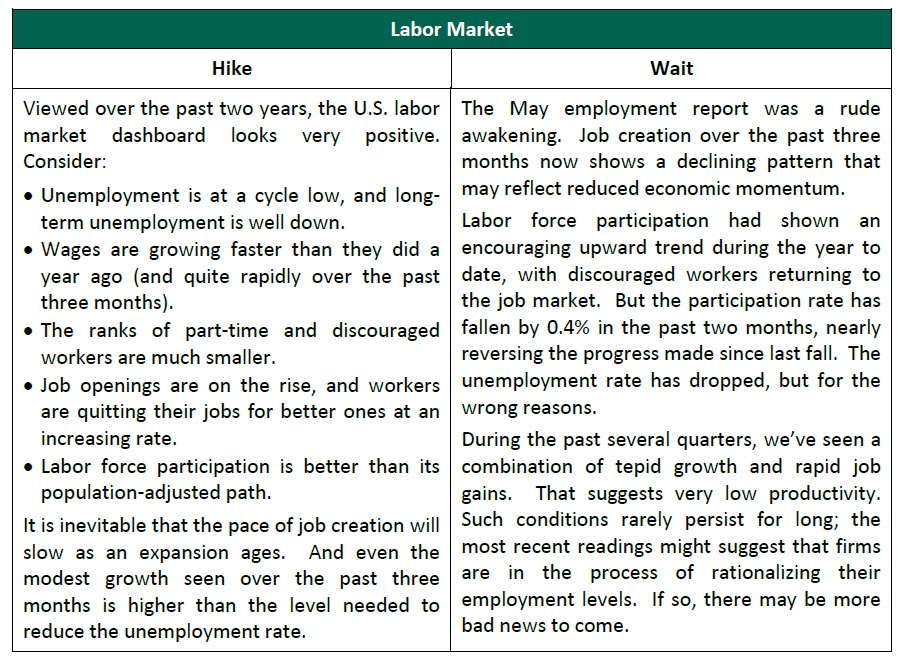

I usually don’t need much assistance to look foolish. But when a rogue report arrives that upends understandings, I look even less credible than usual.

At least I wasn’t alone. The American Bankers Association’s Economic Advisory Committee had gathered in Washington late last week to craft a forecast. Some of our industry’s best and brightest are members. All of us were caught entirely off guard by the May U.S. employment report, and we had to reconsider the consensus we had spent most of Thursday debating.

Without doubt, last Friday’s report initiated some substantial reconsideration within the halls of the Federal Reserve, scarcely a week before a critical policy meeting. Here is our take on the likely content of next week’s conversations.

We’ve spent a great deal of time examining the May job report, in an attempt to separate signal from noise. The Verizon strike held back payroll creation in May by about 35,000 jobs, which will be recouped next month. There were some other unusual outcomes: a sudden increase of 468,000 people working part time for economic reasons, 1.2 million workers leaving the labor force over the past two months, and employment in several categories that fell well short of recent averages. It also bears mentioning that the error around the payroll report is substantial: the 90% confidence band for May was -39,000 to 107,000, big enough to drive a busload of employees through.  The report came completely without warning. (Steve Liesman of CNBC asked, on air, if there was a digit missing.) Other indicators, such as jobless claims, surveys of hiring intentions, and the ADP payroll survey gave no hint of the correction to come. There have been a handful of sharp declines in payroll creation during the current expansion. All have been reversed in fairly short order. So there is a reasonable possibility that the May report was an aberration.

The report came completely without warning. (Steve Liesman of CNBC asked, on air, if there was a digit missing.) Other indicators, such as jobless claims, surveys of hiring intentions, and the ADP payroll survey gave no hint of the correction to come. There have been a handful of sharp declines in payroll creation during the current expansion. All have been reversed in fairly short order. So there is a reasonable possibility that the May report was an aberration.

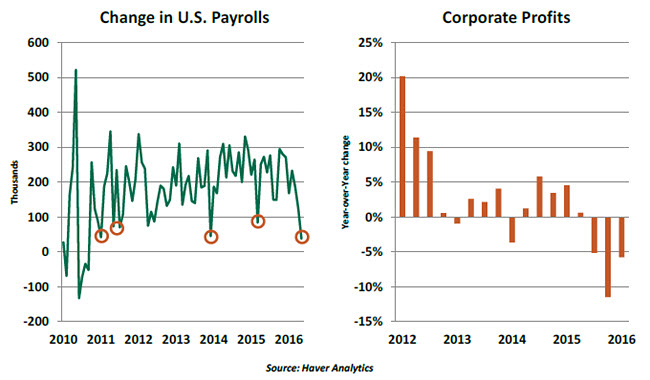

On the other hand, gross domestic product (GDP) has been advancing very slowly and corporate profits have been under pressure. Seeking to reinforce margins, firms sometimes look to economize on expenses, which can mean headcount reductions. There is evidence that this is going on, even in industries outside of energy.

Economists remain puzzled by the developments surrounding productivity. During the first quarter, output per hour for U.S. workers actually declined by 0.6%. There is a series of potential explanations: soft demand (which should improve, lifting GDP without requiring too many more hours), disappointing public and private investment spending, and secular stagnation.

As we have written, we do not agree with those who say that the productivity bust is permanent. And if we are correct in this, then demand for labor should remain strong in both the short term and long term.

Our sense is that the May report understates the health of the American labor market. We expect a bounce back next month, beyond the recovery of the striking Verizon employees. At this stage of the business cycle, readings of 100,000 or more are actually quite respectable. Nonetheless, the uncertainty created by last Friday’s release almost certainly rules out any change of policy next week.

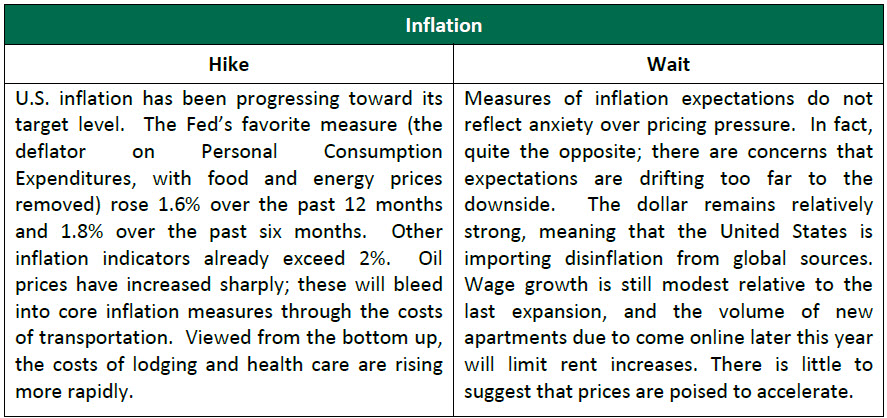

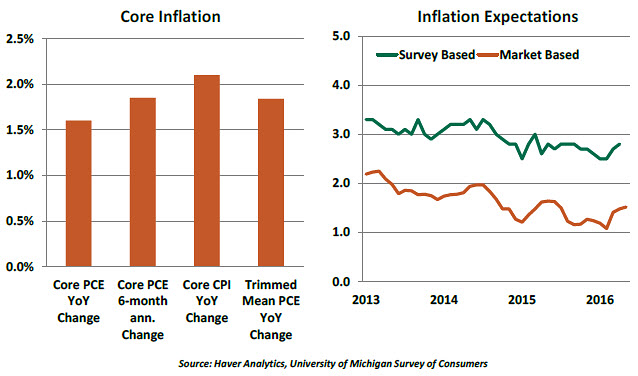

Across the board, U.S. inflation is higher than it was a year ago. For the overall price level, the recovery of oil prices (now at more than $50 per barrel) has been a major theme; gasoline prices are rising in concert.  It is certainly true that inflation is weak elsewhere in the world, but energy is a major contributor to this outcome. Further, the United States produces and consumes services at a higher rate than other economies. Services are predominantly generated domestically, so America is a bit sheltered from imported disinflation.

It is certainly true that inflation is weak elsewhere in the world, but energy is a major contributor to this outcome. Further, the United States produces and consumes services at a higher rate than other economies. Services are predominantly generated domestically, so America is a bit sheltered from imported disinflation.

Inflation expectations are very difficult to read. It is clear that trends in the energy markets exert a heavy influence on market-based and survey measures, despite the fact that these commodities make up a very small portion of price indexes. Implied inflation from trading in inflation-protected securities should be taken with a grain of salt, given the world’s strong appetite for Treasury securities of any kind and a risk premium built into their prices.

In her speech last Monday Janet Yellen made explicit mention of expectations as a reason to be circumspect. If people don’t think inflation will recover, then it makes it less likely that it actually will.

Prior to the job report, Fed officials sounded very much like they were gaining comfort with the notion that inflation would approach the 2% objective in the near term. But a point of debate within the central bank is whether inflation should be allowed to run “hotter” than the target for a while to compensate for the prolonged interval of underperformance. If the Fed takes this tack, then there is less motivation to tighten now.

In our view, inflation will not likely surprise us to the upside any time soon. But U.S. monetary policy is extraordinarily accommodative. And given the long lags between changes in rates and economic reactions, taking steps toward normalcy before inflation gets too hot might make sense. If growth and labor reports recover from recent disappointments, another step upward later this year seems warranted.

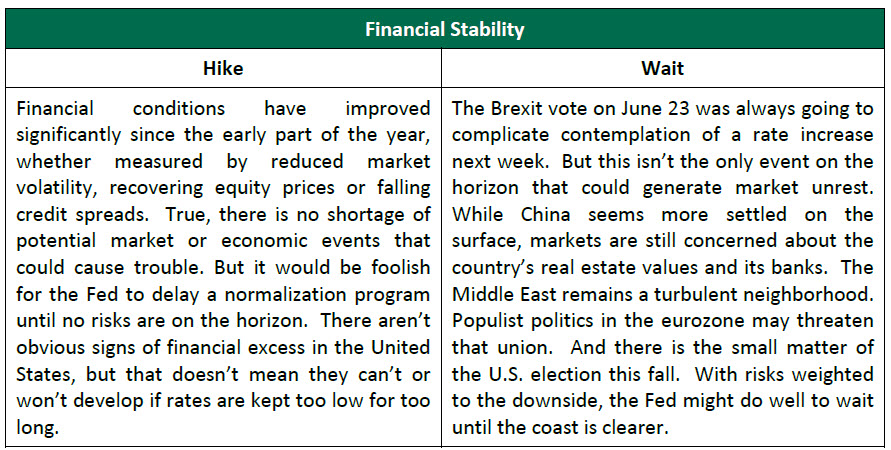

Financial stability is not a formal mandate for the Fed. But financial instability can imperil the achievement of its official goals.  Through references to financial conditions or international linkages, Fed officials have made increasing note of global elements when discussing policy choices. Increases in U.S. interest rates can create “wrong-way” risk for emerging markets that borrowed in U.S. dollars, simultaneously raising their borrowing costs and lowering the value of local currency. Those markets that peg their currency to the U.S. dollar (formally or informally) will see their competitiveness hampered if and when the Fed tightens.

Through references to financial conditions or international linkages, Fed officials have made increasing note of global elements when discussing policy choices. Increases in U.S. interest rates can create “wrong-way” risk for emerging markets that borrowed in U.S. dollars, simultaneously raising their borrowing costs and lowering the value of local currency. Those markets that peg their currency to the U.S. dollar (formally or informally) will see their competitiveness hampered if and when the Fed tightens.

The Fed has made no secret of its desire for strong markets to generate wealth effects. Market corrections would have the opposite effect, and many think the Fed is trying to avoid these at all costs. But the Fed does not like to be seen as providing a put option on equities, or flinching at stress that proves to be transitory.

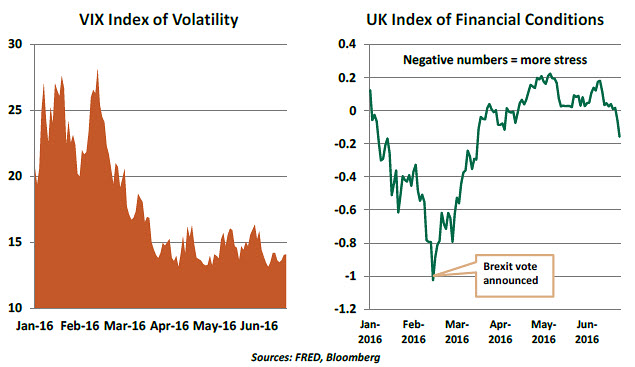

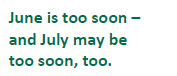

If Brexit supporters prevail on June 23, the global outlook will become more uncertain, enough so that the Fed will likely have to hold off for quite a while. If the vote is to stay, the way should be clear to resume a path to normalization. Markets are very nervous about the outcome.  With June off the table, consideration turns to July. In our view, the timeline makes a move at that juncture unlikely. The Fed will have little new information: only one more job report and no official tally of second-quarter growth. There is no press conference currently scheduled after the July meeting; one could be hastily assembled, but haste is not conducive to strong messaging. Market expectations show a scant (18%) possibility of a July move; to steer that reading northward, the Fed would have to rev up its rhetoric in fairly short order if the June employment report is positive.

With June off the table, consideration turns to July. In our view, the timeline makes a move at that juncture unlikely. The Fed will have little new information: only one more job report and no official tally of second-quarter growth. There is no press conference currently scheduled after the July meeting; one could be hastily assembled, but haste is not conducive to strong messaging. Market expectations show a scant (18%) possibility of a July move; to steer that reading northward, the Fed would have to rev up its rhetoric in fairly short order if the June employment report is positive.

All things considered, we now anticipate the next Fed move in September. The decision will be data-dependent, but if growth and employment follow our expectations, the case should be strong. For now, though, the cost of waiting is low relative to the cost of acting.

None of this is to suggest that the June meeting will be dull. It will be interesting to see how the post-meeting statement characterizes the employment situation and how Janet Yellen spins things in her post-meeting press conference. We will also get an updated set of forecasts from Federal Open Market Committee (FOMC) participants; we know the forecast for 2016 will be downgraded, if for no other reason than the soft first quarter. The unemployment forecast will reveal views on whether the recent decline in jobs creation will reverse.

The dot chart illustrating participants’ expectations for the funds rate will be very revealing. The 2016 column will now cover only six months; we’ll be watching to see how many participants are still calling for two moves before year’s end.

I certainly don’t think this will be the last time that I’m made to look foolish. I just hope I don’t have to conduct a press conference after my next display of ineptitude.