Since the mid-January low, we have become more positive on investment opportunities in emerging markets. In our view, this EM rally can continue, with the potential for more upside in the next six to 12 months. Of course, the sustainability of the rally will depend on fundamental data, global monetary policy and continued stabilization in currencies and commodities—and selectivity remains key as individual economies maintain different growth trajectories.

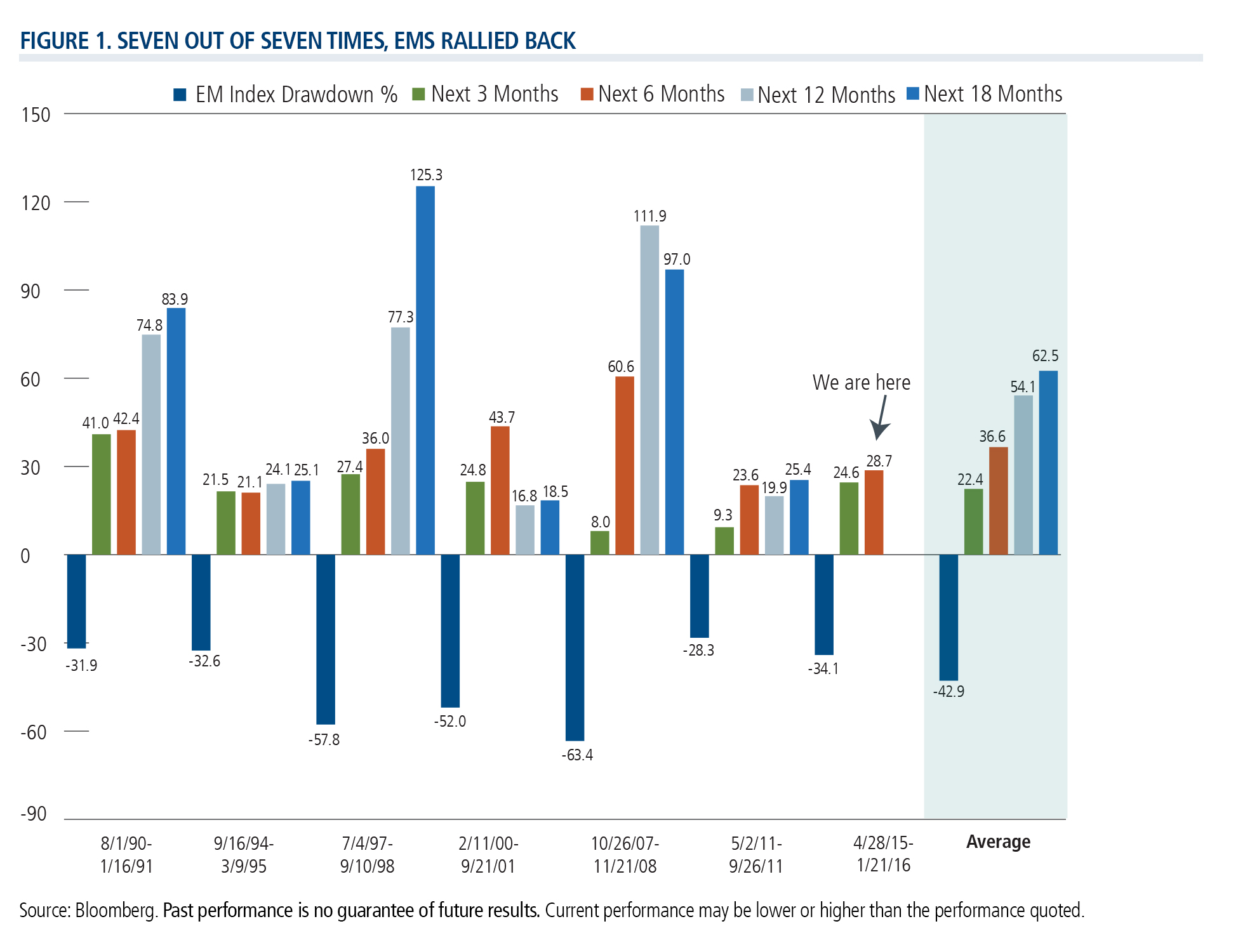

Since the 1988 inception of the MSCI Emerging Markets Index, there have been seven major (25% or more) drawdowns in emerging markets. In each instance—seven out of seven times—the major drawdown was followed by a rally. Notably, the average returns for the 12- and 18-month periods following a major EM drawdown illustrate the potential for gains. July 21 marked the six-month anniversary of the January 21 low in emerging market equities. As Figure 1 shows, this recent rally is fairly similar to the average of the past market rebounds.

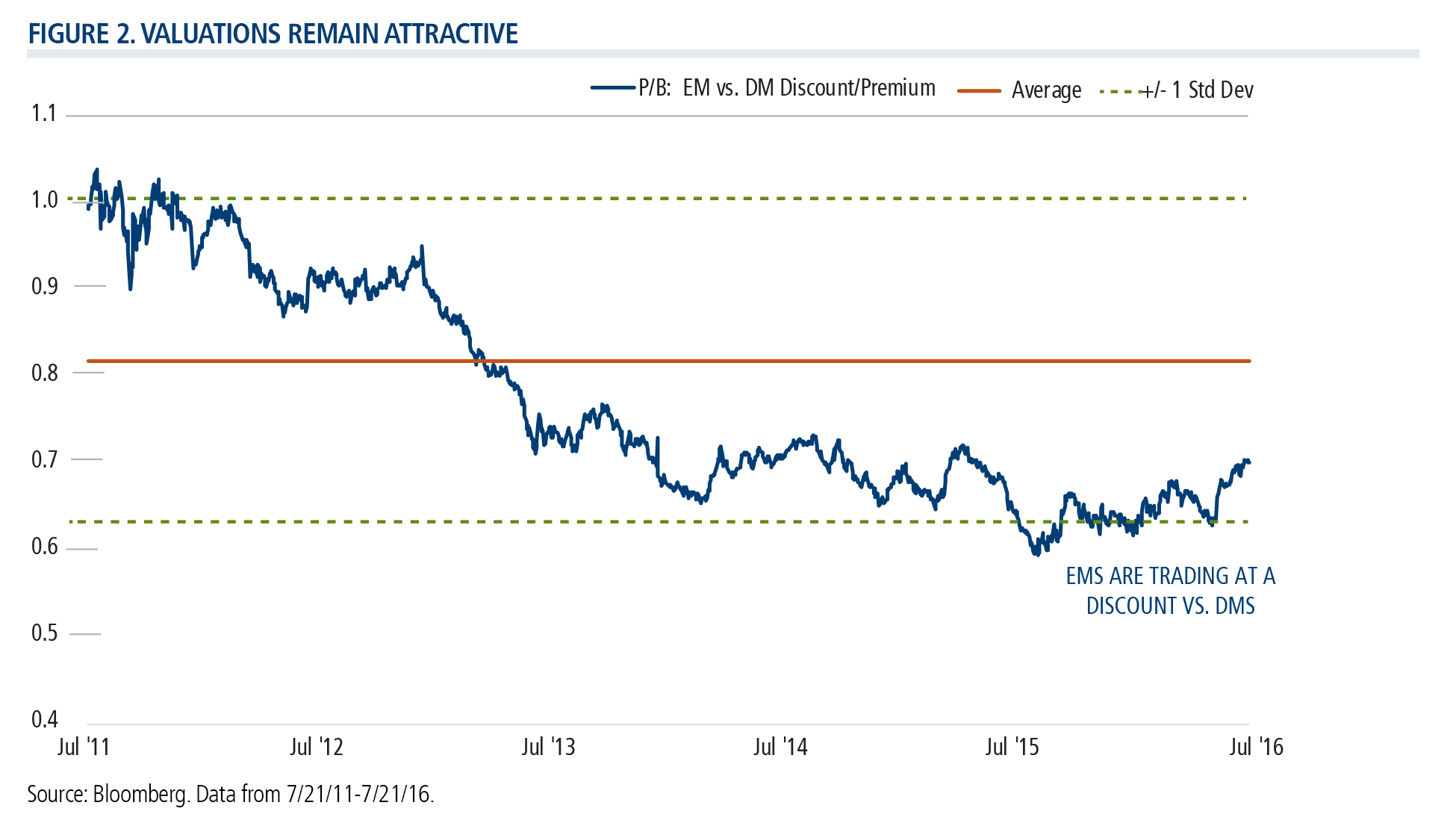

Emerging markets have been trading at a discount relative to developed markets since 2013, as represented by a historical comparison of price-to-book for EMs vs. DMs. To some extent, this reflects the reduced profitability of some companies (in terms of return on equity). However, we believe valuations are supportive to EMs on the whole.

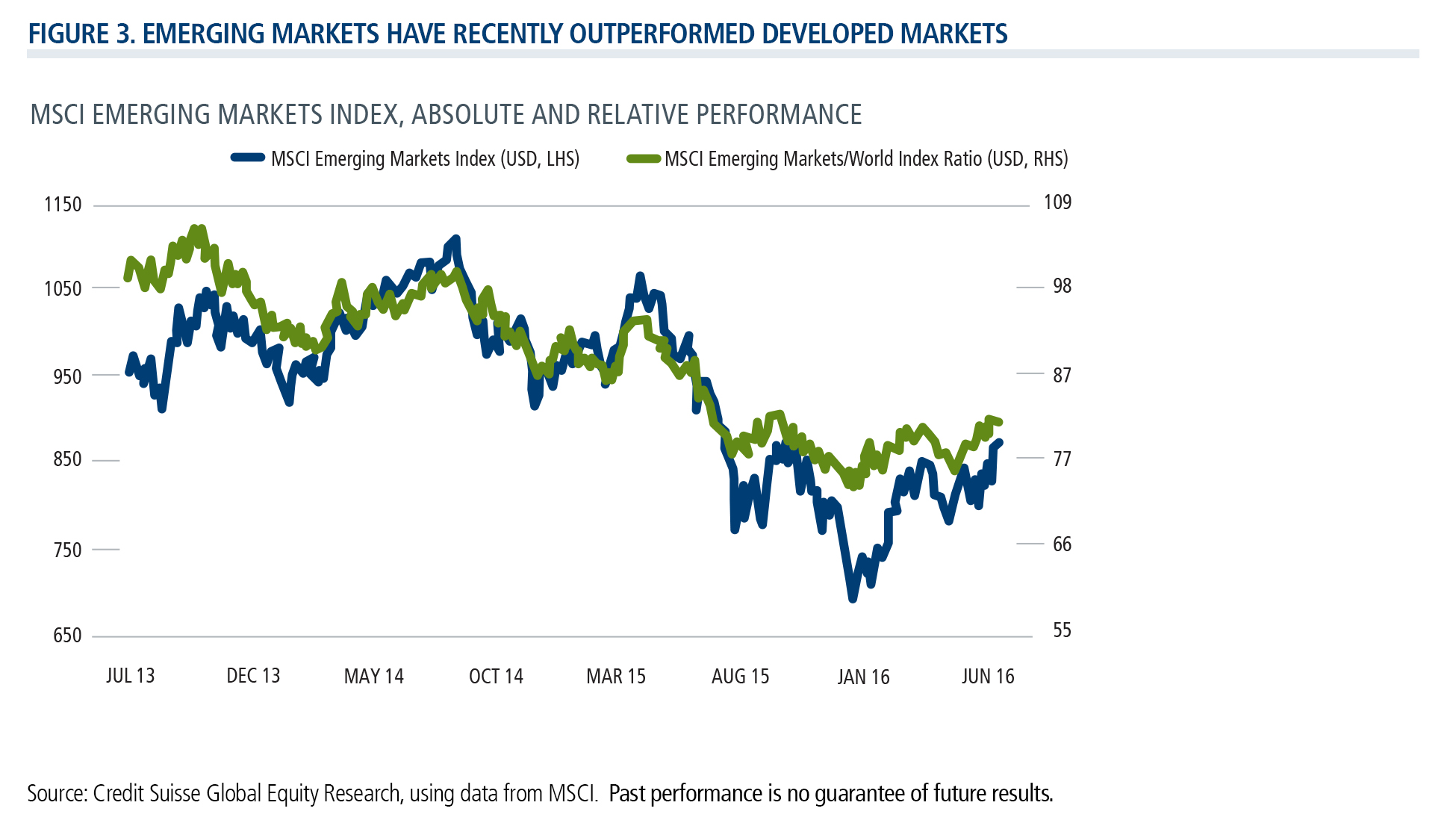

Based on both absolute (blue line) and relative performance vs. developed markets (green line), the EM vs. DM performance ratio has become more supportive for EMs. We believe this could represent a key inflection point.

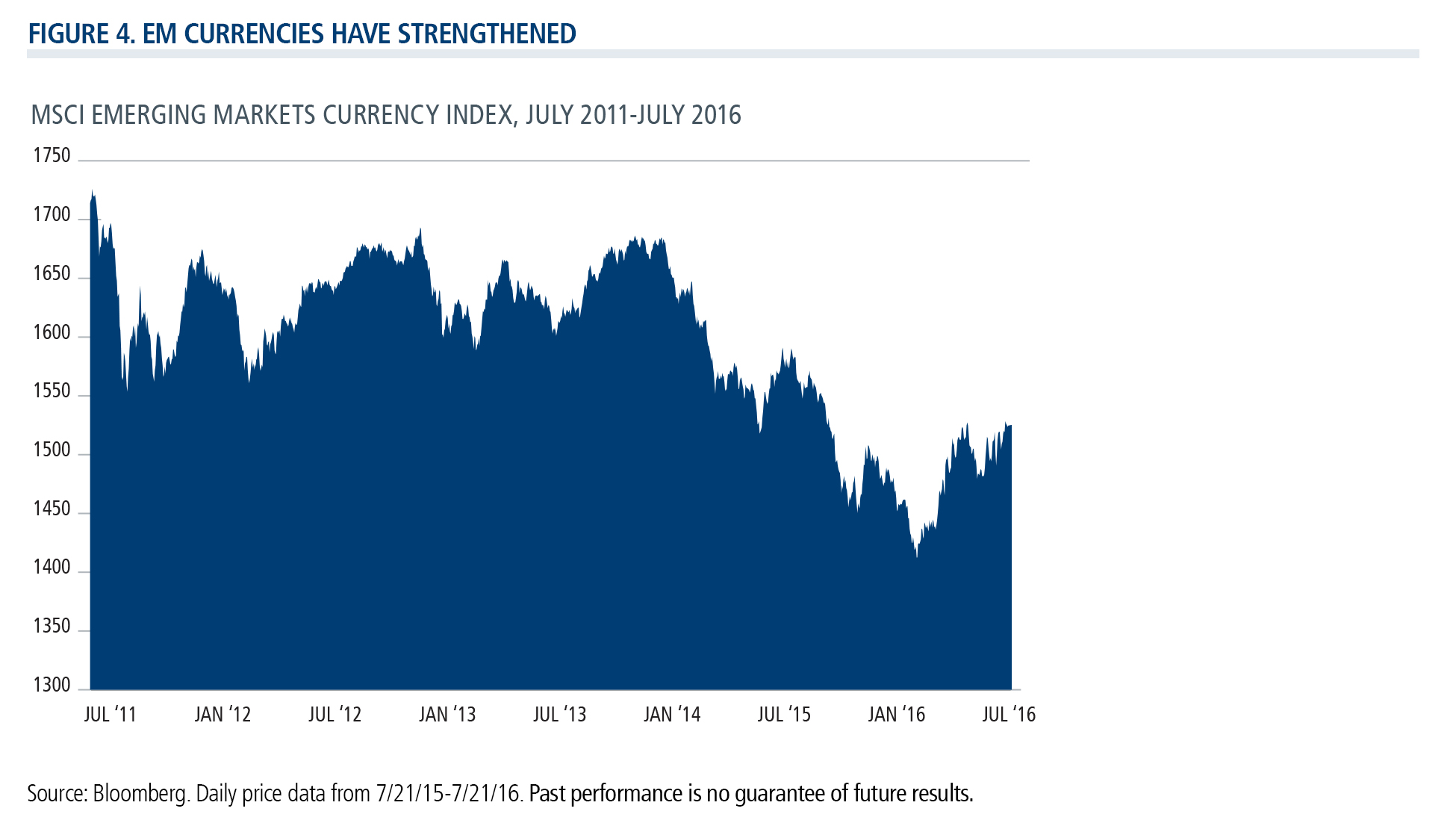

After a few years of considerable headwinds, emerging market currencies have appreciated year-to-date and may support gains in equities.

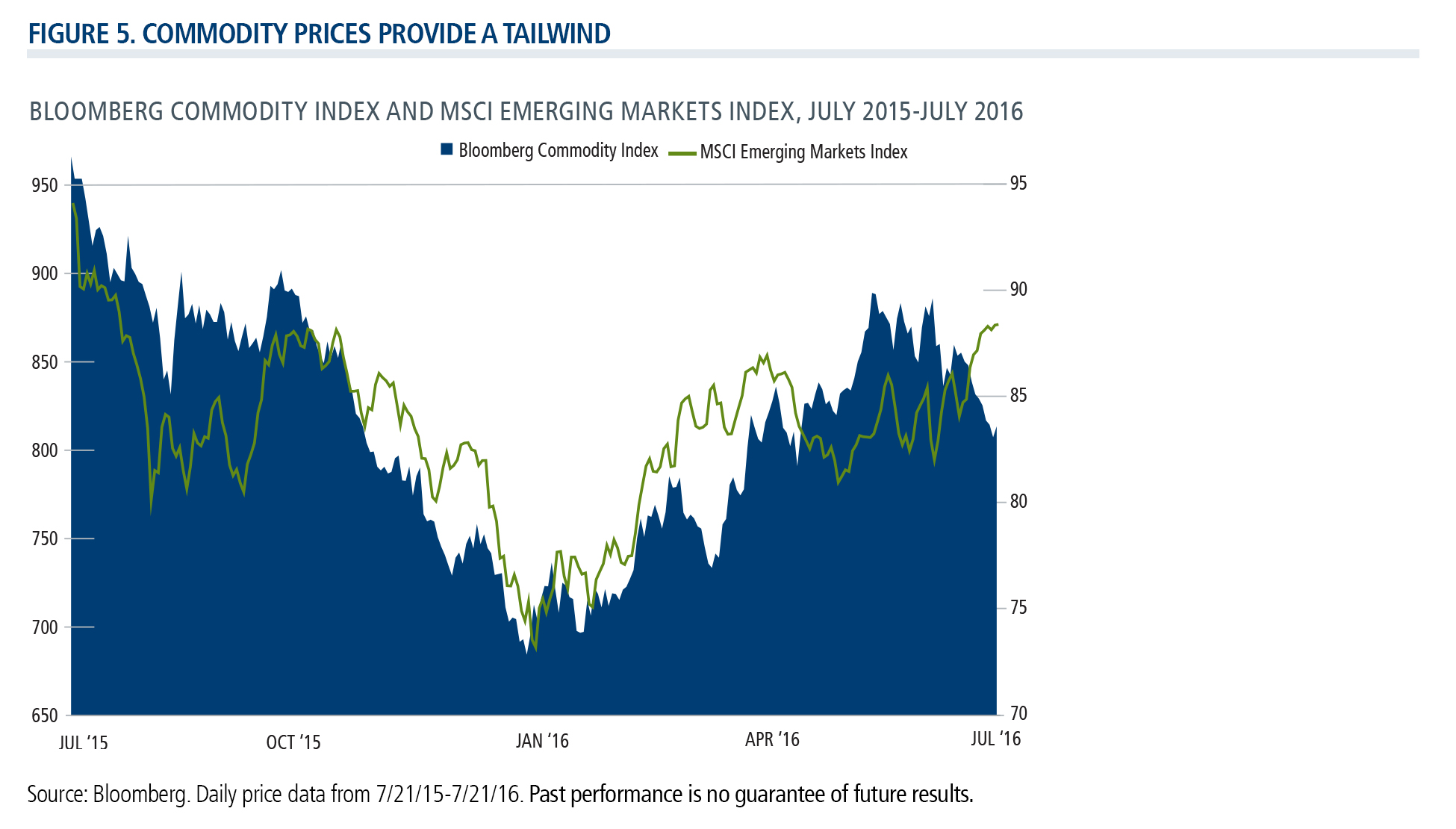

Stabilization in commodity prices may provide another pillar of support to EMs.

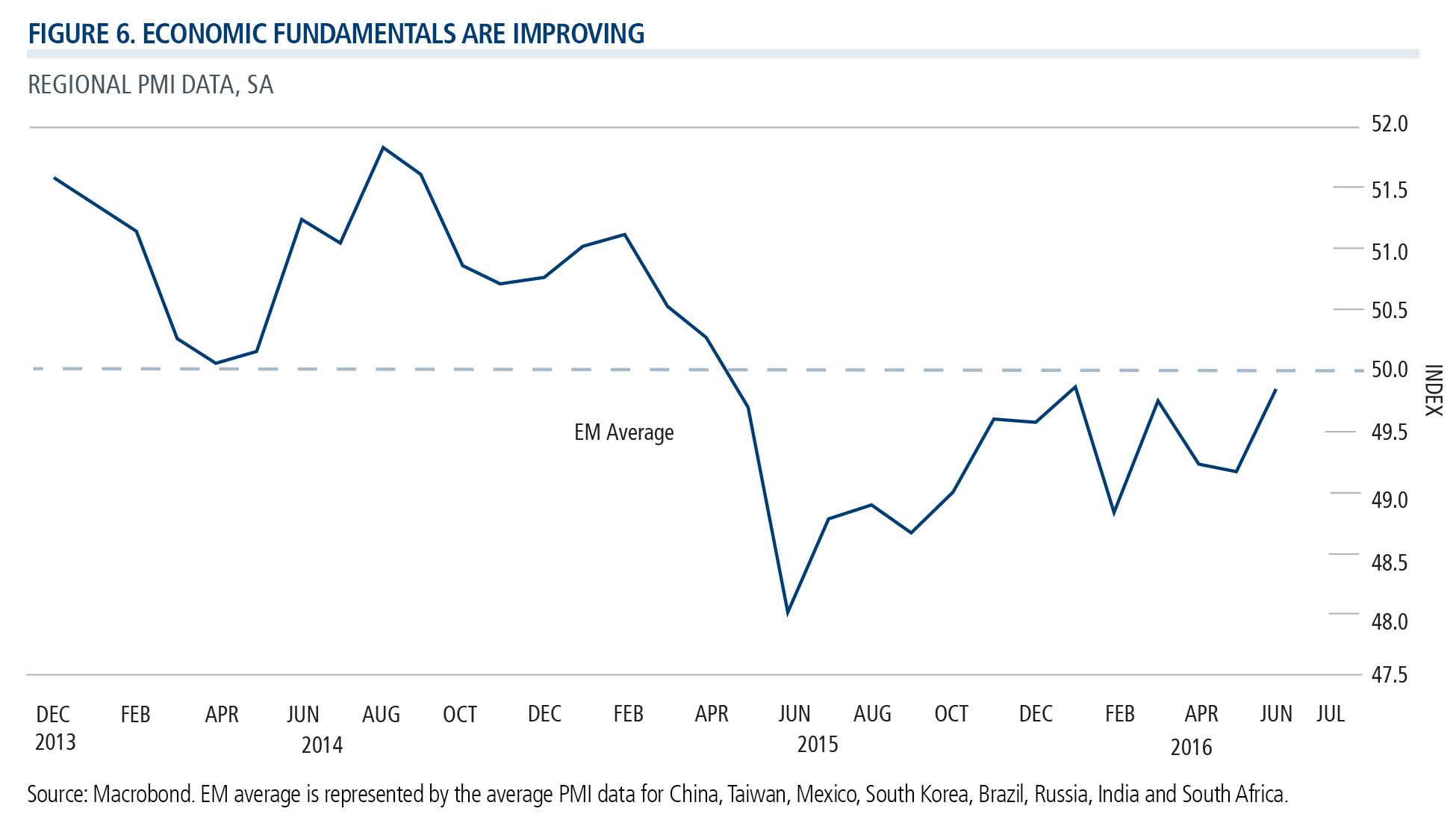

We see signs of improving economic fundamentals for the emerging markets in many areas. For example, the average emerging market PMI, an indicator of economic health of the manufacturing sector, has turned positive and is often a precursor to a broadening pickup in economic growth.

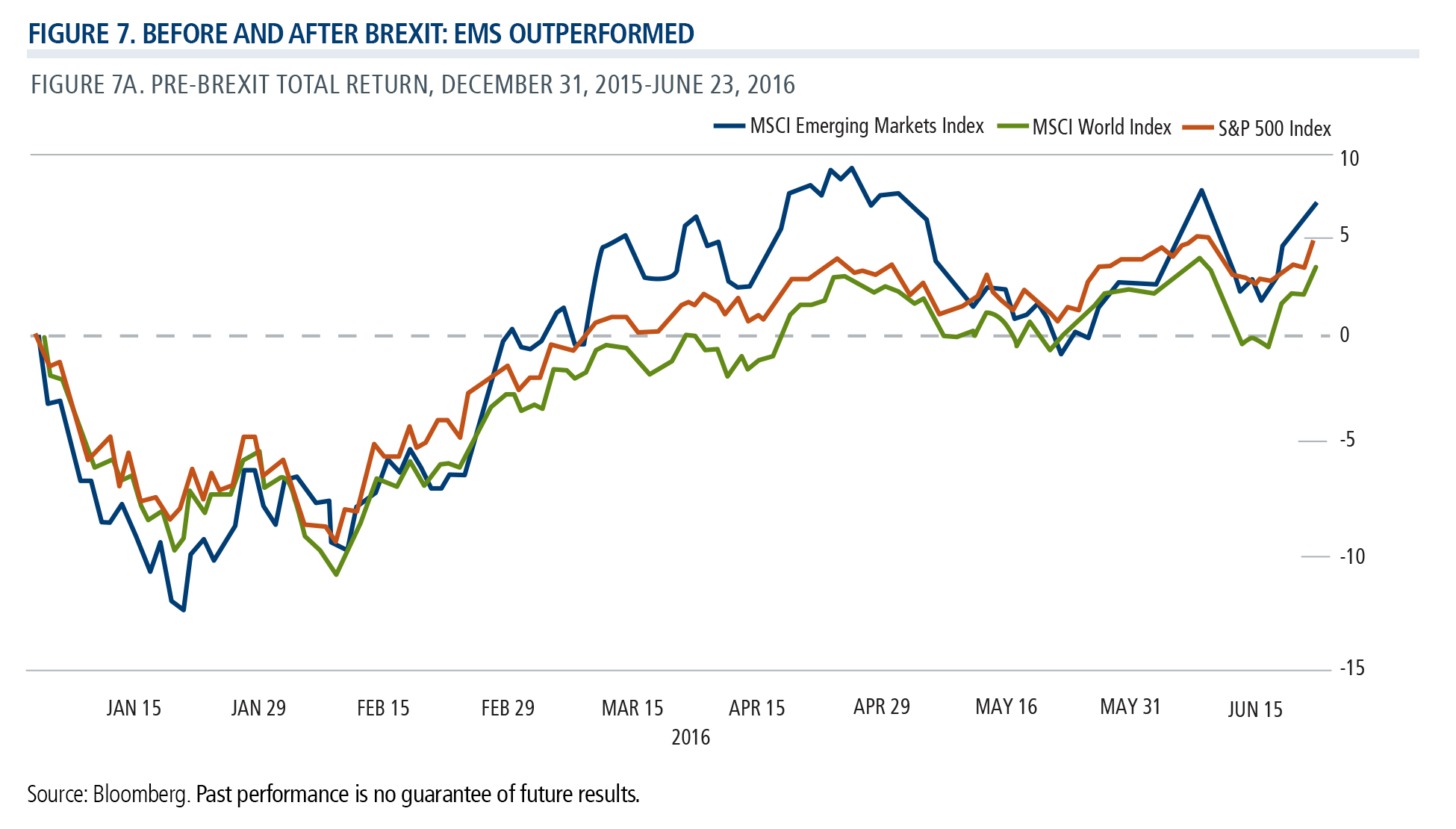

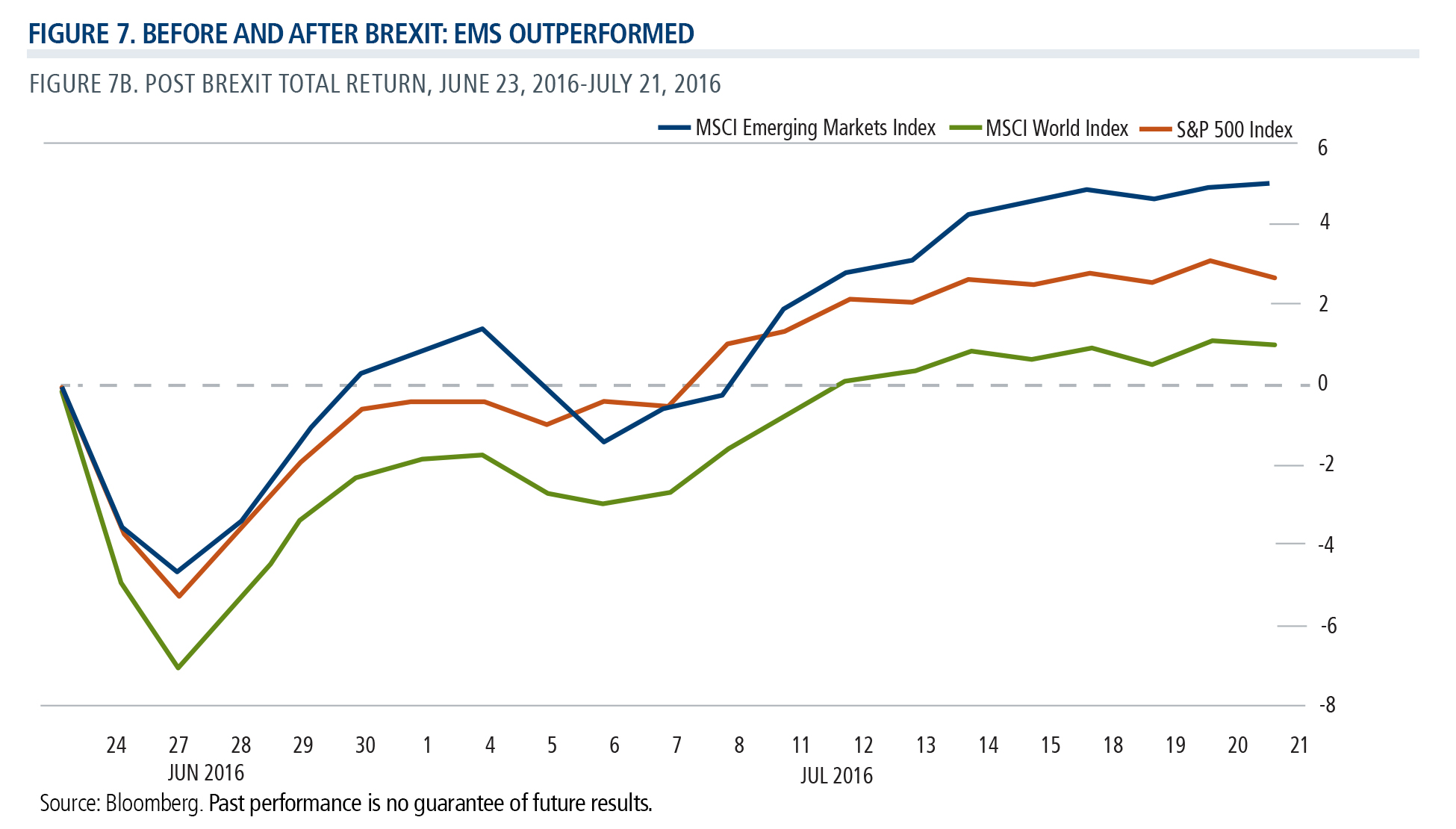

Event risk and policy uncertainty kept many investors on the sidelines. Emerging markets outperformed U.S. and developed market stocks globally, both pre- and post-Brexit.

Positioning

While we see a variety of supportive factors for the emerging markets as a whole, we believe selectivity remains key. Historically, rebounds have been commensurate with the preceding downturn (with the most significant rebounds following the Asian and global financial crises of the late 1990s and 2008, respectively), which we factor into our outlook.

We are maintaining our emphasis on countries that are less tied to commodity prices and those which are moving toward higher levels of economic freedoms. Although economies with lower-quality fundamentals have continued to perform well, we remain concerned about the downside risks associated with countries such as Russia and Brazil. In contrast, prospects look relatively good in Indonesia and India, both of which have cut interest rates. We are also watching the Philippines with great interest, as new leadership looks set to continue with economic reforms. In regard to China, we continue to believe the government has the tools and levers it needs to prevent a hard landing in the near term. Our focus remains on technology and consumption, areas that we believe can benefit from China’s transition to a more balanced consumer-driven economy.

For weekly emerging markets charts and analysis, subscribe to the Calamos EM Snapshot. Subscribe.

Disclosure

Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. We believe the information provided here is reliable, but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The views and strategies described may not be suitable for all investors. The opinions and views of third parties do not represent the opinions or views of Calamos Investments LLC. Opinions referenced are as of July 29, 2016 and are subject to change due to changes in the market, economic conditions or changes in the legal and/ or regulatory environment and may not necessarily come to pass. This information is provided for informational purposes only and should not be considered tax, legal, or investment advice. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations. Indexes are unmanaged, not available for direct investment and do not include fees and expenses. The S&P 500 Index is considered generally representative of the U.S. equity market. The MSCI Emerging Markets Index is a measure of the performance of emerging market equities. The MSCI World Index is a market capitalization weighted index composed of companies representative of the market structure of developed market countries in North America, Europe, and Asia/ Pacific region. The Bloomberg Commodity Index is a broadly diversified commodity price index distributed by Bloomberg Indexes. The MSCI Emerging Markets (EM) Currency Index will track the performance of twenty-five emerging-market currencies relative to the U.S. dollar. Price/Book Ratio-Is a stock’s capitalization divided by its book value. Return on equity is equal to a company’s net income divided by shareholder’s equity. Annualized standard deviation is a statistical measure of the historical volatility of a mutual fund or portfolio.

Foreign Securities Risk — Risks associated with investing in foreign securities include fluctuations in the exchange rates of foreign currencies that may affect the U.S. dollar value of a security, the possibility of substantial price volatility as a result of political and economic instability in the foreign country, less public information about issuers of securities, different securities regulation, different accounting, auditing and financial reporting standards and less liquidity than in U.S. markets. Emerging Markets Risk — Emerging market countries may have relatively unstable governments and economies based on only a few industries, which may cause greater instability. The value of emerging market securities will likely be particularly sensitive to changes in the economies of such countries. These countries are also more likely to experience higher levels of inflation, deflation or currency devaluations, which could hurt their economies and securities markets.

Unmanaged index returns assume reinvestment of any and all distributions and, unlike fund returns, do not reflect fees, expenses or sales charges. Investors cannot invest directly in an index.

Before investing carefully consider the fund’s investment objectives, risks, charges and expenses. Please see the prospectus and summary prospectus containing this and other information or call 1-800-582-6959. Read it carefully before investing.