Every financial website displays key barometers to track global stock performance around the world at a glance—in the form of stock indexes. With the development of indexes came new ways to trade the market, including exchange-traded funds (ETFs). Patrick O’Connor, our head of global ETFs, offers this brief history of index investing and the evolution of factor-based investing which has led to today’s strategic beta ETF offerings.

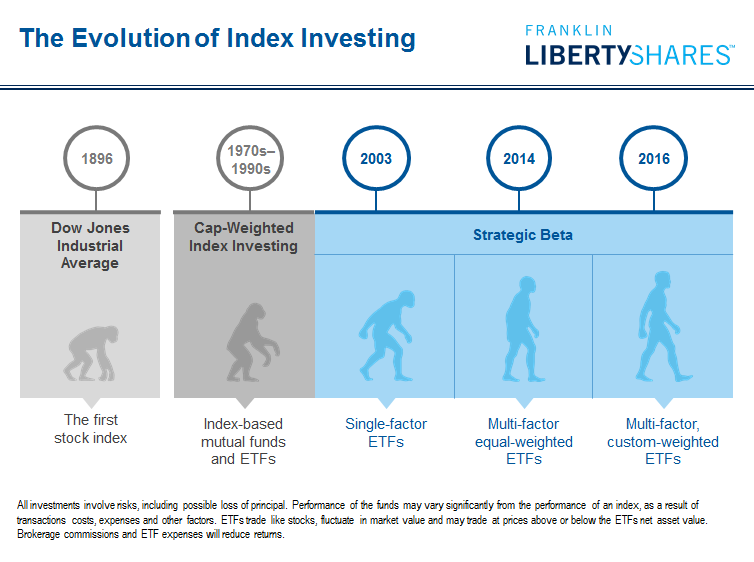

I like to think of the evolution of index investing in Darwinian terms, from the conception of the first stock index to today’s exciting and innovative new products in this space. In 1896, Charles Dow, the editor of the Wall Street Journal and co-founder of Dow Jones & Company, developed the first stock index: the Dow Jones Industrial Average (DJIA). It was more or less a mechanism to track what Charles Dow thought about a basket of hand-picked stocks. Only one company from his original list of 12 remains a DJIA component today with the same name. (Hint: You may own one of its appliances.)

Nearly a century later in the early 1990s, the first exchange-traded funds (ETFs) were introduced in the United States, and today more than $2 trillion in assets are in these vehicles in the United States alone.1

When I first started working in portfolio management in 1999, ETFs were not as ubiquitous as they are today, and it was still very expensive to assemble a basket of stocks as an individual investor. US equities were fairly easy to access, but a basket of international equities or commodities was not. A market-cap weighting offered some benefits; it allowed us to invest in areas we couldn’t get to, but also came with challenges and risks.

ETFs represented the next step in product packaging, but they still tracked a cap-weighted index. However, ETFs did make cap-weighted index investing much more popular, and indexes proliferated. In 2003, factor-based, or strategic beta, investing was first introduced in ETF form. The concept of strategic beta (which some call smart beta) wasn’t actually new; it had been used in institutional portfolios for quite some time. But only in more recent times could retail investors more widely access these types of investing strategies.

The Factor Evolution

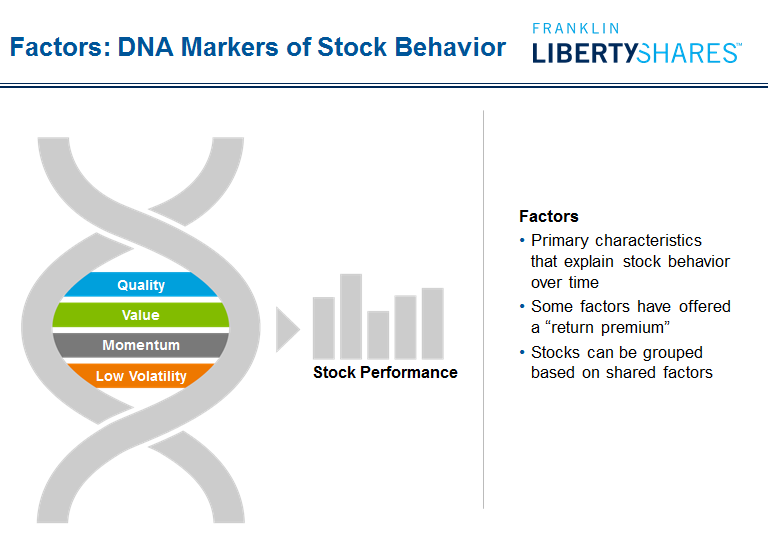

One can think of a factor as a DNA marker of stock behavior; it is a primary characteristic of an investment that explains a stock’s behavior over long periods of time. Just as your DNA determines whether you’ll have blue or brown eyes, factors explain how stocks have tended to move in response to market developments. Our understanding of factors dates back several decades, beginning with Benjamin Graham and David Dodd in the 1930s, who first identified how higher-quality companies tended to perform well, and how stocks with lower price/book and price/earnings ratios2 tended to outperform growth-oriented stocks. Since then, many others have contributed to the understanding of factors.

We have found four factors used to understand stock performance to be the most relevant DNA markers: quality, value, momentum and volatility. Let’s take a closer look at the factors and how we measure them.

(High) Quality: As Graham and Dodd identified, quality is a key driver of stock performance. We think the best measure of company quality seeks to identify those with multiple characteristics, including profitability, strength of balance sheet and efficient use of assets.

(Attractive) Value: By investing in attractively valued stocks, investors seek to benefit from potential upside from low-priced stocks. In measuring value, we think it’s important to identify those with attractive forward and trailing valuation ratios (price/earnings, price/book, price/cash flow) and dividend yield.

(Strong) Momentum: Many investors seek out stocks with strong momentum in order to avoid value traps, viewed as companies that are trading at low multiples but offer little in the way of future potential. We measure momentum by looking for companies that exhibit six- to 12-month relative price strength.

(Low) Volatility: Some investors look to low-volatility stocks to defend against potential market downturns. Stocks that demonstrate lower-than-average variability of returns are often considered “low-volatility” stocks.

Stocks can be grouped based on the primary factors they share. Some factors have provided investors with positive returns above and beyond market indexes over the long term—called a “return premium”—while other factors have been more closely associated with stock risk.

Some investors may be inclined to choose one or two factors for investments, but this approach can also come with ups and downs.

Quality, value, momentum or low-volatility stocks by themselves have moved in and out of favor as the economic cycle has swayed back and forth. Momentum, for example, was the top-performing factor in 2007 when equity markets were strong, but it was the worst performer in 2008 when the global financial crisis hit.3 These swings in performance can be unsettling to many investors, causing them to sell and potentially miss out on rebounding performance.

So let’s consider the options for investing in strategic beta ETFs. You could invest in individual factors, an approach that would offer the opportunity to capture potential risk premiums. Some investors also use them to gain specific factor tilts within a portfolio. But, as mentioned, factors move in and out of favor, and it could be difficult to predict which will be in favor next. And, the ups and downs of individual factor performance could cause investors to sell and miss out on rebounding performance. Finally, buying and selling individual factor investments can increase costs.

Let’s look at another possibility. An investor could invest in a multi-factor portfolio that’s diversified equally across all factors, an approach with some potential advantages:

- It could be used as a core holding, with diversification across factors

- There’s no need to attempt to time factors

- It can offer lower transaction costs

However, this approach doesn’t consider the relative importance of each factor in driving long-term stock performance.

Now let’s look at a third option. A multi-factor, strategically weighted portfolio offers several attributes:

- It considers the role of each factor in driving long-term investment returns

- It allows a manager to target portfolio exposures

- Strategic diversification may provide an attractive core holding

The first strategic beta ETFs tracked single-factor indexes. These portfolios were useful as far as they went, but they didn’t offer the diversification that many investors are seeking today. Then about two years ago, the first equal-weighted multi-factor ETFs were introduced. These portfolios offered factor diversification, but didn’t take into account the relative importance of individual factors. The newest breed of multi-factor strategic beta ETFs weight factors strategically in order to seek better investment outcomes than equal-weighted multi-factor ETFs. We think these ETFs represent an important step in the evolution of strategic beta investing.

At Franklin Templeton, we believe factor weightings should be rooted in economic rationale, best represented by quality and value. Exposure to momentum may help identify investment trends and avoid value traps, while exposure to volatility may help provide defense against market downturns.

While there is certainly more to explore, we think this is an interesting time in the ETF space and that strategic beta solutions will likely continue to grow and evolve.

Patrick O’Connor’s comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

What Are the Risks?

All investments involve risks, including possible loss of principal. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments; investments in emerging markets involve heightened risks related to the same factors. To the extent the funds focus on particular countries, regions, industries, sectors or types of investment from time to time, they may be subject to greater risks of adverse developments in such areas of focus than funds that invests in a wider variety of countries, regions, industries, sectors or investments. Performance of the funds may vary significantly from the performance of an index, as a result of transactions costs, expenses and other factors. The funds’ risk considerations are discussed in the prospectus. ETFs trade like stocks, fluctuate in market value and may trade at prices above or below the ETFs’ net asset value. Brokerage commissions and ETF expenses will reduce returns.

To obtain a summary prospectus and/or prospectus, which contains this and other information, talk to your financial advisor or visit libertyshares.com. Please carefully read a prospectus before you invest or send money.

___________________________________________

1 Source: Investment Company Institute, as of May 2016.

2 The price-to-earnings ratio, or P/E ratio, is an equity valuation multiple defined as market price per share divided by annual earnings per share. For an index, the P/E ratio is the weighted average of the P/E ratios of all the stocks in the index. For an individual company, the price-to-book (P/B) ratio is the current share price divided by a company’s book value (or net worth) per share. For an index, the P/B ratio is the weighted average of the price/book ratios of all the stocks in the index.

3 Quality is represented by the MSCI ACWI Quality Index; Value is represented by the MSCI ACWI Value Index; Momentum is represented by the MSCI ACWI Momentum Index; Minimum Volatility is represented by the MSCI ACWI Minimum Volatility Index. Indexes are unmanaged, and one cannot invest directly in an index. They do not reflect any fees, expenses or sales charges. Past performance is not an indicator or a guarantee of future performance. Index returns reflect reinvestment of dividends and are adjusted for withholding taxes. See www.franklintempletondatasources.com for additional data provider information.

© Franklin Templeton Investments

© Franklin Templeton Investments