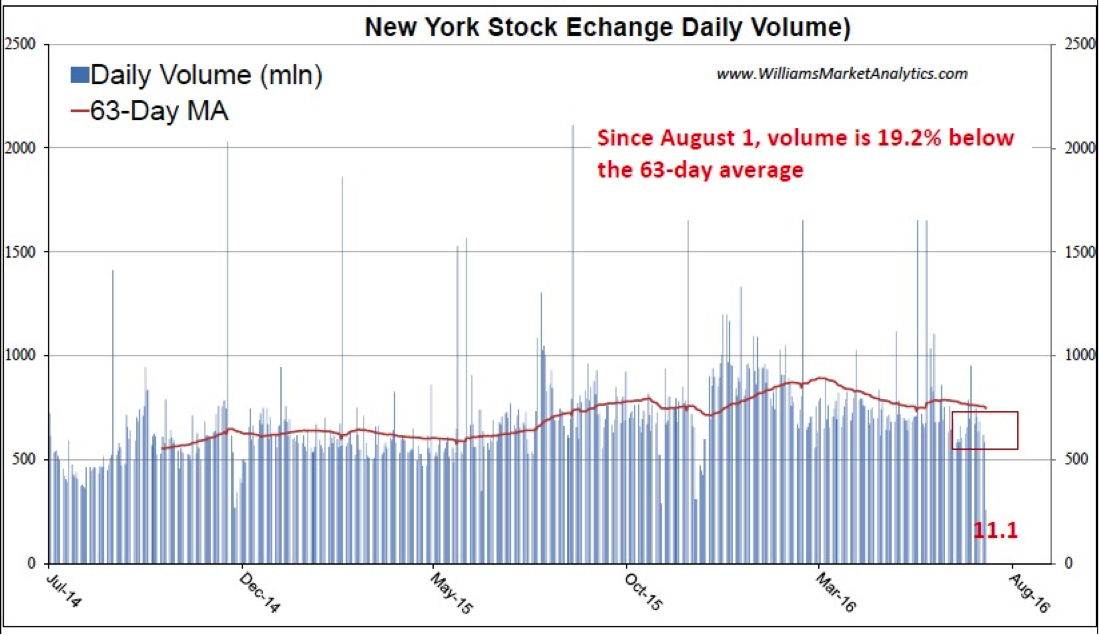

Volume

During the summer holidays, some investment professionals take vacations (not us!). As a result, trading volume dries up (see chart below) and the markets are vulnerable to outsized moves. This is a main reason August tends to see large draw-downs. Our concern with volume is not that the market is rising on low volume (yes, you can make or lose money on light volume), but rather the air pocket we’ll experience if something happens to induce selling. There are very few thoughtful, human investors buying at these levels (over 80% of the equity market are machines, or algos). Who is left buying? Dumb money, including retirement funds that automatically send to the equity markets the fraction of an employee’s monthly salary allotted to pension savings. Each month, the market receives this fresh money, regardless of where the equity market is trading. It is not the dumb money which will catch an equity market fall should investors decide risks are no longer worth the meager upside potential of equities.

Volatility

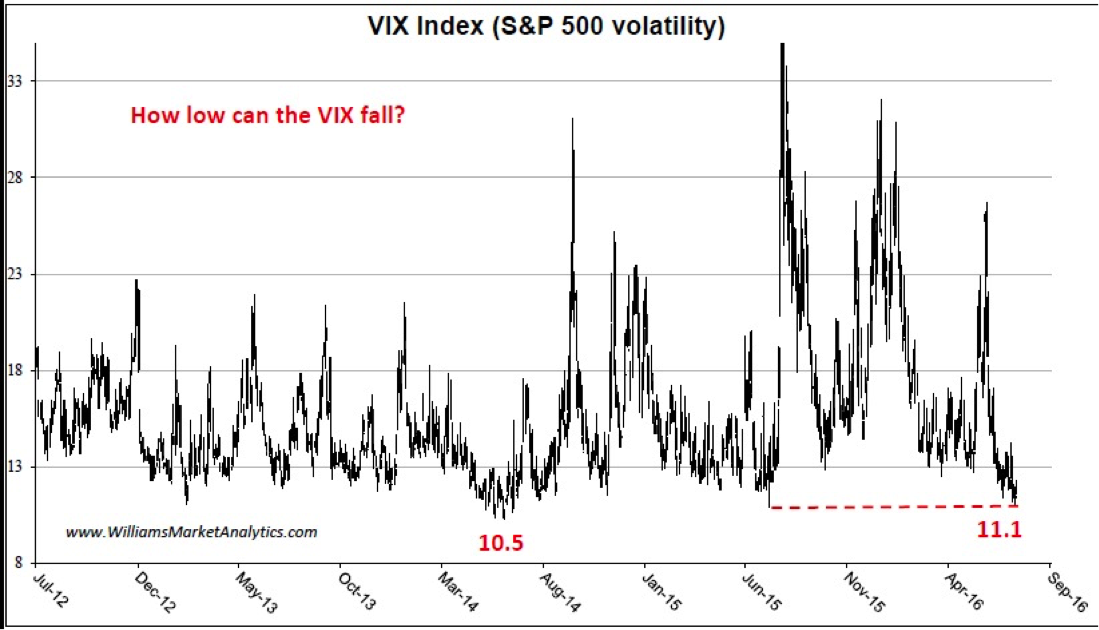

Professional speculators are making record bets in volatility markets that U.S. stocks will keep rallying. Hedge funds and other big traders tracked by the Commodity Futures Trading Commission have pushed net short positions on CBOE Volatility Index futures to 115,000 contracts, the most since 2013. Most VIX-related exchange traded products (ETPs) have declared reverse splits in the past 30-days, as prices neared zero. Many things may be different today, but one thing has not changed: the market will do whatever it takes to prove the majority wrong. Nevertheless, while today is an awful time to buy/hold equities based on the VIX, a low VIX does not mean volatility will instantly pop with a concomitant fall in equities. In the summer of 2014, the VIX meandered between 10.5 and 12 for over two weeks before the S&P 500 corrected -8% in July. In sum, a low VIX is not an easy short, nor is it time to add to equity positions.

Risk

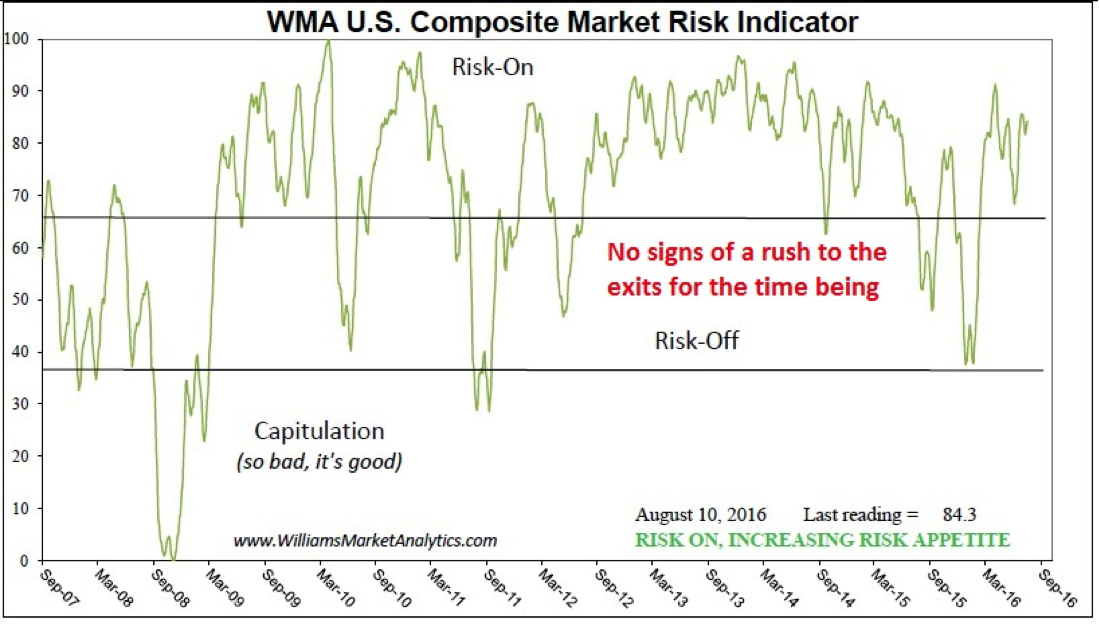

Our WMA U.S. Risk Indicator has been cruising in “Risk On” mode since February. Recall that we recommend a buy the dips / sell the rallies approach in “Risk On” mode. Today the indicator appears to be setting up a lower high, much as we saw throughout 2015.

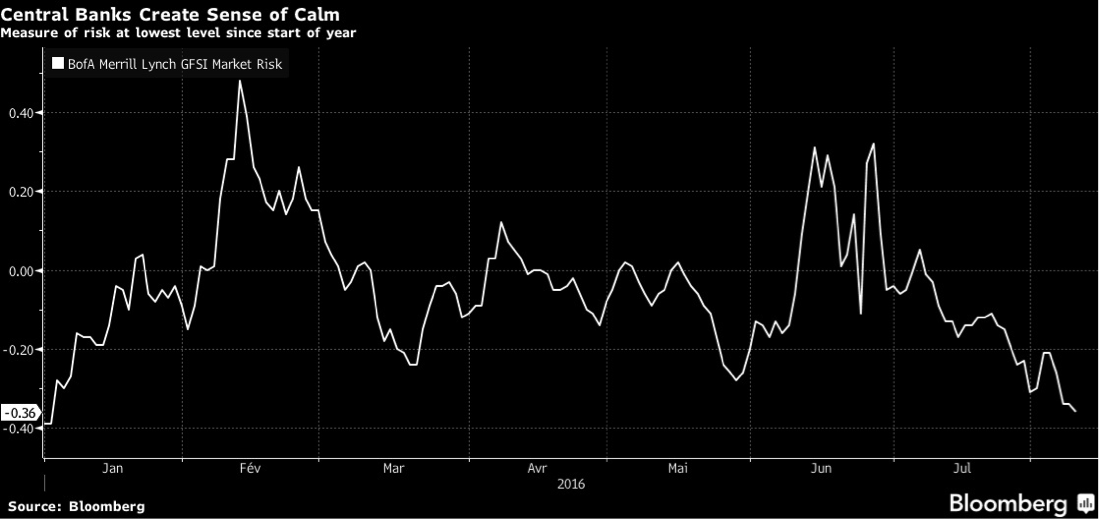

Another sign of market complacency we came across this week is the BoA Merrill Lynch Market Risk Index. Their index is at the lowest level since….January. It’s a distant memory now, but equity investors didn’t enjoy last January too much.

Conclusion

The market cannot keep trending higher forever in the wake of declining profits. The Fed and other central bank moral support for the equity market will only last as long as investor are willing to believe that the Fed can (or will) bail out investors in the next period of turbulence. In a period of extreme complacency and blind confidence in the markets as a whole, it’s anyone’s guess when company valuations and the price of risk will again be taken into serious consideration. In the near term, and assuming “it’s not different this time”, the above market indicators suggest that the current equity move needs a break.