Investors May Need to Lower Return Expectations in Wake of Brexit

SUMMARY

- Brexit shockwaves added a layer of political and economic uncertainty, but fundamental impacts are likely to take time before they become apparent.

- Even just before Brexit, both the U.S. Federal Reserve and the market had ratcheted down expectations for rate hikes.

- Investors may have to recalibrate expectations – the lower returns that many asset classes experienced in the past couple of years could persist.

The historic Brexit vote on June 23 sent shockwaves through the capital markets and sparked a global flight to quality in fixed-income sectors, as investors reacted to new political and economic uncertainty.

Substantive, fundamental impacts on trade and economic growth are likely to take time before they become apparent. In the meantime, investors will likely have an elevated perception of risk and we believe central banks will react accordingly. Following what is now a well-known script, central banks are likely to respond with renewed measures aimed at keeping financial markets on “Novocain.”

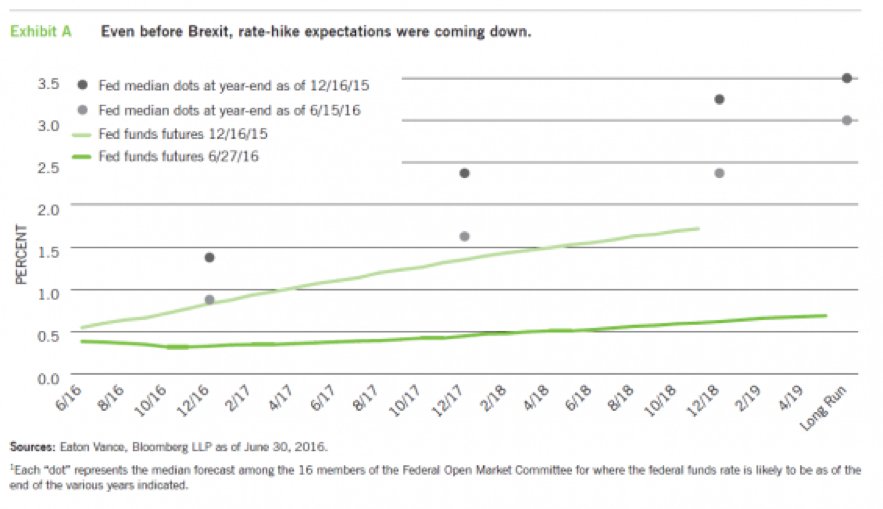

Reduced rate-hike forecasts

Just one month before Brexit, both the market and comments by U.S. Federal Reserve Chair Yellen pointed to a rate hike by July 2016. Following the announcement of a weak U.S. payrolls number in May, the market lowered its rate-hike expectations and Yellen softened her previous more-hawkish tone. Moreover, over the past few years, the market has consistently been more skeptical than the Fed about the prospect for rate increases. Exhibit A shows that the Fed’s “dot” forecast 1 for fed funds as of December 2017 dropped from 2.4% at December 2015 to 1.6% at June 2016. The market’s expectations, as indicated by fed funds futures, fell from 1.4% to 0.45% over the same time frame.

The Fed took its first step toward tightening in December 2015, but that now appears to be on hold. Post Brexit, there is little reason to believe that monetary policy in Europe won’t continue to be in a highly accommodative mode, pushing some sovereign yields further into negative territory. Many have questioned the effectiveness of unconventional monetary policy measures pursued by the world’s major central banks, due to their apparent limited impact in spurring economic growth. However, there is little doubt such measures have caused risk assets to rally. For example, in the U.S., actions by the Fed can take much credit for double-digit increases in both the U.S. stock and high-yield bond markets. From January 1, 2009 through December 31, 2014, the S&P 500 had an average annual total return of 17.2% and high-yield bonds, 16.0%, based on the Barclays U.S. Corporate High Yield Index.

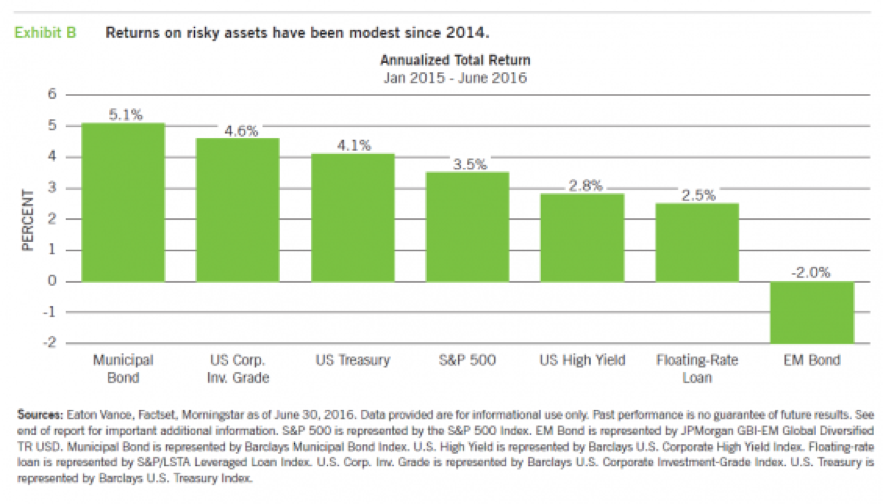

However, over the past couple of years, the continuing dovish stance by central banks has had less impact on financial asset prices and returns. In the past two years returns on risky assets fell, weighed down by concerns over faltering growth, credit quality and lack of value (Exhibit B). For example, from January 1, 2015 through June 30, 2016, the S&P’s average annual total return was 3.5%, and high-yield bonds, 2.7%.

That said, the returns shown in Exhibit B are a cautionary sign that investors may have to recalibrate their expectations in a continuing world of central bank-dispensed Novocain that continues to fall short of stimulating real economic growth. (Fiscal stimulus would help, but achieving political consensus in this regard is a major hurdle.) Also, to the extent Brexit empowers similar anti-globalization sentiment within European countries, or even in the U.S., price volatility is likely to remain the norm.

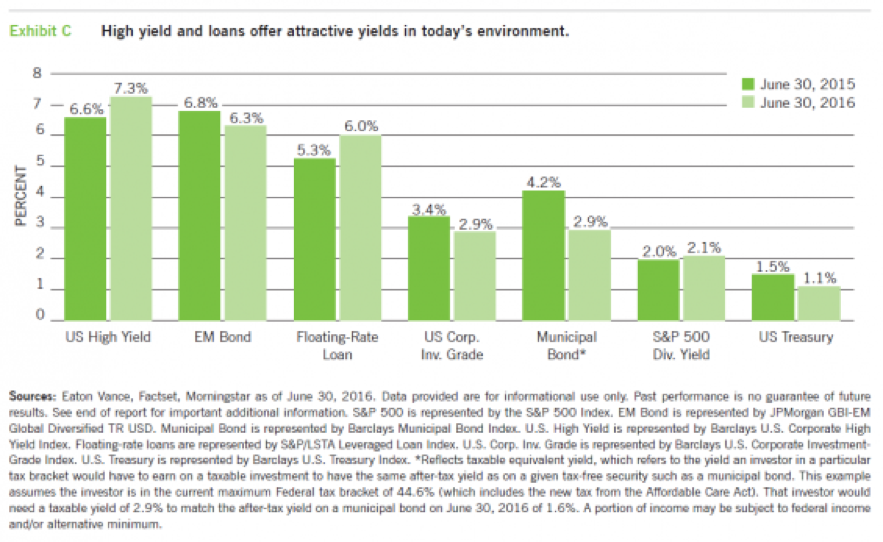

At the start of the year, we viewed investment sectors like U.S. high-yield bonds and floating-rate loans as extremely inexpensive based on historical and relative valuations. Those valuations attracted investors who bid up their prices and they are now closer to fairly valued, in our view. However, as Exhibit C shows, high-yield bonds and loans remain among the highest-yielding sectors; and unlike other fixed-income sectors, their yields are higher than a year ago.

Bracing for volatility

We do not believe the U.S. economy is headed for recession in the near term, but the fits and starts to growth are unlikely to go away. For example, three months ago, there was talk of a strengthening labor market and weak economic growth, but that has flipped. Recently we’ve experienced stronger economic growth and a weaker labor market. Moreover, we won’t know the real potential impact of Brexit for years. Questions following the referendum are many, but a few that come into focus are:

- What will the ultimate trade terms be between the EU and the U.K. The EU has an incentive to make them harsh, lest it encourages other countries to take the same path.

- How will other EU countries react, in light of growing public sentiment against staying in the EU? Will other countries hold similar referenda? Elections in France and Germany will be held next year.

- Will this lead to a greater divergence between U.S. and European economies?

Post-Brexit opportunities

For investors, we believe the most important consideration is to avoid hasty action driven by fear, without being complacent. We’ve already witnessed a significant recovery in the U.K., European and U.S. stock markets. Yet we have not seen a comparable recovery in the bellwether 10-year U.S. Treasury bond yield – it has stayed near its Brexit low. The bond market may be telegraphing that more price volatility lurks ahead.

In a low-growth, low-expected-return environment that is supported by central banks, we believe below-investment-grade U.S. corporate credit – high-yield bonds and floating-rate loans – offers a compelling risk/return proposition. (We believe their high coupons should more than offset possible credit losses). Any sharp sell-off in these sectors – or in specific securities that are insulated from the direct impact of Brexit – could present even more attractive buying opportunities.

Index definitions

Barclays U.S. Corporate High Yield Index measures USD-denominated, noninvestment-grade corporate securities.

Barclays U.S. Corporate Investment Grade Index is an unmanaged index that measures the performance of investment-grade corporate securities within the Barclays U.S. Aggregate Index.

Barclays U.S. Treasury Index measures public debt instruments issued by the U.S. Treasury.

JPMorgan Government Bond Index-Emerging Markets (GBI-EM) Global Diversified is an unmanaged index of local-currency bonds with maturities of more than one year issued by emerging market governments.

S&P/LSTA Leveraged Loan Index is an unmanaged index of the institutional leveraged loan market.

Barclays Municipal Bond Index is an unmanaged index of municipal bonds traded in the U.S.

Standard & Poor’s 500 Index is an unmanaged index of large-cap stocks commonly used as a measure of U.S. stock market performance.

Unless otherwise stated, index returns do not reflect the effect of any applicable sales charges, commissions, expenses, taxes or leverage, as applicable. It is not possible to invest directly in an index. Historical performance of the index illustrates market trends and does not represent the past or future performance.

About Risk

An imbalance in supply and demand in the income market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. Investments in income securities may be affected by changes in the creditworthiness of the issuer and are subject to the risk of nonpayment of principal and interest. The value of income securities also may decline because of real or perceived concerns about the issuer’s ability to make principal and interest payments. As interest rates rise, the value of certain income investments is likely to decline. An imbalance in supply and demand in the municipal market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. There generally is limited public information about municipal issuers. As interest rates rise, the value of certain income investments is likely to decline. Investments involving higher risk do not necessarily mean higher return potential. Diversification cannot ensure a profit or eliminate the risk of loss. Elements of this commentary include comparisons of different asset classes, each of which has distinct risk and return characteristics. Every investment carries risk, and principal values and performance will fluctuate with all asset classes shown, sometimes substantially. Asset classes shown are not insured by the FDIC and are not deposits or other obligations of, or guaranteed by, any depository institution. All asset classes shown are subject to risks, including possible loss of principal invested. The principal risks involved with investing in the asset classes shown are interest-rate risk, credit risk and liquidity risk, with each asset class shown offering a distinct combination of these risks. Generally, considered along a spectrum of risk and return potential, U.S. Treasury securities (which are guaranteed as to the payment of principal and interest by the U.S. government) offer lower credit risk, higher levels of liquidity, higher interest-rate risk and lower return potential, whereas asset classes such as high-yield corporate bonds and emerging-market bonds offer higher credit risk, lower levels of liquidity, lower interest-rate risk and higher return potential. Other asset classes shown, such as municipal and investment-grade bonds, carry different levels of each of these risk and return characteristics, and as a result generally fall varying degrees along the risk/return spectrum.

Costs and expenses associated with investing in asset classes shown will vary, sometimes substantially, depending upon specific investment vehicles chosen. No investment in the asset classes shown is insured or guaranteed, unless explicitly stated for a specific investment vehicle. Interest income earned on asset classes shown is subject to ordinary federal, state and local income taxes, excepting U.S. Treasury securities (exempt from state and local income taxes) and municipal securities (exempt from federal income taxes, with certain securities exempt from federal, state and local income taxes). In addition, federal and/or state capital gains taxes may apply to investments that are sold at a profit. Eaton Vance does not provide tax or legal advice. Prospective investors should consult with a tax or legal advisor before making any investment decision.

The views expressed in this Insight are those of the author and are current only through the date stated at the top of this page. These views are subject to change at any time based upon market or other conditions, and Eaton Vance disclaims any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Eaton Vance are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Eaton Vance fund. This Insight may contain statements that are not historical facts, referred to as forward-looking statements. Future results may differ significantly from those stated in forward-looking statements, depending on factors such as changes in securities or financial markets or general economic conditions.

Before investing, investors should consider carefully the investment objectives, risks, charges and expenses of a mutual fund. This and other important information is contained in the prospectus and summary prospectus, which can be obtained from a financial advisor. Prospective investors should read the prospectus carefully before investing.

©2016 Eaton Vance Distributors, Inc. • Member FINRA/SIPC Two International Place, Boston, MA 02110 • 800.836.2414 • eatonvance.com