Exchange-traded funds (ETFs) are now an established item on the investment menu, and there are now many flavors to choose from. Proponents claim ETFs that are designed to track capitalization-weighted indexes may offer an efficient way to gain broad market exposure, but Patrick O’Connor, our head of global ETFs, says many investors may not understand exactly what it is they are getting with these vehicles. Speaking at the Morningstar Investment Conference in June 2016, O’Connor discussed the potential risks he sees within cap-weighted indexes and how strategic beta ETFs can offer a recipe to address them.

Exchanged-traded funds (ETFs) have grown in popularity, and there are now multitudes of cap-weighted ETFs that cover most segments of the market. The first index-based funds available to investors focused on widely recognized cap-weighted indexes such as the S&P 500 Index. As their popularity grew, other ETFs tracking other cap-weighted indices followed, offering investors an efficient, transparent way to gain broad market exposure in vehicles traded throughout the day. But do most investors really understand the portfolio exposures they bear when investing in cap-weighted index ETFs? I would argue the answer is likely no. There are some potential risks that investors in these funds may have overlooked.

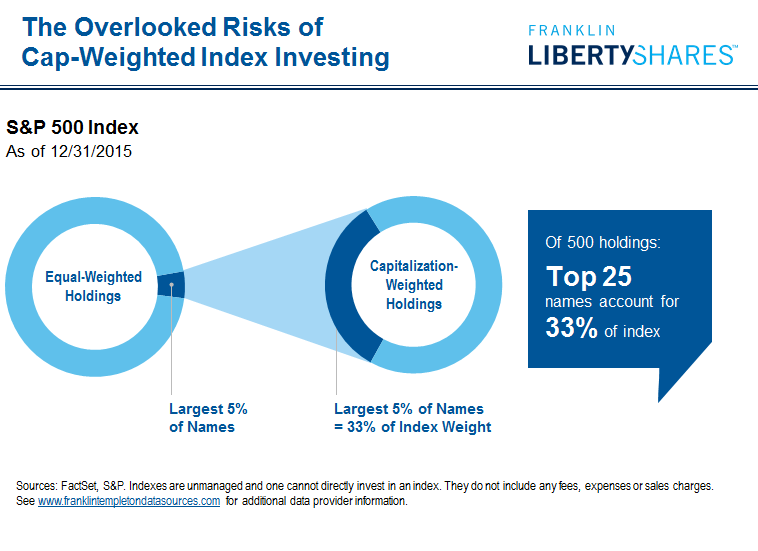

Weightings Risk

The first risk is tied to the heavy weightings that cap-weighted indices tend to have in the largest companies. Cap-weighted indexes weight stocks based on each company’s overall market capitalization, meaning the largest, highest-priced companies make up the largest portion of an index.

For example, just 5% of the holdings in the S&P 500 Index account for one-third of the index by market capitalization.1 That’s a lot to have invested in just 25 companies.

Another thing to consider is that cap-weighted indexes also increase their allocations to stocks that rise in price and reduce their allocations to those that fall in price—without consideration for whether the stocks are overvalued or undervalued, which could lead to heavier concentrations of overvalued securities.

That brings us to the next potential risk—the risk that the largest companies in the S&P 500 Index also tend to be overvalued when compared with their 10-year average price/earnings (P/E) ratio.2 According to our research taking these valuation measures into account, 70% of the 10 largest stocks in the S&P 500 Index were overvalued, as of December 31, 2015 and 56% of the top 25 stocks are overvalued, the very same ones that make up a third of the index allocation.

Why does that matter? Because the price of an overvalued stock could be poised to decline, and when the prices of the stocks that make up a large percentage of an index decline, overall portfolio performance suffers.

Geographic Risk

Some investors choose a cap-weighted index ETF for their emerging markets exposure, perhaps wrongly assuming it’s a relatively low-risk way to gain exposure to stocks that tend to be pretty volatile. The chart below takes a look at the MSCI Emerging Markets Index, which consists of stocks in 23 emerging markets worldwide. If you look a little closer at the index components, you will see that currently more than half of the index’s weight consists of stocks from just three countries—China, Taiwan and South Korea—and all three of those countries are in Asia. If any of those countries experiences a market or macroeconomic shock, a large number of stocks would likely suffer, and an investors’ overall portfolio would likely follow.

Single-Sector Risk

Finally, what could happen if a cap-weighted index becomes overweighted in a single sector? We can examine how the S&P 500 Index changed in the years leading up to the crash in the technology sector in the early 2000s. Before the prices of tech stocks ran up in the mid-1990s, technology stocks comprised about 12% of the index.3 In the three-year period between 1997 and 2000, the tech sector gained more than 300%, while the overall index was up more than 100%.

Sounds pretty good, right? By early 2000, that percentage allocation to the technology sector had ballooned to nearly 35%. We all know what happened after that. The tech bubble burst and the sector lost more than 58% of its value in a two-year period.4 The question is: What impact did this have on the overall index? The answer: It wasn’t good. Because the technology sector made up nearly 35% of the index, the implosion in that sector dragged down the performance of the overall index, so investors in a S&P 500-tracking portfolio saw losses of nearly 20% in 2000—2001 when the tech bubble burst.

The stocks included in the S&P 500 Index (or any cap-weighted index, for that matter) evolve over time as the market cap of different companies increases and decreases.

In periods of great change, the companies included in the index can change a lot. For example, from 1999 through 2003 (when the technology bubble burst), 171 stocks were added to the index, and 164 were removed. That’s pretty high turnover in a relatively short period of time. It’s even more enlightening to look at the list of stocks removed between 2001 and 2003. Nearly half of those stocks were added to the index between 1999 and 2001! You may wonder whether these stocks belonged in the index in the first place. Of course they “belonged,” because that’s how cap-weighted indexes work: They include or exclude stocks without consideration for their sector, their weight in the portfolio, or their valuation.

Enter Strategic Beta

In our view, there may be a better way to construct an index. Let’s take a look at one option that’s sometimes called “strategic beta” or “factor investing.” Strategic beta represents an alternative to market cap-weighted indexes with many different approaches

Strategic beta is based on a rules-based methodology.

- Like cap-weighted indices, strategic beta indices follow pre-defined rules that prescribe the criteria for inclusion of a stock in an index. In this way, they’re different from traditional active management in which a portfolio manager makes individual stock buy-and-sell decisions.

- Unlike cap-weighted indexes, strategic beta indexes seek to capture specific investment “factors” or market inefficiencies.

- Strategic beta indexes follow different rules from cap-weighted indexes.

- Strategic beta portfolios then seek to track a specific index.

There are many different “flavors” of strategic beta.

- The simplest strategic beta index includes all securities in equal weights. The difference is that each stock makes up the same proportion of the index, unlike the S&P 500 Index, which includes stocks by market cap.

- Some strategic beta indices focus on a single factor; these indices are designed to include only those stocks that score well based on a particular factor.

- Some strategic beta indexes combine multiple factors into a single index.

Now, what do we mean by factors? We can think of a factor as a DNA marker of stock behavior, a primary characteristic of an investment that explains a stock’s behavior over long periods of time.

Just as your DNA determines whether you’ll have blue or brown eyes, factors explain how stocks move in response to market developments.

Stocks can be grouped based on the primary factors they share. Some factors have provided investors with positive returns above and beyond market indexes over the long term—called a “return premium”—while other factors have been more closely associated with stock risk.

This DNA molecule lists four factors that are often used to understand stock performance:

- Quality

- Value

- Momentum

- Volatility

Some investors may be inclined to choose one or two factors for investments, but this approach can also come with its ups and downs. Quality, value, momentum or minimum-volatility stocks by themselves have moved in and out of favor as the economic cycle has swayed back and forth. Momentum, for example, was the top-performing factor in 2007 when equity markets were strong, but it was the worst performer in 2008 when the financial crisis hit. These swings in performance can be unsettling to many investors, causing them to sell and then miss out on rebounding performance. Finally, buying and selling individual factor investments can increase costs.

Combining multiple factors may help address the challenges of single-factor investing. First, it eliminates the need to time factors, it may lower transaction costs and because it’s diversified across factors, it may be used as a core holding.

The question then becomes what weights to assign each factor. The simplest option would be to weight the factors equally, but that approach doesn’t consider the relative importance of each factor in driving long-term performance.

As fundamental stock pickers, we at Franklin Templeton believe factor weightings should be rooted in economic rationale. Quality and Value best represent economically driven fundamentals, so we believe they should be given greater emphasis, while Momentum and Low Volatility should have less emphasis in factor allocations. This type of strategically weighted multi-factor approach can be designed to target specific portfolio exposures, which could make it an attractive core holding.5

In sum, we believe that strategic beta portfolios can help meet the needs of investors who desire alternatives to traditional cap-weighted indexes. There are a number of ways investors can employ putting strategic beta to work in their portfolios. We encourage individual investors to talk to an advisor to learn how they might replace or complement cap-weighted index funds.

Patrick O’Connor’s comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

What Are the Risks?

All investments involve risks, including possible loss of principal. Performance of the funds may vary significantly from the performance of an index, as a result of transactions costs, expenses and other factors. Indexes are unmanaged, and one cannot invest directly in an index. They do not reflect deduction of any fees or expenses. ETFs trade like stocks, fluctuate in market value and may trade at prices above or below the ETF’s net asset value. Brokerage commissions and ETF expenses will reduce returns.

1 Sources: FactSet, MSCI, as of 12/31/15. Indexes are unmanaged, and one cannot directly invest in an index. They do not include any fees, expenses or sales charges. See www.franklintempletondatasources.com for additional data provider information.

2 The price-to-earnings ratio, or P/E ratio, is an equity valuation multiple defined as market price per share divided by annual earnings per share. For an index, the P/E ratio is the weighted average of the P/E ratios of all the stocks in the index.

3 Sources: FactSet, S&P. Indexes are unmanaged, and one cannot directly invest in an index. They do not include any fees, expenses and sales charges. See www.franklintempletondatasources.com for additional data provider information.

4 Source: Ibid.

5 Diversification does not guarantee profits nor protect against risk of loss.

© Franklin Templeton Investments

© Franklin Templeton Investments