China’s fragmented equity markets have always created confusion for investors. As MSCI prepares to make a landmark decision on Chinese equities, we think it’s a good time to get ready for a new “All China” opportunity.

For some time now, investors have been waiting for index provider MSCI to announce the inclusion of China’s onshore market, or A-shares, in its global and international indices. The decision—which may be announced on June 15—would mark an important step in the liberalization of China’s capital account. Our research suggests that it could lead to around US$400 billion of inflows into China’s equity markets.

Whether or not MSCI makes its move next week, we believe that it’s only a matter of time before the A-shares door is opened to the world. The potential impact on China’s equity markets—and on the portfolio allocations of global investors—would be profound. Yet investors will need to gain a deeper understanding of the behavior patterns of China’s markets in order to invest effectively in a vastly enlarged pool of stocks.

Understanding Performance Patterns

It’s often said that China’s equity markets resemble alphabet soup because of the various lettered share classes. The onshore A-shares are quoted in renminbi on the Shanghai and Shenzhen stock markets, with limited availability to foreign investors. Offshore stocks include the H-shares, which trade on the Hong Kong exchange and are denominated in HK dollars; ADRs listed in New York; red chips; B-shares; and various legacy share classes.

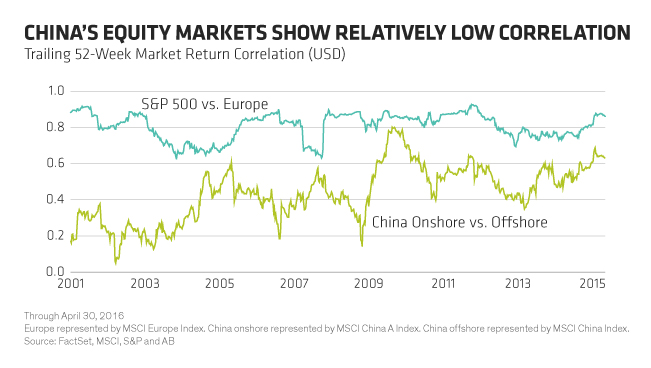

Many investors believe that onshore and offshore markets tend to behave similarly. In fact, our research shows the opposite: the correlation of the market returns of onshore and offshore shares has historically been quite low—much lower than the correlation between the geographically disparate US and European markets (Display).

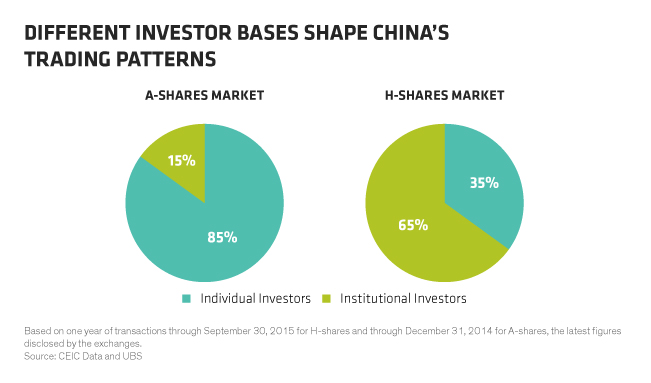

Why the difference? We think it’s mainly because the two Chinese markets have completely different investor bases. About 85% of investors in the A-shares market are domestic Chinese retail investors (Display), typically with short time horizons, which can foment market volatility, especially during moments of uncertainty. In contrast, the China offshore market is dominated by institutional investors, who generally have more patience, resolve and long-term positions.

But as China’s equity markets have gradually opened in recent years, the correlation between the offshore and onshore components has tightened. Investors might think this is because as China opens up, its onshore market will behave more like its global peers. We don’t think so. In our view, as the two markets converge, offshore Chinese stocks will start to look more like their more volatile domestic A-share cousins.

The Big Leap Upward

The potential inclusion of China’s A-shares in the MSCI Emerging Markets Index and other global and international benchmarks will draw China’s various equity markets into a bigger, more liquid and more balanced pool of securities with relatively attractive risk characteristics.

Today, the MSCI China Index—representing offshore Chinese stocks—is dominated by financial and information technology stocks. The MSCI China A Index contains a high concentration of industrial stocks—a legacy of China’s “old style” economy, which is being diversified to include a higher mix of consumer and service industries.

However, the MSCI All China Index, which combines A-shares and offshore stocks, offers a more balanced and diversified investment opportunity. It’s comparatively large and deep, with around 1,000 stocks offering a good mix of the “old” and “new” Chinese economies. Yet most investors still rely on the more fragmented indices when thinking about the market and creating their portfolios.

By eventually fully including A-shares, the China exposure of the MSCI Emerging Markets Index will broaden significantly, from nearly 26% today to about 40%—requiring many investors to rethink their portfolios’ emerging-market equity allocations. This will also have an effect on China exposure in international and global allocations.

Will It Happen?

We’ll sound a note of caution, however: MSCI was expected to include A-shares in its global indices before now, but this was delayed because of market volatility and various structural and regulatory issues. Not all of these issues have been resolved, and it’s possible that expectations of an announcement next week will be disappointed. Indeed, we wouldn’t be unduly surprised if A-shares’ inclusion was delayed another year.

But we think the timing of the move is less important than the near certainty that it will eventually happen. When it does, it will be more important than ever for investors to start looking at China as a single equity market, with a vast range of opportunities for sourcing returns across the world’s most populous nation. As China’s equity markets open to the world, international investors will need to delve much deeper into what really makes Chinese companies tick.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.