Weighing the Week Ahead: What Might Derail the Stock Market Rally?

This week’s calendar includes a light schedule for data with an emphasis on housing. Earnings season is in full swing with important reports every day. The early reception has been surprisingly good, creating plenty of mystified pundits. The financial media will be asking: What Can Derail the Rally in Stocks?

Last Week

The economic news was excellent, and the market reaction was strong. The continuing market rebound has caught many off base. This week’s review is mostly positive on economic data.

Theme Recap

In my last WTWA, I predicted that the post-Brexit rally now depended on earnings, especially management discussions of outlook. I noted that there were a record number of appearances by Fed participants as well as the release of the Beige Book, but felt that would be much less important. This proved to be a very accurate guess. In particular, the reception to some key earnings reports was quite strong. CNBC had a couple of short pieces on the FedSpeak, basically proving the expected lack of fresh news.

I hope readers have stayed with the rally during the post-Brexit move. It is important to know what to watch.

The Story in One Chart

I always start my personal review of the week by looking at this great chart from Doug Short. You can clearly see the two big rally days and the quiet Friday. Doug has a special knack for pulling together all of the relevant information. His charts save more than a thousand words! Read his entire post where he adds analysis and several other charts providing long-term perspective.

The News

Each week I break down events into good and bad. Often there is an “ugly” and on rare occasion something really good. My working definition of “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

The Good

- Rail traffic is shows continuing improvement. Steven Hansen helpfully covers the weekly data and various comparisons. Part of the improvement relates to comparisons to weaker 2015 data, so it is not all good news.

- High frequency indicators have turned better – nearly all of them. New Deal Democrat’s weekly update is very helpful for those wanting a comprehensive survey.

- The Labor Market Conditions Index (recently weak) has improved. “Fred” has the data.

- Wholesale sales improved so I am scoring it as a positive. Steven Hansen goes beyond the seasonally adjusted data, noting that sales are still at “levels associated with recessions’ and there is “degradation in the 3 month averages.”

- Industrial production rose 0.6%, beating expectations of a 0.2% gain. This is a nice rebound in an important sector.

- Initial unemployment claims handily beat expectations at 254K. The extremely low level of new jobless claims continues.

- Retail sales soundly beat expectations with a gain of 0.6% versus 0.2% expected. Ex-auto the results were even better. This was reassuring to those worried about the consumer. (Calculated Risk).

The Bad

- JOLT’s showed a decline in job openings but the important voluntary quit rate was the same. Many observes mistakenly try to use this report to coax out stories about net job growth. That is not the point of this research. It is both slower and less accurate than the regular payroll report. It is much more important for labor market tightness and structure.

- Congress is leaving on recess. Normally I list this under “good news” but this time there are quite a few issues that were not addressed. After the political conventions the return will be brief. Our legislators naturally need to get back to the campaign trail! Maybe it is time to consider a more efficient way of changing leadership. The Hill has the story about work left undone.

- Michigan sentiment declined and missed expectations. The experts at Michigan noted concern about Brexit among the high-income respondents. (Steven Goldstein at MarketWatch). This will be interesting to watch. As usual, Doug Short has the best chartsummarizing the series.

The Ugly

This week our hearts go out to the French. I am really hoping for a week without ugliness.

The Silver Bullet

I occasionally give the Silver Bullet award to someone who takes up an unpopular or thankless cause, doing the real work to demonstrate the facts. No award this week. Nominations are always welcome. There is plenty of misinformation to refute!

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react. That is the purpose of considering possible themes for the week ahead. You can make your own predictions in the comments.

The Calendar

We have a rather light week for economic data, with an emphasis on housing news. While I watch everything, I highlight only the most important items in WTWA. It is important to focus.

The “A” List

- Housing starts and building permits (T). An important sector, but a modest decline is expected in starts. I am more interested in permits.

- Leading indicators (Th). A rebound expected in a series widely followed as a recession signal.

- Initial claims (Th). The best concurrent indicator for employment trends.

The “B” List

- Existing home sales (Th). Less important for the economy than new construction, but a good read on the overall market.

- Philly Fed (Th). Attracting more information as the earliest data with a label from the prior month.

- Crude inventories (W). Often has a significant impact on oil markets, a focal point for traders of everything.

The big story will still be corporate earnings, as reporting season moves into full swing. The Republican Convention will grab plenty of news. FedSpeak will die down after last week’s thirteen appearances.

And of course, we can expect more updates on international crises.

Next Week’s Theme

Markets seem to have digested the Brexit story, and surprisingly shrugged off the terrorist violence. The economic data have quieted recession worries. The post-holiday FedSpeak was not threatening. Early earnings reports were OK, but not great.

So why is the stock market reaction so positive? The punditry is already hard at work on this question. I expect the discussion to continue. The market reaction is clearly at odds with what many call “the fundamentals.” If markets keep going higher, the questions will increase. If stocks pull back, we can expect a parade of pundits explaining why.

Either way, everyone will be asking:

What can derail the rally in stocks?

Feel free to join the discussion in the comments, but I see several worry themes:

- Terrorism. The world is a nasty place and seems to be getting worse.

-

Economic concerns.

- Deflation – signaled by falling commodity prices, especially cheap oil. Or alternatively–

- Inflation – signaled by rising commodity prices, especially higher oil prices.

-

Politics.

- Trump would be a disaster for the U.S. and world economies.

- Clinton would be a disaster for the U.S. and world economies.

- Uncertainty. Not knowing who will be elected is a disaster for the U.S. and world economies.

- Central banks. They painted themselves into a curve, merely delaying the inevitable economic disaster. (I actually heard one of the Fast Money guys use one of mixed metaphors about the Fed. Maybe it was an accident, but he certainly didn’t cite the OldProf!)

- Market valuation. Markets are too expensive. All of them. Investors cannot expect any reasonable return over the next twelve years (except gold, of course).

-

Technical indicators.

- Stocks were declining – lacking leadership.

- Stocks are now overbought and frothy.

- Stocks are stuck in a trading range.

- There was a Hindenburg omen – when was that?

- Weak and mistaken leadership worldwide.

- Delayed Brexit effects.

- Global hot spots – South China Sea, Korea

Quant Corner

We follow some regular great sources and also the best insights from each week.

Risk Analysis

Whether you are a trader or an investor, you need to understand risk. Risk first, rewards second. I monitor many quantitative reports and highlight the best methods in this weekly update.

The Indicator Snapshot

The Featured Sources:

Brian Gilmartin: Analysis of expected earnings for the overall market as well as coverage of many individual companies. This week heexpresses more confidence about growth in earnings.

Bob Dieli: The “C Score” which is a weekly estimate of his Enhanced Aggregate Spread (the most accurate real-time recession forecasting method over the last few decades). His subscribers get Monthly reports including both an economic overview of the economy and employment.

The recession odds (in nine months) have nudged closer to 10%. This does not completely reflect Brexit effects, so we may get a further revision.

Holmes: Our cautious and clever watchdog, who sniffs out opportunity like a great detective, but emphasizes guarding assets.

Doug Short: The Big Four Update, the World Markets Weekend Update (and much more).

The ECRI has been dropped from our weekly update. It was not so much because of the bad call in 2011, but the stubborn adherence to this position despite plenty of evidence to the contrary. Those interested can still follow them via Doug Short and Jill Mislinski. The ECRI commentary remains relentlessly bearish despite the upturn in their own index.

RecessionAlert: Many strong quantitative indicators for both economic and market analysis. While we feature his recession analysis, Dwaine also has a number of interesting approaches to asset allocation.

Georg Vrba: The Business Cycle Indicator, and much more. Check out his site for an array of interesting methods. His latest updatedescribes the elements of the indicator we cite every week.

How to Use WTWA

In this series I share my preparation for the coming week. I write each post as if I were speaking directly to one of my clients. For most readers, they can just “listen in.” If you are unhappy with your current investment approach, we will be happy to talk with you. I start with a specific assessment of your personal situation. There is no rush. Each client is different, so I have six different programs ranging from very conservative bond ladders to very aggressive trading programs. A key question:

Are you preserving wealth, or like most of us, do you need to create more wealth?

My objective is to help all readers, so I provide a number of free resources. Just write to info at newarc dot com. We will send whatever you request. We never share your email address with others, and send only what you seek. (Like you, we hate spam!) Free reports include the following:

- Understanding Risk – what we all should know.

- Income investing – better yield than the standard dividend portfolio, and also less risk.

- Holmes – the top artificial intelligence techniques in action.

- Why 2016 could be the Year for Value Stocks – finding cheap stocks based on long-term earnings.

You can also check out my website for Tips for Individual Investors, and a discussion of the biggest market fears. (I welcome questions or suggestions for new topics.)

Best Advice for the Week Ahead

The right move often depends on your time horizon. Are you a trader or an investor?

Insight for Traders

We consider both our models and also the best advice from sources we follow.

Felix and Holmes

We continue our neutral market forecast. Felix is once again fully invested, including some more aggressive sectors. That continues to work well during the rally. The more cautious Holmes is still fully invested, in a diverse group of 16 stocks from a universe of nearly 1000, selected mostly by liquidity. Sometimes we have had only 14 or 15 stocks. That is revealing. Even when the overall market is neutral, there will often be some strong candidates. That is what we see now. It is not a resounding endorsement of the overall market, but a vote for opportunistic trading. I am curious about what it will take for Holmes to turn “mildly bullish.”

Top Trading Advice

Who is participating in the current market? How and at what levels? Know the background before trading! (Brett Steenbarger).

When you have met your “goal” for a session or a time period, do you stop trading? There is a great discussion at daily speculations. I have a strong opinion on this one, but I am interested in your comments.

Do you use Twitter in your trading? Finding other opinions? Breaking news? Here are some ideas.

Why a systematic daily approach is important to your trading. Holmes was barking appreciatively at the ideas from Pradeep Bonde, especially the unemotional focus on setups and execution. (Easy for him to say!)

Insight for Investors

Investors have a longer time horizon. The best moves frequently involve taking advantage of trading volatility!

Best of the Week

If I had to pick a single most important source for investors to read this week it would be Aaron Task’s 3 Reasons the Stock Market Is Rising Even As the World Feels Like It’s Falling Apart. Here is a key quotation:

The World Isn’t Ending: While there’s plenty to worry about—including global terrorism, uncertainty over what Brexit really means, anxiety over how U.S. election plays out, and much more—the global economy is expanding, albeit slowly, and the U.S. looks pretty good relative to other developed economies. (Insert “best looking horse in the glue factory” joke here.) And despite legitimate concerns about anti-globalization forces being on the rise here and abroad, the volume of global trade is expected to rise 2.6% this year after climbing 2.8% in 2015.

An old Wall Street saying also helps explain why stocks have fared well despite all the negative headlines: The market climbs a wall of worry.

You should be more worried about the stock market when “everyone” is bullish and the conventional wisdom says buying stocks (or real estate or any other asset) is a “no brainer.” That is certainly not the case today: UBS says wealthy investors are holding on to record levels of cash and 84% believe the election will have a significant impact on their financial health, Reuters reports.

The entire article acknowledges some current concerns, but brings the story back to data.

Stock Ideas

Chuck Carnevale remains cautious, even including top dividend candidates. Anyone seriously interested in finding great stocks should be following his series closely. It provides suggestions, but also the underlying reasoning and data.

Barron’s has a cover story on Royal Dutch Shell. The analysis covers dividends, cost-cutting, and oil prices. Even if you do not agree with the conclusion, this is an interesting approach.

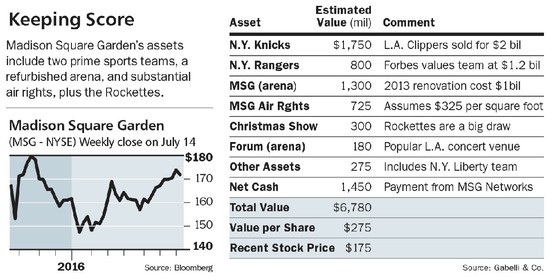

Barron’s also cites Madison Square Garden as almost 60% undervalued on a sum-of-the parts analysis of trophy properties. Once again, this combines an interesting pick with a useful method of analysis.

Market Overview and Outlook

Traders see a conspiracy to keep the market higher. (Art Cashin). I believe that Art is accurately conveying a widespread sentiment.

The Fear and Greed Trader has a nice overall market summary, providing a refreshing balance to the normal daily news. It is a comprehensive summary and well worth reading in its entirety, but here is a key quotation:

The new highs are being dismissed for one reason or another. Maybe those that are saying that are on to something. I prefer that investors, do some research, draw a conclusion, and exhort all to run far away from the rhetoric that has been wrong now for months and years.

I don’t know where the S&P can trade to now with any certainty as momentum is hard to quantify. What I do know is that the entire market dynamic has now changed given this breakout.

Eddy Elfenbein is musing about Dow 20,000, which he thinks might happen this year.

I agree that this is a good time to buy or own stocks, even for those who have missed out so far. Please check out my own recent updateon the market potential and how to find the best stocks and sectors.

Personal Finance

Professional investors and traders have been making Abnormal Returns a daily stop for over ten years. The average investor should make time (even if not able to read AR every day as I do) for a weekly trip on Wednesday. Tadas always has first-rate links for investors in hisweekly special edition. There are several great choices worth reading, but my favorite is the simple and accurate message from Carl Richards:

When I first start working with clients, there’s a period of time I refer to as the financial pornography detox. It’s when you’ll get calls from clients wanting to know what they should do based on what some talking head said or some headline they read. Your job as a real financial advisor is to help them detox from this nonsense and understand they don’t need to do pay any attention to this so-called investment news.

Check the full post for the helpful illustration and the full podcast.

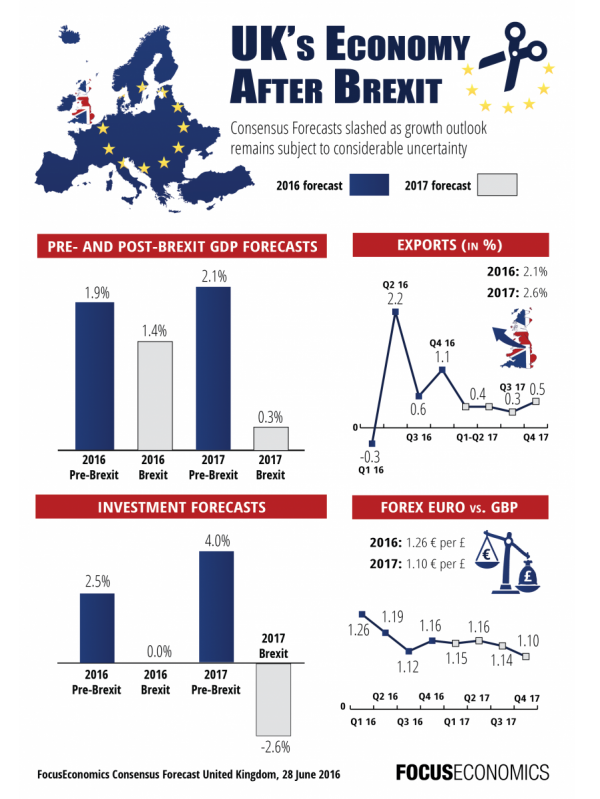

Brexit News

There is continuing interest about implications beyond the immediate effects. I follow these developments in three different ways.

- Fundamental economics. Focus Economics has an excellent update on expectations for the UK as well as implications for other countries. (See also).

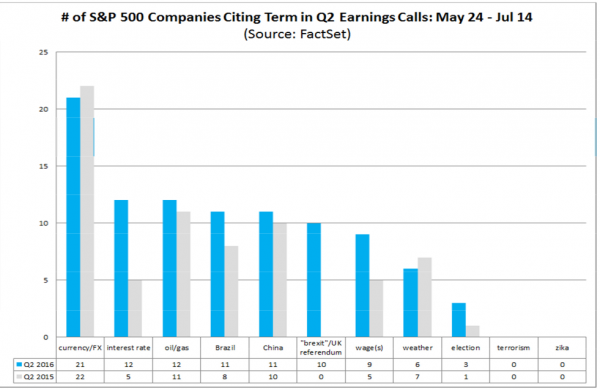

- Earnings data. We know the outlook is important. What sort of factors are coming up in the conference calls? FactSet offers this distribution:

- Extra “color” from the earnings calls. Avondale does a great job with this. I found the JP Morgan comments on loan demand and spending to be especially interesting.

Value Stocks

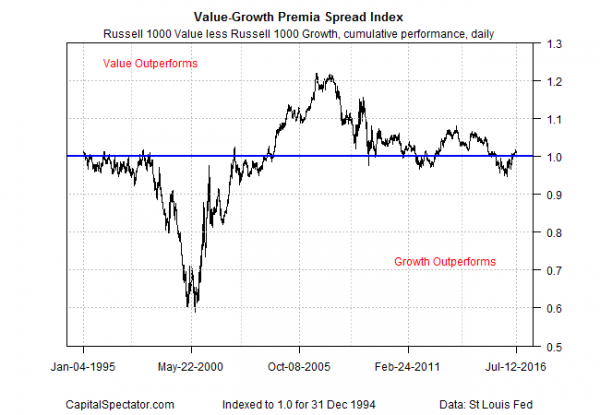

Value strategies have lagged for the last few years. This year the trend seems to be shifting. (The Capital Spectator).

Watch out for….

Any story mentioning the “aging bull.” This popular theme has been taken up by some of the best sources – probably because it resonates with the instincts of the average reader. It is now competing with “self-taught in Austrian economics” as the most dangerous phrase in the investment lexicon. I will omit citing the multiple references last week, but do not be convinced. There is no relationship between the length of a bull market and the expected number of years remaining.

Even bond king Gundlach warns about the current risk in bonds, with the setup in the ten-year Treasury the “worst in his career.”

Final Thoughts

The simple reason for the market rally? Many stocks were priced as if we were already in a recession. As the economic data refuted this notion, prices partially normalized. There is plenty of remaining room, especially in economically sensitive sectors.

Of course there is plenty to worry about. Everyone should be aware of national and world problems, and try to act constructively. Compassion toward those suffering is in the nature of most people, regardless of their values or religious background.

When you think about investments, the problem is sharply different. It is expected and even desirable that the world is filled with problems. The challenge is to understand which problems are actually meaningful for your investments.

One way to keep your eye on the ball (since it is baseball season) is to evaluate the impact of any events on corporate earnings. Look at overall earnings, sectors, and stocks. Be specific. Do not use any lightweight arguments like “the first domino” or “if you see one cockroach.” Brian Gilmartin’s work is a great source for regular updates on earnings trends, combined with his insights. His latest postnotes the reversal in both earnings and revenue, a turning point that he accurately predicted.

If your disciplined investigation cannot determine a link to profits, the news may still be very bad — but not for your investments. Embrace times when everyone else seems to have emotional worries.

Afterword – Worries Circa 2010

From one of my key posts in 2010. Please look at the reasons why so many were depressed about the market six years ago. You probably do not even remember some of them, but they were prominent at the time.

Here is a list of worries that I have noted, in no particular order:

- ETF liquidation doomsday scenario

- Flash crash — and overall worries about market manipulation

- Bush-era tax cut expiration

- Collapse of the euro and/or European Union

- The Hindenburg Omen

- Increase in US budget deficits

- Ominous head-and-shoulders pattern in market averages

- Dow 5000

- Dow 2000

- Dow 1000

- The collapse of the US consumer

- The double-dip recession

- Sell in May

- Sell in October

- Sell, Mortimer, Sell (OK, I sneaked that one in for those who know).

- The BP spill

- Fear of Obama

- Obamacare

- Weakness in the dollar

- Strength in the dollar

- Weakness in China’s economy

- Strength in China, leading to higher rates

- Korea

- Iran

- Initial claims spiking to over 500K

- Initial claims falling, but results skewed by seasonality

- Shadow housing inventory

- Foreclosure robo signing

- Overstated and exaggerated corporate earnings

- Fed blunders — QE II

- High frequency trading

- Worldwide collapse and deflation

- Worldwide hyperinflation

The single most important thing for the investor to understand — right now — is the value of worries. If you are looking for good investment returns, you need a time when others are worried.

The concept of the “wall of worry” is difficult for the average investor. They seem to think it is bad when there are many worries. In fact, the lack of worry is a sign of a market top. Let me simplify.

Here is the image of the market top: “What? Me Worry?”