Reserve Bank of India - Second Bi-Monthly Monetary Policy Review

Policy Rates Remain Unchanged – As expected

The Reserve Bank of India (RBI) quite expectedly kept the key policy rates unchanged at 6.5 percent, in its second bi-monthly monetary policy review. It also kept the cash reserve at 4.0 percent, to provide liquidity as required but progressively lower the average liquidity deficit in the system from one percent of NDTL to a position closer to neutrality.

In its bi-monthly monetary policy statement of April 2016, the RBI had stated that it would watch macroeconomic and financial developments in the months ahead with a view to responding as space opens up. However, as the incoming data since then showed a sharper-than-anticipated upsurge in inflationary pressures emanating from a number of food items (beyond seasonal effects), as well as a reversal in commodity prices, Reserve Bank decided to keep the rates on hold.

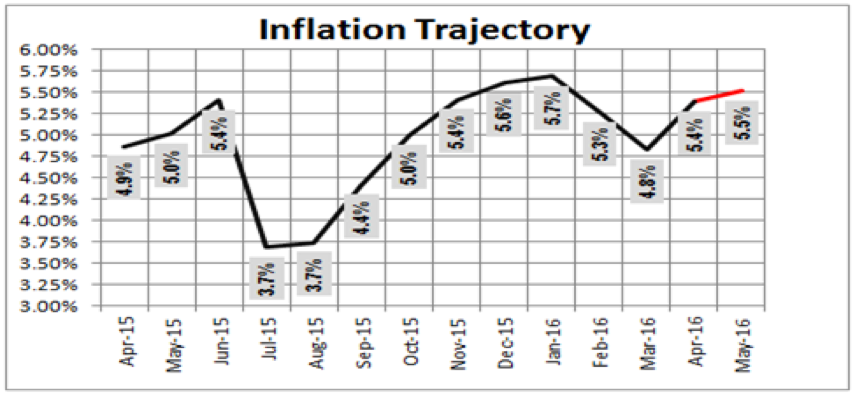

Inflation Projection - maintains March-17 target of 5%, but with upside risk

RBI while maintaining its inflation target of 5% by March -2017, has flagged off upside risk to its projections. While pointing to the recent spike in April inflation figures, RBI stated that firming international commodity prices, particularly of crude oil; the implementation of the 7th Central Pay Commission awards and the stickiness in core inflation pose risks to its inflation target. However, a good monsoon with reasonable spatial and temporal distribution, along with various supply management measures should moderate unanticipated flares of food inflation. In addition, capacity utilisation indicators suggest that the available headroom in industry could keep output prices subdued even as demand picks up.

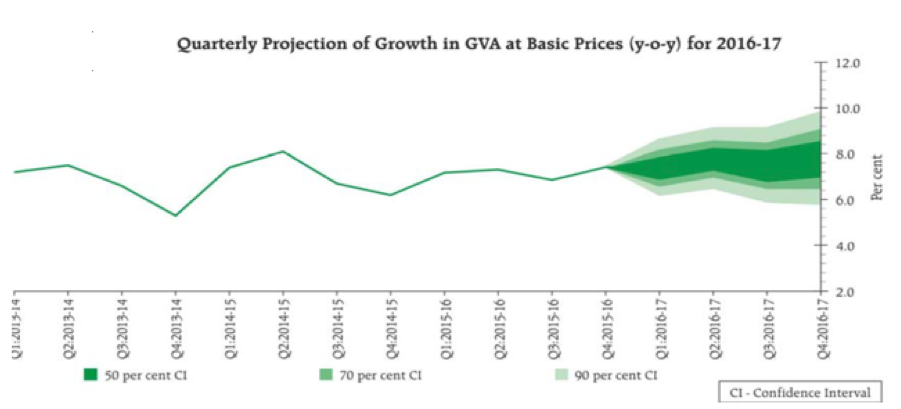

Growth Projection – GVA Growth retained at 7.6%

Noting a gradual improvement in domestic conditions for growth, RBI maintained the GDP growth on GVA basis at 7.6%. A normal monsoon along with implementation of 7th Pay Commission award is expected to drive the consumption demand. Besides, the higher public sector capital expenditure, led by roads and railways, likely to offset the subdued appetite for fresh private investment due to financial stress.

Trajectory of Monetary Policy - Remain accommodative, however further rate reduction looks increasingly difficult.

RBI has done a cumulative policy rate cut of 150 bps since Jan-15, and we believe that further easing space might be very limited. RBI in the latest policy, has maintained that the stance of the policy remains accommodative and will monitor macroeconomic and financial developments for any further scope for policy action. However, we think that, given the recent spike in inflation, stickiness of core inflation and the uptick in commodity prices, meeting the 5% inflation target may be a challenge and expecting further easing of policy rates by RBI looks increasingly difficult, unless food prices fall faster than we expect or oil prices do not rise further

Market Reaction & Outlook

As the RBI’s policy action was in line with the consensus estimate, the reactions to the policy has been rather muted. In fact sovereign bond yields has been trading in a very narrow range in the last 2 months, after a major rally in the month of March-2016.

A 25 bps cut in policy rates in April and the change in the liquidity management frame work, under which RBI induced durable liquidity through OMO purchases to the tune of Rs.700 in the last 2 months, has hardly made an impact on the yields. The major reason for this range-bound movement has been the inflation situation, which has started moving up, keeping the bond market on a cautious note. In the near term we expect the market to watch closely inflation trend and the progress of monsoon.

Market will also closely watch the impact on the liquidity on account of maturity of the forward FX purchases of RBI. It may be noted that, RBI had introduced FCNR (B) Scheme during 2013 crisis to attract dollars from NRI’s. Approximately USD 26bn of USD inflows by way of FCNR deposits largely of 3 years maturity, were collected by banks which were swapped with RBI using FX sell/buy swap for maturity corresponding to that of underlying FCNR deposit. We now expect an outflow of around USD 24 bio on repayment of FCNR (B) deposits during September-November -2106.

While the RBI has fully covered its forward sales through forward market purchases during 2014, these forward purchases are largely front-running the FCNR (B) swaps with regard to maturity. If the RBI allows these forward positions to mature, which in our view is likely, it will lead to banking liquidity to turn neutral by July or August, and a pause on OMOs during this period. Given that liquidity will be ample during this period, we expect shorter end of the curve to remain well anchored. However, a pause in OMOs during this period may weigh on the longer end of the curve.

However during the second half of the fiscal year, there are various factors that will lead to a draining of INR liquidity: 1) a fall in INR liquidity because of FX reserve depletion, reversing the earlier accretion on account of maturing FX forwards; 2) a currency-in-circulation leakage that typically occurs after September during the festive season and 3) the government typically builds up balances in the second half of the fiscal year. To offset tight liquidity conditions in the banking system, we expect the RBI to take a proactive approach, through OMO purchases, which should keep the 10 year bond in 7.40-7.60 range.

Disclaimer: The views expressed in this article are personal in nature. It do not construe to be any investment, legal or taxation advice. Any action taken by the reader or recipient on the basis of the information contained herein is reader’s/recipient’s responsibility alone and Tata Asset Management Limited will not be liable in any manner for the consequences of such action taken by reader / recipient.