Real Estate’s Elevated Sector Status Could Be a Catalyst for Equity REITs

2016 figures to be a momentous year for the real estate investment trust (REIT) industry, which will soon become a class unto itself. Literally. But first, a little background.

In 1999, MSCI Inc. and S&P Dow Jones Indices established the Global Industry Classification Standard (GICS) — a hierarchical industry classification system consisting of 10 sectors, 67 industries and 156 sub-industries. Currently, REITs are classified as a sub-industry of the real estate industry, which, in turn, falls under the financials sector.

That is about to change.

Real estate will soon be a GICS sector

Beginning after market close on Aug. 31, 2016, real estate will get a much-anticipated promotion to global sector status — the first such addition since the establishment of GICS. As part of this move, REITs will be divided into two categories:

- Mortgage REITs, which purchase or originate mortgages and tend to be sensitive to interest rates, will remain a sub-industry of the financials sector.

- All other REITs will be classified as equity REITs, which will form a separate industry under the real estate sector. Equity REITs are companies that own and invest in properties that produce cash flow streams from rents.

Classification change underscores real estate’s unique characteristics

While it is impossible to know the ultimate effects of this landmark change, there could be many potential benefits. We at Invesco Real Estate believe the new, dedicated real estate sector will showcase fundamental differences between real estate and other businesses, and make it easier to see how investment managers are allocated to this area.

Segregating real estate into a class by itself highlights the sector’s potential diversification benefits, yield potential and historical total returns. This change may also shine a light on diversified managers who have been underweight real estate stocks for years.

GICS change could have ramifications for portfolio managers

Index providers have suggested that differentiating real estate into its own sector “reflects the position of real estate as a distinct asset class and a foundational building block of a modern portfolio” and may serve to increase the visibility of the sector to generalist investors.1

We believe there is also potential for a reduction in long-term volatility, as the independent classification may help to decouple real estate from other financials, like banks and insurance companies, and increase real estate’s investor base. This is because GICS is accepted as the primary framework for investment research, portfolio management and asset allocation. As such, it has helped to drive product development — including the rapidly growing exchange-traded-fund market.

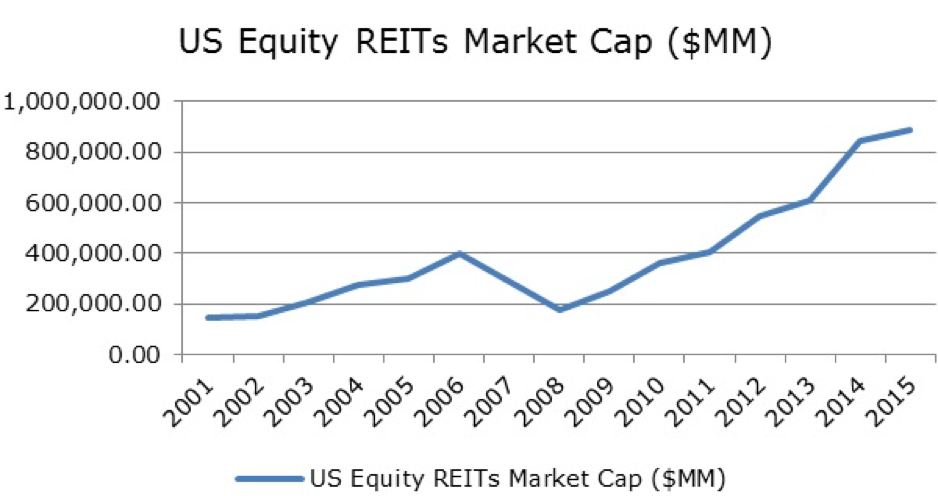

Market cap of equity REITS has grown more than sixfold

REIT Magazine notes that the GICS change is “reminiscent of the decision in 2001 to include

REITs in the S&P Indexes.”2 Following that decision, the market capitalization of US equity

REITs ballooned from $147 billion to $886 billion from 2001 through 2015.3

Source: NAREIT, as of May 31, 2016

Source: NAREIT, as of May 31, 2016

We at Invesco Real Estate applaud the GICS changes as a potential catalyst for equity REITs, and believe real estate as a whole will benefit from its elevated status as the 11th global sector. We look forward to the continued adoption of REITs by both institutional and individual investors alike.

1 MSCI Inc., Dow Jones Indices, March 8, 2016

2 REIT.com, May 24, 2016

3 National Association of Real Estate Investment Trusts, May 31, 2016

Important information

Real estate companies, including REITs or similar structures, tend to be small; mid-cap companies and their shares may be more volatile and less liquid.

The Global Industry Classification Standard was developed by and is the exclusive property and a service mark of MSCI Inc. and Standard & Poor’s.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers, including Invesco Distributors, Inc. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC (Invesco PowerShares). Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.

©2016 Invesco Ltd. All rights reserved.

Real estate’s elevated sector status could be a catalyst for equity REITs by Invesco