KEY TAKEAWAYS

- Improving economic growth and rising Fed rate hike risks make the current bond market environment similar to 2015.

- Pressure may remain on high-quality bond prices, but we do not envision a repeat of the second quarter 2015 bond sell-off as Europe remains a key differentiator.

The trajectory of high-quality bond yields so far in 2016 is looking eerily similar to 2015, when a second quarter bond sell-off caught investors by surprise. Differences are present but a simple chart (lagging the 2016 data by just 10 days) illustrates how Treasury yields may be taking the same course in 2016 as in 2015 [Figure 1].

Treasury yields in both 2015 and 2016 fell sharply to start the year before rising late in the first quarter. The bounce higher in bond yields was, however, much stronger in 2015 compared to the narrower trading range that has characterized the bond market since early February 2016.

Last week’s Treasury sell-off raises the question of whether a 2015-like bond market sell-off, which occurred around the same time of year, may be repeating in 2016. In 2015, Treasury yields began to move higher in late April as economic growth expectations began to improve and Federal Reserve (Fed) rate hike expectations also increased. First quarter economic growth in both 2015 and 2016 was weak but improvement followed. Consensus forecasts for the second quarter of 2016 call for a 2–2.5% growth rate at this early stage—a notable advancement. .

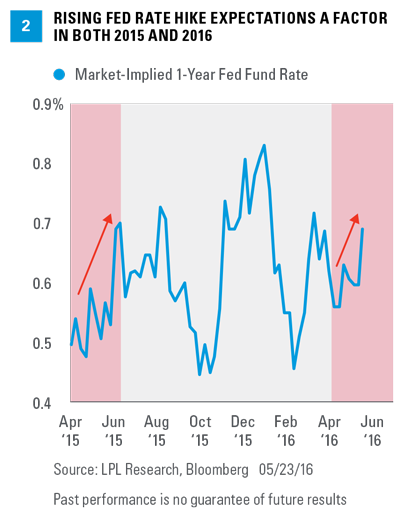

Similarly, both rising Fed rate hike expectations and better growth expectations were responsible for last week’s jump in Treasury yields. Fed rate hike fears were by far the dominant driver, so it’s not surprising that Fed rate hike expectations also increased in the second quarter of 2015 [Figure 2]. The magnitude of the move was much greater in 2015, but 2016 is starting from a higher base given the December 2015 rate increase.

Even after last week’s sell-off, a June rate hike is only priced in at a 33% probability, and high-quality bond prices may still be vulnerable to further weakness if the pattern of 2015 is ultimately repeated. After scrutinizing the release of the April 26–27, 2016 Federal Open Market Committee (FOMC) meeting minutes last week, most investors still doubt the Fed will move in June, leaving expectations relatively modest. A rate hike in June is still not anticipated but remains a potential risk.

A DIFFERENT PATH IN EUROPE

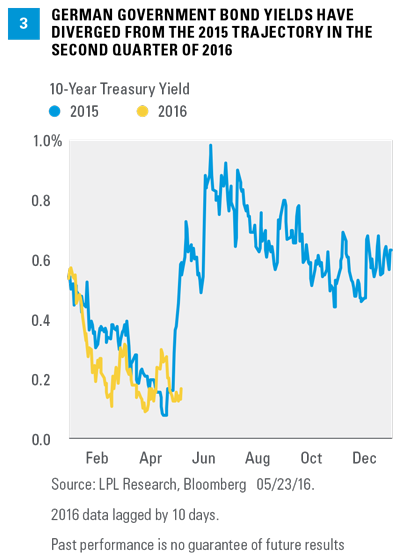

Europe is a differentiating factor in 2016 compared to 2015. The path of the 10-year German government bond yield also showed a similar pattern in both early 2015 and 2016. In 2015, expectations of additional European Central Bank (ECB) rate cuts and bond purchases boosted growth expectations during the second quarter. However, the path of the 10-year German bond yield has taken an almost opposite trajectory since the start of the second quarter of 2016 [Figure 3].

German government bond yields jumped higher in late March following bold policy action from the ECB. With the market growing skeptical of the effectiveness of such policy, and Europe still showing sluggish economic growth, a meaningful turn higher in German bond yields has yet to materialize.

In 2015, Europe was the epicenter of the global bond sell-off during the second quarter. So far in 2016, a similar pattern is not developing and suggests extrapolating a similar sell-off is premature.

Aggressive rate cuts by central banks globally since the middle of 2015 and the growth in the amount of negative yielding government bonds could once again lend support to U.S. Treasuries and avoid a repeat of the second quarter 2015 sell-off. Treasury yields remain among the highest developed country bond yields and continue to benefit from strong overseas demand, which should limit, or slow, any rise in yields.

On the flip side, a key catalyst for a reversal in the global bond sell-off in 2015 was a renewed decline in oil prices. Although renewed oil weakness could once again be a source of strength for bonds, the price is starting from a much lower base level. Furthermore, supply and demand are much better aligned today than at the start of the year, which indicates a similar oil shock is possible but unlikely in 2016. This suggests oil may be a headwind for bonds rather than a catalyst for a reversal.

CONCLUSION

The U.S. bond market may continue to trade cautiously, but the start of a sharp bond sell-off similar to the second quarter of 2015 is unlikely to take hold in our view. Europe, a key driver of last year’s weakness, has witnessed aggressive policy action but still sluggish growth, causing investors to question the effectiveness of bold policy. A knee-jerk jump in yields seems unlikely unless confirmed by a substantial improvement in economic data. Aggressive monetary policy overseas and the increase in the amount of bonds with negative bond yields has helped keep demand for U.S. bonds elevated. The favorable demand backdrop for U.S. bonds should limit the potential rise in yields.

Finally, the message from the U.S. bond market has remained unchanged in the days after the release of the April FOMC meeting minutes—rate hikes pose a risk to growth. The yield curve, as measured by the yield differential between 2-year and 10-year or 30-year Treasury yields, has continued to flatten. Fed risks may maintain pressure on high-quality bond prices but we do not expect a repeat of the 2015 bond market sell-off that saw the 10-year Treasury yield rise by 0.6% in just over two months.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indexes are unmanaged and cannot be invested into directly.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values and yields will decline as interest rates rise, and bonds are subject to availability and change in price.

Government bonds and Treasury bills are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. However, the value of fund shares is not guaranteed and will fluctuate.

Investing in foreign fixed income securities involves special additional risks. These risks include, but are not limited to, currency risk, political risk, and risk associated with foreign market settlement. Investing in emerging markets may accentuate these risks.