Second Quarter 2016 Economic & Capital Market Summary

“It would be so nice if something made sense for a change.”

Lewis Carroll – Alice In Wonderland

Leading up to this past month, the focus of the capital markets was on global economic growth, the weakened condition of the European banking sector and the potential improvement in domestic earnings. The general wait-and-see attitude of the recent initiatives to stimulate economic growth in Japan and Europe combined with signs of improvement in China’s economy helped to provide some stability to equity trading levels. Yet, at the same time investors were trying to digest negative interest rates in Germany, Denmark, Switzerland, Sweden and Japan.

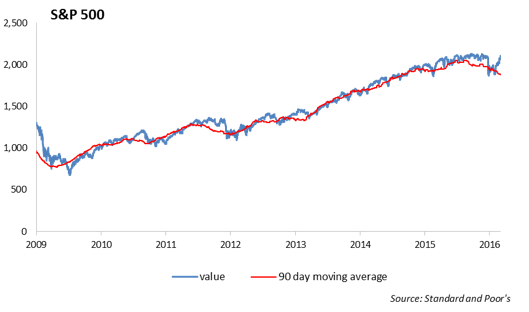

And, then in an instant, things changed. Great Britain voted to leave the European Union. Everyone seemed to indicate that they had prepared for this surprise vote, but no one seemed prepared. After the dust settled and a new Prime Minister was elected, the ten year U.S. Treasury yield hit a record low of 1.39% and the stock market hit a new record high level of 2150 (S&P 500) – at the same time as withdrawals from equity mutual funds have been increasing.

The world seems upside down. In the face of mediocre economic growth and heightened risks in the markets, how can the stock market be hitting record highs and interest rates in the US Treasury markets hitting record lows?

The circumstances of our current investment environment are rooted in the damage caused by the Financial Crisis eight years ago. Since the financial crisis, sovereign countries have incurred more debt to plug budget deficits in order to maintain spending in the hopes of spurring consumption and investment in the hope of jump starting economic growth. The aggressive global central bank policies, which are now focused on incurring more debt in order to buy securities in the open market, are all designed to keep economic growth positive. Ultimately, increased sovereign debt is an impediment to economic growth.

Essentially we are borrowing from future consumption hoping that economic growth will increase enough to normalize the amount of debt incurred. But, the economy is not growing fast enough. Business formation is not taking place at the pace it should, private credit expansion is still slow and wage growth is meager. Inflation-adjusted U.S. median household income has fallen over 7% from its peak in 1999 and food stamp use has more than doubled.

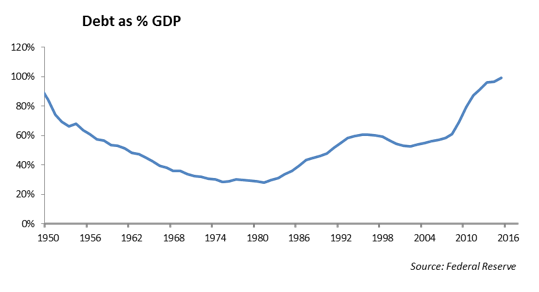

We are near the 100% level of US government debt to GDP which we use as a ratio for the amount of debt issued to support the size of the economy. Our country last reached the 100% debt-to-GDP level following World War II when the U.S. economy was a mere $250 billion in size. Today the economy, measured by GDP approximates $18 trillion. Since World War II, through fiscal initiatives, improvements in productivity, and capital investment our economy experienced healthy growth. Combined with fiscal discipline which helped to control federal debt, significant improvement in the debt/GDP ratio occurred for the two decades following World War II. We do not expect to experience that level of economic growth today.

Fundamental valuations in equities appear over-valued to us even with modest expected improvement in earnings. We are concerned that the near term downside risk for investors is greater than the upside and urge caution going into the second half of the year.

The Economy

The domestic economy showed reasonable growth in the first quarter as GDP nudged higher by 1.1% after several revisions. This is consistent with our thesis that the domestic economy will continue to muddle along in spite of structural problems in the labor and capital markets, the lack of meaningful productivity improvement, recent declines in capacity utilization and the lack of private credit expansion.

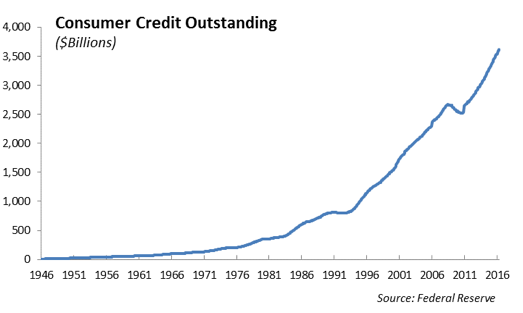

The U.S. consumer is showing signs of strength as consumption, retail sales, and consumer confidence all improved over the past quarter. To support this growth, it appears that the pace of consumer borrowing is also picking up. Consumer credit increased in May at a seasonally adjusted rate of 6.25% according to the Federal Reserve, continuing the growth in credit card, auto loan and student loan balances.

The two critical factors to increased consumer activity are job growth and wage growth. While the May job growth number was weak, June’s was a strong 287,000 nonfarm payroll increase. As monthly job growth trends lower in the second quarter, we are seeing signs of a weaker job market, which will weigh on the economy in the second half of the year.

Elusive wage growth has frustrated many Americans throughout the seven-year economic expansion. There is more progress being made on minimum wage and low level wages. Starbucks and JP Morgan are among companies that recently announced pay increases for low level employees in order to retain valued employees. This validates the recent reading from the Federal Reserve Bank of Atlanta’s wage tracker index, which hit a seven-year high last month.

In stark contrast to historic low levels of interest rates and improved lending from the banks, we believe the credit cycle may be turning negative as the economic expansion hits a later stage. A decline in the credit cycle typically foreshadows a slowdown in the economy.

The recent Fitch default rate study showed an increase in high yield bond defaults to 4.7% in June which was up from 3.8% in April. Bankruptcies in the energy sector have increased as the price of oil dropped to $27 per barrel in February and later has rebounded to $48 per barrel. And, there has been an increase recently in the roll out of hedge funds committed to investing in distressed credit and real estate in the U.S. which is typically a reliable sign of a turn.

The Wall Street Journal recently reported an increase in the number of trucking companies that halted operations in the second quarter. Based on research from Avondale Partners LLC, the reasons for the increase in failures, which removed 2000 trucks from the road, was due to rising fuel prices and weak demand. While this may normalize overcapacity issues in trucking, we take this as one more data point on softening in the domestic economy.

The Dangers of Current Global Monetary Policies

Monetary policy is what the Federal Reserve does to influence the amount of money and credit in the domestic economy. Changes to the amount of money and credit affects the level of interest rates (the cost of credit) and, in turn the performance of the U.S. economy. The way the Federal Reserve’s affects the amount of money has varied through the years. Many remember when the Fed targeted the money supply and monetary aggregates such as M2 and MZM were analyzed weekly for changes. More recently, the Fed targeted the level of the Fed Funds rate which represents the inter-bank lending rate that banks charge one another. On average these various monetary regimes of the Federal Reserve last roughly 30 years.

As the Fed Funds rate was forced to zero after the Financial Crisis, it was a less useful tool to effect change in money and credit. As a result, we have transitioned to a new monetary regime in which the Federal Reserve leverages its balance sheet and purchases securities directly in the open market at target amounts. This quantitative easing is a very powerful tool and has proved effective in forcing interest rates lower across the yield curve.

Current domestic monetary policy is in a holding pattern as the Fed sits on its portfolio of Treasury securities and reinvests cash flows. We do not believe the Fed is going to have the window to push rates higher this year even though they have indicated a desire to do so.

The Central Banks of developed countries around the world are using quantitative easing to force interest rates lower. The result is negative interest rates which is both unprecedented and dangerous. We do not believe that persistent negative interest rates will overcome the structural problems imbedded in the global economies and capital markets in a manner sufficient to stimulate economic growth beyond the country’s current potential growth rate. It is just another way of mortgaging the future of that country by borrowing consumption from future years.

While the United States is not currently experiencing negative interest rates, there is clearly a probability that our Federal Reserve will attempt it if the economy experiences a rapid slowdown. Our financial system is not set up for a negative interest rate scenario and we believe serious damage to the domestic banking and insurance industries will result.

Investment Strategy

U.S. Treasury yields have declined for 35 years reaching the lowest levels in history after the Brexit vote. The result is an average annual rate of return for the U.S. Barclays Aggregate of 8.30%. While we would be one of the first to raise caution about investing in long duration fixed income purely for total return at current interest rate levels, the Barclays U.S. Aggregate index posted a 5.31% return over the first six months of the year! That is a remarkable return when one considers that the yield on the 30 Year U.S. Treasury yield was a mere 3.01% at the beginning of the year.

After surviving the tumult of the first quarter volatility and the meltdown in the energy sector, credit spreads have tightened dramatically during the second quarter. We still like credit sectors; however, are taking the opportunity to harvest some of the spread tightening and move up in quality. We are slightly short durations and will look to shorten further if the economy shows improvement. Our bigger concern is being on the wrong side and exposed to another flight to quality rally in which U.S. Treasury yields decline sharply.

Puerto Rico officially defaulted on its debt at the end of last quarter. This represented a large holding for us; however, our bonds were all insured and matured July 1, 2016 representing a successful exit of our Puerto Rico position. The municipal bond market remains one of the best performing fixed income asset classes. New issue in the municipal bond market is healthy.

With the recent rally after Brexit, we see much of the equity market as fully valued. The consumer staples. Industrial and healthcare sectors all showed strong performance last quarter. Even the safe havens of telecom and utilities have rallied sharply and are up 10% in the closing month of the quarter. As a result, we are moving to reduce volatility from portfolios where possible. We expect earnings in the second half of the year to be mixed but mildly better than the first six months of the year. The head winds of currency should abate, which will be positive for multinationals.

We have been overweight banks, which hurt performance after the Brexit vote and rapid decline in interest rates. While bank earnings will be challenged in this persistently low interest rate environment, we believe there is sufficient progress on reducing problem loans to help free up risk capital which will be a positive for shareholders.

Volatility has declined sharply since the first quarter of 2016. With the decline in volatility and the sharp appreciation in domestic equity valuations and tightening in credit spreads, we are reducing the risk sectors in portfolios. We believe the risks to the downside are disproportionally higher than to the upside and prudence would dictate reducing risk. We don’t see market chaos on the horizon, but that is the point. It is what we don’t see that concerns us given the current valuations.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2016 Winthrop Capital Management