Newsletter, Volume 9, No. 3 - May 2016

IT REALLY HAPPENED!!

I still find it hard to believe; however, the Department of Labor actually issued its long-awaited Fiduciary Rule. Investment News did an outstanding job of describing the history of the process that led to the final issuance. Also, if you make it to the end of the story, you’ll be treated (?) to a video interview I did on the story.

DID I READ THIS CORRECTLY?

Wonder why they needed a rule? From an on-going “debate” on a professional blog site, emphasis mine:

“Again you don’t get it. Making us Fiduciaries takes away arbitration. That was the reason it didn’t make sense to sue prior. If we are all Fiduciaries we are responsible for any advice we give. That’s the problem. None of your high and mighty excuses or rationalizations is going to save us from an onslaught of lawsuits.”

Imagine the horror of being responsible for the advice we give!!! I don’t know how I’ll sleep at night.

COMING SOON TO A STORE NEAR YOU

From USA Today: “Fear knot: Nike’s self-tying shoes are here”

It seems that after a ten-year technology project, Nike has it figured out. As soon as you put on a pair and hit the “+” button, your shoes are tied. Want “out?” Hit the “-.”

First we hear that cursive writing is being eliminated, now shoe tying. What next? Driving?

INTERESTING

As reported in Investment Advisor, Senator Elizabeth Warren noted that “firms like Prudential Financial, Lincoln National, Jackson National and Transamerica have publically chided DOL’s rule to change the definition of fiduciary under the Employment Retirement Income Security Act (ERISA), they are telling their investors the rule ‘will have no significant impact on the companies.’” The Senator went on to note, “Publically traded companies are rarely held accountable for the assertions they make when lobbying in Washington, even if these assertions are untrue. But when communicating with investors, publically traded companies are required by law to provide full and accurate information about any material matters that may affect their business models and valuations.”

A BIT OF SOBERING HISTORY

MORE GURUS BITE THE DUST

From the Wall Street Journal:

“Marc Levine, chairman of the $16 billion Illinois State Board of Investment, had a provocative question this month during a board meeting about hedge funds. “Why do I need you?” Mr. Levine asked. A lot of big investors are asking the same question. Pension funds, insurers and university endowments helped pump up hedge funds to a record $3 trillion in assets over the last decade. But with results falling behind the total return of the S&P 500 for seven straight years and the high-fee structure now politically sensitive in some states due to mixed results, many of them are pulling back.”

MORE SOBERING STUFF

From my partner Lane. If you thought the market seemed rocky, you’re right.

WE’RE OPEN FOR BUSINESS

I’ve never made a pitch for our firm in my NewsLetter, but I found this so amazing I couldn’t resist.

At J.P. Morgan, $9 Million in Assets Isn’t Rich Enough

Firm’s private bank is doubling the minimum to $10 million in investible assets for clients

Wall Street Journal:

“JPMorgan is getting significantly choosier when it comes to its private banking clientele, raising the threshold for such tailored wealth management 100% to $10 million…. Customers with less than $10 million in investable assets, meanwhile, will be migrated to the company’s Private Client Direct platform, people familiar with the move tell the Journal.The difference between the two platforms can be stark: private bank teams usually handle a “few dozen clients” at a time, while Private Client Direct teams, which are sometimes just half the size of the private bank teams, support around 100 customers on average, people familiar with the matter tell the publication.”

If you happen to be one of the “poor” people affected by this policy change, we’d be happy to chat with you at Evensky & Katz/Foldes Financial. We believe that $1 – $10 million is serious money and we provide very personalized planning for clients with those assets.

ON ONE HAND AND ON THE OTHER

The recent April Barron’s Big Money Poll (a survey of some of the nation’s top money managers) found:

62% believe the market is fairly valued.

26% believe it’s overvalued.

11% are bullish, 19% are bearish, and 70% are neutral.

However:

Only 32% expect the market to rise by 10% or more in the next 12 months and

66% expect it to fall by 10% or more.

Sector choices:

Best – Basic Materials 12%; Consumer cyclicals 7%; Consumer staples 9%; Financials 11%

Worst – Basic Materials 12%; Consumer cyclicals 6%; Consumer staples 8%; Financials 10%

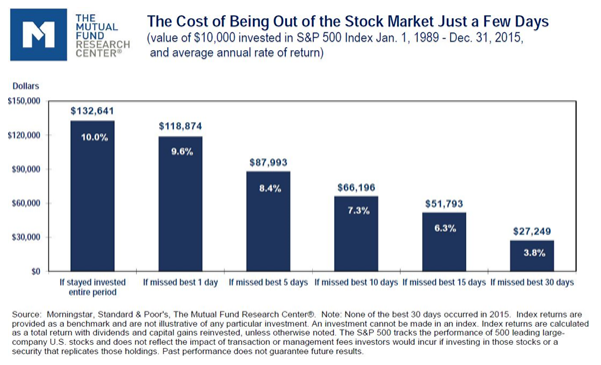

WOULD BE MARKET TIMERS – KEEP THIS IN MIND

This excellent chart by the Mutual Fund Research Center echoes the warnings about market timing that I’ve highlighted in past NewsLetters.

TERRIFIC

There will be more company for us old fogeys. From my friend Mary Beth Franklin in Investment News:

“Between 2016 and 2035, the number of Americans age 65 and older, currently about 65 million, is expected to increase by 57%, nearly triple the rate of growth of the 35- to 44-year-old population and more than 10 times the rate of the 25- to 34-year-old cohort during the same 20-year period.”

I’M SHOCKED!!!

It seems not only market timers have troubles. A recent study by two Wharton professors analyzed the historical performance of Jim Cramer’s Action Alert PLUS portfolio from 2001 to 2016 (since the inception of the portfolio and the recommendation was made on “Mad Money”) and found that he significantly underperformed the S&P 500 both in absolute terms and on a risk-adjusted basis.

Thank you, Wharton….

INTERESTING STATISTIC

From an IMCA White Paper:

“In terms of their relationships with financial advisors, consumers are beginning to expect a fiduciary standard, even if they are not familiar with the terminology. More than 75 percent of investors expect all financial professionals offering fee-based advice to act in their clients’ best interest in all aspects of the financial relationship. The same percentage indicated they would not seek services from a broker if they knew the broker was not required to act in their best interest in all aspects of the financial relationship.”

If you or you know someone who is not clear whether an advisor is acting in his or her best interest, you might want to have a copy of our Fiduciary Committee’s simple “Mom-and-Pop” Put My Interest First Oath. Just drop me a note at [email protected] and I’ll send you a copy.

DID YOU KNOW?

At least according to a list my friend Leon sent:

• In more than half of all states in the United States of America, the highest-paid public employees are college sports coaches.

• It costs the U.S. government 1.8 cents to mint a penny and 9.4 cents to mint a nickel.

• Apple has more cash than the U.S. Treasury.

• Alaska has a longer coastline than all of the other 49 U.S. states put together.

• The city of Juneau, Alaska, is about 3,000 square miles in size. It is actually larger than the entire state of Delaware.

• Montana has three times as many cows as people.

• The grizzly bear is the official state animal of California, but no grizzly bears have been seen there since 1922. They are plentiful in Mississippi, Tennessee, and other southern states, however.

• The United States has 845 motor vehicles for every 1,000 people.

CAN YOU BELIEVE?!

Mena sent me this and observed, “We can now all move to the North Pole while still [being] able to consult with our doctor. [We] just need an Internet connection.”

GUNS UP

For those not in the know, the two-finger sign “Guns Up” is the symbol for Texas Tech. Mrs. Laura Bush joined Deena in saluting the University after their presentations at a recent conference.

A GOOD GIG …

From Bloomberg: “Five years after Occupy Wall Street protesters took over Zuccotti Park in downtown Manhattan, spawning a national discussion about the divide between America’s highest and lowest earners, the pay gap has only gotten wider. Now, even as bankers bemoan their declining bonuses and job prospects, it’s helping fuel the campaigns of Donald Trump and Bernie Sanders.

The spread is even more pronounced over the past 25 years. When adjusted for inflation, wages for investment bankers and securities-industry employees, including salary and bonuses, increased 117 percent from 1990 through 2014, according to U.S. Bureau of Labor Statistics data. Over the same period, wages for all other industries rose just 21 percent, to $51,029 in 2014, about one-fifth of the $264,357 that bankers and brokers earned that year.”

I’ll bet that the new Department of Labor (DOL) Fiduciary Rule will put a crimp in the growth.

… AND A GOOD TIP

With all of the news on the DOL Fiduciary Rule comes this tip from Ron Lieber in the New York Times:

“… [Y]ou cannot be too wary when turning your money over to a financial professional.… If your broker does have disclosures (and you should check every year or so for new ones that may have popped up), ask some questions. If the response is defensive, that ought to tell you something. If brokers don’t like answering your inquiries, perhaps they ought to work in an industry where there isn’t as much disclosure.

If the response is unintelligible, keep pressing. If the brokers have gotten in trouble for pushing complex products that you (or they) don’t understand, then that is a significant sign as well. The money management industry is much too complicated, and it’s not your job to translate the gibberish that some of its sales agents spew.

For any of these conversations to happen, however, you have to dive into BrokerCheck [http://brokercheck.finra.org/] in the first place. It takes 60 seconds. Do it right now; you’ll find links to the records of many financial planners in there as well.

Too many people do not do this, which is a source of endless frustration and sadness to people like Professor Matvos. ‘Despite the information being out there, the most vulnerable people don’t know that it’s there,’ he said. ‘The big puzzle we face is how do we get those people to use the information at their disposal?’”

Professor Matvos was one of the authors of the “bad broker” research I reported in my last NewsLetter.

This is yet another good reason to use the Fiduciary Committee’s simple “Mom-and-Pop” Put My Interest First Oath.

ACTIVE OOPS

From Yahoo Finance via CNBC: “Much of the past decade has been rough for active fund managers, but 2016 hasn’t been just bad, it’s been history-making bad.

Fewer than 1 in 5 large-cap funds beat the S&P 500, the lowest level since at least 1998, the furthest back Bank of America Merrill Lynch data go. (The S&P gained 1.4 percent in the first quarter.) For growth-focused funds, the news was even uglier: just a 6 percent beat rate at a time when the S&P benchmark has gained just over 1 percent year to date.

Value managers did a bit better with a 19.6 percent beat rate, while core funds fared comparatively well, with 29 percent topping the benchmark. However, results declined each month through the year.

‘The recipe for distress may boil down to a few factors,’ Savita Subramanian, BofAML’s equity and quant strategist, said in a report for clients. She pointed to high levels of correlation, or the tendency of stocks to move in the same direction at once, which translates into difficulty topping basic market benchmarks.”

A FEW THOUGHTS FROM MY #1 SON

• I find it ironic that the colors red, white, and blue stand for freedom, until they’re flashing behind you.

• I changed my password to “incorrect,” so whenever I forget it, the computer will say, “Your password is incorrect.”

• Hospitality is the art of making guests feel like they’re at home when you wish they were.

• There may be no excuse for laziness, but I’m still looking for it anyway.

• Women spend more time wondering what men are thinking than men spend thinking.

• Is it wrong that only one company makes the game Monopoly?

• Change is inevitable, except from a vending machine.

• The grass may be greener on the other side, but at least you don’t have to mow it.

• If at first you don’t succeed, skydiving is not for you.

• Money is the root of all wealth.

PATIENCE PAYS

Diversification isn’t just a fancy word; it’s a powerful planning tool to mitigate market risk. Recent markets provide a good example of why you might not want to bail out of a poorly performing investment or jump into a hot one.

From 1/8/2015 to 1/8/2016, of the 66 funds we monitor and use in portfolios, these were at the bottom:

55 of 65 iShares S&P Mid-Cap 400 Value

61 of 65 iPath® Pure Beta Broad Commodity ETN

62 of 65 iShares North American Natural Resources

63 of 65 iPath® Bloomberg Cmdty TR ETN

64 of 65 US Global Investors Global Res Instl

65 of 65 Goldman Sachs MLP Energy Infras Instl

From 1/1/16 to 5/16/16 these were among the top funds:

1 of 65 iShares North American Natural Resources

2 of 65 iPath® Pure Beta Broad Commodity ETN

4 of 65 US Global Investors Global Res Instl

6 of 65 iShares Edge MSCI Multifactor USA Sm-Cp

11 of 65 iShares S&P Mid-Cap 400 Value

Another way of looking at it:

From 1/16/2016 to 5/15/2016:

12 funds that underperformed the market from 1/8/2015 to 1/8/2016 were outperforming from 1/16/2016 to 5/15/2016.

10 funds that outperformed the market from 1/8/2015 to 1/8/2016 were underperforming from 1/16/2015 to 5/15/2016.

To wrap it up, a few last observations about the DOL Rule

WHY?

From AARP, The High Cost of Bad Advice

• Reduced investment returns of 1 percentage points annually

• An estimated $17 billion annual loss for IRA investors

• Running out of money five years earlier after 401(k) is rolled into an IRA

• An estimated $12,000 loss by rolling a $100,000 account into an IRA

MY, OH MY

Two of the main arguments against the Department of Labor’s proposed “Fiduciary Rule” are highlighted in an American Council of Life Insurers paper on “Concerns about the Proposed Fiduciary Regulation,” namely:

• Millions of existing small-balance IRA owners are likely to lose access to the financial advisor of their choice or any financial advisor at all.

• The majority of others will face higher costs when providers shift brokerage accounts to advisory accounts.

A recent announcement by LPL (the largest organization of independent financial advisors in the U.S.) makes that position sound like Chicken Little. From InvestmentNews: “LPL cuts prices on its portfolios… LPL also is lowering minimums.”

Jim Weddle, managing partner at Edward Jones, when discussing new accounts with lower minimums, told the Wall Street Journal, “‘We reshaped the offer,’ Mr. Weddle said. ‘No one wants to be regulated out of serving clients.’”

A FINAL THOUGHT

If investing is exciting, then you’re not investing. I hope you have a wonderful summer; it’s just around the corner (I hope). See you again in a few months.

Harold R. Evensky, CFP®, AIF®

Chairman

Evensky & Katz / Foldes Financial Wealth Management

© Evensky & Katz / Foldes Financial Wealth Management

© Evensky & Katz / Foldes Financial Wealth Management