Newsletter, Vol 9, No 4 - July 2016

TOPSY TURVEY

From InvestmentNews, this rather extraordinary reminder…

Long-term Treasury securities have outperformed the Standard & Poor’s 500 stock index for the past 10 years. The SPDR S&P 500 ETF (SPY) has gained an average 7.27% over the past decade, according to Morningstar Inc. But the iShares 20+ Year Treasury Bond ETF has gained an average 9.31% during the same period.

From a very long-term historical perspective, this is an anomaly. Long-term government bonds have earned an average 5.64% per year since 1926, while large-company stocks have gained an average 10.01% per year. (Both figures assume reinvested interest and dividends.)

SOME PEOPLE NEVER GET OLD

From my friend Peter…

THE INTELLIGENT INVESTOR

Jason Zweig writes this column for the Wall Street Journal, but I think it should be named The Intelligent Journalist. Jason has a long history of providing his readers with valuable advice. His article following the Brexit news was a wonderful example.

“The More It Hurts the More You Usually Make Investors hate uncertainty, but they despise surprise. And the ability to withstand the shock of surprise is what separates great investors from everyone else.”

Wise words worth remembering when the world seems to be falling apart.

GRAIN OF SALT

I’ve written before about my skepticism of the Barron’s Top 100 Financial Advisors list, largely based on the fact that it is entirely dominated by brokers at major financial services firms. Although I am admittedly biased, I don’t find it credible that there are almost no fiduciary-based investment advisors who make the cut. It seems I’m not alone. Fitapelli Kutra, a New York law firm, recently issued a press release noting:

Every year Barron’s Magazine issues its list of the top 100 financial advisors in the United States. According to Barron’s, a proprietary ranking system is used to rank advisors based on a number of factors, which include production revenue [my emphasis] and an evaluation of each advisor’s regulatory record. Fitapelli Kurta reviewed Barron’s 2016 ranking and learned that an alarmingly high number of the advisors on the list have some regulatory disclosures, which include suspensions by securities regulators, customer complaints, a termination and millions in settlements and arbitration awards. The information for this press release was gathered by looking up each financial advisor’s BrokerCheck report, which is made publically available by the Financial Industry Regulatory Authority, or FINRA.

What brought this to the attention of the media was the recent case of broker Dawn Bennett. As the release noted:

One high profile example of why this ranking system is so flawed is Dawn Bennett. Ms. Bennett was previously ranked as a top 100 advisor despite having a $450,000 settlement payment disclosed on her license. This week Ms. Bennett was barred from the securities industry and ordered to pay $4 million in fines and disgorgements. It gets worse. According to a March 2, 2016 brief, the SEC alleged that Ms. Bennett made false submissions to Barron’s to be included in the rankings in “[an] attempt to boost a fledging advisory practice.

So much for Barron’s ratings.

TURNS OUT THE OBVIOUS ISN’T SO OBVIOUS

Speaking of Brexit, the WSJ notes that “[i]n the closing hours of the referendum, pollsters were predicting that the Remain camp would win by up to a nine-point margin. Betting odds said a pro-EU result was almost inevitable.” Whoops!

OH MY!

From NPR:

For the first time in more than a hundred years, younger adults — those aged 18 to 34 — are more likely to be living in their parents’ homes than with a partner or spouse.

CRAZY

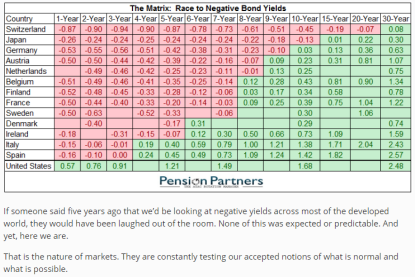

My partner Brett shared this blog from Pension Partners with me.

IF YOU COULD…

…represent the entire population of the world as a village consisting of 100 people, maintaining the proportions of all the people living on Earth, that village would consist of:

57 Asians

21 Europeans

14 Americans (North, Central, and South)

8 Africans

There would be:

52 women and 48 men

30 Caucasians and 70 non-Caucasians

30 Christians and 70 non-Christians

89 heterosexuals

11 homosexuals

6 people would possess 59% of the wealth

80 would live in poverty

70 would be illiterate

50 would be suffering from hunger and malnutrition

1 would own a computer

1 would have a university degree

From my partner John.

LEXOPHILE From my friend Peter: Lexophile is a word used to describe those who have a love for words, especially in phrases and puns such as “You can tune a piano, but you can’t tuna fish!” There is a competition to see who can come up with the best lexophile phrases every year. Here are a few of my favorites; the current winner is at the end.

No matter how much you push the envelope, it’ll still be stationery.

If you don’t pay your exorcist, you can get repossessed.

I’m reading a book about anti-gravity. I just can’t put it down.

I changed my iPod’s name to Titanic. It’s syncing now.

A thief who stole a calendar got twelve months.

When the smog lifts in Los Angeles, U.C.L.A.

A will is a dead giveaway.

A boiled egg is hard to beat.

Police were summoned to a daycare center where a three-year-old was resisting a rest.

He had a photographic memory that was never developed.

Those who get too big for their pants will be totally exposed in the end.

WHAT COMES AFTER ONE BILLION DOLLARS PER DAY?

Americans set an all-time record for charitable donations in 2015. Gifts by individuals, as opposed to corporations or foundations, were the single-largest factor in pushing the total over $373 billion, or more than $1 billion per day. That is great news for charities and the causes they serve, but behind the impressive generosity is a stagnant number: charitable giving by individuals as a percentage of their disposable income has not changed for forty years.

Will this giving rate stay the same forever, or could we give even more? Kim Laughton, President of Schwab Charitable, in her article “Beyond 2%” (Click here to read full article) uncovers a surprising psychological barrier that we all experience when it comes to charitable giving. Kim also reveals how tax-efficient donor-advised funds and other simple strategies could change giving habits and add billions in support of worthy causes.

Full disclosure: I’m a long-time Schwab Charitable client. It’s a great program and definitely worth checking out.

GO FIGURE

On Saturday, July 16, there was an attempted military coup in Turkey, one of the few Muslimmajority democracies and a key asset for the U.S. in the fight against ISIS. One hundred sixtyone civilians were killed and 1,140 were wounded. Naturally, the market reacted on Monday — NOT. Here’s the end-of-the-day headline from Yahoo Finance.

I looked and couldn’t even find a reference to Turkey. Amazing!

FINGERS CROSSED

A recent headline: “FINRA elects Vanguard’s John Brennan chairman to replace Richard Ketchum.” FINRA is the Financial Industry Regulatory Board, an industry self-regulatory organization responsible for supervising and regulating the brokerage industry. Although I’m a tad less skeptical than many of my friends, FINRA is generally perceived by the fiduciary universe as very pro-industry (i.e., not investor sensitive). So, the appointment of the former Vanguard CEO to take over as Chair seems like the hen has been hired to guard the fox house. I don’t understand how it happened, but it sure sounds like good news for investors.

BIGGER MAY BE SMARTER

A number of financial service and insurance organizations have sued the Department of Labor in order to stop the implementation of the DOL Fiduciary Rule. It’s interesting to see some of Wall Street’s biggest firms opposing the anti-DOL lawsuits. Included in those unwilling to go on record as “Brokers who sue the DOL because they don’t want to act in their clients’ best interest” are Bank of America, JP Morgan, Chase, Morgan Stanley, and Wells Fargo. Good for them!

I DON’T THINK SO

Repairing wind turbines looks like a great job opportunity, but it’s not for me!

MACHO I may not want to repair wind turbines, but I can still be macho.

WHO KNEW?

What would you guess is the number of practicing CPAs in the U.S.? I bet you would be way off.

The official count was 664,532 licensees as of April 22, gleaned from NASBA’s national database of CPAs that aggregates data from 51 of the 55 CPA licensing jurisdictions nationwide.

The total does not include data from Delaware, Hawaii, Utah, or Wisconsin.

I’LL CLOSE WITH MORE “I DON’T THINK SO” AND A MORAL

This time I’m referring to Market Timing. I’ve not seen any statistics, but I have little doubt that many investors bailed out of the market when the Brexit vote was completed. Sure enough, in the few days following the vote, the market did indeed take a dip. However, I also doubt many (if any) of those bailing out got back in. We’ve been monitoring the markets subsequent to the vote (6/23/16) and here’s the market reaction through 7/18/16 (less than one month) — and a few days after the attempted coup in Turkey!

iShares S&P 500 (IVV) +3.16%

Market timing doesn’t pay.

I hope you’ve had a great summer. See you again in a few months.

Harold R. Evensky, CFP® , AIF®

Chairman

Evensky & Katz / Foldes Financial Wealth Management

© Evensky & Katz / Foldes Financial Wealth Management

© Evensky & Katz / Foldes Financial Wealth Management