Weighing the Week Ahead: Is the Brexit Vote a Turning Point for Stocks?

This week’s economic calendar has plenty of data during a week where many will want to anticipate the long weekend. Despite these factors, most are still trying to digest the Brexit decision. There will be stories on politics, polling, history, and human interest. The economic and financial market consequences will get the most play from financial media.

Is the Brexit Decision a Market Turning Point?

Last Week

There was some significant economic news, but attention focused on Europe and the United Kingdom.

Theme Recap

In my last WTWA, I predicted that the week would be all about Brexit. Despite Yellen’s Congressional testimony, the Brexit theme was a wire-to-wire winner.

Last week’s “Final Thoughts” section was also on target, suggesting a plausible range for the week’s trading.

The Story in One Chart

I always start my personal review of the week by looking at this great chart from Doug Short. You can clearly see the early strength, based mostly on the Brexit polls, followed by Friday’s collapse. Doug has a special knack for pulling together all of the relevant information. His charts save more than a thousand words! Read his entire post where he adds analysis and several other charts providing long-term perspective.

The News

Each week I break down events into good and bad. Often there is an “ugly” and on rare occasion something really good. My working definition of “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

The Good

- Hotel occupancy continues at a near-record pace. (Calculated Risk).

- Fed stress tests were solid. Banks can $526 billion in losses under the “adverse scenario.” (MarketWatch). Bloomberg’s editors have a contrarian viewpoint.

- Existing home sales were strong. Bill McBride explains that it would have been even better if inventory were not so low. It is a complex story because baby boomers are “aging in place” and some single-family homes were converted to rentals. The numbers do not always reveal the underlying strength. And BTW, mortgage rates are near record lows. The good news was reflected in the Lennar earnings release.

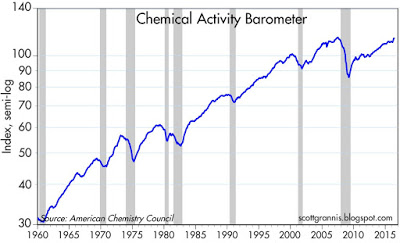

- Chemical activity is up 3% in the last three months. (Scott Grannis).

- Initial jobless claims dropped to 259K, a great reading. It is important to monitor job creation as well as job losses, so this good news is not the whole story.

The Bad

- Durable goods orders declined by 2.2%, missing expectations. Steven Hansen examines year-over-year changes in the adjusted data and arrives at a slightly better conclusion.

- Social Security financing projections got worse, exhausting the funds two years earlier than expected. D-Day is now 2028. Political leaders need to get a compromise solution in place very quickly. The longer the delay, the more difficult the solution becomes.

- Leading indicators declined 0.2% when a gain of 0.2% was expected.

- Rail Traffic continues to decline, although the rolling average is a little better. We have been following Steven Hansen’s coverage of this topic (GEI), partly because of the exhaustive analysis of past data. At some point we might see the effects of reduced coal consumption to show up.

- Michigan sentiment slightly missed expectations with a reading of 93.5. Doug Short has the best representation of the history of the series and the link between sentiment and the economy.

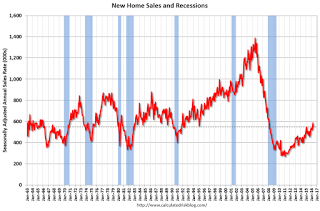

- New home sales at an annual seasonally adjusted rate of 551K missed expectations of 560K and decreased from the prior month.Calculated Risk provides a chart of the long-term results.

The Ugly

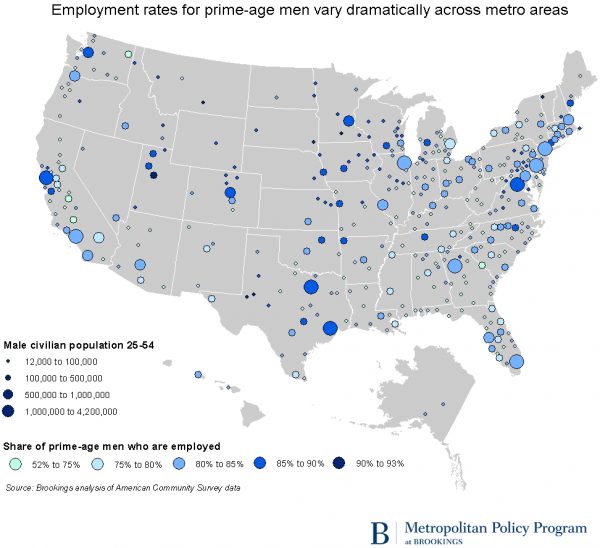

Non-working, prime-age men. With varying motives, there is a very misleading and oft-repeated “94 million people can’t find jobs.” While this is technically true, it includes grandma, teenagers, and people who prefer to study or take care of families – among others. A much better group to study is men between the ages of 25 and 54. The White House Council of Economic Advisors released a report examining the long term decline in labor force participation in this group, a trend they call “worrisome.” Various sources have provided summaries of the 50-page report and added commentary. Alan Berube (Brookings) does this nicely, including this chart of areas where the problem is greatest.

The Silver Bullet

I occasionally give the Silver Bullet award to someone who takes up an unpopular or thankless cause, doing the real work to demonstrate the facts. No award this week. Nominations are always welcome.

Noteworthy

I enjoy Pandora’s music service, often listening as I write WTWA. I have never owned the stock, but when their CEO appeared on CNBC last week I turned off the mute and TIVO’d back to watch the interview. Among other things, he discussed the potential for targeted political advertising. He stated that they could predict votes with 90% confidence using only two variables: Zip code and Pandora playlists.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react. That is the purpose of considering possible themes for the week ahead. You can make your own predictions in the comments.

The Calendar

We have a big week for economic data, with many participants edging out the door by noon on Friday. I always highlight only the most important items, helping us all to focus.

The “A” List

- The ISM Index (F). Important for those on recession watch.

- Consumer Confidence (T). Good read on employment and spending.

- Personal Income and Spending (W). Key data on consumer health.

- Auto Sales (F). Continuing strength in this private data series?

- Initial claims (Th). The best concurrent indicator for employment trends.

The “B” List

- Pending Home Sales (W). Less direct impact than new home sales, but a good read on the housing market.

- Construction Spending (F). A noisy series, but an important sector.

- Q1 GDP (T). This is the final estimate – at least until benchmark revisions. Old news, but it is what goes in the books.

- More Fed Stress Test Results (W). Which banks can increase dividends and buy back shares?

- Chicago PMI (Th). Market will watch for a hint about the ISM report.

- Crude inventories (W). Often has a significant impact on oil markets, a focal point for traders of everything.

Fed Chair Yellen is meeting with ECB President Draghi at a European forum on central banking. That should be interesting! We’ll get some additional FedSpeak later in the week.

Next Week’s Theme

With the momentous Brexit results known, it is time for the pundits to explain what it all means. Despite the daily flow of economic reports, Friday’s stage-setting selloff guarantees that attention will once again focus on Brexit. It is certainly historic, and might provide a tipping point for the UK or Europe.

While the financial media theme for the week ahead will be broader, the key point will be:

Is the Brexit result a turning point for equity markets?

As was the case last week, I read many articles on this topic, watched webinars from experts, and listened to the punditry. (As I write this, I am reminded of the best football preview program. Mrs. OldProf, who grew up in Green Bay is an enthusiastic and knowledgeable fan. She loves the show, and so do I. You have to record it in the middle of the night and watch it on Sunday morning. One of the hosts, Merril Hoge, usually says that he did “70 hours of tape study” in the prior week! The plays he selects to analyze provide some credibility for this claim).

Since I read quickly, I did not spend 70 hours on Brexit. I did read a lot more than you probably want to. In this week’s WTWA I want to cover a range of key perspectives. Read some of these links, the best and most responsible samples of each type, and draw your own conclusions. Then check out mine at the end of this post.

- Every market was rocked, or hammered – but maybe not a Lehman moment. CNBC kept running the “Markets in Chaos” subhead. The WSJ coverage was more moderate than most, but it will still worry most.

- Expect more volatility. Beware! (Oppenheimer)

- Brexit is bad for U.S. companies and corporate profits. (Barron’s)

- Expect a decline in UK GDP. Econbrowser summaries key studies.

- Expect weakness in the global economy. (The Atlantic).

- The process will lead to more uncertainty and pain. (Hale Stewart at Bonddad. Also here and here. Further thoughts from his colleague, New Deal Democrat).

- Cameron has sent the UK into a “potential investability vacuum.” (Reuters BreakingViews)

- The voting “disaster” will lead to the breakup of the UK. (Reuters BreakingViews)

- The result may affect U.S. consumer confidence and the 2016 Presidential election. (Benn Steil via GEI)

- Voter remorse from Brits who did not understand? Google searches raise the question.

Quant Corner

We follow some regular great sources and also the best insights from each week.

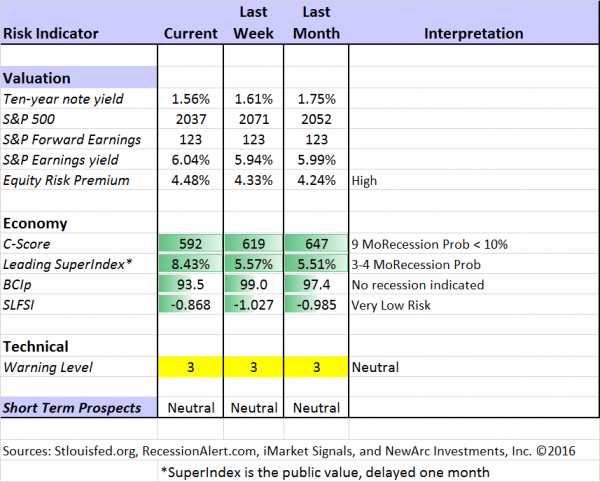

Risk Analysis

Whether you are a trader or an investor, you need to understand risk. Risk first, rewards second. I monitor many quantitative reports and highlight the best methods in this weekly update.

The Indicator Snapshot

The Featured Sources:

Brian Gilmartin: Analysis of expected earnings for the overall market as well as coverage of many individual companies. This week heexpresses more confidence about growth in earnings.

Bob Dieli: The “C Score” which is a weekly estimate of his Enhanced Aggregate Spread (the most accurate real-time recession forecasting method over the last few decades). His subscribers get Monthly reports including both an economic overview of the economy and employment.

This week the recession odds (in nine months) have nudged closer to 10%. This does not completely reflect Brexit effects, so we may get a further revision.

Holmes: Our cautious and clever watchdog, who sniffs out opportunity like a great detective, but emphasizes guarding assets.

Doug Short: The Big Four Update, the World Markets Weekend Update (and much more).

The ECRI has been dropped from our weekly update. It was not so much because of the bad call in 2011, but the stubborn adherence to this position despite plenty of evidence to the contrary. Those interested can still follow them via Doug Short and Jill Mislinski. The ECRI commentary remains relentlessly bearish despite the upturn in their own index.

Georg Vrba: The Business Cycle Indicator, and much more. Check out his site for an array of interesting methods. His latest updatedescribes the elements of the indicator we cite every week.

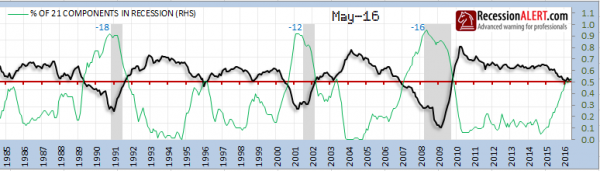

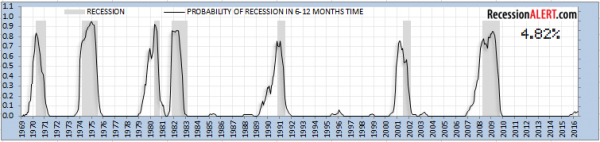

RecessionAlert: Many strong quantitative indicators for both economic and market analysis. While we feature his recession analysis, Dwaine also has a number of interesting approaches to asset allocation. Dwaine’s most recent update, U.S Economy most vulnerable to any shock since 2008, shows the recent deterioration in conditions. Read the full post, but the two charts below show the decline of the long-term leading indicators despite continuing low odds of an imminent recession.

As we review the weekly indicators it is important to maintain perspective. A 20% chance of a recession would be average. It is not a reason for fear, since it says that a recession is very unlikely. There will be a time to exercise more caution, but we are not yet close to that point.

I know that some readers have wondered whether the needle was “stuck” on these indicators. There is a temptation to tap on the gauge to see if it moves! We are seeing a little movement this week after a very quiet stretch.

How to Use WTWA

In this series I share my preparation for the coming week. I write each post as if I were speaking directly to one of my clients. For most readers, they can just “listen in.” If you are unhappy with your current investment approach, we will be happy to talk with you. I start with a specific assessment of your personal situation. There is no rush. Each client is different, so I have six different programs ranging from very conservative bond ladders to very aggressive trading programs. A key question:

Are you preserving wealth, or like most of us, do you need to create more wealth?

My objective is to help all readers, so I provide a number of free resources. Just write to info at newarc dot com. We will send whatever you request. We never share your email address with others, and send only what you seek. (Like you, we hate spam!) Free reports include the following:

- Understanding Risk – what we all should know.

- Income investing – better yield than the standard dividend portfolio, and also less risk.

- Felix and Holmes – top artificial intelligence techniques in action.

- Why 2016 could be the Year for Value Stocks – finding cheap stocks based on long-term earnings.

You can also check out my website for Tips for Individual Investors, and a discussion of the biggest market fears. (I welcome questions or suggestions for new topics.)

Best Advice for the Week Ahead

The right move often depends on your time horizon. Are you a trader or an investor?

Insight for Traders

We consider both our models and also the best advice from sources we follow.

Felix and Holmes

We continue our neutral market forecast. Felix is fully invested in fairly aggressive choices. This was good for most of the week, but bad on Friday. The more cautious Holmes is still fully invested, but fared better in Friday trading. Holmes uses a universe of nearly 1000 stocks, selected mostly by liquidity. Even when the overall market is neutral, there will often be some strong candidates. That is what we see now. It is not a resounding endorsement of the overall market, but a vote for opportunistic trading.

Top Trading Advice

Brett Steenbarger once again challenges traders. What can you learn from this?

His crisp analysis shows why it is important to be unique, and also how to do it successfully.

Dr. Brett’s Brexit advice emphasizes the difference between novice and expert traders.

Josh Brown explains how to use the VIX in your trading. There are very good results from watching VIX spikes during an uptrend. (See also Dana Lyons). Many investors take the opposite viewpoint about the “fear gauge.” Maybe that is why it works so well. Maybe it is related to what Dr. Brett is saying!

Why do traders blow out? One reason is “revenge trading.”

Insight for Investors

Investors have a longer time horizon. The best moves frequently involve taking advantage of trading volatility!

Best of the Week

If I had to pick a single most important source for investors to read, it would be this analysis from “Davidson” via Todd Sullivan. This is extremely important and worth reading carefully. Twice if you need to. He takes on the basic issue of why most analyses of value and momentum methods are wrong, introducing what he calls the 1% solution.

A key point is that value investors have great influence on markets:

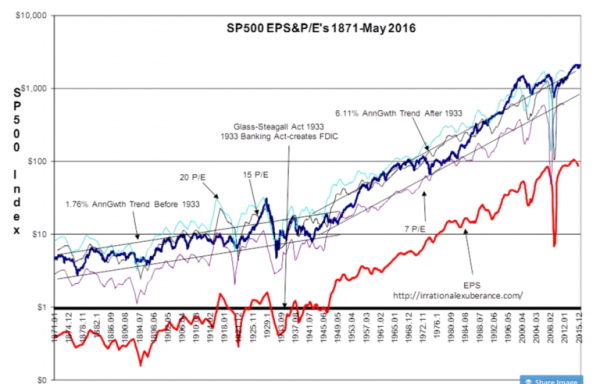

The long-term perspective reveals that SP500 Index has grown ~6.1% in line with long-term earnings. Value Investors perform contextual analysis to determine at what price they find long-term value in markets. The period 1965-1982 was a period of SP500 underperformance relative to earnings. Rising inflation caused Value Investors to contract P/E levels.

From the SP500 EPS & P/E’s 1871-May 2016 chart, it appears we may be near a market top, but Value Investors today indicate this is not the case in their experience. Explaining why Value Investors are likely to be right requires contextual analysis which many do mentally. Warren Buffett’s now famous saying, “My brain is a computer” explains why this is so.

He provides a lot of additional explanation and detail, concluding:

Be patient. Several years of economic expansion appear to be ahead of us. I expect investors to shake off the current pessimism and shift equity markets higher. Investment success relies in having realistic expectations and being grounded to fundamentals.

(At some point several years from now, the economic data should indicate that an economic correction is likely. I will then recommend an appropriate shift in strategy. But, not today!!)

[Jeff] This is very strong and exactly right for investors.

Stock Ideas

Airlines benefiting from Brexit? Raymond James provides some ideas. (via Barron’s)

Ben Levisohn asks, Biotech: Buy the Brexit Blowup? His sources suggest that the selling greatly exaggerates the actual impact on many stocks. Check it out for specific ideas.

How about diversifying by strategy rather than by allocation? Michael Batnick explains how this can both improve returns while reducing risk. (Holmes is vigorously wagging his tail in agreement).

Tesla. Really? Every big firm hates the deal to buy Solar City and has downgraded the stock. One contrarian source likes the underlying numbers and notes the potential that the deal would be withdrawn. That was our thinking when we initiated a small option position. This is the kind of situation that can provide a great risk/reward ratio, but not by just buying the stock.

The Hardest Question: When to Sell

Chuck Carnevale wisely notes:

The most common complaint that I have heard from investors over my 40+ years in the financial services industry is as follows: “Everyone wants to tell me what to buy and when, but no one ever tells me when to sell.”

Hint #1: Do not sell just because the price drops.

Hint #2: Keep the stock’s fair value in mind.

Read the full post for plenty of helpful analysis and examples.

Personal Finance

Professional investors and traders have been making Abnormal Returns a daily stop for over ten years. The average investor should make time (even if not able to read AR every day as I do) for a weekly trip on Wednesday. Tadas always has first-rate links for investors in hisweekly special edition. There are always several great choices worth reading, but my favorite this week is Morgan Housel with (yet another) great piece. It is aimed at new grads (although nearly everyone could benefit). He asks various sources for their best advice in five words. There are plenty of good ideas here, even though he allows four more words of advice than Dustin Hoffman got.

What would I say? How about: Don’t spend all at once. Well that was what my son calls “dad humor.”

My own father had great advice, and it did not take five words: Always think of tomorrow.

Runner up? This analysis of the 30-year mortgage, which might cost buyers an extra $100,000 or so, just so they can reach for more than they can afford.

Doing your own work?

If you are a serious individual investor making your own decisions, you should monitor your stocks via Seeking Alpha’s excellent transcript service. You can also get a lot of information from Avondale Asset Management’s weekly summary.

Final Thoughts

There is an important distinction among various Brexit effects: politics, history, economics, and markets. If we were sitting down for a cup of coffee or a beer, I would discuss any of them. As investors we should be mainly concerned with the last, and perhaps a bit with the economic effects.

That will be my focus.

The Path Mattered

The five-day path to the final decision was very important. The range of the week’s trading was within the +/- 2% we cited last week. The week started with a rally when markets mistakenly thought that the “remain” vote would prevail. When the opposite occurred, the market gave that gain back and declined another 1.3% or so. Everything was within the range that we expected.

- If you kept this in mind, the big selling on Friday was not a surprise.

- The path set up a big news event – markets in chaos, stocks slammed, Brexit threatens world economy, etc. Suppose that the vote had been on Monday, before the run-up. A decline of 1.3% would have been a relatively normal reaction to some negative news – not a catastrophe.

- The psychology is in place. The weekend news coverage will frighten individual investors, probably leading to a weak day on Monday.

Most Fears Are Speculative

The measurable effects are all modest.

The biggest negative impacts all relate to speculation about the effect of uncertainty.

Investment Implications

As is often the case, the best risk/reward for investors is contrarian.

- Allow markets to digest the Brexit information and don’t panic; (Morgan Housel and also MarketWatch)

- Ignore those pitching a personal, political, or product agenda;

- Emphasize quantitative fundamentals. Earnings impacts may be exaggerated; (Brian Gilmartin)

- Choose value stocks;

- Do not overreact to headlines calculated to sell advertising; (Chuck Jaffe, MarketWatch) and finally

- As I noted last week, this may not be the final chapter. (Bloomberg)

Read these sources carefully and contrast with the more speculative fears.

The most difficult thing for most investors is to “stay the course” in the face of frightening news and incessant recession predictions. It is also the most rewarding.