Commodities have become a hated asset class, with cumulative losses totaling over 50% during the last 5 years, as measured by the Bloomberg Commodity Index. Despite recent returns, a strategic allocation to the commodity asset class still makes sense for many investors given its desirable combination of inflation protection and low correlation with the equity and fixed-income asset classes.

Although poor performance in commodities may raise the question of why any such allocation should even exist, it ignores the fact that diversification is a useful tool for dealing with an unknown future, and always looks somewhat damaging in retrospect. Given that returns remain difficult to predict consistently, diversification still provides the only free lunch in investing.

Here are four reasons for why current investors should remain invested and why everyone else should consider the current environment as an opportunity to add commodity exposure to their portfolios.

Diversification

Commodity returns are directly tied to the economic cycle, due to their linkage with the prices of raw materials. This means that commodity returns typically bottom out simultaneously with the depth of an economic recession and peak at the height of an economic boom. This outcome is in contrast to both bonds and equities, which tend to have price movements that are offset from the economic cycle, with extreme valuations happening markedly before or after economic peaks and troughs. This intrinsic offset between the cycle of returns for commodities and those of more mainstream asset classes makes them naturally diversifying to one another.

This persistently lower level of correlation with both equities and bonds delivers an expected diversification benefit at the portfolio level for most investors, as portfolios that include an allocation to commodities are able to produce higher expected returns with lower expected volatility than portfolios that do not contain such an allocation.

Reports of Inflation’s Death May Be Greatly Exaggerated

Another reason for holding commodities is for protection against inflation. U.S. inflation has been trending upward since mid-2015, and has posted annual rates above 2% for the last six months. It is also worth noting that CPI remained above 1.5% over the course of 2015, despite the crash in energy prices. Given the importance of energy prices to most aspects of a modern economy, the fact that core inflation remained in excess of 1.5% even while oil prices dropped by half indicates that inflation would have been much higher if energy prices had stayed flat in 2015.

Historically, commodities have performed strongly in times of inflation, while equities have struggled and fixed income has dropped. If inflation continues to rise, an allocation to commodities could prove beneficial to an investor’s portfolio, and will likely provide far more inflation protection than many other mainstream asset classes.

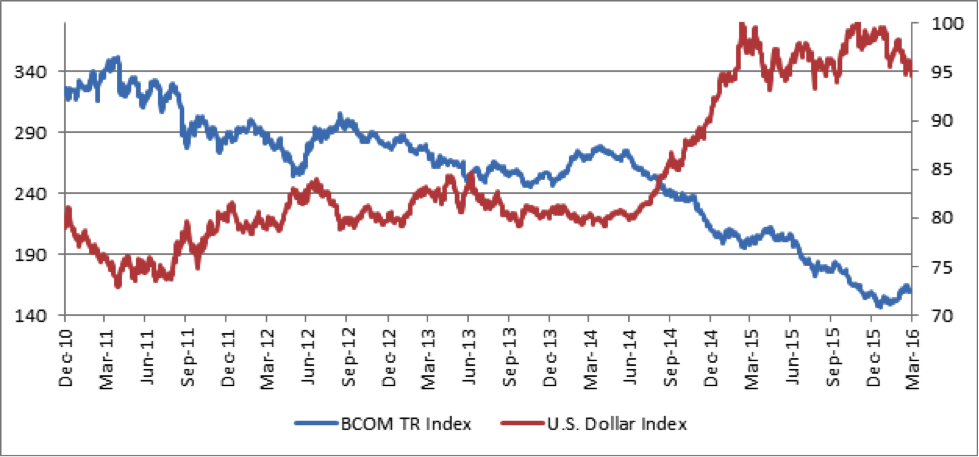

Dollar Strength

Many commodity investors have noted a link between the strength of the U.S. dollar and the prices of commodities – as the dollar strengthens against other major currencies, commodity prices tend to fall, and vice versa.

Bloomberg Commodity Index Total Return vs U.S. Dollar Index, 12/31/2010-3/31/2016

Sources: Bloomberg, Parametric 3/31/2016.

In fact, the strength of the dollar and the price level of commodities are practically mirror images of one another, with the pronounced strengthening of the U.S. dollar over the past 18 months being accompanied by a dramatic sell-off in commodities. The future direction of currency markets is unknown, but if the dollar were to weaken dramatically, it could provide a strong tail wind to commodity prices for the U.S.-based investor.

The Cure for Low Prices Is Low Prices

Many consider commodities to be the one asset class where price reversals are the norm. This is due to the following dynamic between prices and supply:

- A shortage of supply causes an increase in prices. As prices rise, more producers are incentivized to dedicate resources to capitalize on this increased demand.

- Given the amount of time needed to increase production, the resulting supply tends to overshoot the true demand, and the market turns to an oversupplied condition.

- As a result, prices eventually drop, and commodity producers reduce their output or decrease their efforts directed toward discovering and extracting new supplies.

- This, in turn, causes a decline in supply, which also overshoots the mark of true demand, to the downside. This causes the cycle to start anew, with price increases coming about due to inadequate supplies.

Given the scale of the drop in commodity prices over the past five years, producer reaction to these price signals has been extreme. Recent news headlines detailing mine closures, reduced acreage in crop plantings, and declining rig counts in the natural gas and petroleum fields of North America seemingly provide evidence that any recovery, when it comes, will be sharp and long-lasting, given the amount of production that has been sidelined and the amount of time that will be required to bring adequate supplies back online.

Conclusion

Commodities have become one of the most shunned asset classes over the past five years, as the recent bear market has been notable for both its length and magnitude. This decline has caused many investors to either exit, or reduce their strategic allocation to commodities. In this brief we have laid out supporting arguments that should assist in motivating an investment in commodities. They remain a powerful diversifier to an investor’s portfolio; recently observed increases in CPI make its inflation-protection properties appealing; recent returns for the asset class have been diminished by currency impacts, which are unlikely to be repeated; and the size and severity of the last downturn may predicate a sharp recovery when it occurs. Investors should look past recent returns and, instead, make a decision based on the future potential of this asset class.

Disclosures

Parametric Portfolio Associates® LLC (“Parametric”), headquartered in Seattle, Wash., is registered as an investment adviser with the U.S. Securities and Exchange Commission under the Investment Advisers Act of 1940. Parametric, headquartered in Seattle, WA, is a leading global asset management firm, providing investment strategies and customized exposure management to institutions and individual investors around the world. Parametric offers a variety of rules-based, risk-controlled investment strategies, including alpha-seeking equity, alternative and options strategies, as well as implementation services, including customized equity, traditional overlay and centralized portfolio management. Parametric is a majority-owned subsidiary of Eaton Vance Corp. and offers these capabilities through investment centers in Seattle, WA, Minneapolis, MN and Westport, CT (home to Parametric subsidiary Parametric Risk Advisors LLC, an SEC-registered investment adviser).

Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. We believe the information provided here is reliable, but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. Past performance is not indicative of future results. The views and strategies described may not be suitable for all investors. Investing entails risks and there can be no assurance that Parametric will achieve profits or avoid incurring losses. Parametric does not provide legal, tax and/or accounting advice or services.

Charts, graphs and other visual presentations and text information were derived from internal, proprietary, and/or service vendor technology sources and/or may have been extracted from other firm data bases. As a result, the tabulation of certain reports may not precisely match other published data. Data may have originated from various sources including, but not limited to, Bloomberg, MSCI/Barra, FactSet, and/or other systems and programs. Parametric makes no representation or endorsement concerning the accuracy or propriety of information received from any other third party.

The value of commodities investments will generally be affected by overall market movements and factors specific to a particular industry or commodity, which may include weather, embargoes, tariffs, health, and political, international and regulatory developments. Economic events and other events (whether real or perceived) can reduce the demand for commodities, which may reduce market prices and cause their value to fall. The use of derivatives can lead to losses or adverse movements in the price or value of the asset, index, rate or instrument underlying a derivative due to failure of a counterparty or due to tax or regulatory constraints.

The Bloomberg Commodity Index (BCOM) is formerly known as the Dow Jones-UBS Commodity Index. BCOM is a broadly diversified index composed of futures contracts on physical commodities. “Bloomberg” is a trademark and service mark of Bloomberg Finance L.P. (“Bloomberg”). The S&P 500 Index represents the top 500 publicly traded companies in the U.S. “Standard & Poor’s” and “S&P” are registered trademarks of S&P Dow Jones Indices LLC (“S&P”), a subsidiary of The McGraw-Hill Companies, Inc. The views and opinions expressed herein is not sponsored or endorsed by Barclays, Bloomberg or S&P and they make no representation regarding the content of this material. Please refer to the specific provider’s website for complete details on all indices.

All contents copyright 2016 Parametric Portfolio Associates® LLC. All rights reserved. Parametric Portfolio Associates, PIOS®, and Parametric with the iris flower logo are all trademarks registered in the U.S. Patent and Trademark Office.

Parametric is located at 1918 8th Avenue, Suite 3100, Seattle, WA 98101. For more information regarding Parametric and its investment strategies, or to request a copy of Parametric’s Form ADV, please contact us at 206.694.5575 or visit our website, www.parametricportfolio.com.