- Both the United States and Europe are showing more economic improvements than expectations.

- Economic data from Japan indicates improvements.

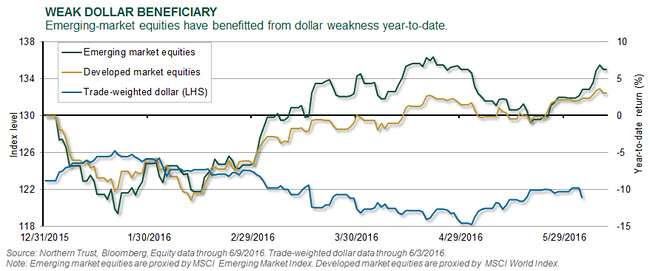

- The weaker dollar has led to emerging market outperformance.

- Are these improvements strong enough to withstand the Brexit uncertainty?

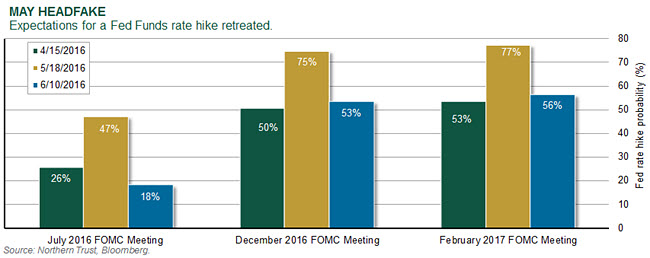

It appears that, once again, the Federal Reserve’s hopes to raise interest rates are being stymied by the economy. Just last month the Fed’s minutes showed a predisposition to raise rates soon, and Chair Janet Yellen said it would probably raise rates “in coming months” should the data continue to meet expectations. Soon after the market raised the odds of a hike by December to 75% (see chart below), the May jobs report showed weak job creation along with a downward revision of prior employment gains. Futures markets now project just a 56% chance of a hike by next February and a full rate hike isn’t priced in until August 2017. While the softer labor market data is unwelcome, it fits our expectation of a slow-moving Fed with the attendant weaker U.S. dollar and the associated positive impact on emerging markets and natural resources.

While U.S. labor markets softened, broader economic releases during the last month have been a little better, with both the United States and Europe showing an improvement relative to expectations. Recent data from Japan has shown improvements. Emerging-market growth has been in line with expectations, while China has shown mild deterioration. Bond markets have rallied on both fundamental and technical factors, as U.S. 10-year and 30-year Treasury bonds have fallen 0.12% and 0.16%, respectively, in yield. Led by the weaker dollar, emerging-market equities have outperformed, followed by U.S. equities, while European and Japanese equities have generated losses.

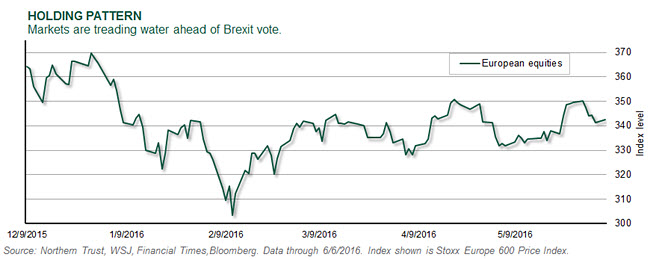

The British referendum on European Union (EU) membership takes place on June 23, and this is our primary risk case for the financial markets. Polling data can be misleading, as can bookmaking odds, which can be influenced by the size of the bets being made. We think those in favor of “remaining” in the EU have solidified the economic argument, while those in favor of “leaving” are increasingly focused on immigration. Even a successful “remain” vote, which is our expectation, will not fully quell the volatility around governance of the European Union. Thankfully, Europe’s economic momentum is solid, which helps mitigate some of the uncertainty surrounding the vote. A “leave” vote, however, could seriously dent this momentum and pressure the pound and related risk assets, while strengthening the dollar.

U.S. EQUITY

- Earnings estimate revisions have begun to move higher through the second quarter.

- Multiple market factors point to increased confidence in broader economic growth.

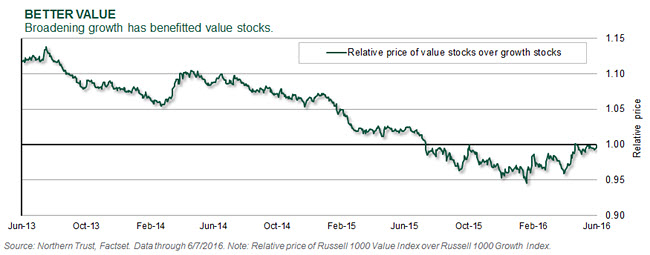

Through the second quarter, commodity prices have continued to move higher, driving positive earnings revisions in the energy and materials sectors. Breadth is improving: only the financial sector has seen negative revisions to earnings estimates since the end of February. Since the February low, we’ve seen a number of market factors reverse, which points to increased confidence in broadening economic growth. Small caps outperforming large caps, high-volatility stocks outperforming low-volatility stocks, and value outperforming growth are all consistent with improved growth prospects. As growth broadens, investors have less need to pay a premium for growth and safe-haven stocks, facilitating a rotation into value. We remain constructive on U.S. equities as better second-half growth and positive earnings revisions support the current market valuation.

EUROPEAN EQUITY

- The ECB is cautiously optimistic on growth.

- The Brexit vote remains a key risk.

On the back of an improving jobs picture, better private consumption and especially strong German output, the eurozone posted 2.1% gross domestic product (GDP) growth in the first quarter. Economic output is now back to pre-financial crisis levels, and its recent strength led the European Central Bank (ECB) to increase its 2016 GDP forecast to 1.6%. Despite this positive traction, inflation remains subdued and the ECB is cautiously optimistic, noting that “risks … remain tilted to the downside, but the balance of risks has improved.” Taking no new action at its latest meeting, the ECB awaits the impact of stimulus measures announced in March (including corporate bond purchases that begin this month). Assuming further economic stabilization and a vote that keeps the United Kingdom in the EU on June 23, markets could see a relief rally and turn positive for the year.

ASIA-PACIFIC EQUITY

- Positive first-quarter GDP masks underlying weakness.

- Japanese Prime Minister Shinzo Abe delays expected sales tax increase.

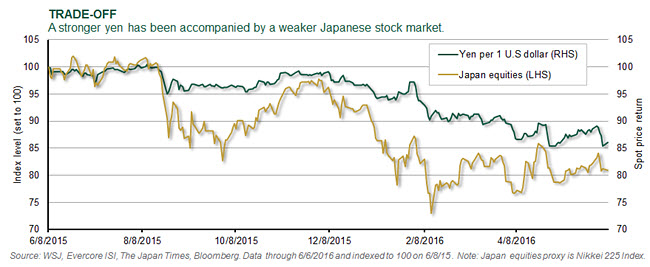

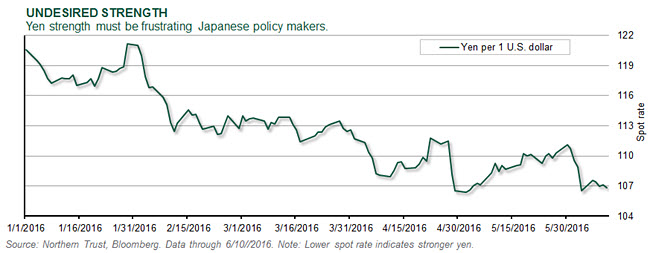

Despite a positive first-quarter GDP report for Japan, private consumption remained tepid, business spending declined, inflation eased and corporate profits have been weighed down by a stronger yen. As a result, Japanese Prime Minister Shinzo Abe announced the delay of an expected sales tax increase as well as his intention to roll out additional fiscal stimulus of ¥5 trillion to ¥6 trillion. Despite the ongoing malaise, there are pockets of strength: negatives interest rates are favorably affecting vehicle sales and housing starts (mortgage rates are near 1%) while the job market is proving especially resilient (jobs/applicants ratio is at a multi-decade high) and is yielding wage gains. Any stabilization in the global economy would benefit Japan’s export-led economy both in terms of demand as well as the currency implications relative to Japan’s perceived “safe haven” status and other central bank policy.

EMERGING-MARKET EQUITY

- U.S. dollar weakness has reduced pressure on emerging markets.

- The emerging markets have greater policy flexibility due to U.S. dollar weakness.

As expectations for an increase in the Fed Funds rate have been pared back, the U.S. dollar has weakened. (Fed Funds futures currently aren’t pricing in a rate increase until August 2017.) This more benign outlook for U.S. interest rates has alleviated pressure on emerging markets and creates more policy options. China continues to ease policy, and dollar weakness enhances its ability to manage its currency. South Korea, the second-largest emerging market, recently took advantage of reduced Fed expectations to reduce its policy rate for the first time in more than a year. Our recommendation in April to eliminate our underweight to emerging-market equities hinged on the weaker dollar, along with reduced downside risks around China over our tactical timeframe.

REAL ASSETS

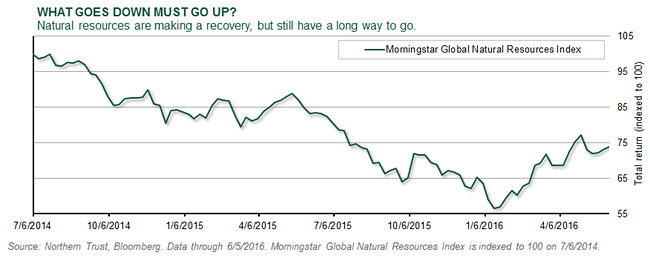

- Natural resources have been supported by better fundamentals and a backtracking Fed.

- Changing investor sentiment can have big near-term impacts on this small asset class.

After taking a breather in May, equity-based natural resources have started to rise again. Two primary factors are at play: supply/demand dislocations — notably in the oil markets — are starting to correct. U.S. oil inventories reached their peak in April and are steadily declining. Two, the Fed’s rate hike trajectory was derailed by the disappointing May U.S. jobs report, pushing the dollar down and commodity prices up. Continued capital inflows could pressure the relatively small asset class, pushing valuations higher. The asset class is up 35% since its lows, but still 30% below its high. We remain moderately underweight (having just increased our allocation last month), but are mindful of the potential for upside risk in the asset class.

U.S. HIGH YIELD

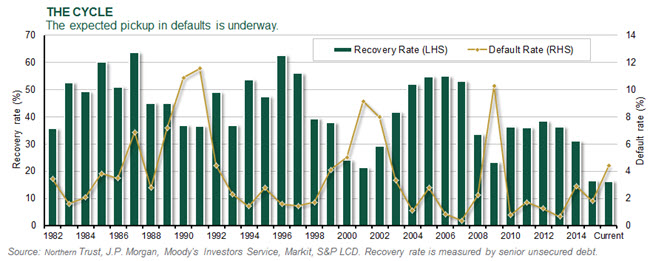

- High yield default rates are on the rise.

- Recovery rates have declined as defaults have increased.

The U.S. high yield default rate has increased to 4.4% after enjoying a very low default rate of 1.5% from 2010 to 2015. This is consistent with the long-term rate, but it could increase to more than 6% by year end. Defaults have been concentrated in energy, commodity and retail sectors. As the default rate increases, the recovery rate has historically fallen. The recovery rate averaged 37% from 2010 to 2014, but has since fallen to 16.5%. This is reflective of the decline in commodity prices and the amount of capital that went into commodity sectors prior to the downturn, and isn’t reflective of a market-wide increase in defaults. The increase in defaults, combined with lower recovery rates, demonstrate the importance of managing credit risk. Longer term, we expect default rates of 5% with a 50% recovery rate, leading to a 2.5% credit loss.

U.S. FIXED INCOME

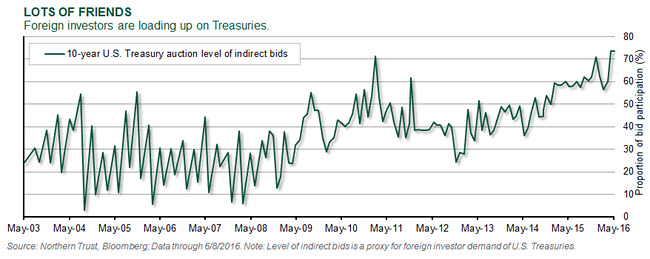

- Foreign demand for U.S. Treasuries has hit record highs.

- We expect rates to remain low as more global investors gravitate toward U.S. Treasuries.

Fixed income is a global asset class, and historically low interest rates around the globe have led foreign investors to seek the relative attractiveness of the U.S. Treasury market. Indirect bids in U.S. Treasury auctions are often used to gauge foreign demand and these bids have been rising, with demand at the recent 10-year note auction hitting all-time highs. The substantial demand from abroad is just another factor investors need to consider when framing their interest rate outlook. With most central banks outside the United States easing monetary policy and with global growth challenged, we expect U.S. Treasury yields to remain lower for longer than many believe. In addition, foreign investors have been historically biased toward dollar-denominated investments.

EUROPEAN FIXED INCOME

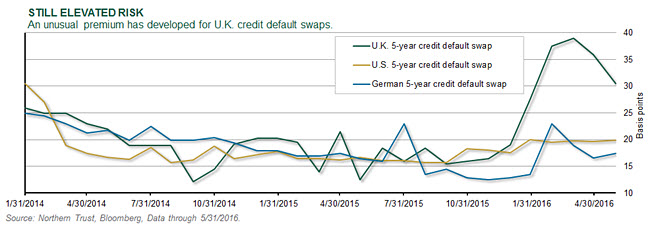

- Markets stepped up their concern over Brexit risks.

- The ECB delivered a confident message in June.

Market concerns over Brexit appear to have increased as the latest opinion polls show growth in support for the “leave” camp and bookmakers shorten their odds against this outcome. The associated flight to quality has taken global government bond yields to record lows amid expectations that global central banks will keep interest rates at exceptionally low levels. While 10-year Gilts are trading at their all-time low yield, the price of bond protection for U.K. sovereign risk has risen sharply. At its June meeting, ECB President Mario Draghi heralded the success of the ECB’s monetary policy decisions, which have supported the recovery in European markets. The ECB’s first corporate bond purchases commence this month amid tightening credit spreads. Although downside risks remain, the ECB’s upward revisions to its 2016 growth and inflation projections suggest it may be sidelined for now.

ASIA-PACIFIC FIXED INCOME

- Pressure continues to mount on the Bank of Japan.

- The Reserve Bank of New Zealand is likely to follow the Reserve Bank of Australia in taking interest rates lower.

Pressures on the Bank of Japan to implement additional policy easing appear to be on the rise, with the yen strengthening amid signs that Abenomics has stalled. Questions regarding the efficacy of negative interest rates remain, and the push toward additional asset purchases may be complicated by the record lows in Japanese government bond yields (which are now negative out to 15 years). While maintaining monetary policy at its June meeting, the Reserve Bank of New Zealand looks likely to follow Australia and reduce interest rates in coming months as concerns regarding currency strength and low inflation prevail. Although increasing commodity prices will eliminate some of the downward pressure on inflation, uncertainties related to global growth appear to be hurting domestic confidence and activity.

CONCLUSION

During our asset allocation discussion this month, we hesitated to draw too strong a conclusion from one poor payroll report in the United States. (To be fair, the prior two months’ job gains were also lowered.) We’ve characterized the major economies as operating in “growth channels,” as currency devaluation strategies are no longer working, global demand is weak but recessionary risks are low. Markets are also underpinned by supportive, but stale, monetary policy. Low interest rates support valuations across asset classes, but there’s increasing concern over the negative impact of low/negative interest rates. The poor reaction of the Japanese markets to the introduction of negative interest rates earlier this year (falling equity prices, rising currency) is a case in point.

Despite the many legitimate concerns facing the markets — ranging from modest growth to the remaining firepower of central banks — there have been pockets of strength in the asset markets this year. Underpinned by the rally in yields, investment-grade fixed income has generated strong relative returns while high yield fixed income has additionally benefited from the tightening of credit spreads. Interest-rate-sensitive assets like global infrastructure and real estate have also benefited from falling rates, while emerging-market debt and equities have benefited from the declining value of the U.S. dollar. We think the decline in yields is justified by the moderate growth outlook, along with the intermediate-term outlook for disinflation.

It’s challenging, as asset allocators, to face an issue such as the potential of Britain leaving the EU. With the outcome being binary, you have an unacceptably high risk of being wrong in making a big bet. What if an investor significantly reduces his or her exposure to U.K./European equities as a hedge against Brexit, only to find the vote to “remain” is the winner? The upward adjustment in asset prices would be too quick to reverse course and the strategy would lose money (without even considering the tax impact of the initial sale in taxable accounts). With our view that a “remain” vote is the most likely outcome, we’ve chosen to not recommend a reduction to U.K./European equities ahead of the June 23 referendum. Our recommended positioning remains moderately overweight overall risk, with significant overweight positions in U.S. equities and high yield bonds. We believe these assets should allow us to participate in market upside during the next year — and should outperform European and Asian equities in a down market.

The opinions expressed herein are those of the author and do not necessarily represent the views of The Northern Trust Company. The Northern Trust Company does not warrant the accuracy or completeness of information contained herein, such information is subject to change and is not intended to influence your investment decisions.