Thoughts on Brexit and the Implications for Investment Strategy

After 43 years of membership in the European Union (EU), Great Britain voted last week to withdraw its membership. In spite of all the polls which leaned toward staying, all the political leaders cajoling voters to remain, and the international pundits from the International Monetary Fund to the President of the United States who lobbied Great Britain to remain in the EU, the British public voted to leave. It appears to us to be a vote for independence and sovereign pride, in spite of the unknown costs.

Let’s begin with some of the more obvious issues. First, this is a total unknown journey so there is no real precedent for the capital markets to lean on. Second, this divorce is going to take a long time. Third, this is going to be massively complicated. Fourth, this is a political event that will have long term ramifications for the capital markets.

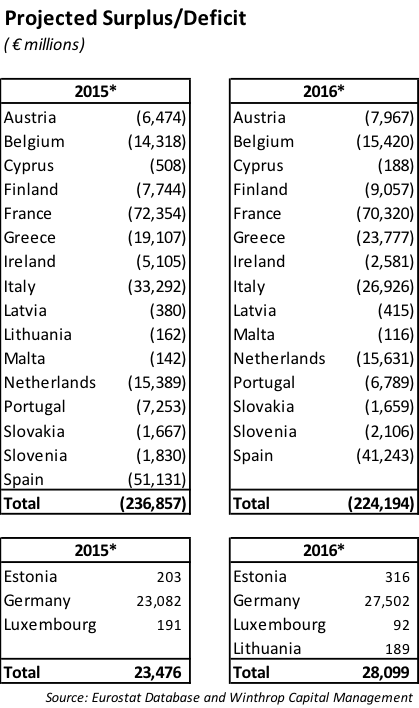

As we review Europe’s economic and political position leading up to this historic vote, we have a few thoughts on the near term implications for investors. Following the Financial Crisis, the European Union has struggled to show it can generate sustained economic growth without its member countries generating large budget deficits and, in turn, funding its deficit through increased debt borrowings. While there has been improvement over the past two years, there are still significant gaps in complying with the Maastricht Treaty. The chart on the right shows the member countries that make up the euro and their expected budget deficits. The result of the cumulative deficits since the Financial Crisis is reflected in over €2.375 trillion in additional debt in the Eurozone.

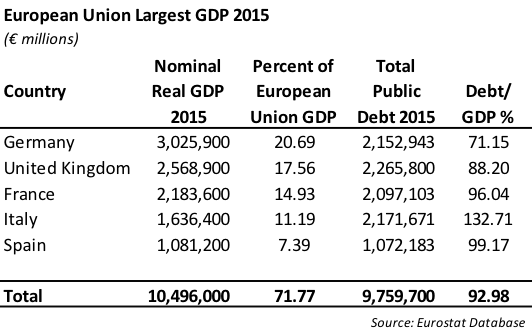

This is a political event which will require political solutions. There is no perfect solution. Rather, like most political solutions, no party involved in this separation will be pleased with the final solution. Simply put, within the EU member countries either pay into the pot or take money out of the pot. Great Britain, which represents 17.5% of the combined GDP of the EU, consistently paid into the pot. Looking ahead, the European Union will have funding gaps that will need to be filled through additional revenue (not likely) with Great Britain leaving.

First, this is not a stimulative initiative for Great Britain nor the EU. To put it in other words, we expect this will be a near term drag on economic growth for both the EU and Great Britain. Britain’s withdrawal from the EU will likely suppress capital investment as companies begin the long process of allocating resources under the uncertainty of current trade agreements. In addition, it may act as a deterrent for employment growth as companies buckle down under the uncertainty caused by Britain’s exit.

Second, as economic growth slows, we expect sovereign debt levels will likely increase relative to GDP for countries in the European Union over the next two years. High levels of debt ultimately inhibit economic growth for a country. However, in order to maintain current spending levels over the next two years during protracted negotiations, the member countries will likely use debt to finance the short fall in budgeted revenues. The combination of slower economic growth and increasing debt will put pressure on credit ratings. The sovereign credit rating of the United Kingdom was cut from AAA to AA by Standard & Poor’s rating service today. We would expect to see ratings downgrades in several member countries over the next two years.

Third, the European banks will be under more pressure if economic growth in the Eurozone stalls. The European banks operate with higher leverage and a less stable deposit base than their U.S. counterparts. Every financial crisis spreads through the banking system and we expect the European banking system will feel pressure under the weight of Great Britain’s decision to leave. Maintaining the credit ratings of the European banks is critical to confidence in the global financial system since they have significant counter party exposure on derivative transactions.

Fourth, any increase in monetary actions from the ECB will have a diminished impact on economic growth. The ECB announced an increased monthly purchase to €80 million per month under the current €1.2 trillion quantitative easing program. Ultimately, the EU needs to address the structural problems that are impeding business formation, private credit expansion and economic growth through structural reforms, not monetary policy initiatives.

Fifth, we expect the Federal Reserve is on hold for the remainder of the year and will have difficulty trying to push rates higher. US Treasury yields will move lower as uncertainty in the capital markets grows and global growth slows. Credit spreads will move wider with heightened volatility.

Sixth, volatility will remain elevated over the near term as both the EU and Great Britain work through the details of the separation. The EU has always had great difficulty building consensus and is known to “dither” and has trouble making the tough decisions that require political will. We have seen many examples of dithering including the development of a prudential bank regulator function and most recently with immigration.

Up until this point, we believed that U.S. domestic equities have been range bound waiting for an improvement in economic conditions and movement from the Federal Reserve to push rates higher. This now changes that view. While domestic earnings should show some improvement for the second half of the year, the head winds from declines in the pound and euro currencies will be more pronounced. We expect volatility will increase and active management strategies will provide better opportunities for return than passive buy-and-hold. We expect credit spreads will widen if volatility increases.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2016 Winthrop Capital Management