As we plan our holiday weekend we were discussing our attendance at the Stone Bank July 4th parade. My wife and son are excited about this family tradition while I was hoping for something new. Stone Bank is a small unincorporated town 30 miles west of Milwaukee and the parade is everything a small town U.S.A. 4th of July parade should be. It has high school marching bands, fire trucks from the surrounding area throwing candy, service men and women, water balloons, motorcycles and classic cars with local politicians, maybe even the county sheriff! As we discussed the parade, it became apparent that this is a great way to celebrate our country’s birthday. Sometimes “more of the same” is ok.

For the last several days the market has been focused on all things British as a result of the “leave” vote out of the U.K. However, as we pointed out in our last writing, the U.K. has little impact on the U.S. economy, corporate earnings and the direction of asset prices here. What does have a meaningful impact is the U.S. consumer who continues to drive more than two thirds of our economy’s growth.

U.S. Consumer

Today we received an important report on the health of consumer spending. The report showed a May increase of .3% and a revised April increase of .8%. With these numbers it looks like second quarter spending could come in at 4%, supporting the idea that overall economic growth will be 3 to 4 times greater than the first quarter.

This report also included one of the Federal Reserve’s measures of inflation, the personal consumption expenditure deflator (PCE deflator). We know that one of the Fed’s concerns is keeping inflation stable. The PCE deflator rose .2% in May over April, however the annualized rate of growth was only .9%. Excluding the effects of the more volatile food and energy components, it was a higher 1.6%. Still this is well below the Fed’s target of 2%. Many investors are arguing that we will see an uptick in inflation and that will cause the Fed to finally move again to raise rates. We’re not so sure.

Wages

We know that as we move through the year, the transitory effect of last year’s lower energy prices will come out of the deflator and the inflation rate will rise. However, the most important kind of inflation comes from growth. One example of this would be wage inflation. As the unemployment rate comes down and the supply of workers gets smaller, you would expect wages to rise causing wage inflation. However, the current dynamics of the labor market have created a situation where wage inflation has been subdued even though the unemployment rate is below 5%. Due to the large number of people in part-time jobs wishing they could be full-time and the retirement pace of baby boomers at the top-end of the pay scale, wage inflation is only 65% of what we would expect at this point in an economic cycle.

Still it is positive and we can see this in today’s personal spending report.

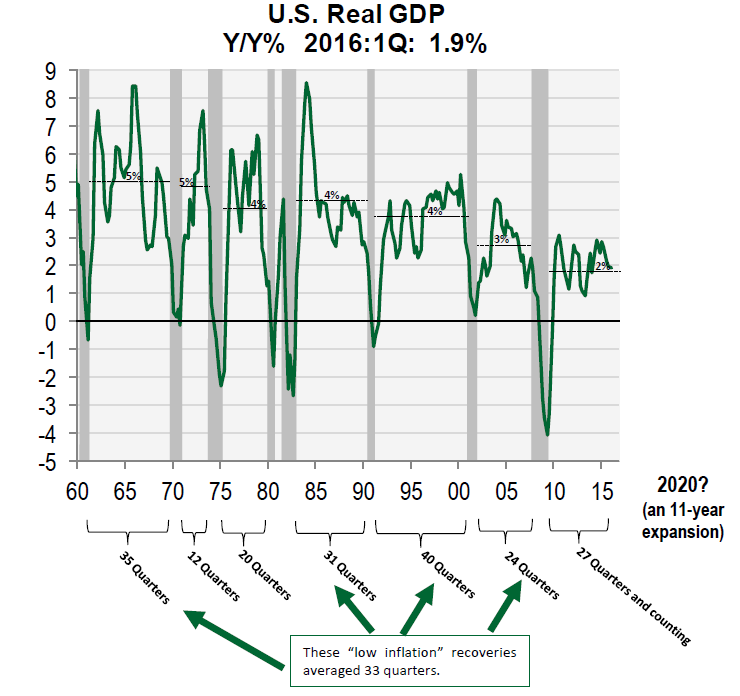

What all of this means is that this year’s economic growth rate is likely to look much like last year’s. In fact, as you can see in the chart below, we have been running at around a 2% growth rate since 2010. You may also notice that the current rate of economic growth is well below what we’ve experienced over the last several decades. So, should we expect something different in the near-term? We would argue not.

Source: Cornerstone Macro

However, there is a silver lining. Because inflation is running at a relatively low rate, the chart also indicates that economic growth periods last longer when inflation is low. That suggests that while the current growth rate is below the long-term average, the business cycle expansion period may last longer than usual. And so, sometimes more of the same isn’t so bad.

Enjoy your 4th of July holiday weekend and take in a small town U.S.A. parade. There is nothing better.

Brian Andrew is Chief Investment Officer for Johnson Financial Group