Executive Summary

Over the last six or seven years, most financial assets have done very well. The performance divide has not been between low-risk assets and high-risk assets or between liquid assets and illiquid assets, but between long-duration assets and short-duration assets. Long-duration assets such as stocks, bonds, real estate, and private equity have benefitted from a large fall in the discount rate associated with their cash flows, while short-duration assets have been hurt by the same fall. Investors tend to tilt their portfolios in favor of those assets that have done well, and today that pushes them to be increasing effective duration in their portfolios, just when the potential returns to those assets have dropped. What we believe would be most helpful to investors are short-duration risk assets, as they offer the potential of decent returns over time with less vulnerability to rising discount rates. These assets, generally lumped together under the “alternatives” title, are generally out of favor today given their disappointing performance since the financial crisis, but the characteristics that made them disappoint may well prove a blessing if discount rates start to rise.

Introduction

In most of the economic ways that count, the years following the financial crisis have been somewhere between disappointing and unspeakably bad. Economic growth in the developed world has been slower than at any comparable period barring the Great Depression. Productivity growth has been the worst since the invention of GDP,1 and corporate investment has remained stubbornly low. According to a McKinsey Global Institute report, two-thirds of households in the developed world had incomes as of 2014 that were flat or fell relative to 2005 (81% of households for the US in particular).2 After a burst of growth in the emerging world associated with China’s enormous stimulus policy of 2008-10, growth has also come to a crawl in the emerging economies, laying bare corruption and structural problems that appeared to be minor when times were better. But in one way, the last seven years have been a glorious success. Performance of most financial assets has been very strong, with assets from US equities to global real estate and infrastructure to credit and government bonds all giving strong returns. Even the laggards – non-US developed and emerging equities – have been disappointing on a relative, though not really an absolute basis. It isn’t all that often that everything does well at the same time. We have been conditioned to think of stocks and bonds as complements to each other, with one doing well when the other does poorly. In this cycle, we’ve gotten an almost magical benefit, where on a daily basis the correlations have been negative, but over the full seven years both assets have gone up strongly, along with most other assets. Apart from emerging equities, the only assets that have really disappointed seem to be commodities, cash, hedge funds, and other hedge-fund-like alternative assets and strategies. We believe there is a common factor that explains much of this. We believe further that it is important to realize that the strong returns to the assets that have done well over the last seven years are at best a one-off benefit and, more plausibly, will have to be given back over time. To us, this suggests that while alternatives have been a drag on institutional portfolios over the last six or seven years and privates (real estate, private equity, venture capital) have been a boost, in coming years the reverse may well be true.3

The duration effect

The common factor that explains much of the return pattern we have seen in recent years is duration. The assets that have done well do not necessarily share that much in common, but they do all share a structure that they embody at least somewhat predictable cash flows that will occur over an extended period of time. The value of those cash flows changes materially if the discount rate applied to those cash flows changes. We are used to talking about the duration of fixed income instruments, but not necessarily for assets like equities, real estate, LBOs, etc. But all of these assets can readily be valued through a discounted cash flow process, and the sensitivity of the present value to a change in the discount rate is precisely analogous to the duration of a fixed income security.

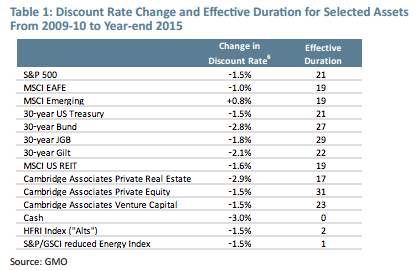

And what has happened to those discount rates is pretty uniform across asset classes.4 Table 1 shows an estimate of the change in the discount rate from a 2009-10 average to year end 20155 along with an estimate of the effective duration of the asset class with regard to that change.

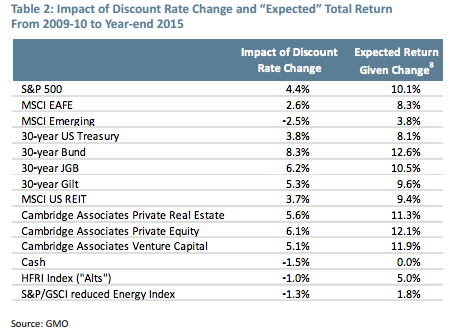

Emerging equities is the only asset class for which the discount rate seems to have risen over the period, and that move certainly does feel idiosyncratic to emerging. Otherwise, discount rates have fallen somewhere between 1% and 3%, with a median of 1.5% and an average of 1.7%. But while the discount rates have all done similar things, the impact on asset classes has varied because of differing durations of the assets. I apologize for the overly precise effective durations for the asset classes in Table 1. They range from mathematically true for the government bonds, to true for a given split between growth and income for equities, to educated guesswork in the case of private equity and venture capital. But, to me, the striking discrepancy is between the first 11 asset classes and the last 3. For any asset with a long duration, the discount rate fall has been a decided positive for returns for the asset class. But for short duration assets, it has actually been a negative. This occurs because there are two sides to the fall in discount rates. It increases the present value of distant cash flows, but it also decreases the current income available on the asset. The negative side of this is simplest to think about in the case of cash. Cash is the purest short duration asset. If cash rates fall, there is no capital gain to enjoy, but the income earned in subsequent periods will be reduced. The 3% fall in the discount rate for cash in this case means that relative to the 2009-10 market expectation of where cash rates would be at the end of 2015, we actually wound up 3% lower. As a result, the impact of the fall in the discount rate was approximately -1.5%.7 That is to say, relative to market expectations from 2009-10, cash investors achieved about 1.5% less than they originally bargained for through 2015. The impact for a holder of a constant maturity 30-year Treasury bond portfolio, on the other hand, was a windfall of 3.8%. Yes, the investor did receive less income over the period because the yield on the bonds fell, but that impact was swamped by the gain from the higher present value of the future cash flows. We can see this for all of the assets in Table 2.

The first column in the table shows the impact of the change in the discount rate, incorporating both the change in price and change in income. The second column shows the total expected return given the actual change to the discount rate. The point of this is to be able to look at what asset classes have done relative to a reasonable expectation of what they should have given this one important factor. This is shown in Table 3.

Even given the change in discount rates, there were some surprises. REITs have done surprisingly well behind pretty strong FFO (funds from operations) growth, the S&P 500 has done surprisingly well behind good earnings growth, and commodities have done impressively badly as boom turned to epic bust.

But the most striking thing to us is how the gap between the privates and alternatives shrinks profoundly when we take out the discount rate shift. We all learned in 2008 that alternatives (which are often packaged as hedge funds but do not have to be) contain some pretty equity-like risks when things go badly wrong. But since then, while the S&P 500 has risen 15% a year, “privates” have risen similarly, and even dopey old US Treasury bonds have made 7.9%, alternatives, as proxied by the HFRI hedge fund index, have risen a paltry 4.2%. Far from the “equity-like returns for bond-like risk” they were sold as, they have proven to be “sub-bond-like returns for bond-like risk.”

Portfolio implications

Given this pattern, it is no surprise that many institutional clients are questioning their allocation to alternatives and increasing their allocation to private assets. In general, there has not been a particularly apparent rush into long-duration fixed income despite the strong returns, because the simple math of bonds is such that most investors realize intuitively that falling bond yields are a negative for future returns. But there has been continued enthusiasm for strategies that have the same effect – notably risk parity variations – because they allow investors to think that, despite the massive holdings of bonds in these portfolios, they are “balanced” and reasonably safe even against scenarios that involve rising rates.

But the trouble with returns that come from falling discount rates is that they represent an increase in the present value of the asset without any increase to the cash flows to the asset class. The future expected return to the asset has fallen, and in a way that more or less precisely counteracts the increase in current value. In other words, the present value of the assets has risen but the future value of the assets has not. Nowhere is this clearer than for the purest long-duration asset in existence, the zero coupon bond. Let’s say that you will need, with absolute certainty, $1 million in 2026. The safest way to reach that goal is to buy a $1 million face value 10-year zero coupon Treasury bond maturing in 2026. Such a bond currently has a yield of 1.625%, which means it will cost you $851,127 to buy it today. Assume that tomorrow the yield falls by 1% to 0.625%. Your brokerage statement will declare the value of your bond to be $939,596, a gain of over $88,000. Whoopee! You’ve just made over half of the necessary return over the next 10 years in a single day. But the value of that bond in 2026 has not changed at all. It has a fixed maturity value of $1 million. The only thing that has changed is the discount rate being applied to that cash flow, not the cash flow itself. Assuming you still need $1 million in 2026, there is no windfall to spend. Economically, nothing has changed for you, whatever your brokerage statement says.

This is the nature of the discount-rate-driven gains for asset classes such as equities, bonds, and real estate. Beyond the discount rate change, it is still true that US equities have done surprisingly well, emerging equities surprisingly badly, and so on. But even if those “surprises” are permanent (and our guess is that for the most part they are not) the fact that the valuation of US equities has risen guarantees that the future returns to US equities from here will be lower than they would have been otherwise, and the same is true for all of the long-duration assets whose discount rates have fallen over the period.

The most shocking hole that will be blown through people’s portfolios is if discount rates rise again fairly quickly. Even if the circumstance is one in which the global economy is doing well, the impact of a 1.5% increase in the discount rate on equities from here is a fall of over 30%, which would almost certainly be enough to swamp the earnings impact of the decent growth. For bonds, of course, there would be no possible counter to the discount rate effect. For a portfolio that is fully invested in long-duration assets (i.e., consists of a combination of stocks, bonds, real estate, and private equity), the possible performance implication is on the order of the falls experienced in the financial crisis – perhaps a 20-33% fall depending on the weightings – despite the fact that the global economy was doing just fine.

So what can we do to protect portfolios against this possibility? One answer would be to hold cash, which, as a zero-duration asset, would be a beneficiary of rising discount rates. The trouble with cash, of course, is that if the discount rates do not rise, it is doomed to deliver little or nothing. What we would ideally like is to hold a short-duration risk asset – one where if nothing changes we are getting paid a decent return but where a rising discount rate will not destroy multiple years’ worth of returns. We believe alternatives fit the bill pretty well. If things hold together, we should expect to make money from activities such as merger arbitrage or exploiting carry trades or global macro. If the world does surprisingly well and causes investors to raise their expectations for discount rates, these strategies should be largely unaffected and could still make money. If we head into a severe recession or financial crisis, they will presumably lose money, as we saw in 2008, but that is no different from other risk assets.10 To be clear, I’m not arguing that the returns to alternatives are likely to be a lot higher than we have seen since 2009-10. Alternatives have been mildly disappointing since 2009, doing almost 1% worse than one might have expected. The more sobering truth is that the 4.2% return they have achieved since then simply looks pretty good given the other choices on offer, and their lack of vulnerability to rising discount rates is a comfort in a world where almost everything in a traditional portfolio is acutely vulnerable to discount rate rises should they happen.

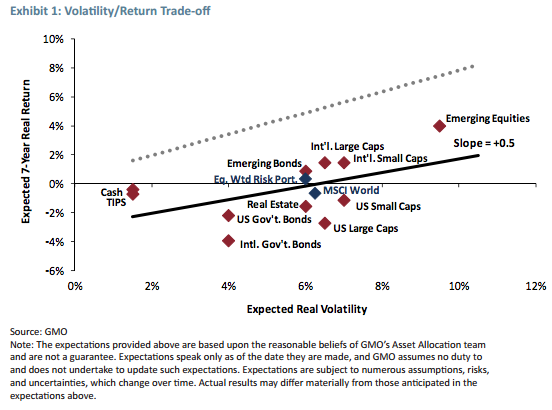

Today does not look like a great opportunity to reach for risk, despite the temptation in the face of unprecedentedly unattractive yields on government debt. Exhibit 1 shows a simple way of looking at the risk/reward trade-off available to investors today. It takes our seven-year forecasts for asset classes and plots the expected returns against expected volatilities for the assets.11

Volatility is an admittedly flawed proxy for risk, but for the point I am trying to make here it does the job. The key aspect of the chart is the regression line drawn through the cloud of points. This tells us the general relationship between volatility and return available today. The slope of the line at equilibrium would be about 0.7. Today it is 0.5, although arguably even that flatters the attractiveness of risk assets because a fair bit of the slope comes from the extremely unattractive returns on offer from non-US government bonds, which today have an average yield of 0.16%, and most of the rest comes from emerging equities, which happens to be both the cheapest and most volatile asset of the group. But taking the figure at face value, expected risk premia are positive today, if lower than average. The most striking thing about the chart is how low the regression line is on the page. The dotted line above shows what the line would look like at equilibrium. While it is true that today’s slope is somewhat flatter than normal, the striking difference is how much lower the line is on the page than equilibrium – four to five percentage points lower! I admit that it is possible we are overstating this gap. Our forecasts assume that discount rates move back to “normal” over the next seven years, and it is possible that the discount rate falls we have seen are, in fact, permanent. If so, the damage is “only” the 1-3% falls we have seen in discount rates. But either way, we believe two things are clear. First, market prices give no indication that this is a good time to move risk up in your portfolio. Perhaps one could make an argument for taking close to a normal amount of risk, but certainly not more. And second, the expected return to a normal portfolio today is somewhere between meaningfully lower and stunningly lower than normal.

Conclusion

The unwelcome truth is that there is not a tremendous amount investors can do about the fall in prospective returns. If the shift is permanent – the “Hell” scenario we’ve written of before – returns will be lower to all assets for which the discount rate has fallen, but at least the windfall gains will have to be repaid only very slowly. If the shift is temporary, we will wind up giving back the windfalls of the last six to seven years. The temporary shift scenario is better for investors in the long run, but it would be massively painful in the interim, because it will affect almost every asset in most investors’ portfolios.

The charm of alternatives today is that we believe they should perform similarly in either the temporary or permanent shift scenario, and there are almost no other assets with expected returns above cash for which that is the case. The problem with alternatives is that they are more complicated to manage than traditional assets, generally have higher fees associated with them, and require more oversight. Normally, those problems are enough to make them less appealing than traditional risk assets such as equities and credit. Today, however, they seem well worth the extra effort. Their generally disappointing performance over recent years, rather than a sign to dump them once and for all, should probably be recognized as a signal of their potential utility in the market environment we face in the coming years.

There is no panacea for the low returns implied by asset valuations today. Anyone suggesting differently is either fooling themselves or trying to fool you. But piling into the assets that have been the biggest help to portfolios over the past several years, as tempting as it may be, is probably an even worse idea than it usually is. And a deeper analysis of what led returns to be disappointing for the asset classes that have lagged may help investors avoid the error of abandoning decent assets just when their time may be about to come.

Ben Inker is co-head of GMO’s Asset Allocation team and is a member of the GMO Board of Directors. In addition, he oversees the Developed Fixed Income team. He joined GMO in 1992 following the completion of his B.A. in Economics from Yale University. In his years at GMO, Mr. Inker has served as an analyst for the Quantitative Equity and Asset Allocation teams, as a portfolio manager of several equity and asset allocation portfolios, as co-head of International Quantitative Equities, and as CIO of Quantitative Developed Equities. He is a CFA charterholder.

Disclaimer: The views expressed are the views of Ben Inker through the period ending July 2016, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2016 by GMO LLC. All rights reserved.

1 This is a little less impressive than it sounds, given that GDP wasn’t created until the middle 1940s, but nevertheless.

2 “Poorer than their parents? A new perspective on income inequality,” McKinsey Global Institute, July 2016.

3 Venture capital might be an exception to this. As Jeremy Grantham has written, venture capital has some unique characteristics that may well accrue to its benefit in this cycle. It is the hardest asset class to make any sweeping generalizations about entrance valuations; it can be a significant beneficiary of the high return on corporate capital that currently exists in the US; and, as the most volatile asset around, is probably least plausibly affected by a change in the yields to low-risk assets. Even with these characteristics, assuming it could continue its fairly torrid returns of the last cycle seems like a real stretch.

4 I have to admit that part of the reason for the apparent uniformity is that for asset classes for which I couldn’t really estimate a discount rate (private equity, venture, commodities, alternatives) I used 1.5%, which is the same as the US 30-year Treasury and the S&P 500.

5 I wanted to take a starting point that was approximately “normal” for the asset classes. Each asset recovered from the financial crisis at a slightly different rate, so taking an average level from the entire 2009-10 period seemed that it would be rough justice for “normal” for most assets.

6 For equities, this is calculated as the change in the Shiller P/E for the asset class. For bonds, the change in the yield; for REITs, the change in dividend yield for equity REITs; for real estate, the fall in the aggregate cap rate for commercial real estate; for cash, the difference between the actual cash rate in 2015 and the average five-year/one-year forward rate. For private equity, venture capital, alternatives, and commodities, I used the change for US equities as a proxy.

7 This assumes that rates were expected to increase linearly over the period. While this wasn’t strictly true, it is close enough for our purposes here.

8 The “expected” total return reflects the impact of the discount rate change and the “normal” return to the asset if discount rates had remained constant and is included for illustrative purposes only. It is not a projection or an expectation that GMO has or has had at any point in time.

9 The returns are for total return indices, annualized between an average of the 2009-10 levels and year-end 2015, for the following indices: S&P 500; MSCI EAFE; MSCI Emerging; Datastream constant maturity indices for the US, German, Japanese, and UK 30-year bonds; the MSCI US REIT index; the Cambridge Associates indices for commercial real estate, private equity, and venture capital; the HFRI fund weighted hedge fund index; and the S&P/GSCI reduced energy index.

10 Actually, global macro is quite likely to be an exception to this. It is clearly an alternative asset, and has had long-term performance similar to that of the other alternatives mentioned. But its return pattern has been notably different. Many global macro funds have been able to make money during turbulent times and have tended to struggle when things are calm. If they can pull off that pattern and give a decent return above cash over the cycle, they are arguably more valuable to a portfolio than the “riskier” alternatives. The flip side is that it is harder to understand exactly why returns should be sustainably above cash for the general sector, given the return pattern is one you’d generally expect to pay for.

11 If the volatility scale looks odd, it is because it is annualized seven-year volatility, which is, to a first approximation, traditional annualized volatility divided by the square root of seven.

© GMO