Would a crystal ball give dividend investors an edge?

For several weeks Janet Yellen made the case the case for continued Fed rate hikes. Like a good prosecutor on Law and Order, she presented the evidence brick by brick, indicator by indicator. Then nonfarm payrolls burst into the courtroom as a surprise witness, testifying that employment in May was weaker than expected. It now appears the Fed chair has asked for a recess.

In the wake of that latest economic disappointment, the CME’s Fed Fund futures recently placed the odds of a June Fed rate hike at just 2% compared to 26% the prior month. Odds placed on a hike at the July, August, September and November meetings also moved lower. No meeting in 2016 garnered odds greater than 50%. With such low odds, it’s anyone’s guess as to when the Fed will act.1

But what if an investor didn’t need to guess? What if an investor knew when the Fed would raise rates and invested accordingly? Maybe that crystal ball purchased years ago from the Sharper Image suddenly displayed the number “0.25” alongside a Fed meeting date. Based on past Fed interest rate cycles, what would our lucky investor invest in?

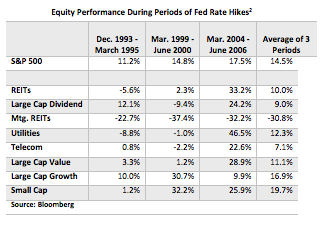

The tables below reflect the last three Fed tightening cycles based on the quarterly change in the Fed Funds rate. Cumulative returns from various equity indices are compared with the return from the S&P 500. The indexes represent large cap value, large cap growth, small cap, and several traditional dividend-oriented portfolios:

Over these periods, which date back to 1993, divining changes in the Fed Funds rate would not have given an investor much of an advantage. No index led the pack more than once. Although small caps and large growth stocks delivered the highest returns on average, this was largely due to big returns during the tech bubble (middle period). These sectors lagged when tightening ended and the bursting bubble punished high expectation stocks in particular.

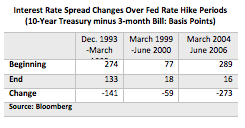

If our investor with the crystal ball seeks income and capital gains, the one clear message from the data is to avoid mortgage REITS as the Fed hikes rates. These companies can be held hostage to narrowing interest rates as it is their mission to borrow short term and invest in (typically) long term mortgage securities. As the table below illustrates, interest rate spreads narrowed in each of the three Fed Funds cycles. We use the difference between the 10-year Treasury and 3-month Treasury bill yield as a measure of interest rate spreads:

But knowing when the Fed will make its next move may or may not mean that mortgage REITs will underperform during the next series of rate increases. In the prior three tightening periods, spreads narrowed even as longer term rates continued to rise. Short term rates simply rose faster.

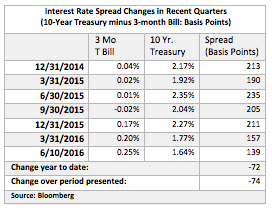

This time around, longer term bond yields have been falling while short term rates have been rising – despite there being just a single rate hike on the books. Further, instead of trying to slow a growing economy, the Fed is awaiting an economy it perceives healthy enough to weather a rate hike. Our investor with a view of tomorrow’s Fed Funds rates may need to dial in future 10-Year yields before making a bet either way on the MREIT sector:

Aside from MREITS, the first table gives us little indication as to how we can expect dividend stocks to perform during a series of Fed rate hikes. But it also signals that Fed tightening does not guarantee poor performance from dividend payers. In fact, REITs and utilities were among the best performers in one period. Traditional large cap dividend payers did well in two of the three periods. Dividend payers generally underperformed in the middle period. This again reflects the tech bubble when investors were chasing growth at any price.

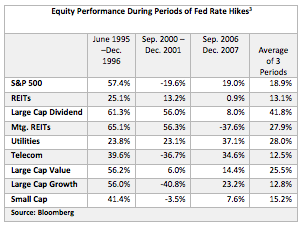

Results were just as mixed following the end of Fed tightening, although dividend stocks tended to outperform the broad market. The table below presents returns from the same group of indexes in the six quarters following that final Fed rate hike of the period:

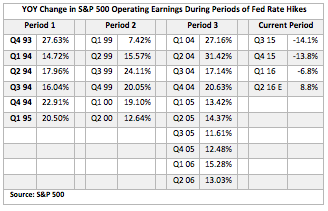

While the investing and economic backdrop in each period is different, today’s low bond yields hint that the current environment is clearly unique. Consider that corporate profits grew at a healthy rate during the prior three cycles. Yet S&P 500 operating profits were sliding (year-over-year) even before the rate bump in December. While profits are expected to improve in the second half as energy companies recover and the dollar wreaks less havoc on overseas exposure, this is clearly not a typical tightening environment. Past relationships are hardly destiny this time around:

Perhaps our investor’s crystal ball should come with a disclaimer: “Future performance is not guaranteed, even if the timing and extent of the Fed’s rate hikes are known.”

Rather than a crystal ball, our investor may have been better off buying a Sharper Image foot massager.

1 Probabilities of possible Fed Funds target rates are based on Fed Fund futures contract prices assuming that the rate hike is 0.25% (25 basis points) and that the Fed Funds Effective Rate (FFER) will react by a like amount.

CME Group’s 30-Day Fed Fund futures prices have long been used to express the market’s views on the likelihood of changes in US monetary policy.

2 Performance period reflects the calendar quarter prior to the first rate hike through the quarter reflecting the last rate hike. Indices represented in addition to S&P 500 are FTSE NAREIT All Equity REITs Index, Dow Jones Select Dividend Index, FTSE NAREIT Mortgage REITs Index, Philadelphia Utility Index, S&P 500 Telecommunication Services Sector Index, Russell Large Cap Value Index, Russell Large Cap Growth Index, Russell 2000 (Small Cap) Index.

3 Performance period reflects the calendar quarter following the final Fed rate hike.