“Insanity is doing the same thing, over and over again, but expecting different results.”

“We cannot solve our problems with the same thinking we used when we created them.”

- Albert Einstein

US equity indices reached new, all-time highs following Britain’s late-June “Brexit” vote. Yet, domestic equity markets have essentially moved sideways for the past eighteen months. The same goes for global equities. Even the unassertive descriptor “sideways” overstates the case – the full path of US equity markets during the period included three bouts of significant downside volatility.

Interestingly, the most recent few weeks have been positive for just about every asset class. Following the initial risk-off reaction to the Brexit vote, equities rebounded while “haven” assets such as US Treasury bonds and gold continued to rise. The best explanation we have come across is as follows: sovereign debt (including long-dated US Treasury bonds) rallied as the European Central Bank (ECB) and Bank of England promised still more accommodative policy. This drove yields on European sovereign debt further into negative territory. Still risk-tolerant and willing to reach for yield, investors drove equities (particularly dividend-oriented equities) higher. Gold, too, rallied, as ultra-low fixed income yields minimize the opportunity cost of owning gold and gold buyers seemingly believe the only possible outcome from all of the central bank intervention is permanent debt monetization (and with it, permanent currency debasement).

Despite the oil collapse that began in late 2014 and resumed in earnest in the middle of 2015, the Chinese growth scare from late 2015 through early 2016, and the more recent Brexit panic, some signs of investor risk seeking have emerged. These indicators have us willing (somewhat compelled) to commit additional capital to risk assets. However, there has been no real resolution in either the energy sector or China, valuations remain stretched, economic fundamentals continue to slow, and longer-term measures of investor sentiment continue to point toward investor risk aversion. Thus, any additional risk taking on our part will be incremental, paced, and judicious.

It’s the Central Bankers’ market; we’re all just livin’ in it.1

As of the end of June 2016, the world’s four major central banks (the Federal Reserve, the European Central Bank, the Bank of Japan – BOJ, and the People’s Bank of China – PBOC) had expanded their asset totals to $17.2 trillion dollars. This is an increase from $16.4 trillion just three short months earlier, $15.6 trillion at the end of 2015, and just over $5 trillion at the end of 2006. ECB and BOJ asset purchases are responsible for the recent increase, as the Fed and PBOC have held asset levels relatively constant of late.

No matter the problem, the central banks can solve it. Worried about China’s growth? Don’t, the Federal Reserve will just hold off raising rates. Another weak quarter of Japanese growth? No problem, the Bank of Japan will just buy some equity exchange traded funds. Afraid of what Brexit might portend? You shouldn’t be, the European Central Bank and the Bank of England will just keep buying assets.

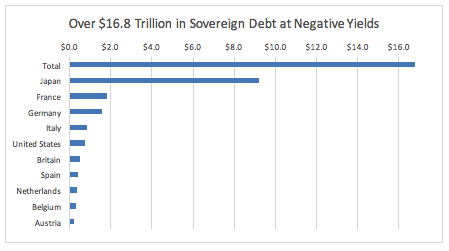

The impact of recent central bank actions has been particularly acute in the prices of sovereign debt. In last quarter’s letter, we presented a graphic showing the almost $8 trillion in global sovereign debt that traded at negative yields. As we wrote then: “That is correct – borrowers are paying to hold securities issued by Japan and fifteen European countries.” Well, the weird got weirder. Today, sovereign debt trading at negative yields tops $16.8 trillion dollars!

Source: The Bloomberg

Equities: Modest Progress, Significant Downside Volatility

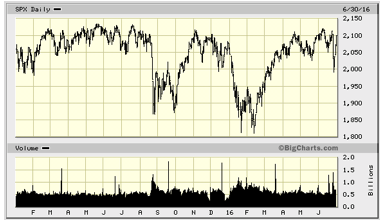

Despite central banks’ aggressive efforts, broad, global equity markets barely changed over the past eighteen months and experienced three meaningful downturns. The MSCI All Country World Index is down 0.2% over the period from January 1, 2015 through June 30, 2016.

Source: Bigcharts.com

From January 1, 2015 through June 30, 2016 the S&P 5002 returned 5% including dividends.

Source: Bigcharts.com

Similarly, from January 1, 2000 through June 30, 2016 the S&P 500 returned 72% including dividends and experienced two 50% multi-year drawdowns. Over sixteen and a half years, this is just 3.3% annualized.

Source: Bigcharts.com

Valuations

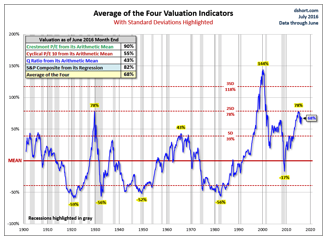

US equity valuations remain at significantly elevated levels as the following chart, courtesy of Doug Short, highlights. A combination of four valuation measures shows the S&P 500 to be 68% above its historical average implying downside risk in order for markets to return to historical fair value.

Source: dshort.com

Other valuation measures look worse. Ned Davis research publishes a chart depicting the historical price to sales (P/S) ratio of the median stock in the S&P 500 index. That P/S ratio for the median stock has never been higher.3 It currently stands at 2.22x and is over 2 standard deviations above the historical median P/S ratio. A correction to the historical median of 0.9 would mean almost 60% downside!

Deteriorating Fundamentals

Unfortunately, investors buying risk assets at today’s elevated prices cannot point to improving economic and corporate fundamentals as rationale. Industrial production has been persistently slowing since the beginning of 2015.

Source: fred.stlouisfed.org

Likewise, the consumer portion of the economy is weakening. Retail sales growth has been persistently slowing since peaking all the way back in 2011.

Source: fred.stlouisfed.org

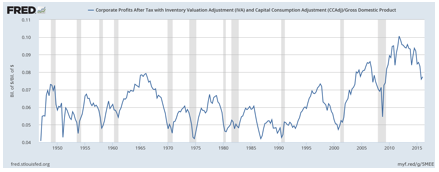

The corporate world looks similar. Corporate profit margins4 rose to their highest level on record in the fourth quarter of 2014. They have since deteriorated. Yet, profit margins remain well above their historical average, implying additional downside risk. Profit margins mean-revert because high profit margins lead to competition – that is capitalism in a nutshell.

Source: fred.stlouisfed.org

Corporate sales growth has been slow for some time and recently began to turn negative. Decreasing sales and contracting profit margins have put pressure on earnings. S&P 500 earnings per share (EPS) have been lower year over year for the last four quarters. Lower earnings make it harder for stock prices to rise.

Source: http://us.spindices.com/indices/equity/sp-500

And, Yet…

Investors have returned to risk seeking. Whether due to a lack of significant enough economic turmoil and corporate impairment, or simply because unprecedented (and dangerous) central bank behavior continues to induce yield chasing (for now), any investor panic remains short lived. One primary statistic we study to assess investor risk preference is credit spreads. Credit spreads have been narrowing for months now and recently flipped to narrower on a year over year basis. It is a blunt tool, but the signal is unambiguous.

Source: The Bloomberg

Most trend-following statistics are equally bullish. Nonetheless, longer-term measures of investor risk aversion show diminishing breadth (increasing investor selectivity). As of the July 7, 2016 market high, Lowry’s reports only 16% of stocks in their “operating company only” universe were within 2% of their all-time highs. Additionally, 36% of stocks in this same cohort were already down 20% or more. The rally is thin and getting thinner by the day.

Conclusion

Central bankers ignore Einstein’s wisdom. Artificially low interest rates led to the housing boom and bust in 2008. The same thinking has led central banks to expand their collective balance sheets threefold since the “great recession.” Today, the thinking seems to go, if low rates and asset purchases are not enough to stimulate the real economy, we will make rates negative and buy even more assets. Central bankers’ insistence on doubling down on insanity, increasing the stakes, will eventually lead to an economic catastrophe greater in magnitude than the great recession of 2008.

Valuations and the long-term destabilizing effect of the central banks’ actions keep us cautious. However, we recognize the shorter-term indicators that signal investors’ willingness to accept risk. We are cautiously adding to our risk (mostly equity) exposure, but maintain an all-weather balance with exposure to US Treasury bonds, gold, and cash.

*****

As always, if you have any thoughts regarding the above ideas or your specific portfolio that you would like to discuss, please feel free to call us at 1-888-GREY-OWL.

*****

Sincerely, Grey Owl Capital Management Grey Owl Capital Management, LLC

This newsletter contains general information that is not suitable for everyone. The information contained herein should not be construed as personalized investment advice. Past performance is no guarantee of future results. There is no guarantee that the views and opinions expressed in this newsletter will come to pass. Investing in the stock market involves the potential for gains and the risk of losses and may not be suitable for all investors. Information presented herein is subject to change without notice and should not be considered as a solicitation to buy or sell any security. Any information prepared by any unaffiliated third party, whether linked to this newsletter or incorporated herein, is included for informational purposes only, and no representation is made as to the accuracy, timeliness, suitability, completeness, or relevance of that information.

The stocks we elect to highlight each quarter will not always be the highest performing stocks in the portfolio, but rather will have had some reported news or event of significance or are either new purchases or significant holdings (relative to position size) for which we choose to discuss our investment tactics. They do not necessarily represent all of the securities purchased, sold or recommended by the adviser, and the reader should not assume that investments in the securities identified and discussed were or will be profitable. A complete list of recommendations by Grey Owl Capital Management, LLC may be obtained by contacting the adviser at 1-888-473-9695.

Grey Owl Capital Management, LLC (“Grey Owl”) is an SEC registered investment adviser with its principal place of business in the Commonwealth of Virginia. Grey Owl and its representatives are in compliance with the current notice filing requirements imposed upon registered investment advisers by those states in which Grey Owl maintains clients. Grey Owl may only transact business in those states in which it is notice filed, or qualifies for an exemption or exclusion from notice filing requirements. This newsletter is limited to the dissemination of general information pertaining to its investment advisory services. Any subsequent, direct communication by Grey Owl with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of Grey Owl, please contact Grey Owl or refer to the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov).

For additional information about Grey Owl, including fees and services, send for our disclosure statement as set forth on Form ADV using the contact information herein. Please read the disclosure statement carefully before you invest or send money.

1 Apologies to Dean Martin and Frank Sinatra.

2 All references to S&P 500 returns in this section are for the investable SPY ETF.

3 Ned Davis Research’s data goes back to 1964.

4 As a percentage of gross domestic product.