Brooks Ritchey, senior managing director, K2 Advisors, looks beyond the day-to-day data and policy debates to a bigger-picture trend that could have important market and economic implications: the aging of the global population.

As legendary Rolling Stones frontman Mick Jagger has crooned, it clearly can be a drag getting old—and this applies to economies as well as aging rock stars.

The world is getting older (much older in some geographies), and to us this is without question becoming a meaningful drag on economic growth—one that will likely persist into the future.

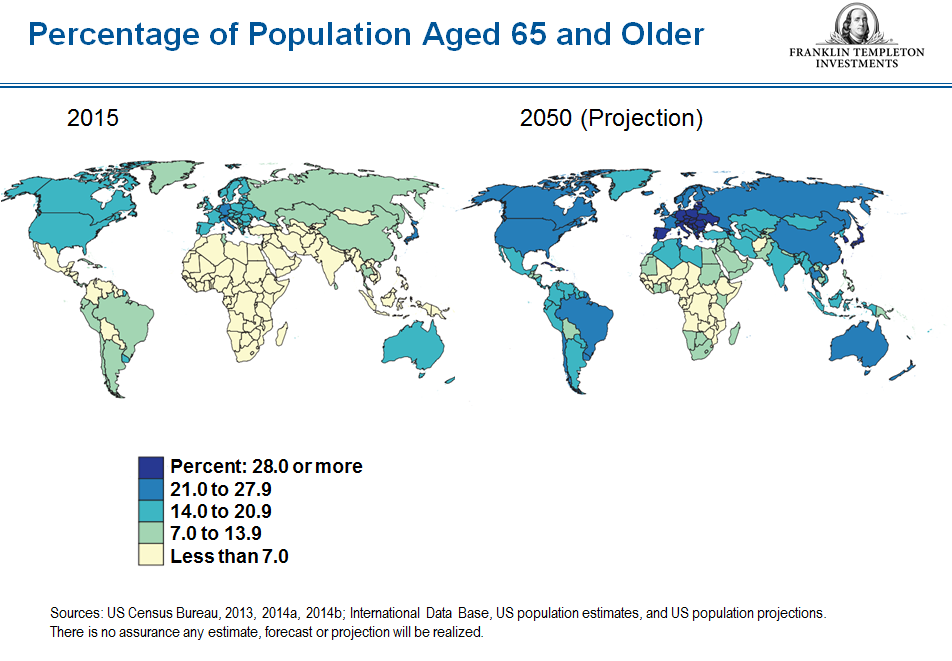

Consider the data: According to the US Census Bureau, among the 7.3 billion people on earth today, an estimated 8.5%, or 617 million, are aged 65 and older.1 By 2050, that number is projected to be roughly 20%, or 1.6 billion people worldwide. In other words, approximately one-fifth of the earth’s population will be over the age of 65 in about 30 years.2

Remarkably, by 2020—and for the first time in human history—it has been projected that people over 65 will outnumber children under age five. This crossing is just around the corner, and these two age groups will likely continue to grow in opposite directions for the foreseeable future.

In less-developed countries, especially those in Asia and Latin America, this doubling is moving much faster—projected to occur in less than two decades. (See the chart below.)

The speed at which country populations are aging is increasing exponentially as well. A commonly used measure for the rate of aging is the number of years it takes for a population aged 65 and older to double from 7% to 14% of the total. For most developed nations, where this doubling has already taken place, it took roughly three-quarters of a century on average. For France it was 115 years, for Australia it was 73 years, for Sweden it was 85 years and for the United States it was 65 years.3

The World Health Organization and others have observed that some of today’s emerging countries—as opposed to what the developed markets experienced in the 20th century—could likely be the first nations to grow old before they grow rich.

The reasons for this disparity are numerous, including the ability to extend life, modern medicine, better agriculture, social engineering (China’s national child-limit policies for example). Whatever the cause, this is truly a new phenomenon, and one that could have significant economic, social and geopolitical implications for the world.

Can’t Get No (Market) Satisfaction

Clearly the world is growing grayer (and hopefully, wiser, although the jury is still out). But what does this mean from an economic, or more closely, a market perspective?

First, let’s look at where things stand today in terms of economic strength. Despite the best efforts of central banks to paper the world with money, what have we really gained? Yes, we exchanged a potentially catastrophic global depression and entire collapse of the US banking system for a milder setback (now referred to as the Great Recession). In addition, we propped up risk assets along the way (in some instances indiscriminately), often at the expense of true fundamental valuations and alpha opportunities. But from an economic growth standpoint, what has been the gain? Based on the latest projections, it would seem not much—at least as we see it.

On April 27, the Bureau of Economic Analysis reported that the US economy grew at just a 0.5% annualized rate in the first quarter. The number missed expectations, reflecting growth at half the rate recorded in the fourth quarter 2015 and at the lowest quarterly growth rate since the first quarter of 2014, when the winter was blamed for a negative reading (apparently people were surprised it was cold in North America). This was also the third consecutive quarter of gross domestic product (GDP) growth rate declines.

Based on these numbers, it appears that the massive quantitative easing (QE) programs (the ZIRPs, NIRPs, LTROs, ESMs, EFSMs, etc.), while smoothing the aftermath of excessive leverage, have yet to succeed in terms of jump-starting growth. Why?

Some might say the economic theory underpinning those programs was flawed from the beginning (see our prior blog: ZIRPs and NIRPs and Unintended Consequences). Others argue that they were—and still are—the only path forward. Perhaps even more liquidity is needed? In my view, the answer is probably somewhere in the middle, and hopefully someday we can find that equilibrium.

Academic QE arguments notwithstanding, there are other real and significant structural headwinds impacting economic growth—key among them is the aforementioned explosion in the world’s aging population. This trend cannot be ignored.

Time Is on Our Side? No It’s Not

Economics can be defined as the study of how people make choices under conditions of scarcity, and the impact of those choices on society. In a future world where presumably goods and services remain static but a shrinking number of people venture out to buy those goods and services (scarcity of demand), what could we expect the natural economic adjustment to be? Falling prices perhaps? Deflation?

Demographic trends are like a slow leak in an upstairs bathroom. They may be so gradual and understated in influence that they go unnoticed or unrecognized for some time—maybe decades—until the tub falls through the ceiling. In other words, economists and other observers often marginalize the aging of the global population. While the shift in demographics has thus far been smooth and gradual, in our view, the potential volatility this could someday bring to global economies and markets is significant. Has the water stain on the ceiling already started to form?

Remember, production depends on population, not just for labor but for consumption as well. There are two basic components to GDP: growth in productivity and growth in the size of the workforce. So to grow an economy you need to either increase the (working-age) population or increase productivity.

We’ve Been Around a Long, Long Year

It seems pretty apparent we will not be growing the workforce anytime soon. Consider the baby boom generation, the bulge of people born after World War II between 1946 and 1964. According to the Pew Research Center in Washington, DC, 10,000 baby boomers turn 65 (the age historically associated with retirement) every day in the United States. This began in 2011 and will continue each day until 2029. Think about the implications of that—10,000 every day!

More retirees mean slower household formation, reduced consumer spending, and downward pressures on equity prices as retirement cuts purchasing power. Boomers will likely sell shares to finance retirement—as their mentality shifts from growing wealth to preserving it. No new homes, fewer vacations, no new cars every few years, less conspicuous consumption. Health care will likely be their primary concern.

According to economist John Mauldin, the average savings for a 50-year-old in the United States is $42,000. A couple aged 65 can expect to pay $218,000 for medical treatments over the next 20 years. One in three people have no money saved for retirement at 65, and almost 40% are 100% dependent on Social Security. Looking at those figures, it doesn’t appear that there is much in the way of disposable income on the horizon.

A Storm Is Threatenin’ (Our Retirement)

As we think about the global economic machine going forward, it is important to put ideas around aging and the Westernized notion of retirement in perspective. The assumption that one leaves the work force at 65 and settles into a leisurely life of shuffleboard, golf and 5 p.m. dinner service followed by movie screenings at the five-star senior residence in Florida or some other sunny locale is a relatively new social construct—and a decidedly Western one as well.

For most of human history, people worked as long as they were physically able and then died shortly thereafter (sadly, in some parts of the world this is still a reality). So this practice of retirement, albeit representing a great social advancement, is relatively new. As such, the longer-term economic implications cannot be fully understood or anticipated.

Consider China’s one-child policy, for example. This has created a social stratum where each worker in today’s generation will likely end up supporting two parents, four grandparents, and perhaps one or more of their own children. In addition, China does not have a Social Security program or other similar safety net, and a large portion of its population is still living what we would consider to be below the poverty line. Never mind conspicuous consumption—what are their prospects for simply living in retirement?

You Can’t Always Get What You Want …

In our view, collectively the prospective headwinds created by the trend toward global aging look pretty ominous. The bottom line is that if you want an economy to grow, there must be an economic environment that is friendly/fertile for growth. Today, it seems we don’t have that environment, outside of central bankers manning the liquidity fire hoses.

Structural challenges notwithstanding, there may be some industries that stand to benefit from this shift. We might expect to see strong growth in the health care sector for example, including health care technology and pharmaceuticals. Alternatively, we may find that technology gives us an edge in overcoming the production deficit left behind by the retirees. Maybe the machines can produce more with less.

The point is we cannot predict the future and so may not get what we think we want from this paradigm shift in global demographics. In the end, however, we may find we get some things we never thought we needed.

The comments, opinions and analyses presented herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

What Are the Risks?

All investments involve risks, including the possible loss of principal.

_______________________________________________________

1 Source: US Census Bureau, “An Aging World: 2015, International Population Reports,” issued March 2016.

2 Ibid.

3 Ibid.

© Franklin Templeton Investments

© Franklin Templeton Investments