Impact Investing and Goals-Based Financial Planning

Impact investing has moved front and center on advisors’ radar screens, and rightly so.1 Clients from millennials to baby boomers are exploring the opportunity and encouraging their advisors to come up with options for investing in the space.2

As with all things, the landscape of impact investments is constantly changing, presenting new opportunities as well as additional challenges for advisors and their clients. Representative of this sea change in the financial services industry are the following developments:

- Prudential’s public commitment to build a $1-billion impact investment portfolio by 2020

- Bain Capital’s announcement that it will create a new business unit that focuses on “double bottom line investments”

- Goldman Sachs Asset Management’s announcement of its intention to acquire Imprint Capital Advisors, a prominent impact investment firm

Not only are financial institutions making inroads in this space, but government institutions across the globe are gearing up to allocate assets and resources to values-based investing, evidenced by the following developments:

- The U.K. government legislation to grant 30-percent tax relief for those investing in social investments

- The European Union’s formal recognition of firms that invest 70 percent of investor capital into European social businesses as European Social Entrepreneur Funds

- The G-8 establishing the Taskforce on Social Impact Investing, which in 2013 convened a Social Impact Forum

- The Obama administration’s efforts to bring together diverse players in the impact investing space to participate in a White House Roundtable on Impact Investing, organized to address a number of diverse global challenges

Impact investing comprises investments in companies, organizations, and funds with the intention to generate social and environmental impact alongside a financial return. Those who advocate this strategy represent a diverse group of political and religious organizations3 and public and private change agents, including private foundations, public foundations, private banks, development and government agencies, privately held funds, individuals, and a variety of other institutions such as pension funds. To these investors, impact investing offers an often innovative, market-based solution employed to address environmental, social, and governance issues across a wide array of policy areas. Contrast this proactive approach with the traditional values-based investing approach known as socially responsible investing (SRI), which employs negative screening as the primary method of investing consistent with one’s values.

Why have investors reached a tipping point when it comes to values-based investing? The reason is simple. A growing awareness exists among both policymakers and investors that the current method of tackling social problems is not working. Whether you call it new capitalism, social entrepreneurship, or collaborative capitalism, the assumption behind this movement is that solving complicated social issues requires a new model of capitalism that harnesses market forces to solve complex social issues. Thus, we are seeing first-hand a new generation of social entrepreneurs and values-based investors creating market solutions to solve so-called “wicked (social) problems.”4

The reasons for advisors to consider adding an impact investment offering to their suite of solutions are many and include the following:

- Investing for social impact is rapidly gaining momentum among high-net-worth individuals of all wealth levels5

- Millennials are demonstrating a strong desire to invest for both social and financial impact6

- The solution set for impact investing is growing, evidenced by the recent proliferation of numerous impact investment instruments across all asset classes

- The growing body of research, validating the positive performance-differential for impact investing

- Many consider it “the right thing to do”7

As legend has it, attendees at a 2007 Rockefeller Foundation meeting at Lake Como, Italy, coined the term “impact investing.”8 Eight years later in 2015, the lexicon of impact investing is vast and varied and includes terms such as: sustainable responsible investing (SRI)9; values-based investing; and environmental, social, and governance (ESG) investing. As more investors enter the space, the definition of what qualifies as an impact investment has broadened to include comprehensive approaches such as green investing and thematic investing.

Impact investing represents the emergence of a new paradigm used to address social and environmental issues. Impact investing complements—rather than replaces— philanthropic endeavors. Most agree that impact investing requires a deliberate intention on the part of the investor to garner a positive impact—however measured, i.e., impact investing requires both intention and outcome.10

It is important to note, however, that impact investments do not represent an asset class. Instead, this collection of instruments constitutes a wrapper for different investment strategies across all asset classes. It is this author’s opinion that impact investing will follow the same trajectory as nontraditional or alternative investments—especially hedge funds. Impact investing mirrors the evolution of nontraditional assets in many ways, e.g., early challenges with defining the space, persistent misperceptions around status as an asset class and performance characteristics, and the emergence of niche players in the space.

Goals-Based Wealth Management and Impact Investments

Often described as a holistic approach to wealth management, goals-based financial planning follows a well-defined process to determine each client’s unique set of needs and goals—both financial and nonfinancial. As part of this process, the advisor’s role is to assist each client in aligning his/her goals with appropriate investment strategies.

At this stage in the financial-planning process, the advisor’s primary task is to help each client identify and formulate goals built around a hierarchy of needs, beginning with the most basic needs and culminating with higher-order needs.

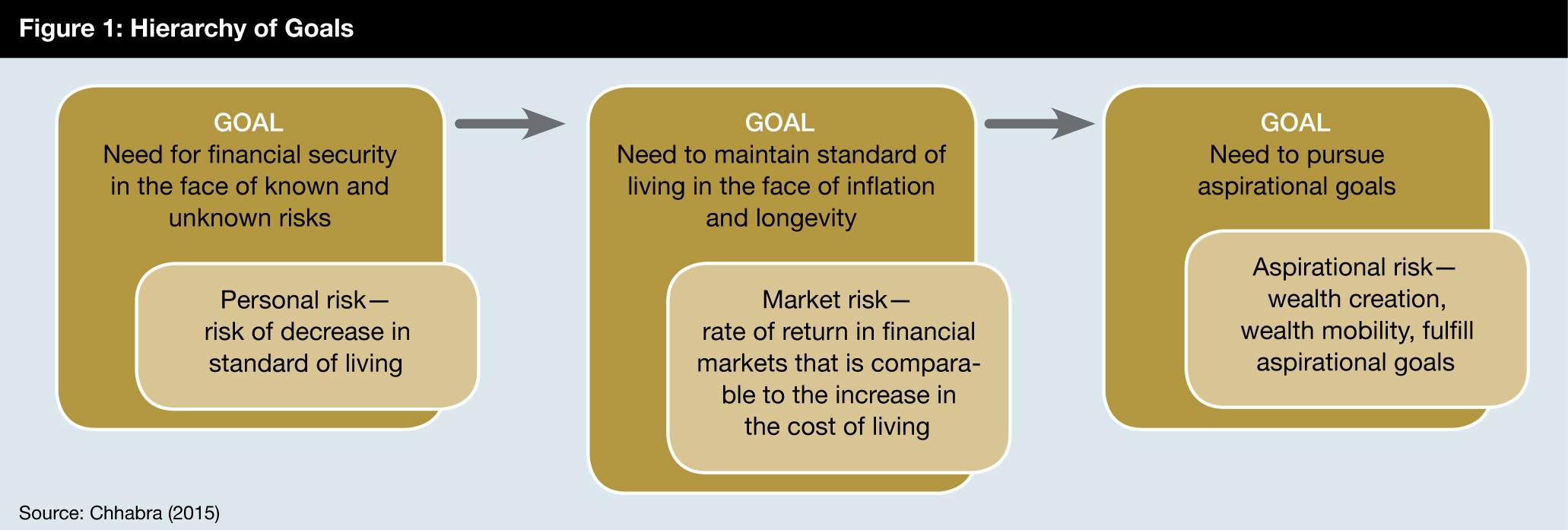

For example, Chhabra (2015) describes a wealth allocation framework that designs a portfolio using three seemingly incompatible objectives: (1) the need for financial security, (2) the need to maintain a living standard in the face of inflation and longevity, and (3) the need to pursue aspirational goals.11 Chhabra instructs the advisor to engage in an effective dialogue with clients to quantify four dimensions for each goal: target value, time horizon, risk tolerance, and priority. The next step requires matching each goal category with its appropriate risk bucket. In Chhabra’s wealth allocation framework, the more important the goal, the safer the securities in the risk bucket (see figure 1).

In addition to lifestyle goals, such as owning a luxurious home, aspirational goals often include a plethora of philanthropic objectives. For those clients fortunate enough to move up the hierarchy to the point of satisfying aspirational goals, Chhabra’s assumption is that these clients will fund aspirational goals with residual assets—and only after funding financial-security and standard-of-living goals first. Further, he assumes that clients and advisors will use only the riskiest assets to achieve aspirational goals.12

However, over the past few years, financial intermediaries have responded to the demand for values-based investments by creating a variety of strategies—both public and private—across all asset classes. Today, the process of incorporating impact investments into existing portfolio strategies offers investors the opportunity to engage in values-based investing along a continuum of diverse risk/return levels at every level of the hierarchy of needs.

Integrating an impact investment strategy within the financial-planning process requires advisors to add a preliminary step of assessing goals “above the line” to enhance and complement the traditional “below the line” method of financial planning. The Fithian brothers use a simple decision-making tool called the “Planning Horizon” to help clients view goals and objectives both above the line and below the line (Fithian and Fithian 2012). In the Fithians’ view, traditional financial planning activity generally takes place “below the line” and involves the how of achieving clients’ wealth goals, i.e., the strategies and products advisors use to accomplish wealth objectives. Conversations that take place “above the line” deal with the why of planning, i.e., clients’ deepest and personal intents for their wealth. Before an advisor sits down with a client to discern, document, and categorize goals into essential, important, and aspirational buckets,13 an advisor must delve into the thought processes behind a client’s articulated goals by asking probing questions such as the following:

- What do you really care about?

- What are you passionate about?

- Where do you want to have an impact?

- What do you believe is worth doing?

Planning for Impact

Many methods exist for advisors to use in helping investors discover their personal values and beliefs.14 Rockefeller Philanthropy Advisors (RPA) discusses a process for helping donors formulate philanthropic goals that is also useful for helping investors formulate impact investing objectives.15 RPA’s approach follows three steps:

- Frame the issue

- Narrow the focus

- Define the outcome (impact)

The process is straightforward, but walking clients through each step in a thoughtful and thorough manner requires a major commitment of time on the part of the advisor. At first glance, understanding a client’s definition of a very general issue is seemingly unmanageable. However, with patience and insight, advisors can successfully help clients define an impact investment strategy.

Continue reading this article now.

Margaret M. Towle, CAIA®, CIMA®, CPWA®, is a Financial Advisor, Managing Director-Wealth Management at Merrill Lynch. She has been an active participant in the financial services industry for more than 30 years, including advising institutional and individual clients on impact investment strategies across all asset classes. Contact her at [email protected].

Endnotes

1 This article is not meant to provide tax, legal, or investment advice.

2 This article focuses on incorporating values-based goals and objectives within the financial-planning process for individual investors. Thus it is beyond the scope of this article to address the process of integrating values-based goals within institutional portfolios. However, it is worth noting that institutional investors face some unique challenges in this regard. For a detailed discussion of fiduciary duty, see “Responsible Investing for the Modern Fiduciary: Aligning Goals, Duties, Investments and Impact,” Northern Trust, November 2014, https://www.northerntrust.com/documents/line-of-sight/wealth-managem....

3 For example, in 2014, Pope Francis organized a symposium on impact investing. During the symposium, the pope stated: “Impact investors are those who are conscious of the existence of serious unjust situations, instances of profound social inequality and unacceptable conditions of poverty …” Pope Francis, “Investing for the Poor,” Vatican Symposium on Impact Investing (2014), http://www.investingfor thepoor.org/.

4 “Wicked problems” encompass challenges that are broad and not easily solved, for example issues such as the current refugee/immigration crisis in Europe, prisoner recidivism in the United States, global poverty in developing countries, or climate change. Horst Rittel was one of the first to formalize a theory of wicked problems, along with a discussion of the characteristics of wicked problems.

5 More than 88 percent of participants in a recent Capgemini RBC Wealth Management study of high-net-worth investors of all wealth labels, ages, genders, and geographies consider it important to deploy their capital and resources to “drive positive effects of society and/or the environment.” See “United States Wealth Report 2014,” page 20, Capgemini RBC Wealth Management.

6 A recent U.S. Trust study found that of the participants interviewed, one-third of all high-net-worth investors and nearly two-thirds of millennials currently own or employ social impacting investing strategies. See 2014 U.S. Trust Insights on Wealth and Worth® Survey.

7 In fact some, such as Paul Shoemaker of Social Venture Partners, argue that it is something that you “can’t not do.” See Shoemaker (2015).

8 See http://impactalpha.com/rockefellers-high-impact-investment/.

9 Even the term SRI has changed meanings over the years. SRI is now known as “sustainable responsible investing.” Historically, SRI was known as “socially responsible investing” and implied a negative screening process to eliminate what is often called “sin” investments, such as tobacco, guns, and alcohol.

10 Interestingly, not all agree that impact investment firms/intermediaries articulate a clear intention of delivering a social impact. For example, a solar energy firm may in fact address an environmental issue that results in a positive impact, yet be agnostic regarding the positive/negative impact of its activity.

11 See Chhabra (2015). Chhabra’s conceptual framework for goals-based wealth management somewhat resembles Abraham Maslow’s psychological “hierarchy of needs.”

12 Chhabra (2015, 98) states that assets in the aspirational risk bucket are “riskier than the market in general and include the possibility of catastrophic failure and loss of principal.” Assets in this bucket include venture capital, options, single-manager hedge funds, and leveraged real estate investments, among others.

13 Jean L. P. Brunel suggests using “better” (different) words to discuss goals and risks. For aspirational goals, ask clients to discuss “needs, wants, wishes, and dreams.” For risks, ask clients to talk in terms of “nightmares, fears, worries, and concerns” (Brunel 2015, 83).

14 Advisors interested in incorporating clients’ values and missions within an (impact) investment strategy can learn some useful lessons from advisors in the philanthropic world. A valuable knowledge base is the curriculum for the CAP® (Chartered Advisor in Philanthropy) offered by The American College of Financial Services. See http://www.theamericancollege.edu/financial-planning/cap-philanthropy.

15 See “Your Philanthropy Roadmap,” Rockefeller Philanthropy Advisors, 2013, http://www.rockpa.org/ roadmap.

© Investment Management Consultants Association (IMCA)