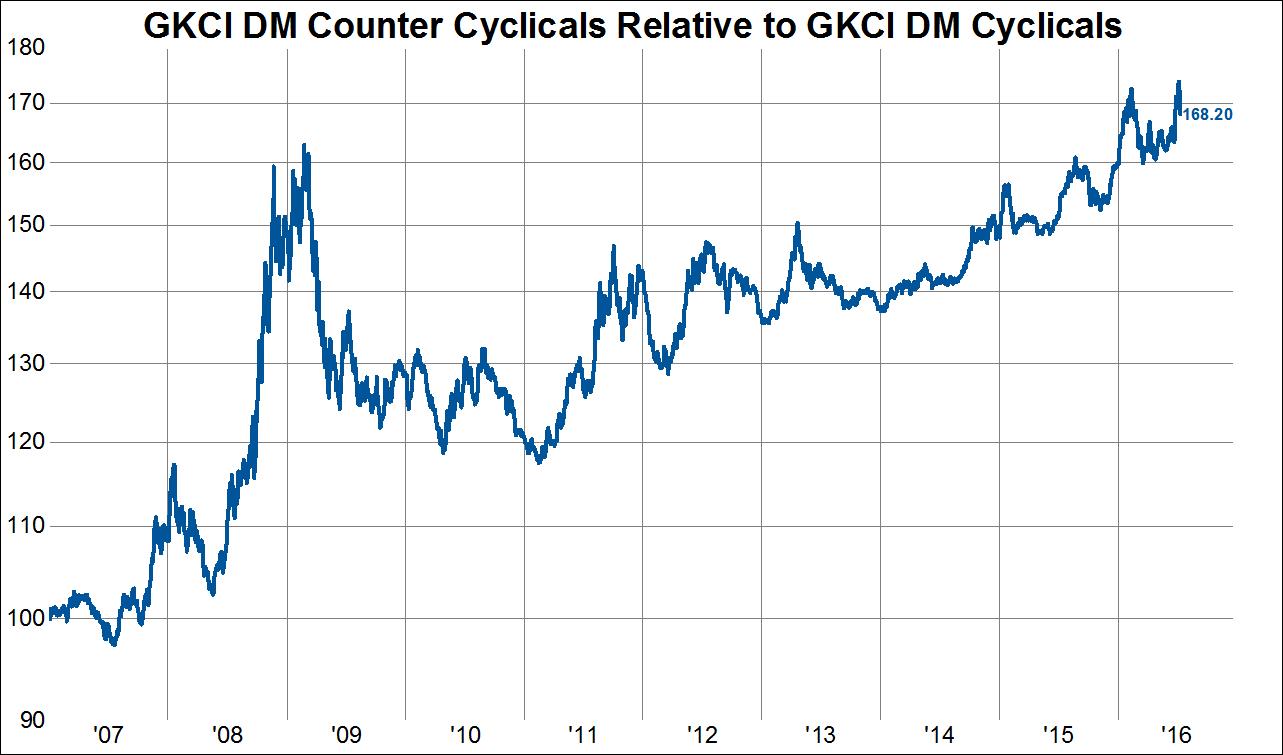

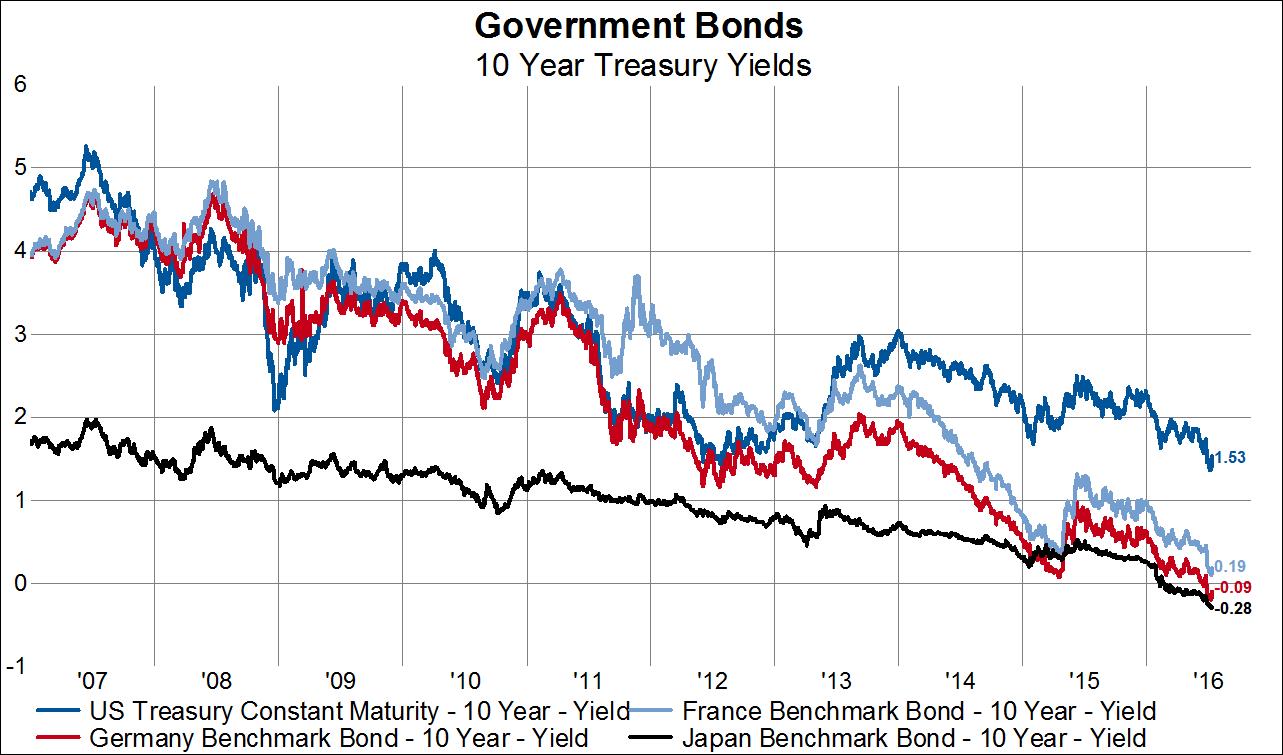

The post Brexit change in sentiment has been swift and considerable. More specifically, the change in sentiment over the last two days has been swift and considerable. Indeed, prior to Monday the S&P 500 had rallied 6.4%, but 10-year Treasury Bond yields had declined about 8bps, crude oil was down 2%, copper was flat, gold was up 3% and counter cycle stocks had outperformed cyclicals by 44bps. Not exactly a risk-on type of setup, especially when keeping in mind that the major European stock indexes remain down nearly 20% in USD terms from their 2014 highs and banks everywhere look downright terrible. Then, yesterday as the S&P 500 hit a new all time high and the move higher was repeated again today, rates rose, gold fell, and oil and copper rallied along with the beaten down cyclicals. Clearly, Monday and Tuesday were risk-on days, and this begs the question of whether we’ve just seen the beginning of a new trend or whether we’ve experienced a mean reversion move after being extended in the safe haven assets. A listen to the financial punditry would have one believing in the latter (without a doubt as usual!), while a look at the long-term trends would have one questioning if this may be an opportunity to add to one’s bond or counter-cyclical exposure. We don’t pretend to know the outcome, but suggest that it will take much more than two days of risk-on behavior to put a dent in ingrained trends that have been in place since 2006 and show no sign of reversing, as the charts below show.