“Yeah, but no, but yeah, but …”

Vicky Pollard, Little Britain

As pointed out in the July Absolute Return Letter, published only days ago, Brexit requires a great deal of thinking. All we know at this point in time is that Brexit will (probably) happen at some point over the next 2-3 years, but we still have no idea what the actual implications will be. It all depends on the forthcoming negotiations between the UK and the EU (and the rest of the world), and David Cameron and Boris Johnson probably both did the wise thing and chickened out, because that isn’t going to be much fun.

In that context I note that it has taken Canada ten years to negotiate their free trade agreement with the EU, and that was prioritised by the EU negotiators. The EU have already declared that the UK will not be prioritised. On top of that, the UK will now have to negotiate trade agreements with pretty much every country around the world that it does business with – a monumental task, and the legal resources to do that job do not exist, according to a government official.

As events unfolded, it would probably be fair to say that the vote wasn’t really about what it was supposed to be about; that got lost along the way. No, it turned into a referendum for or against immigration and a protest vote against Brussels and London. The amount of bitterness in large parts of the country – and in particular in the North – is such that many saw the referendum as an opportunity to give Brussels and London (or at least the elite in those cities) a slap in the face.

Economic illiteracy

It turns out that the most googled subject in the UK in the days following the referendum was the EU, and one of the most frequently asked questions was What is the EU? I am not at all suggesting that people in the UK are illiterate on economic affairs – only that a fair number of them are (my feeble attempt to add some black humour to a rather grim subject). That said, and apart from the fact that illiteracy on economic matters is not a particular British phenomenon, the outcome of the referendum should teach us all a lesson.

In the UK, the divide between the upper classes and the lower classes, between rich and poor, is getting ever more substantial. The divide between the ‘haves’ and ‘have nots’ is probably bigger now than it has been at any point since World War II, and something needs to be done to correct that. So many people in the north of the country voted ‘Leave’ because they feel let down by London. In their eyes, the ‘haves’ all live in and around London and, with a few noticeable exceptions, that is correct. Now, they were offered the opportunity to express what they think about that. If these imbalances are allowed to continue to escalate, terrible social conflicts are on the horizon.

Furthermore, there is compelling evidence to suggest that many people didn’t really understand the gist of the issue at stake. Sunderland is a good example. Nissan employs no less than 27,000 people at its car factory in Sunderland and is one of the largest employers in the North-East of England. According to my brother-in-law, who knows one or two things about the car manufacturing industry, it is not prohibitively expensive to move a car factory from one place to another, as long as you do it when a new model is introduced. The reason? The robots that build the cars account for a very substantial percentage of the total cost, and the robots are always replaced when new models are introduced.

Despite the massive importance of Nissan to the local economy, and the risk of Nissan going elsewhere if the UK were to leave the EU, no less than 61% of people in Sunderland voted to leave. At a smaller scale, the same happened in Swindon in the South-West, which is the home of Honda UK. Quite astonishing.

Another example would be the fact that the regions most economically dependent on EU grants voted Leave – almost without exception (chart 1). By doing that, people in the North effectively cut off the hand that feeds them.

Chart 1: Leave vote by region

Source: Financial Times, June 2016

How the Remain campaign got it all wrong

The Remain campaign was – in my humble opinion - hopelessly managed. It is basic knowledge that you should never give voters an open invitation to protest, because voters love to do precisely that, social divide or not. We have seen that happen so often before (in the UK and elsewhere), so why did the UK government make that basic mistake? I wish I knew but I don’t.

Poor research was another glaring mistake, or perhaps it was hubris oozing out of an overly confident Remain campaign? Allow me to share some examples with you. One of the fluffier arguments put forward by the Leave campaigners leading up to the referendum had to do with immigration. Leave campaigners said that Albania, Macedonia, Montenegro, Serbia and Turkey - with a combined population of 88 million - are all in line to gain EU membership in the coming years.

Michael Gove, one of the leaders of the Brexit campaign, said back in May that the population of the UK would increase by between 2.6 million and 5 million by 2030 (and he specifically said would rather than could). He based his prediction on the future migration from the five countries mentioned above on the assumption of their accession in 2020.

That argument would have been so easy to take apart. Firstly, all EU member nations have a right to veto the accession of new member states, so it would be very easy to stop. Secondly, at least in the case of Turkey (by far the biggest of the five), the UK wouldn’t be alone. It is common knowledge that the relationship between Germany and Turkey, and between Mrs. Merkel and Turkey’s President Erdogan in particular, is below freezing point, and Turkey would never stand a chance of getting past both Germany and the UK. Why did the Remain Campaigners not play that card?

The most obvious card for the Remain campaigners to play would have been Putin’s undiluted support for the Brexit campaign. Considering how unpopular and distrusted the Russian leader is in the UK, why did Cameron never ask the people of Britain why they would support something that Putin wanted so badly? That would have killed the Brexit campaign in less than 5 minutes.

Given the Remain campaigners’ failure to respond to some obvious mistakes by the Brexit campaigners, the more cynical side of me actually wonders if Cameron really wanted the UK to stay in the EU? Perhaps he did but with some caveats, which would explain his lukewarm campaign.

The prisoner’s dilemma

Now, a couple of weeks after the referendum, we are admittedly in a bit of a dilemma – almost akin to a prisoner’s dilemma. The more financial markets puke over the next few months, the more likely lawmakers on both sides are to forget past disagreements and insults, and work on a solution that would keep the UK in the EU. On the other hand, if financial markets get a whiff of something about to happen - a possible compromise solution – financial markets will perform better, and thus make it less likely to happen.

FX markets, equities and commodities all puked the first couple of days after the referendum but, more recently, the atmosphere has been somewhat more upbeat - at least in equities and commodities. I have checked with a few friends in the industry, and the picture they have painted is remarkably consistent. Investors have not suddenly turned gung-ho on Brexit. A very substantial part of post-Brexit buying is short covering.

What happens next?

The rest of this one-off summer 2016 Absolute Return Letter on Brexit is dedicated to the road forward. What could happen, or rather, what is likely to happen next? The following five points are certainly not a given, but neither are they just plain speculation. Each and every one of them have a reasonably good chance of materialising and, in the following, I will assign a (very subjective) probability to each of them, so let’s begin with the first, and probably most contentious, prediction:

1. Brexit may never happen.

This rather controversial prediction is based on modern day constitutional law and how democratic regimes all over the Western World work. Whether you look at the UK or any other modern day democracy, it is obvious that there are significant checks and balances in place to ensure that any action undertaken by the government is not based purely on majoritarian views, but on the views of the representatives of those people, and what those representatives consider the best outcome for the nation.1

Modern day democracies were set up this way to protect minorities – to avoid a ‘bullying’ majority forcing through legislation deemed inappropriate for the nation. The British parliament is heavily skewed towards Remain, with 479 MPs polling for Remain versus 158 for Leave. That leaves the government in a bit of a pickle but, at the same time, with enough ballast to look for a way out.

Given the political turmoil in recent days – Boris Johnson dropping out of the race to become the next Prime Minister after sustaining some pretty serious back-stabbing conducted by a surprisingly Machiavellian Michael Gove – it is probably fair to say that anything can now happen; however, as things stand at this moment, Theresa May is emerging as the favourite to become the next Prime Minister of the UK.

This is relevant as far is Brexit is concerned, as she is a Remainer. Should she win, the government under her leadership will probably bend over backwards in their frantic search for a solution to the Brexit crisis. What that solution is remains to be seen but, as I mentioned earlier, the more ‘uncooperative’ financial markets turn out to be in the weeks and months to come, the more likely other European leaders are to swallow some pride and work out a compromise solution.

Probability of Brexit never happening with Theresa May at the helm: 30-40%.

Probability of Brexit never happening with a Leaver at the helm: 10-20%.

2. Assuming we proceed with Brexit, a second independence referendum in Scotland goes ahead – and possibly one in Northern Ireland as well.

Scotland voted overwhelmingly in favour of staying in the EU – 62% to 38%. Not even in the pro-EU capital of the country was there a bigger majority. There is little doubt in my mind that, should the UK actually exit the EU, a second Scottish independence referendum is an inevitability, and the result of the 2014 referendum, which was a relatively slim 55% majority in favour of remaining part of the United Kingdom, could very well be overturned. The fact that Scotland will have to go through the entire application process again is not likely to act as a deterrent, such is the appetite for EU membership north of the border.

Northern Ireland is in a slightly different position. The demand for independence in that part of the country is almost non-existent, but a growing number of people want the two Irelands to be re-united, and an EU exit would most likely have the effect of pushing more people in that direction.

The reality facing the political establishment in the UK is therefore a total meltdown of the United Kingdom2, should Brexit happen. This will only encourage our political leaders to be even more creative in their search for a compromise solution.

Probability of a second Scottish referendum: 80-90%.

Probability of Scotland leaving the Union: > 50%.

Probability of a referendum on Irish re-unification: 20-30%.

Probability of Northern Ireland leaving the Union: 10-20%.

3. Brexit leads to an avalanche of referenda in other European countries.

Should Brexit actually happen, Leavers all over Europe (and there a many of them) will demand a referendum in their country as well. Coming from Denmark, I follow the political debate in that country particularly closely, and there is no doubt in my mind that a British exit will be akin to pouring petrol on the fire of a very emotional Danish debate.

Geert Wilders, the leader of the far-right Dutch Freedom Party, has promised to put a possible Dutch referendum on the agenda in the general elections next March, should he win. One shouldn’t take such a promise lightly, as the Freedom Party holds a substantial lead in the opinion polls at present. In other words, the Netherlands could possibly be next to exit.

In France, Marine Le Pen, leader of the Front National, has suggested that France could follow Britain in leaving the EU, hailing the Brexit vote as the beginning of a “movement that can’t be stopped”. Le Pen has said that, if she wins the French presidential election next April, she will hold an in/out referendum on the country’s membership of the EU within six months. Having said that, opinion polls don’t fancy her chances of becoming the next French president. I do not agree with Le Pen on many issues, but I would have to agree that Britain has started an avalanche that may be difficult to stop.

Probability of another EU country holding a referendum within two years: 70-80%.

Probability of another EU country deciding to leave within two years: 20-30%.

4. Whether Brexit actually materialises or not, the outcome of the UK referendum leads to a significant slowdown in economic activity all over Europe; consequently, policy rates stay put for the time being.

Leavers in the UK live in a dream world; such is the conviction that Brexit will lead to an acceleration of economic growth. Little do these people (appear to) understand that the UK is already very competitive when compared to most other countries around the world (as discussed in the April Absolute Return Letter).

Consequently, longer term, Brexit is likely to have little or no (positive) effect on GDP growth. As far as the rest of Europe is concerned, longer term, the effect of Brexit will also be relatively modest. The UK economy simply isn’t big enough to really matter.

In the short term, all of Europe (the UK included), is likely to be negatively impacted by Brexit. I have spoken to a handful of company owners around Europe after the UK referendum, and they all told me the same story. Until we have more clarity, all new investments have been frozen. If that view is representative, it doesn’t take an Einstein to figure out what could happen to GDP in the second half of 2016.

The risk to GDP growth short-term has pretty much eliminated any risk of rate hikes anywhere in Europe, at least for the remainder of this year. It was already very low in the Eurozone but growing steadily in the UK. Meanwhile, in the U.S., a slowdown in Europe is likely to have at least some effect on the Fed’s actions.

Probability of a UK recession in the second half of 2016: 60-70%.

Probability of a Eurozone recession in the second half of 2016: 40-50%.

Probability of the Bank of England staying put in the second half of 2016: > 90%.

Probability of the ECB staying put in the second half of 2016: > 95%.

Probability of the Federal Reserve Bank staying put in the second half of 2016: 30-40%.

5. Social and political instability in the UK to rise, as people get more and more disappointed that Brexit doesn’t deliver ‘better times’ as promised by the Leave campaign.

Not only is Brexit unlikely to lead to any increase in economic growth but, in the years to come, and for reasons entirely unrelated to Brexit, economic growth in the UK is likely to remain quite subdued, at least when compared to the growth we have enjoyed in the last 30-35 years.

As time goes by, and economic growth continues to disappoint, political infighting and rising tensions between the ‘haves’ and ‘have nots’ could generate a very unhealthy overall climate.

That said, the opposite could also happen. Brexit never materialises, the overall economy deteriorates as a result of worsening demographics, and the Leavers blame it on a government that ‘saved’ Britain from Brexit, even if the deterioration in overall economic conditions has nothing whatsoever to do with the EU.

In other words, whether Brexit actually happens or not, because slow economic growth is pretty much set in stone for many years to come, one side is more than likely to blame the other. On a personal level, I have had a great deal to do with the NHS in the last couple of years, and I am amazed how many in the NHS workforce actually come from abroad. If we leave the EU, and hospitals in the UK are constrained from recruiting abroad, NHS services will almost certainly deteriorate, which is likely to create social unrest.

Alternatively, if we stay in the EU, the NHS will continue to recruit abroad, as the British labour market cannot deliver sufficient hospital staff with adequate training and knowledge. As GDP growth doesn’t pick up, as the Leave-supporters were told it would, the government will come under fire, the NHS will be heavily criticized for its recruitment policy by an ignorant public, and social conditions will become more unsettled.

Corporate profits under pressure

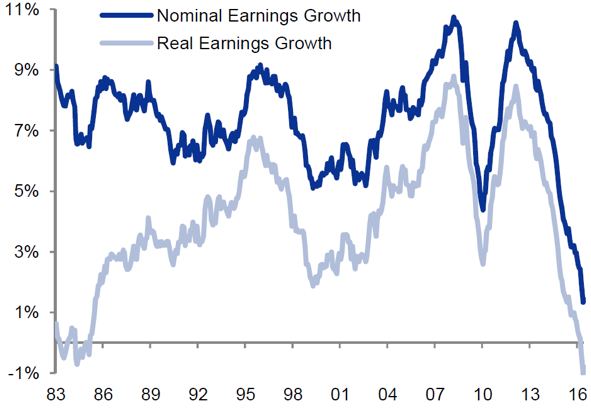

As we all know, when corporate profits come under pressure, jobs are lost. Global earnings growth is now the lowest it has been since the great bull market took off in the early 1980s (chart 2). The obvious implication is that unemployment will rise. As more people lose their job, social unrest can only increase and, in the UK, one side of the Brexit campaign will blame the other.

Chart 2: Global earnings growth (10-year rolling)

Source: Goldman Sachs Global Investment Research, Datastream, June 2016

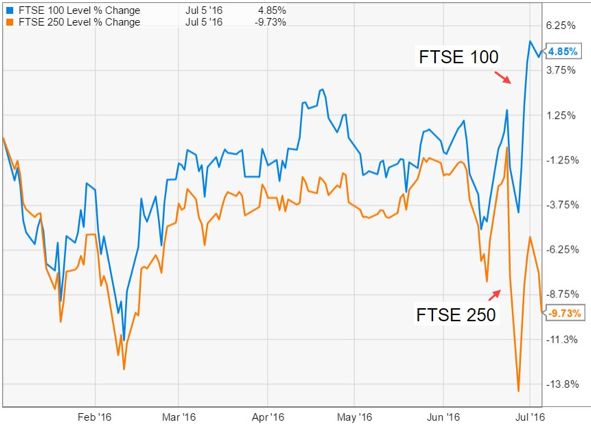

One final note, before I wrap it all up. The financial instrument that has taken the biggest hit so far is the UK currency. GBP continues to fall and is now at a 30-year low vs. USD. Exporters obviously stand to benefit from that, and the FTSE 100 index, which consists largely of big exporters, is benefitting. Meanwhile, the FTSE 250 index, which consists mostly of smaller, domestically orientated companies, is having a rough time (chart 3).

Chart 3: FTSE 100 vs. FTSE 250

Source: The Daily Shot, Ycharts.com, June 2016

Should I be right, and some sort of compromise solution worked out, there is a trade to be done here, as FTSE 250 will dramatically outperform FTSE 100 for a period of time. I wouldn’t put the trade on yet, though, as I need to be even more convinced than I am now that Theresa May will indeed become our next Prime Minister.

Conclusion

Holding a referendum on the EU, when lower economic growth is on the cards regardless, and when you have to deal with a very anti-EU, and very sensationalist British newspaper industry, was a massive mistake, and David Cameron threw in the towel as a consequence.

Brexit may still happen, or it may not. That said, demographic factors will prevent the economy from growing anywhere nearly as fast as it has done in the last 30-35 years, and every bit of help would be appreciated. Now, all the uncertainties caused by the outcome of the referendum will have exactly the opposite effect. Already modest economic growth will turn even lower.

From an investment point of view, uncertainty is never good, and the combination of Brexit and a new Prime Minister provides plenty of uncertainties indeed. UK equities are therefore likely to be a no-go in the short term, and the fact that equities rebounded following the sharp fall the first couple of days after the referendum gives me little confidence. Technical factors (short covering) rather than fundamental factors drove equities higher, which is not a very comforting piece of news.

Having said that, there is an important bargaining reality that will guide negotiations in the months to come, and that reality is likely to impact financial markets in a more positive way, once the worst dust has settled. I am referring to the reality (and I paraphrase Woody Brock) that both sides – i.e. the UK and the EU – will lose a lot if Brexit is the ultimate outcome. In other words, both sides have a strong incentive to work out a Remain solution, even if neither side will admit to that at this moment in time.

Niels C. Jensen

7 July 2016

©Absolute Return Partners LLP 2016. Registered in England No. OC303480. Authorised and Regulated by the Financial Conduct Authority. Registered Office: 16 Water Lane, Richmond, Surrey, TW9 1TJ, UK.

Important Notice

This material has been prepared by Absolute Return Partners LLP (ARP). ARP is authorised and regulated by the Financial Conduct Authority in the United Kingdom. It is provided for information purposes, is intended for your use only and does not constitute an invitation or offer to subscribe for or purchase any of the products or services mentioned. The information provided is not intended to provide a sufficient basis on which to make an investment decision. Information and opinions presented in this material have been obtained or derived from sources believed by ARP to be reliable, but ARP makes no representation as to their accuracy or completeness. ARP accepts no liability for any loss arising from the use of this material. The results referred to in this document are not a guide to the future performance of ARP. The value of investments can go down as well as up and the implementation of the approach described does not guarantee positive performance. Any reference to potential asset allocation and potential returns do not represent and should not be interpreted as projections.

1 Thank you to Ecstrat for pointing this out, See here.

2 Which is really called The United Kingdom of Great Britain and Northern Ireland, to give its full name.