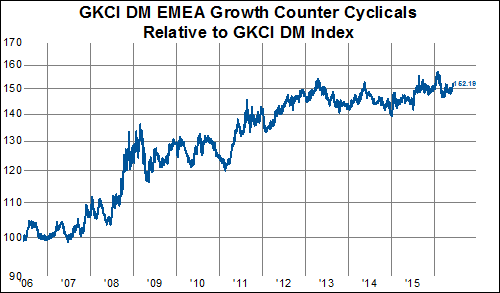

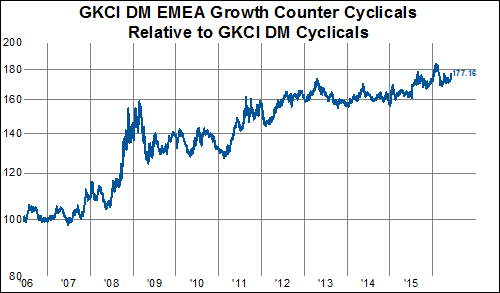

Earlier this week, we endeavored to show how companies with excellent fundamentals (i.e. Knowledge Leaders) are not always rewarded in the stock market, highlighting the less than positive trends in many of our point-and-figure charts for the Health Care sector in DM EMEA. As promised, now we will share some interesting new trends among other groups in the region: Industrials, Materials, and Information Technology. To be sure, these cyclicals have been largely out of favor over the last several years as the growth counter-cyclicals (Health Care and Consumer Staples) have dominated market performance– up more than 60% versus the broad developed market and nearly 80% when compared to just cyclicals.

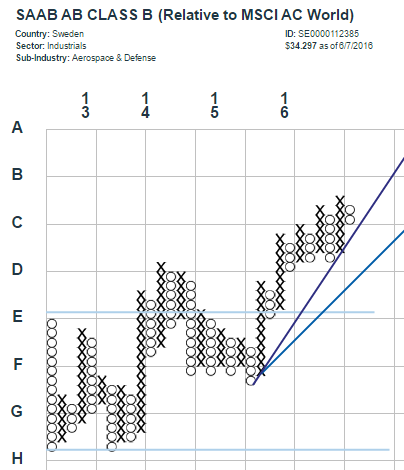

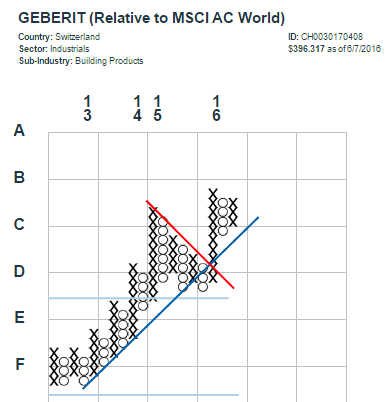

Limiting ourselves to only the Knowledge Leaders in DM EMEA, we were surprised to find more positive chart patterns (bases and breakouts) in the above mentioned cyclical sectors. Below is a sampling of our findings.

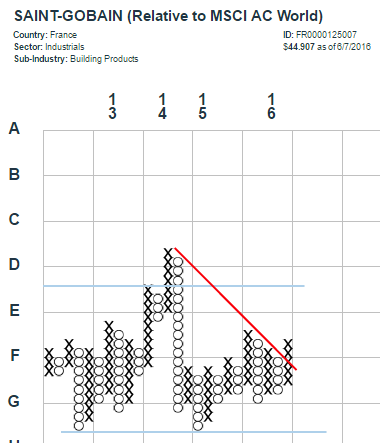

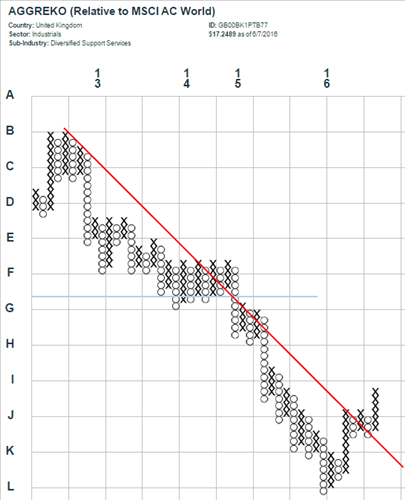

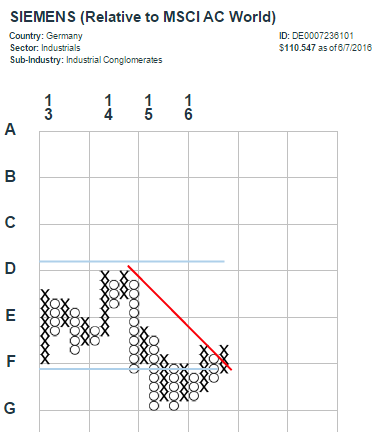

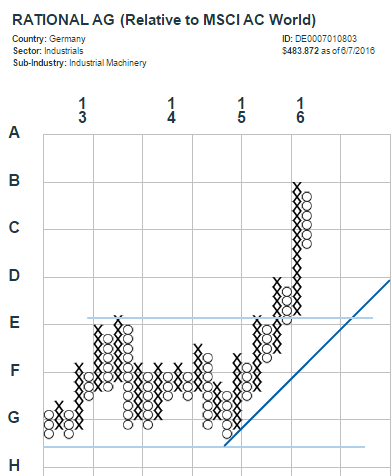

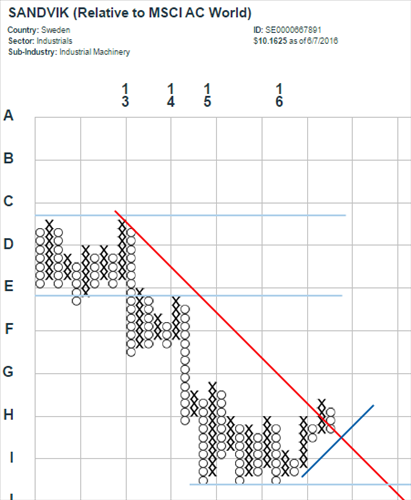

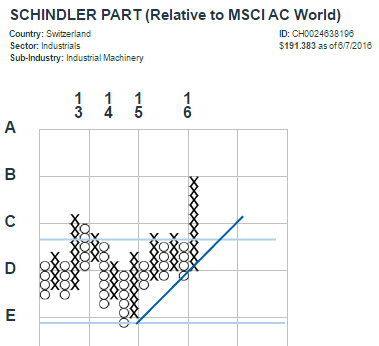

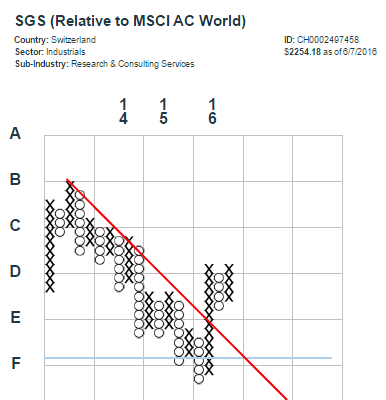

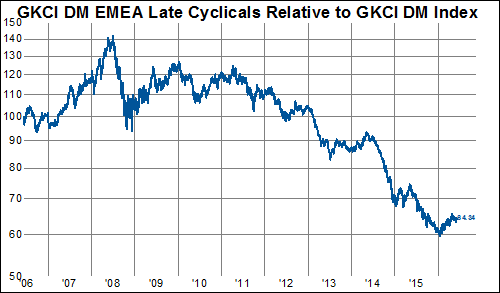

GKCI DM EMEA Industrials (late cyclical)

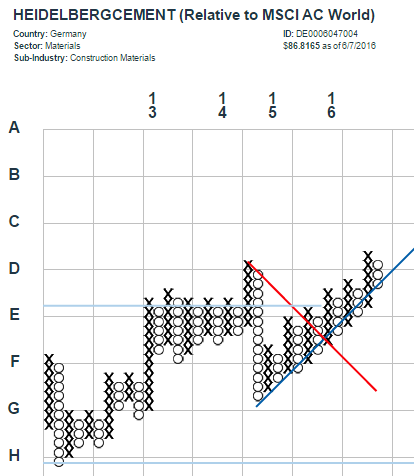

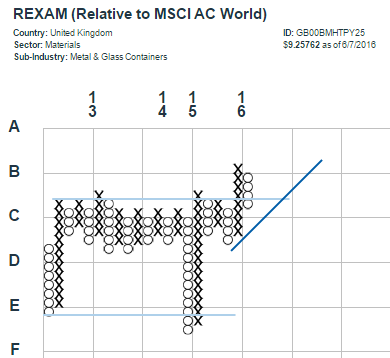

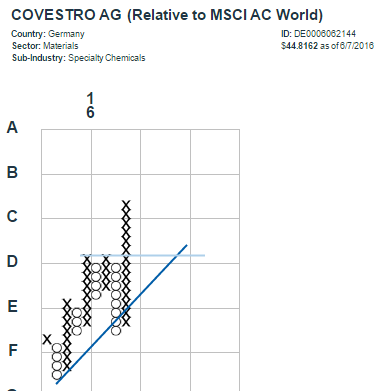

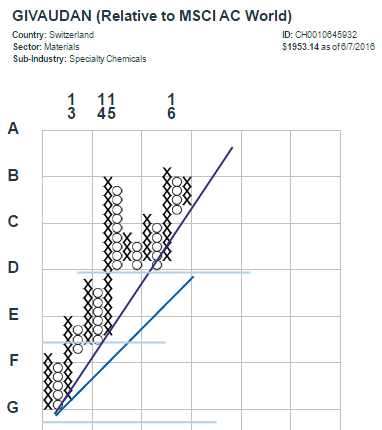

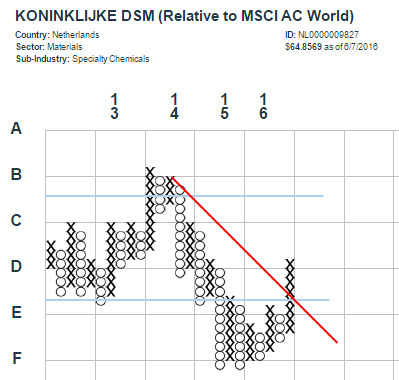

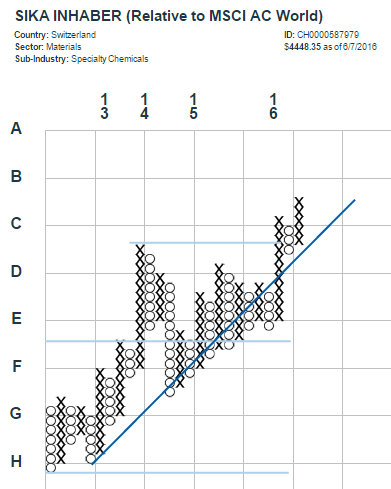

GKCI DM EMEA Materials (late cyclical)

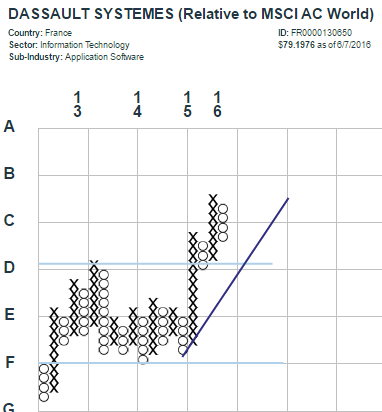

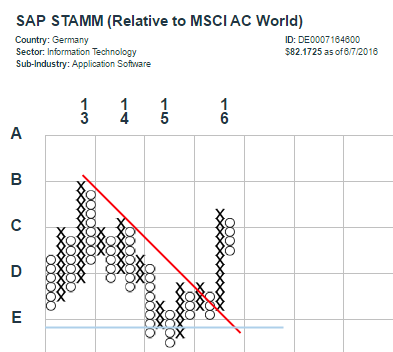

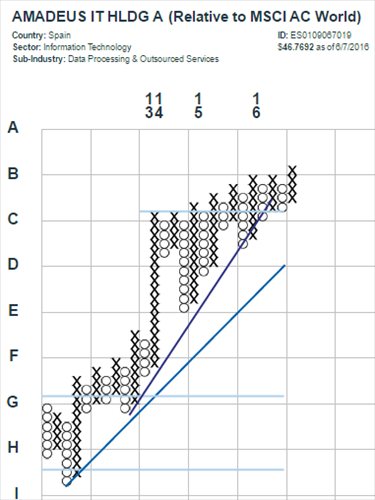

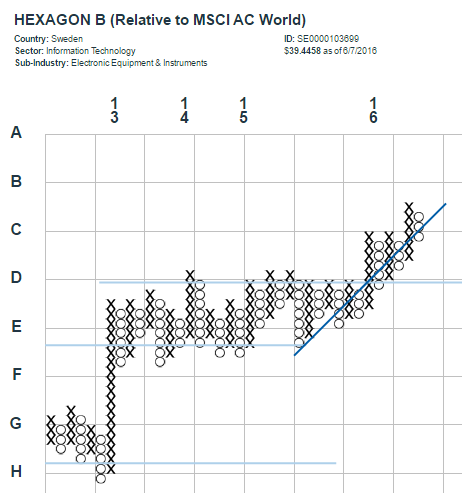

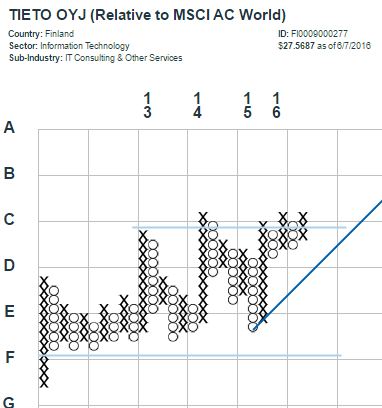

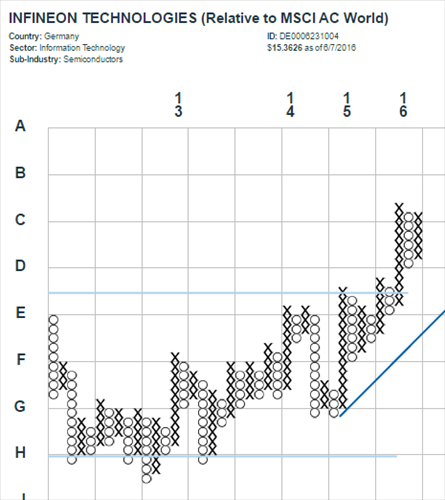

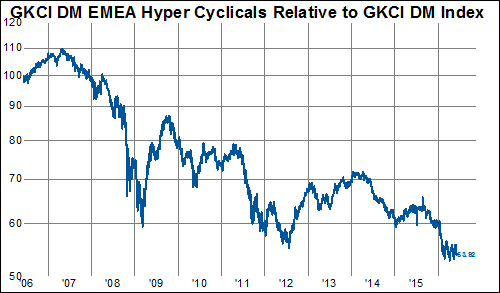

GKCI DM EMEA Information Technology (hyper-cyclical)

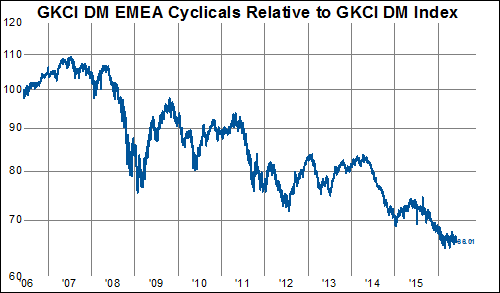

Now, before anyone gets really excited for us to harp on something other than the outperformance of growth counter-cyclicals, refer back up to the relative performance chart at the beginning and realize that the very persistent uptrend has NOT broken down just yet. Has it softened/ moderated somewhat? Sure. And relative performance of the overall cyclicals basket appears to be attempting to form a base so far this year:

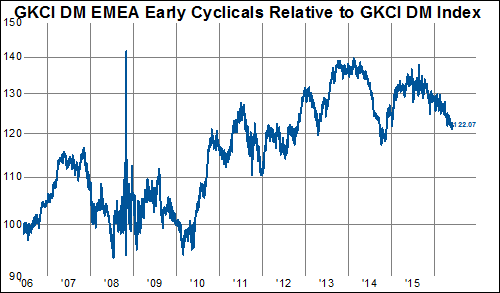

Among cyclicals, however, there are very different trends. Early cyclicals (Consumer Discretionary) looks pretty terrible while the hyper cyclicals basket, a combination of Information Technology and Financials, is dominated by the underperformance of stocks belonging to the latter sector. And then we have the late cyclicals, where the Industrials and Materials have managed to overcome extreme weakness among Energy stocks to put in a small base over the last few months.

While we maintain a relatively large bias towards more defensive, counter-cyclical stocks, more recent (and more constructive) trends in DM EMEA cyclical sectors have undoubtedly piqued our interest.