A Classic Case of Failed Socialism: What’s Next After the Brexit?

Defying sentiment polls leading up to yesterday’s historic Brexit referendum, British voters said “thanks, but no thanks” to excessive EU taxation and regulation, choosing to take back Britain’s sovereignty in financing, budgeting, immigration policy and other areas essential to a nation’s self-identity. It was a momentous victory for the “leave” camp, led by former London mayor Boris Johnson and U.K. Independence Party leader Nigel Farage, who invoked the 1990s sci-fi action film “Independence Day” by declaring June 23 “our independence day” from foreign rule.

As I’ve been saying the last couple of weeks, British citizens and businesses have grown fed up with an avalanche of failed socialist rules and regulations from Brussels, responsible for bringing growth and innovation to a grinding halt. Even if the referendum had gone the other way, it should still have served as a wake-up call to the European Union’s unelected bureaucratic dictators. Euroscepticism and populist movements are gathering momentum in EU countries from Italy to France to Sweden, and last week, fiercely independent Switzerland, which voted against joining the EU in the 1990s, finally yanked its membership application for good.

American voters should be paying attention. Many have already pointed out the parallels between the Brexit movement and Donald Trump’s populist campaign for president. This connection was not lost on Trump, who tweeted early Friday morning: “They took their country back, just like we will take America back.”

Britain’s decision to leave exposes the fragility of trade right now and mounting apprehension toward globalization. The EU is mired in tepid growth, and the blame cannot be pinned on immigrants, as some have tried to do. Instead, Brussels’ policies are anti-growth. Moore’s Law says the number of transistors in a microchip doubles every two years. That’s just a fact. American entrepreneurs embrace and indeed push the limits of technological innovation, but “Eurocrats,” to a large extent, seem to be in open opposition to it. This is why many large, successful American tech firms such as Facebook and Google are treated with such hostility in Europe. The bureaucrats are so against growth and prosperity, it wouldn’t surprise me if they tried to do away with Moore’s Law.

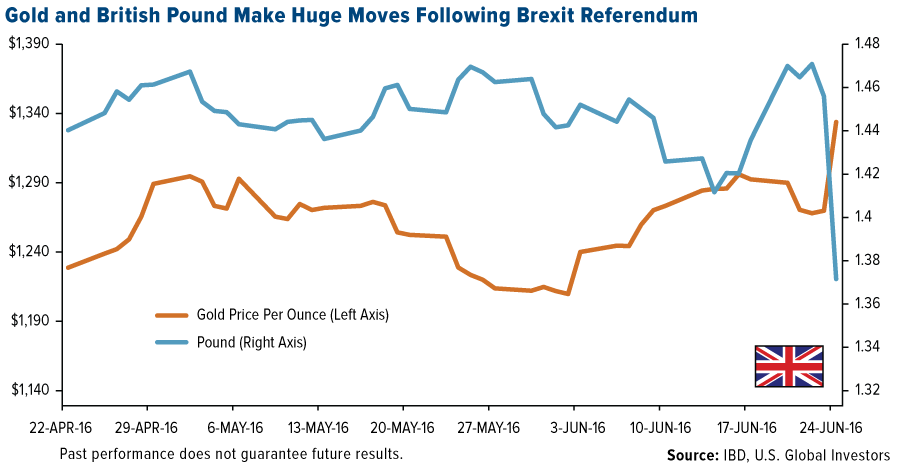

A Legendary Day for Gold

Immediately after results were announced, the British pound sterling, one of the world’s reserve currencies, collapsed spectacularly against the dollar, plunging to levels not seen since Margaret Thatcher’s administration. The euro, the world’s only fiat currency without a country, fell more than 2 percent.

Gold, meanwhile, screamed past $1,300 an ounce to hit a two-year high, proving again that the yellow metal is sound money and fervently sought by investors worldwide as a safe haven during times of economic and political uncertainty.

Uncertainty is indeed the order of the day. As the World Gold Council (WGC) put it today, “It is difficult to find an event to compare this to.” Trading blocs have fractured before, but none as large and significant as the EU. As the world’s fourth most liquid currency, gold saw massive trading volumes. At the Shanghai Gold Exchange, an all-time record amount of gold was traded following the Brexit—the equivalent of 143 tonnes in all.

“We expect to see strong and sustained inflows into the gold market, driven by the intense market uncertainty that now faces the global markets,” the WGC wrote.

The Brexit lifted not just bullion but gold stocks as well, with many of them climbing to fresh highs. Shares of Barrick Gold shot up 10 percent in early-morning trading while Yamana Gold and Newmont Mining both saw gains of over 8 percent

I’ve always advocated a 10 percent weighting in gold—5 percent in physical gold, 5 percent in gold stocks—with rebalancing done on a quarterly basis. Gold is now up at least one standard deviation for the 60-day period, meaning now might be a good time to take some profits and rebalance. It’s been a spectacular six months!

So What Happens Now?

As I said, global growth is unstable, especially in the EU, and the Brexit will only add to the instability. This will likely continue to be the case in the short and intermediate terms as markets digest the implications of the U.K.’s historic exit.

It should be noted that the country will remain a member of the EU for two more years, during which time the nature of the relationship following the official divorce can be negotiated. These negotiations will take place without David Cameron, who unexpectedly announced early this morning that he was stepping down as prime minister.

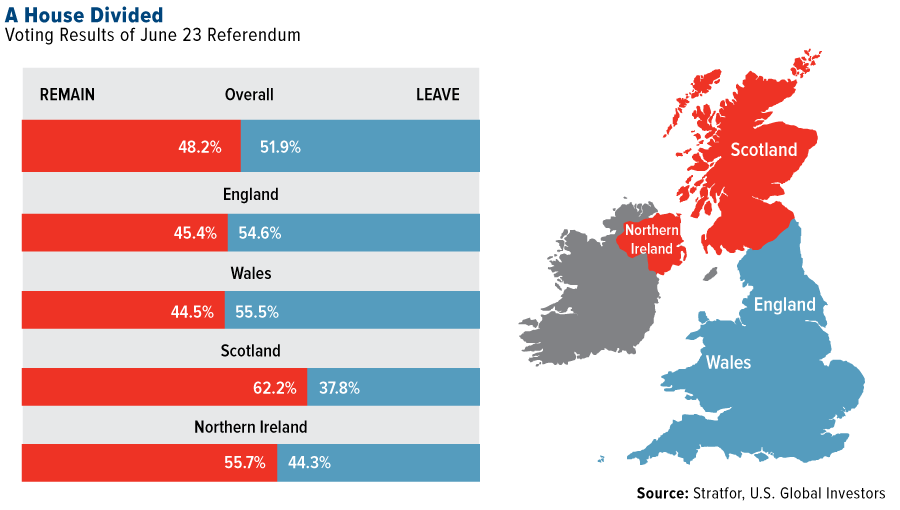

The results of the referendum also call into question the unity of the kingdom itself. England and Wales both voted to leave the European bloc while Scotland and Northern Ireland were aligned in their desire to remain members

|

|

Reacting to the outcome, Nicola Sturgeon, the First Minister of Scotland and leader of the Scottish National Party, said the people of Scotland see their future “as part of the European Union.” A second attempt at pulling out of the U.K., then, seems likely. In September 2014, you might remember, a referendum to quit the United Kingdom failed. Northern Ireland will become the only part of the U.K. to share a land border with an EU country (the Republic of Ireland), and it’s unclear at the moment whether a physical border, complete with passport control checks, will need to be erected.

In the meantime, it’s important to “keep calm and invest on.” We should expect volatility in the short term, but the global selloff might be a good opportunity to nibble at stocks that could rally once the initial shock has subsided.

For investors looking to minimize the volatility, short-term, tax-free municipal bonds continue to be attractive on global negative interest rates and falling currencies. Muni bond funds have seen inflows of more than $30 billion this year alone, with the week ended June 22 seeing the highest inflows in over three years at $1.4 billion.

Explore the $3.7 trillion muni market.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost -1.56 percent. The S&P 500 Stock Index lost -1.64 percent, while the Nasdaq Composite fell -1.92 percent. The Russell 2000 small capitalization index lost -1.50 percent this week.

- The Hang Seng Composite gained 0.28 percent this week; while Taiwan was down -1.06 percent and the KOSPI fell -1.44 percent.

- The 10-year Treasury bond yield fell 4 basis points to 1.56 percent.

Domestic Equity Market

Strengths

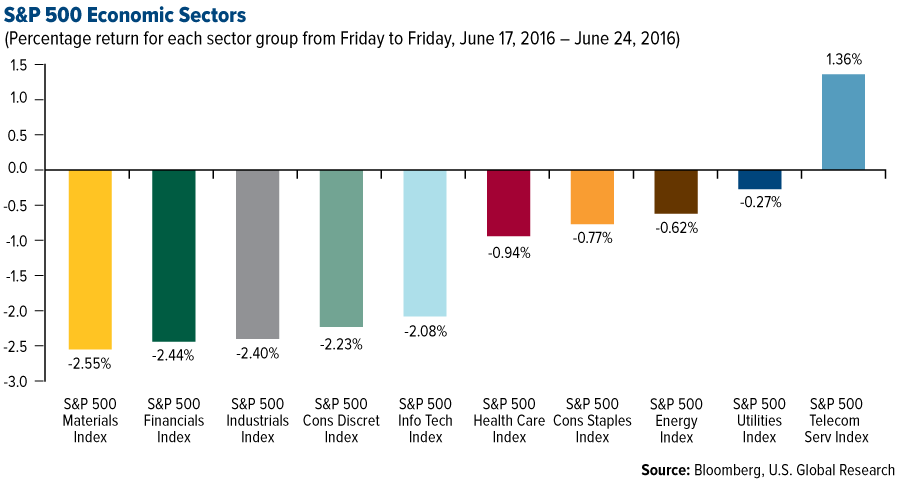

- Telecommunication services was the only positive sector on Friday after Brexit and was also the best performing sector for the week, increasing by 1.36 percent.

- Marathon Oil Corp was the best performing stock for the week, increasing 11.47 percent. Marathon Oil acquisition of PayRock Energy was perceived positively by the market as it will improve the quality of its asset base. Morgan Stanley upgraded Marathon Oil to overweight from equal weight after the announcement.

- Consumer confidence climbed to the highest point since mid-March as Americans grew more optimistic about the economy, personal finances and the buying climate, according to the weekly Bloomberg Consumer Comfort Index released Thursday. Bloomberg Consumer Comfort Index increased to 44.2 for the period ended June 19 from 42.1 in the prior week, the largest increase since January 2015.

Weaknesses

- Materials was the worst performing sector for the week, decreasing by -2.55 percent. Industrial metal weighed on materials, but precious metals caught a bid in the risk-off atmosphere.

- Wynn Resorts was the worst performing stock for the week, falling -10.34 percent. It was an exceptionally soft week in Macau with average daily gaming revenues falling 22 percent week-over-week with the distraction of the Euro 2016 soccer tournament. According to Nomura, gaming revenues tracked down 7-11 percent in June year-over-year vs forecast of flat.

- The International Monetary Fund (IMF) cut its growth forecast for U.S. The IMF said the U.S. economy will grow 2.2 percent this year, less than its projection of 2.4 percent in April. The fund left unchanged its forecast for a 2.5 percent expansion in 2017. There’s a clear case for the Fed to proceed on a "very gradual" path in raising its benchmark rate, the IMF said in a statement Wednesday after concluding its annual assessment of the world’s biggest economy.

Opportunities

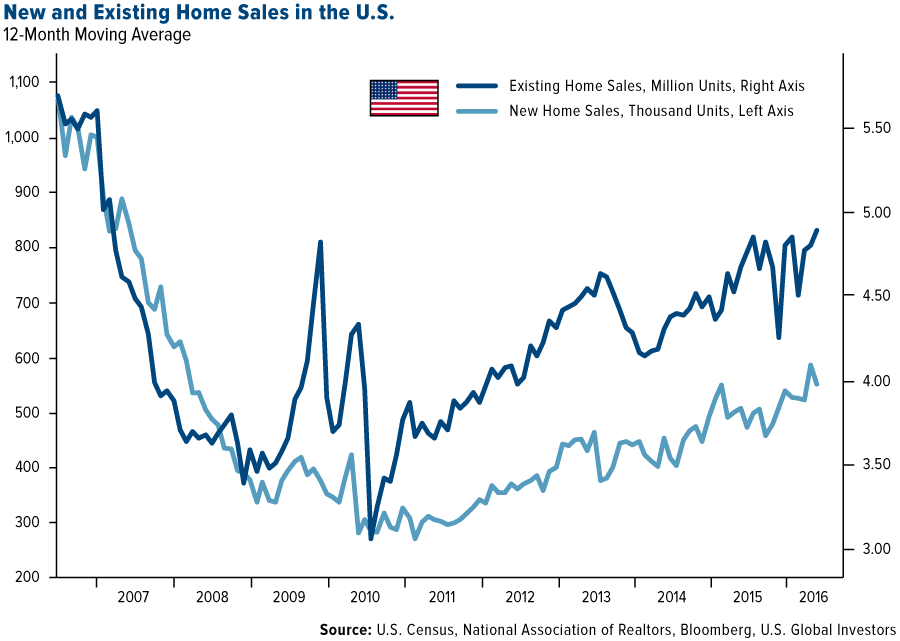

- Existing home sales increased 1.8 percent month-over-month in May from the prior month to a seasonally adjusted annual rate of 5.53 million, the National Association of Realtors (NAR) said on Wednesday. That was the strongest pace since February 2007. NAR flagged support from low rates and accumulated equity (driving trade-ups). The number of new homes sold fell -6 percent in May, better than the -9.5 percent slump anticipated by economists polled by Bloomberg. The rejuvenated housing market has provided a boost to the economy, helping offset a slowdown in business spending and a downturn in the energy sector.

- Drug and biotechnology stocks surged Wednesday after the U.S. government said a cost-cutting mechanism created under Obamacare, known as the Independent Payment Advisory Board, or IPAB, will likely be triggered in 2017, not this year as some investors had feared. Evercore ISI also pointed out that if IPAB were implemented next year, 2019 would still be the earliest we could see reforms. Goldman noted IPAB may be a non-issue for several years.

- Initial jobless claims fell to 259,000 for the week ending June 18, down from the prior week’s 277,000 level and better than consensus for 270,000. This data continue to point to a healthy and stable labor market.

Threats

- The Wall Street Journal pointed out S&P 500 buybacks hit $1614.4 billion in the first quarter, up 12 percent year-over-year and the second-highest on record. The Journal also noted that for the 12 months ended March 2016, S&P 500 companies spent a record $589.4 billion on buybacks. In terms of buyback support, the paper highlighted the usual suspects such as record cash levels, low borrowing rates and activist pressure. Limited organic growth opportunities have been flagged as another driver. The paper also noted widely discussed buyback backlash driven by concerns that an unwillingness to boost capex threatens future growth and productivity.

- Orders for U.S. capital goods unexpectedly fell 0.7 percent May, the most in three months, pointing to weakness in investment even before the likely damage to confidence stemming from U.K. voters’ decision to leave the European Union.

- Global risk assets were under pressure on Friday after Britain voted to leave the EU by 51.9 percent to 48.1 percent. U.S. stock market was down as well in the wake of the U.K.’s decision to secede from the European Union. UBS Group AG sees up to $150 billion selling should equity volatility persist in the S&P 500 Index for the next week, especially by quantitative traders who make buy and sell decisions based on price trends.

The Economy and Bond Market

Strengths

- The Markit U.S. Manufacturing PMI beat expectations this week. An actual print of 51.4 beat analysts’ expectations for a rise from 50.7 to 50.9.

- Treasuries rose for the week along with demand for other safe-haven assets. In addition to Treasuries, and particularly on Friday, investors flocked to trusted assets like the U.S. dollar, Japanese yen, German bunds and of course gold.

- Initial jobless claims in the U.S. came in better than anticipated at 259,000, ahead of expectations for 270,000.

Weaknesses

- Brexit, Brexit, Brexit. For many investors today, no matter how much strong coffee they might have sipped with their “Brexit” tacos in the wee hours of the morning, it still seemed like some sort of bad dream. Others remain more sanguine. Regardless, markets were caught wrong-footed, and in any case, sizeable (but hardly insurmountable) challenges lie ahead for the U.K. and EU.

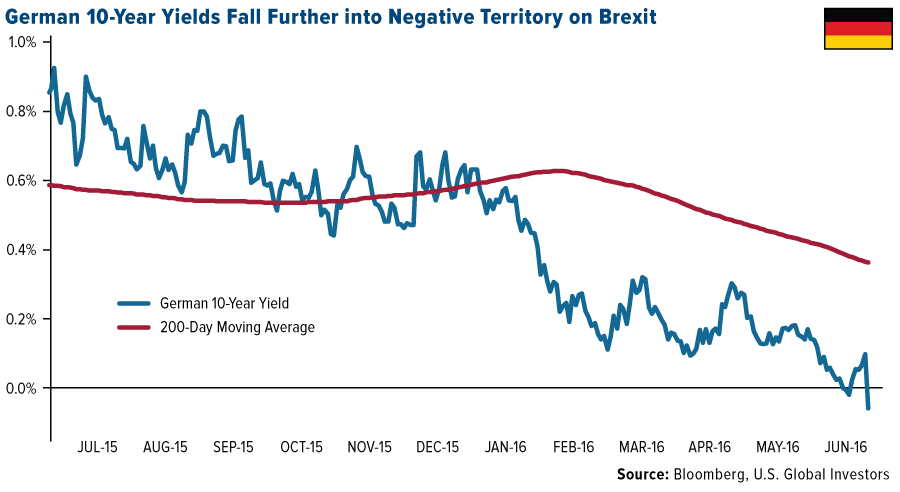

- Yields on safe-haven German 10-year bunds declined once again into negative territory, falling on Friday as low as -0.17 percent before recovering to close negative at about -0.05 percent.

- Many Japanese exports declined for another consecutive month, with shipments to China, Europe and the U.S. all coming in lower.

Opportunities

- Within U.S. economic policy, a potentially more accommodative Federal Reserve may well help to bolster demand for yield. Expectations for a July hike are now literally zero—economists are instead giving a 10 percent chance to a cut! Brexit fears and fallout now threaten to delay additional hikes even further, with many economists now suggesting the U.S. may not hike rates again until early 2017. Globally, uncertainty about forthcoming fiscal and monetary economic policies, foreign exchange markets and rates, and slower global growth may also help the search for quality yield and safety.

- Moody’s affirmed the EU’s Aaa rating and stable outlook on Friday following the Brexit results.

- Bloomberg reports that even prior to the U.K.’s vote to leave the EU, U.S. state and local-government bond funds had already seen cash inflows accelerate. This week marks the 38th-straight week of inflows to muni funds.

Threats

- The potential for missteps in central banking policies globally remains an ongoing wildcard.

- High levels of volatility in foreign exchange markets may well force central bankers’ hands and lead them to intervene to protect their currency ranges. Friday’s violent price action and significant volatility prompted a series of statements from the likes of the Bank of Japan, Bank of England and European Central Bank, among others.

- What clever-but-ominous-sounding portmanteaus can you coin? We’re all familiar now with Brexit, and of course Brexit’s scary predecessor, Grexit. So too you may have heard dark, intimidating whispers of Nexit or Frexit—but surely among our new favorites are the words Departugal, Oustria and Italeave, among others. Test out your own fear-mongering creativity!

Gold Market

This week spot gold closed at $1,316.72 up $17.72 per ounce, or 1.36 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, gained 4.25 percent. Junior miners underperformed seniors for the week as the S&P/TSX Venture Index traded off 0.64 percent. The U.S. Trade-Weighted Dollar Index jumped higher with a 1.38 percent gain.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

|

Jun-21 |

Germany ZEW Survey Current Situation |

53.0 |

54.5 |

53.1 |

|

Jun-21 |

Germany ZEW Survey Expectations |

4.8 |

19.2 |

6.4 |

|

Jun-23 |

U.S. Initial Jobless Claims |

270k |

259k |

277k |

|

Jun-23 |

U.S. New Home Sales |

560k |

551k |

586.k |

|

Jun-24 |

U.S. Durable Goods Orders |

-0.5% |

-2.2% |

3.3% |

|

Jun-27 |

Hong Kong Export YoY |

-2.0% |

-- |

-2.3% |

|

Jun-28 |

U.S. GDP Annualized QoQ |

1.0% |

-- |

0.8% |

|

Jun-28 |

U.S. Consumer Confidence Index |

93.4 |

-- |

92.6 |

|

Jun-29 |

Germany CPI YoY |

0.3% |

-- |

0.1% |

|

Jun-30 |

Eurozone CPI YoY |

0.8% |

-- |

0.8% |

|

Jun-30 |

U.S. Initial Jobless Claims |

267k |

-- |

259k |

|

Jun-30 |

Caixin China PMI Mfg |

49.1 |

-- |

49.2 |

|

Jul-1 |

U.S. ISM Manufacturing |

51.4 |

-- |

51.3 |

Strengths

- The best performing precious metal for the week was palladium, rising 2.24 percent. Palladium surged early in the week, doing just the opposite of gold, when polls indicated British voters were more likely to vote “remain” in the Brexit referendum, thus economic uncertainty would be maintained.

- However, the palladium price dropped on Friday as gold soared to a two-year high following the U.K.’s vote to exit the European Union, boosting haven demand. According to Bloomberg, U.K. voters backed leaving the EU by 52 percent to 48 percent, causing turmoil across markets and prompting Prime Minister David Cameron to resign.

- Gold dealers in London say they have never seen anything like it, describing the rush from consumers to sell gold, and many more to buy the precious metal following the U.K.’s vote to exit the EU. “We’re doing 10 times the business we normally do,” said Michael Cooper, commercial director of ATS Bullion Ltd. BullionVault saw its busiest day ever on Friday, reports Bloomberg.

Weaknesses

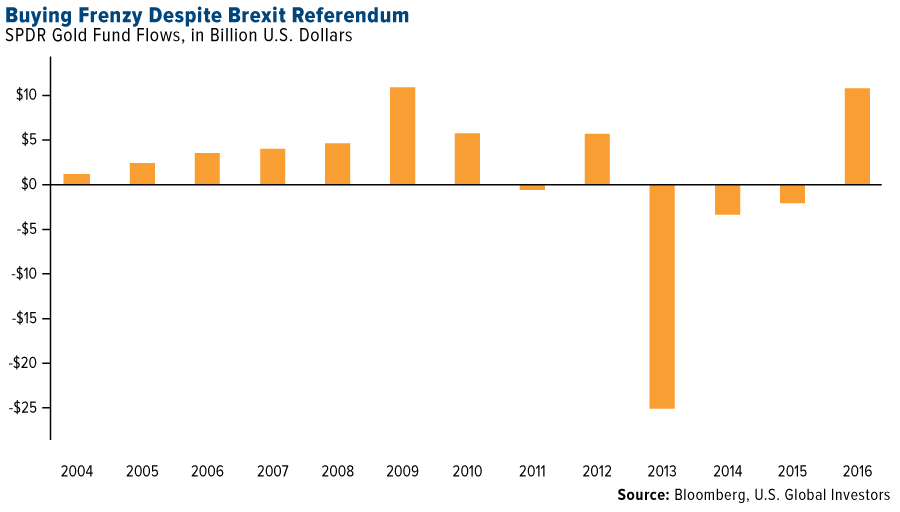

- Despite the surge in gold prices on Friday following the U.K. vote, it was the worst performing precious metal for the week, although still up 1.43 percent. Gold backed ETFs have seen a surge in assets this year as investors have started to discount that political leaders at the central banks around the world have lost their mojo, as you can see in the chart below.

- Gold experienced weakness most of the week, falling for the first four days of the week as polls on the Brexit referendum showed uneven results. Gold tumbled by the most in almost a month as other polls on Monday showed voters tilting toward remaining in the EU.

- Kinross Gold Corp. temporarily halted mining at its Tasiast mine in Mauritania, reports Bloomberg, after the Ministry of Labor banned some of its expatriate workers from the site due to invalid work permits. The stoppage comes a week after a three-week strike by unionized workers ended at the mine, one Seeking Alpha article points out.

Opportunities

- According to the median of 12 forecasts in a Bloomberg survey of analysts and traders from New York to Canada, gold prices could reach as high as $1,424 an ounce by year end, reports Bloomberg. “The Brexit referendum lowered the probability for an interest rate hike,” said commodity analyst Thorsten Proettel. Low rates are a boon to gold because it increases the metal’s appeal as a store of value, the article continues..

- Capital spending by gold producers has been decimated, writes Sean Gilmartin at Bloomberg, which will lead to a long-term decline in the mine supply of the metal. According to UBS, high quality gold equities still offer attractive leverage to gold price upside, and will outperform physical gold in a rising price environment. Other opportunities for the metal come in the mergers and acquisitions space, reports the Financial Review, particularly in the West African-focused gold space driven by strong acquirers out of North America. In an all-share deal, Teranga Gold made an offer to buy Gryphon Minerals, boosting its share price by 22 percent on the news.

- Hartley’s reports on Burey Gold Limited this week, noting the company’s release of significant drilling results from its maiden RC drilling program in the northern zone of its Giro project. Highlights include 2 meters at 196 grams per ton from 12 meters, and 15 meters at 255.6 grams per ton from 15 meters. Additional results include 33 meters at 6.1 grams per ton from surface and 12 meters at 21.2 grams per ton from 3 meters. Hartley’s writes “These results confirm our opinion that the Giro project has potential to define a company-making asset particularly given these significant high grade results.”

Threats

- Physical demand for gold out of both India and China was tepid during the first half of the year, reports Bloomberg. Demand was historically weak in India, with the discount averaging $25 an ounce in 1H versus $8 a year ago. Also contributing to the overall weakness was a poor farming year in India, continues the article, yielding less disposable income for Indians to buy gold.

- Although a vote for Brexit will benefit gold, reports SocGen, other commodities such as copper and oil could suffer. Mark Keenan, SocGen Asia head of commodities, points out that a rising U.S. dollar will depress metals such as copper, and risk aversion may hurt oil.

- In a note from Sovereign Man this week, the author reflects on how much has changed since the publication started seven years ago. He points out that U.S. government debt soared 70 percent, that the Federal Reserve’s balance sheet more than doubled, and that the U.S. government has been caught red-handed spying on everyone – all in seven years’ time. “We’ve seen an appalling rise in police violence and Civil Asset Forfeiture to the point that the U.S. government now steals more than every thief in America combined,” he continues. Perhaps Donald Trump is right in that Mexico will pay to build a wall on its northern border, which is to keep Americans from crossing illegally into Mexico.

Energy and Natural Resources Market

Strengths

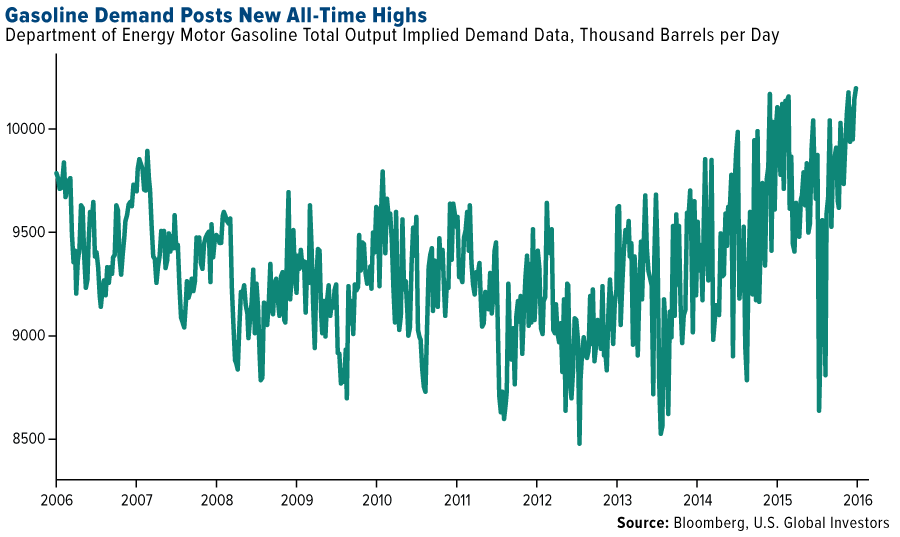

- Gasoline demand rises to all time high. The Energy Information Administration (EIA) said domestic gasoline consumption hit a record high of 9.81 million barrels per day last week, incentivizing refiners to buy more crude and turn it into gasoline.

- The best performing sector for the week was the NYSE Arca Gold Miners Index. The index rose 4.5 percent for the week, tracking gold’s gains after investors sought safety following a surprise UK vote to leave the EU.

- The best performing stock in the broader natural resources sector was UPM-Kymmene OYJ. The Finnish paper and forest products company rose 8.6 percent for the week after The District Court of Helsinki ruled in favor of the company, resolving a case brought forward by the Finnish Forest and Parks Service.

Weaknesses

- Railway volumes continue to disappoint. Canadian rails published even weaker than expected second-quarter volumes this week, leading to a negative revision to earnings per share (EPS) forecasts. With no visible pick up in coal and oil loadings, the one area of strength for the Canadian rails has been intermodal. However, in recent months intermodal carloads have turned negative, which is cause for concern given intermodal is often viewed as an indicator of the broader economy.

- The worst performing sector for the week was the S&P 500 Fertilizers & Agricultural Chemicals Index. The index dropped 4.8 percent for the week as investors fear the Monsanto acquisition by Bayer may be at risk of not being completed, now that British pound and the Euro have dropped in value vis-à-vis the U.S. dollar.

- The worst performing stock in the S&P Global Natural Resources Index was CF Industries Holdings Inc. The agricultural chemicals company dropped 10.2 percent for the week as investors fear the company may be forced to write down the value of its chemicals’ facilities in the UK following the collapse in the British pound after the “Brexit” vote results were announced.

Opportunities

- The new Saudi oil minister, Khalid Al-Falih, says the oil glut is over. “We see a balanced market, we see supply and demand converging. We may have started inventory drawdowns that will continue for the foreseeable future,” said the minister. The facts support his views; despite near record production, the kingdom’s oil inventories have declined for a record six consecutive months.

- Utilities may continue to outperform after reaching all-time highs. The S&P 500 Utility Index hit a record high this Friday in a bid to safety after the UK referendum. However, the sector may continue to outperform as lower, rather than higher rates, appear in the horizon now that central banks have to mitigate negative consequences of the “Brexit.”

- Indian demand for gold may surge following RBI Governor Raghuram Rajan’s departure. The surprise decision by Rajan to return to academic life following the end of his term this September is negative for Indian investors. However, according to CLSA’s Christopher Wood, the news is very positive for gold demand, which has been declining recently precisely because of Rajan’s focus on increasing real interest rates.

Threats

- The iron ore market will take longer to balance, according to BHP Chief Executive Officer Andrew Mackenzie. Excess supply may take a decade to be absorbed after a boom, in which low-cost miners including BHP, Rio and Fortescue ramped up output just as growth cooled in China.

- Rules on Chinese outbound mergers and acquisitions may be tightened. China's appetite for overseas acquisitions, especially in the natural resources sector, has already outgrown last year's record. However, that may be about to change as China's leaders attempt to curb the outflow of its foreign reserves, which dropped more than half a trillion dollars last year. Lawyers say the State Administration of Foreign Exchange (SAFE), the custodian of the country's $3.19 trillion reserves, is anxious that the deal outflows could weigh on the yuan currency.

- China’s demand for oil and refined products may be faltering. Domestic diesel consumption fell 8.6 percent from a year ago in April, while refiners ran at the fastest daily rate on record. As a result, China’s diesel exports increased to a record in May as easing demand forced refiners to send surplus fuel overseas.

China Region

Strengths

- Despite the week’s late volatility, Hong Kong’s Hang Seng Composite Index actually finished the week higher with a 0.67 percent total return, ahead of its regional peers.

- Private wealth in the Asia-Pacific region surpassed that of North America for the first time last year, fueled by stronger economies and real estate markets, according to a Cap Gemini SA report. Millionaires’ assets in Asia-Pacific countries surged almost 10 percent to $17.4 trillion, outstripping North America’s $16.6 trillion.

- Chinese watch retailer Hangdeli Holdings Ltd. (3389 HK) was a top gainer in the HSCI for the week, rising nearly 18 percent even as the company offered to pay cash to purchase up to $175 million of its outstanding senior debt.

Weaknesses

- China home prices for the May period rose in only 60 major cities, down from 65 in April.

- HSCI constituent and health care provider Harmonicare Medical Holdings fell nearly 16 percent for the week, putting in new 52-week lows and suffering a downgrade from Morgan Stanley.

- All regional currencies outside of the Hong Kong dollar finished down for the week, led lower by the South Korean and the Philippine peso. The Japanese yen—a safe haven—surged to just shy of the 99 level in Friday trading before retreating back above 102. The Nikkei was pummeled, dropping nearly 8 percent on Friday.

Opportunities

- Citing a “person with knowledge on the matter,” Bloomberg reports that Tesla Motors is eyeing Shanghai to become the company’s production base in China – an investment potentially worth around $9 billion. Jinqiao Group, a government-owned company in Shanghai, signed a non-binding memorandum of understanding with Tesla, according to the unnamed source.

- During the first five months of 2016, Hong Kong remains the world’s leader in the IPO market, reports the South China Morning Post, in terms of funds raised and number of listings. Despite recent market volatility over economic uncertainties in mainland China, this news could bolster Hong Kong’s status as a key global player in the near future, continues the article.

- As the European Championship kicked off this month, a popular sports season has been ignited, reports the South China Morning Post, sparking fund inflows into the sports sector. “The European Championship has marked the start of a sports feast this summer, followed by the Chinese Super League, the Olympics, and the qualification games for the 2018 FIFA World Cup in Asia,” said Lin Juan, an analyst for Ping An Securities.

Threats

- Minutes from the Bank of Japan’s April policy meeting show that several policymakers are worried that overseas economies continue to pose downside risks to Japan’s economy and prices, reports Reuters. These members urged the central bank to pay close attention to these risks, and “ease monetary policy without hesitation” if needed in the future.

- In the second quarter, Apple reported a 26 percent sales slide in greater China (which includes Hong Kong and Taiwan), reports the Wall Street Journal, accounting for more than half of its first quarterly revenue decline in over a decade. A municipal tribunal’s injunction made public last week, barring the sale of the iPhone 6 and 6 Plus in Beijing, could hurt the company further. The case against Apple was brought on by Shenzhen Baili (which appears to be another name for smartphone startup Digione), and is a reminder that “no amount of corporate diplomacy is likely to soften Beijing’s hostility toward foreign companies,” the article continues.

- Chinese banks witnessed a 47 percent drop in net foreign exchange transactions from April to May, according to official data released early this week. China Daily reports that the amount has narrowed from $23.7 billion in April to $12.5 billion in May, suggesting the pressure of capital outflow is easing. Concerns over capital outflow have risen as the economy slows and the Chinese currency has dropped.

Emerging Europe

Strengths

- Russia was the best performing country this week, gaining 20 basis points. Vladimir Putin wants the West and the eurozone to be weak, and the U.K. vote to leave the EU works in his favor. Europe will have to concentrate more on its own problems and may pay less attention to Russia. In Moscow, some analysts said the Brexit would be seen not as a tragedy but as a major opportunity..

- The Ukrainian hryvnia was the best performing currency this week, gaining 3 basis points against the U.S. dollar. The currency was the least affected by the Brexit announcement. The central bank lowered its key policy rate to 16.5 percent from 18 percent, while most Bloomberg analysts predicted a cut to 17 percent. Inflation continues to ease and the hryvnia reached its strongest level since January.

- Health care was the best performing sector among Eastern European markets this week.

Weaknesses

- Greece was the worst performing market this week, losing 9 percent. Greece is a high beta market, declining and/or rising more than the broader market. Banks were hit the hardest, losing about 30 percent in the past five trading days.

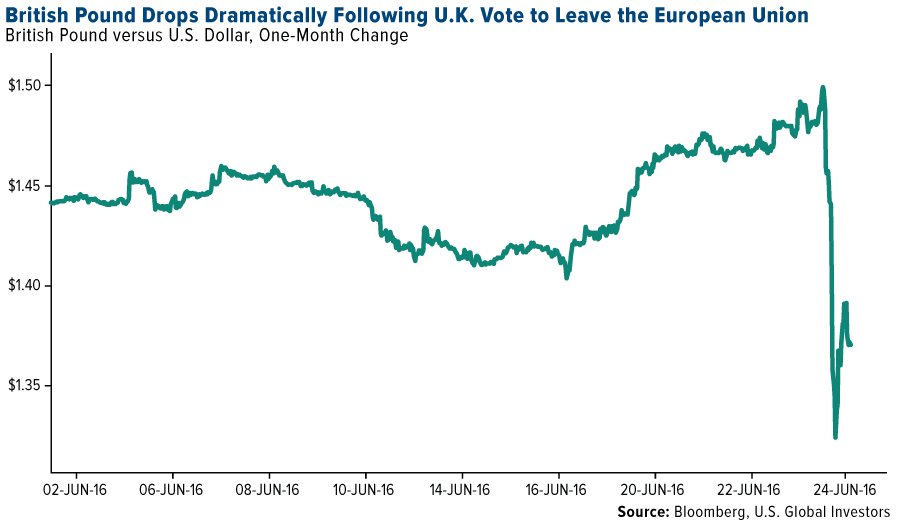

- The Hungarian forint and the Polish zloty were the worst performing currencies this week in Emerging Europe, losing more than 2 percent each against the U.S. dollar. Poland and Hungary are the biggest beneficiaries of EU finding. Future EU findings could decline with the Brexit announcement. Markets and currencies were affected by a sharp selloff in the British pound. The chart below shows the British pound price change against the U.S. dollar over the past month.

- The financial sector was the worst performing sector among Eastern European markets this week.

Opportunities

- The European Central Bank (ECB) agreed to make Greek bonds eligible for collateral, allowing the country’s lenders to access cheaper refinancing. Greek lenders can now pledge the nation’s junk-rated debt against regular central-bank funding. The ECB will examine the possibility for Greek bonds to participate in its asset-purchase plan at a later stage.

- Russian bonds have come into favor this month as the central bank cut its main interest rate after 10 months, while Brent crude oil continues to rally. The yield on the five-year ruble denominated notes declined to 8.87 percent on Wednesday, the lowest since July 2014. Forward rate agreements show that derivatives traders are predicting 60 basis points of rate reductions over the next three months.

- Eurozone Manufacturing purchasing managers’ index (PMI) data ticked up to 52.6 from 51.5, while most Bloomberg analysts were expecting a small decline. This suggests GDP growth is likely to be steady in the second quarter.

Threats

- As the chart below shows, during the days prior to the U.K. referendum the net balance of telephone and online polls suggested the U.K. would remain in the EU. However, the U.K. has voted to leave the EU, creating enormous political and economic uncertainty. David Cameron announced his resignation as Prime Minister on Friday. The Brexit may have created the “beginning of the end” of the U.K. as we know it. Scotland and Northern Ireland may be ultimately lost as well. The bigger threat is that other EU countries may follow the U.K.’s steps.

- EU ambassadors from the 28 EU nations agreed on Tuesday to extend sanctions against Russia until January. Their decision is still subject to approval by senior leaders, but it is not expected to change. The sanctions target Russia’s energy, financials and defense sectors, restricting the trade that EU businesses are allowed to conduct with Russia.

- Tension between Turkey and the EU is growing. Erdogan accused the EU of not wanting to accept Turkey as a member, as it is a “Muslim-majority country,” and suggested holding a U.K.-style referendum to let Turks decide if discussions between the EU and Turkey should continue.

(c) US Global Investors