- Central banks globally are hampered by market expectations and unpredictability.

- Asset markets continue to be volatile and react in nontraditional ways.

- Political uncertainties in the U.S. presidential elections and the U.K. Brexit referendum have lessened some, but continue to hang over the markets.

Something’s gotta give. The global growth environment remains subpar — stable but at a disappointingly sluggish pace. Central bankers, where possible, continue to ease policy, but the financial market reaction is increasingly unpredictable. In this environment, the predominant theme this year has been a bounce back in the most beaten-down assets — including commodities and emerging markets. The bounce back in commodity prices is driven more by a rationalization of supply than a major change in the outlook for demand. Economic reports have been softer out of the United States in recent months, while they modestly improved in Europe, Japan and emerging markets. Global manufacturing continued to struggle in April, while the services sectors showed better growth.

On the monetary policy front, the Federal Reserve remains in a difficult spot. Undoubtedly, it would like short-term interest rates to be higher than they are today. However, the Fed is boxed in by market expectations — investors are expecting just one rate hike over the next year. The European Central Bank (ECB) continues to favor easy policy, especially in front of the risk of the “Brexit” referendum, but it needs to manage conflicting internal views. In Japan, the Bank of Japan (BOJ) must be confused by market expectations — in recent months there’s been a negative market reaction to both its loose and tight monetary policy. In this environment, the tighter linkages between the Chinese government and its central bank (the People’s Bank of China) allows for more direct policy action.

While the outlook for growth and monetary policy remain fairly static, asset markets are anything but placid. Asset prices have been volatile this year, often acting in nontraditional ways. Even though a 25% jump in oil prices has supported both commodities and high yield bonds, fixed income investors have driven the 10-year Treasury yield from 2.27% to 1.70% — surely not a sign of inflation worries. Gold has also jumped 20%, driven by investors seeking a hedge against the declining effectiveness of central banks and concerns over currency values. Risk asset markets may continue meandering until “something gives” — leading to a major break in either fiscal or monetary policy. We remain moderately overweight risk assets, as we assess the potential for something to break the global economy out of its current melancholia.

U.S. EQUITY

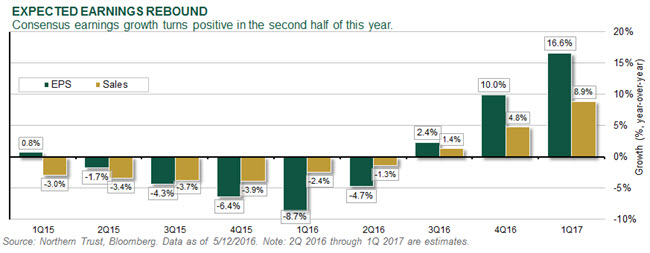

- Sales and earnings per share (EPS) remained in the red in the first quarter, weighed down by energy.

- Growth is expected to become positive after the second quarter.

Sales and earnings growth in the first quarter remained negative. Excluding the energy sector, sales grew slightly, while EPS fell by 4%. Growth in the second half is expected to rebound sharply, aided in part by a rebound in commodity prices and the weaker dollar. The consumer discretionary sector is the key, and trends have been mixed at best. Retail earnings significantly disappointed this quarter — calling into question whether consumers may be pulling back or spending on experiences instead of goods. We expect future earnings growth that’s more conservative than consensus, but valuations aren’t unreasonable. With growth likely to become positive in the second half of the year, we remain constructive on U.S. equities.

EUROPEAN EQUITY

- The ECB held rates steady at its April meeting.

- Inflation remains tepid but the underlying economic picture brightens.

After unleashing a barrage of dovish measures at its March meeting, the ECB reaffirmed its accommodative stance in April but otherwise stood pat. Despite its inaction, the ECB made certain to reassure jittery markets by noting that it remains at the ready with “all instruments available.” However, underlying data suggests improved economic traction. In particular, eurozone gross domestic product (GDP) is estimated to have grown 1.6% year-over-year in the first quarter, unemployment dropped to its lowest rate (10.2%) in almost five years, and an ECB survey indicated an easing of credit and increased demand for bank loans. Recent equity and commodity market stability also undoubtedly lent support to the ECB’s latest wait-and-see decision. While headwinds remain — including tepid inflation, a stronger euro and the Brexit referendum — recent green shoots could prove supportive of equity markets.

ASIA-PACIFIC EQUITY

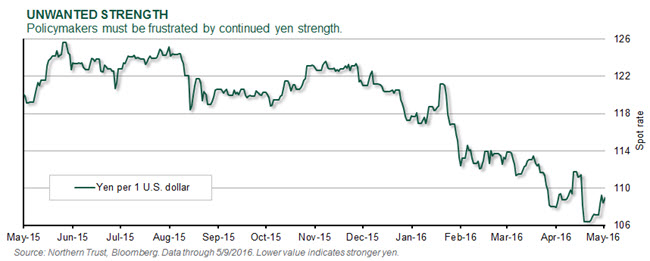

- Despite market pressure for action, the BOJ held rates steady in April.

- The yen continues to strengthen and equity markets decline in the wake of BOJ inaction.

With unwanted appreciation in the yen potentially undermining Japan’s export-driven economy and derailing consumer spending, speculation was rampant that the BOJ would unleash further easing measures in April. Despite this market pressure, the BOJ held policy steady and decided to further evaluate the impact of negative-rate measures implemented in February. Unsurprisingly, the BOJ’s inaction led to the yen strengthening another 3%, and equity markets dropped about 6%. The BOJ attempted to reassure the market by noting that, “there is plenty, plenty of room to push down the negative rate” and that it will “do whatever is necessary.” With a strong yen likely to weigh negatively on both corporate and consumer behavior in the near to medium term, it’s not surprising that the BOJ cut its GDP and inflation forecasts.

EMERGING-MARKET EQUITY

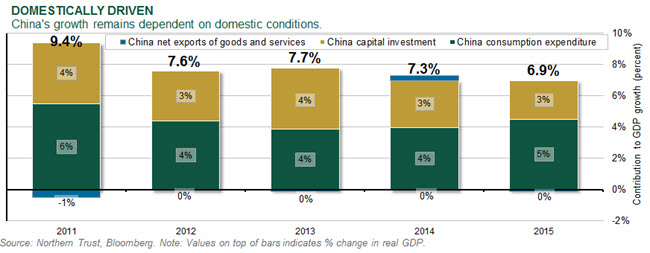

- Volatility in Chinese growth data continues.

- We see short-term stability, but expect longer-term slowing in China.

While China’s meteoric economic rise has been helped by its powerful export capability, domestic activity is a more important driver of overall growth. This is increasingly true as global growth has slowed and global trade flows have decreased correspondingly. Even though economic data reported for April showed some slowing from March, the context is important because March was particularly strong. Year-over-year growth of 6% in industrial production was down from 6.8% in March, but was well above the lows of the last year. Fixed-asset investment also slowed from 11% in March to 10% in April, but that level is broadly consistent with activity over the last year. We believe that Chinese policy makers will continue to seek to reduce the downside risk to the economy through targeted stimulus. Longer term, we expect high debt levels to constrain growth and to lead to growth slowing to below 5%.

REAL ASSETS

- Oil prices continue their march upward in a slow-growth environment.

- Fundamental headwinds are being offset by other developments.

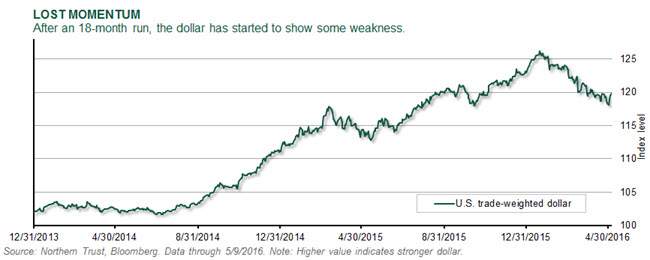

Global growth remains subdued and oil inventories remain near record levels, but this hasn’t stopped oil prices from continuing their upward march. The approximate 80% increase in the price of oil since mid-February has been driven by speculation of supply cuts. More recently, these supply cuts weren’t from the anticipated OPEC production cuts. Rather, wildfires in Canada and sabotage in Nigeria were the culprits. Nevertheless, the resulting price action is to be expected when spare capacity is tight and prices are low. Recent dollar weakness has also removed one of the major headwinds to oil prices. We believe a lower Fed policy trajectory reduces the odds of the resumption of dollar strength. These developments help offset continued fundamental challenges, prompting us to reduce our natural resources underweight this month.

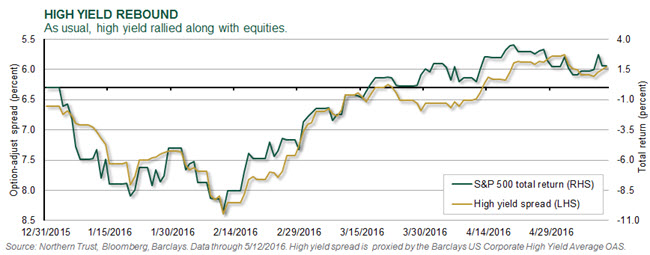

U.S. HIGH YIELD

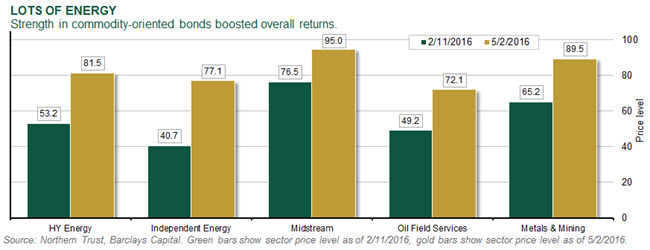

- High yield has gained more than 13.5% after declining 5.2% to start the year.

- Strong high yield returns have been driven by a recovery in distressed commodities.

High yield fell 5.2% through February 11 because of concerns about falling oil prices, banking sector volatility and fear of a Fed policy error. As oil has recovered into the $40 per barrel range, high yield has posted a strong recovery and is up close to 7% year-to-date. The strong returns have been driven by distressed commodity sectors. These sectors have so dominated returns that 32 of 45 index sectors have underperformed the index return. Although commodity prices have improved, it hasn’t been enough to fix fundamental issues, as seen by the 30 energy and metals and mining defaults so far this year. We’ve recently reduced our tactical overweight to high yield, reflecting the strong performance this year and the sizable level of our previous overweight.

U.S. FIXED INCOME

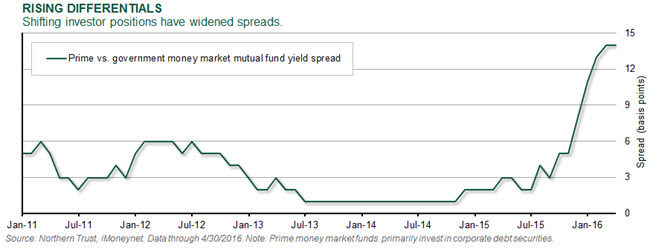

- Money market reform has begun to affect short-end market technicals.

- We expect continued widening of yields between government and prime money market mutual funds.

Amid a changing regulatory environment, institutional investors have begun to shift their cash into government money market mutual funds. SEC money market reform provisions that come into effect in October 2016 will subject institutional clients who remain in funds that take credit risk to variable net asset value (VNAV) pricing for the first time, as well as potential redemption fees and liquidity gates. As such, investors are gravitating toward government funds that will stay at a constant net asset value (NAV). As demand for higher-quality, short-term government paper increases, the yield differential between the two types of money market mutual funds has widened. We believe this trend will continue over the course of the year as many institutional investors reposition their cash portfolios into government funds.

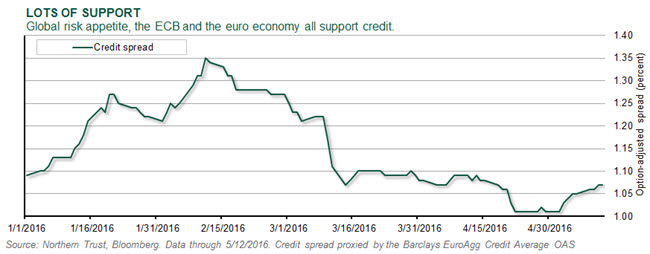

EUROPEAN FIXED INCOME

- European markets are staging a recovery.

- The U.K. referendum continues to dominate the outlook.

A variety of economic indicators suggest that momentum in the euro area has improved, with the ECB’s accommodative policy stance likely a help. Even as markets wait to learn the extent of the ECB’s asset purchasing intentions, corporate bond spreads have been narrowing sharply despite a step up in new corporate debt issuance. The only worrying sign is that the euro has strengthened recently, but this may encourage the ECB to take further action.. Polls for “Brexit” appear to be swinging back toward a vote to remain, yet the Bank of England continues to emphasize risks to both growth and inflation related to the event. The markets are now assigning little probability of an interest rate hike before 2018.

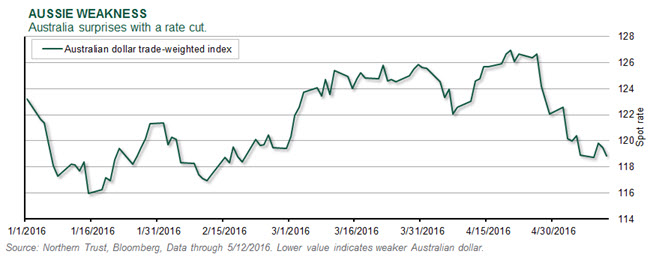

ASIA-PACIFIC FIXED INCOME

- The Reserve Bank of Australia surprises markets with an interest rate cut.

- Chinese economic data fails to allay fears of a slowdown.

The Reserve Bank of Australia announced a surprise 0.25% cut to its cash target rate at its May meeting to a record low of 1.75%, while markets were expecting only a dovish statement. Citing a lowered inflation outlook, the decision may have had the desired effect by weakening the currency from its strong appreciation earlier in the year. Even though commodity markets appear to have staged a recovery, it’s clear that the global inflation outlook is little changed. China’s GDP growth in the first quarter was confirmed at a respectable 6.7% year-over-year, but data releases since then highlight that activity remains soft with a decline in the PMIs and a mixed report on imports and exports. Against this backdrop, markets will look to the central bank to steady the ship’s course.

CONCLUSION

The most significant recommendation coming from our asset allocation discussions this month is the reduction of our recommended overweight to U.S. high yield bonds by 4%, reflecting the strength of their rally since the market lows in February. While we expect high yield to continue to generate attractive risk-adjusted returns during the next year, the magnitude of the opportunity has been reduced by the rally in high yield spreads in recent months. We also wanted to make this change while liquidity in the high yield market was relatively good. We’ve recommended splitting the proceeds evenly between natural resources (reducing our recommended underweight by half) and investment-grade bonds (where we still remain significantly underweight). We think a more stable outlook for China, along with a weaker U.S. dollar, reduce the downside risks around natural resources. The increased investment in investment-grade bonds was driven by a desire to not increase overall portfolio risk at this time, along with our sanguine outlook for interest rates.

As we assess the recent increase of populist politics across the globe, we counsel investors to not confuse the “message” with the “messenger.” Most pundits have been blindsided by the success of populist candidates in recent electoral campaigns, especially in the United States. We expect this populist pressure, driven by poor economic and weak income growth, to persist in coming years. This helps drive our “something’s gotta give” theme. Whether it’s an accelerated move away from austerity toward fiscal stimulus, or a shakeup of central bank leadership, pressure is building to try something different.

This pressure continues to feed our two biggest risk cases to the markets — that of Brexit and of the election of a populist U.S. president. Markets crave predictability, and the more anti-establishment the election outcome, the greater the uncertainty. We continue to expect Britain to vote to stay in the European Union, and while the betting sites support this view the polls are uncomfortably close. In the United States, the nominees on both the Republican and Democratic sides seem set, and the only thing we’re comfortable predicting about the six-month run up to the U.S. election is that it’ll be volatile! We’ll be analyzing the prospects for something “to give” on the fiscal or monetary policy front over the next year as a potential catalyst for the next big change in risk appetite.