Weighing the Week Ahead: Will Earnings Expectations Sustain the Rally in Stocks?

This week’s calendar includes a pretty normal schedule, but not the most important economic reports. There will be an abundance of FedSpeak, with questions about last Friday’s employment data. Despite this, the real story will be the start of earnings season. Expectations are pretty low. Statements about the outlook are always important, but that is especially true right now. The financial media will be asking: Can the profit outlook sustain the rally in stocks?

Last Week

The economic news was pretty good, and the market reaction was even stronger. The continuing market rebound has caught many off base. This week’s review emphasizes Friday’s employment report, since that was the biggest news.

Theme Recap

In my last WTWA, I predicted that the post-Brexit rally might continue if the economic news was good. This could lead to discussion of a possible “summer rally.” After a poor start to the week, the economic data finally turned the trick. From my “final thought” from last week:

Rightly or wrongly, much will depend on the employment report. The economy is the key to future earnings. Recession odds are low, earnings are improving, the oil issue has stabilized, and the Fed is on hold.

In addition to summer rally discussions, there was continuing skepticism – sucker’s rally, bull trap, and similar terms were bandied about. Sometimes I am right about the theme, but incorrect in my expectations. Last week both were on target.

The Story in One Chart

I always start my personal review of the week by looking at the great chart from Doug Short that summarizes the week. Since that post has not yet been updated this week, here is the picture from CNN Money. It was a pretty quiet week until the big Friday rally.

The News

Each week I break down events into good and bad. Often there is an “ugly” and on rare occasion something really good. My working definition of “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

The Good

- Rail traffic is showing improvement, but the story reflects some mismatch in holiday timing and weaker comparisons. (Steven Hansen).

-

Las Vegas real estate sales are improving, up 7.1% year-over-year. Calculated Risk notes:

This is a key distressed market to follow since Las Vegas has seen the largest price decline of any of the Case-Shiller composite 20 cities.

- Energy prices are lower, with gasoline down 50 cents from last year. The Oil and Energy Insider has plenty of good data. The charts show the forward curve of prices – not just the current spot. U.S. Production continues to decline.

- Spenders coming back from the mortgage crisis? Victoria Stilwell at Bloomberg makes the case, noting that time has “healed the wounds” allowing more credit for those who had foreclosures.

-

Long-leading indicators have improved. New Deal Democrat has a mid-year summary of ten indicators with demonstrated lead times. This is well worth a look. One nugget among the many good ideas:

The yield curve remains as positive even now, with the same slope as it had in the middle of the 1970s, 80s, and 90s expansions. The 5-year spread is even wider than it was during most of the 1960s.

- ISM services handily beat expectations (56.5 versus 53.3 expected and 52.9 last month). Scott Grannis analyzes the components and has a good chart comparing the U.S. to the Eurozone. He suggests that worries may be over-stated.

-

Employment news was good. We should follow multiple sources on employment, especially because of the volatility and revisions in the “official” data. This week the news was all good, but perhaps not as good as the initial market reaction would suggest.

- The ADP reported a gain of 172K private jobs, beating expectations of 152K. This is an important independent source.

- Initial jobless claims hit a new low at 254K, beating expectations by 14,000.

-

Non-farm payrolls recorded a stunning net gain of 287K, exactly the opposite of last month’s result of 11K after revisions. This was good news, but not as good as it seemed. It requires a deeper look.

- Commentary varied widely. For details, check out the summaries at Bloomberg and The Wall Street Journal. The bearish pundits either denied the strength, said that the market was not prepared for a rate increase, or both. Bullish commentators saw Santa in July, a reassuring number that would not cause the Fed to react.

- Many fine sources showed balance. This report was not as good as it seemed, nor was last month’s so bad.

- The charts are always interesting. Here are some of the most important from The WSJ and Bob Dieli’smonthly employment report (subscription required). To summarize from the WSJ, the change in earnings growth is still disappointing; most net job creation is full-time, the number of those wanting but not getting full-time jobs has declined significantly. From Dr. Dieli, the overall path of growth is the main theme. The duration of unemployment is an important and often-neglected story. Both sources have many more helpful charts and plenty of analysis.

The Bad

-

China rollover risk. Tom Orlik at Bloomberg Intelligence analyzes the current situation and the need to roll over $24 trillion in debt.

The amounts involved, the maturity mismatch between assets and liabilities, and the fragile state of final borrowers all increase the chances of a misstep — and the severity of an impact should one occur. That underlines the importance for the government to maintain buoyant nominal growth, ample liquidity and low interest rates.

- Manufacturing orders declined by 1%. Steven Hansen (GEI) has the full story with multiple takes on this data series. He sees more of a mixed picture.

- The worldwide yield curve is flattening. Ed Yardeni discusses this story, concluding that while not recessionary, it bears watching.

The Ugly

Three days of violence. Like everyone else, I was sickened and saddened by events. Leaders of all stripes had comments. My own favorite professor, Neil Browne, always emphasized the need for Asking the Right Questions. Although he has allegedly retired, his mission continues. He posted a thoughtful and insightful perspective.

The Silver Bullet

I occasionally give the Silver Bullet award to someone who takes up an unpopular or thankless cause, doing the real work to demonstrate the facts. No award this week. Nominations are always welcome. There is plenty of misinformation to refute!

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react. That is the purpose of considering possible themes for the week ahead. You can make your own predictions in the comments.

The Calendar

We have a fairly normal week for economic data. In my calendar I highlight only the most important items, helping us all to focus.

The “A” List

- Retail Sales (F). Will this reflect improved sentiment and employment?

- Industrial production (F). A volatile data series–closely watched given the recent manufacturing weakness.

- Michigan Sentiment (F). Good read on employment and spending.

- Initial claims (Th). The best concurrent indicator for employment trends.

The “B” List

- China Q2 GDP (F). It is amazing how quickly this number is generated….

- CPI (F). May start to get some attention if the expected increase occurs.

- PPI (Th). See CPI.

- Fed Beige Book (W). Descriptive reports from various Fed districts, prepared for next FOMC meeting.

- Business inventories (F). May data, but relevant for GDP.

- Wholesale inventories (T). Volatile May data – a factor in GDP calculation.

- Crude inventories (W). Often has a significant impact on oil markets, a focal point for traders of everything.

The big story will be corporate earnings. Fed fans can enjoy appearances from at least six of the regional Presidents. Expect each to be asked if Friday’s employment data changes the likely timing and number of rate increases.

Next Week’s Theme

Markets seem to have digested the Brexit story. The economic data have quieted recession worries. We can expect plenty of post-holiday FedSpeak, but little real news from those sources. It is the start of the Q2 earnings season. There are questions about both the top and bottom lines, but expectations are pretty low. The real question is about the future.

Everyone will be asking:

Can the profit outlook sustain the rally in stocks?

Feel free to join the discussion in the comments, but I see three key questions:

-

Will the outlook for earnings be stronger?

- Optimists note that the dollar has stabilized, as has the decline in energy. Earnings expert Brian Gilmartin has emphasized these themes, while still noting the sequential declines in revenues and earnings.

- Pessimists emphasize the “earnings recession” and the sluggish second-quarter economy.

-

Will stocks respond if the earnings outlook is good?

- Optimists note ultra-low valuations in many economically sensitive sectors. These stocks have room to run skepticism wanes.

- Pessimists point to lagging sectors that seem to lack upside. And of course, the familiar themes about overall market valuation.

-

Will fundamental improvement be supported by the technical analysis followers?

- Optimists see a potential breakout from the long-run trading range.

- Pessimists see an overbought market.

Quant Corner

We follow some regular great sources and also the best insights from each week.

Risk Analysis

Whether you are a trader or an investor, you need to understand risk. Risk first, rewards second. I monitor many quantitative reports and highlight the best methods in this weekly update.

The Indicator Snapshot

The Featured Sources:

Brian Gilmartin: Analysis of expected earnings for the overall market as well as coverage of many individual companies. This week he expresses more confidence about growth in earnings.

Bob Dieli: The “C Score” which is a weekly estimate of his Enhanced Aggregate Spread (the most accurate real-time recession forecasting method over the last few decades). His subscribers get Monthly reports including both an economic overview of the economy and employment.

This week the recession odds (in nine months) have nudged closer to 10%. This does not completely reflect Brexit effects, so we may get a further revision.

Holmes: Our cautious and clever watchdog, who sniffs out opportunity like a great detective, but emphasizes guarding assets.

Doug Short: The Big Four Update, the World Markets Weekend Update (and much more).

The ECRI has been dropped from our weekly update. It was not so much because of the bad call in 2011, but the stubborn adherence to this position despite plenty of evidence to the contrary. Those interested can still follow them via Doug Short and Jill Mislinski. The ECRI commentary remains relentlessly bearish despite the upturn in their own index.

Georg Vrba: The Business Cycle Indicator, and much more. Check out his site for an array of interesting methods. His latest update describes the elements of the indicator we cite every week.

RecessionAlert: Many strong quantitative indicators for both economic and market analysis. While we feature his recession analysis, Dwaine also has a number of interesting approaches to asset allocation.

As we review the weekly indicators it is important to maintain perspective. A 20% chance of a recession would be average. It is not a reason for fear, since it says that a recession is very unlikely. There will be a time to exercise more caution, but we are not yet close to that point. There are many very questionable recession stories right now.

How to Use WTWA

In this series I share my preparation for the coming week. I write each post as if I were speaking directly to one of my clients. For most readers, they can just “listen in.” If you are unhappy with your current investment approach, we will be happy to talk with you. I start with a specific assessment of your personal situation. There is no rush. Each client is different, so I have six different programs ranging from very conservative bond ladders to very aggressive trading programs. A key question:

Are you preserving wealth, or like most of us, do you need to create more wealth?

My objective is to help all readers, so I provide a number of free resources. Just write to info at newarc dot com. We will send whatever you request. We never share your email address with others, and send only what you seek. (Like you, we hate spam!) Free reports include the following:

- Understanding Risk – what we all should know.

- Income investing – better yield than the standard dividend portfolio, and also less risk.

- Holmes – the top artificial intelligence techniques in action.

- Why 2016 could be the Year for Value Stocks – finding cheap stocks based on long-term earnings.

You can also check out my website for Tips for Individual Investors, and a discussion of the biggest market fears. (I welcome questions or suggestions for new topics.)

Best Advice for the Week Ahead

The right move often depends on your time horizon. Are you a trader or an investor?

Insight for Traders

We consider both our models and also the best advice from sources we follow.

Felix and Holmes

We continue our neutral market forecast. Felix remains almost fully invested, including some of the currently-popular fixed income sectors. That is working well. The more cautious Holmes is still fully invested, in a diverse group of 16 stocks from a universe of nearly 1000, selected mostly by liquidity. That group is also responding well. Even when the overall market is neutral, there will often be some strong candidates. That is what we see now. It is not a resounding endorsement of the overall market, but a vote for opportunistic trading.

Top Trading Advice

Worried about the Bloodbath of 2016 and post-Brexit fallout? The Trading Goddess has your back with ten suggestions. My favorite is the pocket chain saw.

Wondering when to sell? Adam H. Grimes helps with the question of when to take profits.

Brett Steenbarger shows the preparation needed for trading. (Start at 3 AM? Hmm). He does describe the need to have a balance including some quality time away from the market.

Insight for Investors

Investors have a longer time horizon. The best moves frequently involve taking advantage of trading volatility!

Best of the Week

If I had to pick a single most important source for investors to read this week (HT Abnormal Returns), it would be Phil Huber’s Fun With Strikethroughs: Wall Street Maxim Edition. He takes on the common misperception that good investing can be accomplished through a few simple rules, and he does so adroitly with humor. You will enjoy the entire list, but here is my favorite:

As goes January, so goes the year nothing.

Stock Ideas

Chuck Carnevale is cautious, even including the dividend aristocrats. He carefully describes his valuation concerns while highlighting the best candidates.

Philip Van Doorn (MarketWatch) has more stocks that were hammered by Brexit yet still favored by analysts. Those shopping for laggards may wish to take a look.

Market Overview

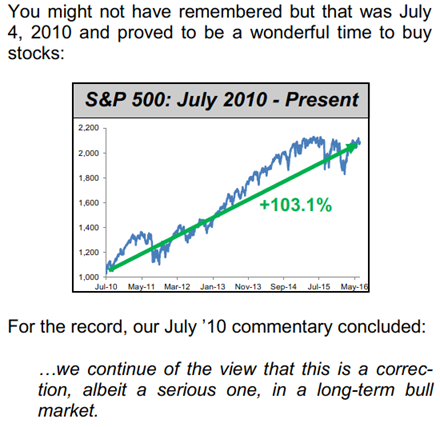

Shawn Langlois’ excellent “Need to Know” column features a variety of interesting market perspectives. This week’s “the call” segment featured Joe Fahmy’s four reasons for the Dow to hit 20K this year. (Check out www.dow20k.com for a prediction on this subject made in 2010 – when the Dow was at 10K).

Laszlo Birinyi publishes an excellent monthly newsletter (subscription required). He covers many analytic methods, but he features a collection of past media stories on the market. It is a helpful way to keep perspective. Take this one for example:

[Jeff] This might sound like something from last month, but it was actually written in 2010.

[Jeff] Maintaining the right long-term perspective is one of the biggest challenges for investors. I cite this striking example not to highlight the error of a single analyst. It was mainstream — a prevailing opinion published in a leading source.

Personal Finance

Professional investors and traders have been making Abnormal Returns a daily stop for over ten years. The average investor should make time (even if not able to read AR every day as I do) for a weekly trip on Wednesday. Tadas always has first-rate links for investors. This week, during his well-deserved vacation, he invited suggestions for good posts that had not gotten much attention at the time of original publication. This produced a number of high-quality ideas that he featured throughout the week. I am not surprised. My sense of something that is really good does not always resonate with readers. Other bloggers share this experience.

I am featuring one of these posts as this week’s best. In addition, please check out Wednesday’s article on Portfolio Management, and have a look at my suggestion. Cullen Roche’s piece on fear and negativity also has a timeless quality.

Watch out for….

The so-called “safe” stocks. These stocks are so overbought that it was a prevalent theme in this week’s investment advice.

Ian Bezek warns about utility yield chasing.

Ellie Ismailidou and Anora Mahmudova (MarketWatch) have a similar warning.

Corporate bond yields are also threatened (Barron’s).

Barron’s questions the fundamentals of the utility business – slowing growing demand vs. supply.

Final Thoughts

Stocks will eventually respond to an improving economy. We might have to wait for third-quarter earnings reports, another three months. An improved outlook will speed up this process, since stocks have tracked forward earnings. Improving the outlook will improve those projections.

Jeremy Siegel explains how stabilizing energy stocks, low interest rates, and improved earnings could lead to a 15% increase in stocks.

Years ago we could expect conference calls to “talk up” both current news and future prospects. A skeptical attitude was a healthy approach! More recently, CEO’s seem more interested in keeping expectations low. The financial community will pounce on negative statements and extrapolate to similar companies. It should be a great story.

The rotation from yield stocks to cyclical names and financials is the best opportunity for long-term investors.

But even more patience might be required.