The rising cost of college has added an additional financial burden for many parents who don’t want to see their children suffer under a mountain of student loan debt. This noble goal unfortunately has many sacrificing their own retirement nest egg to help secure their children’s future. Roger Michaud, senior vice president and director of sales for Franklin Templeton’s 529 College Savings Plan and chair emeritus of the College Savings Foundation—the leading nonprofit helping American families save for their children’s college education—says financing college isn’t just a savings issue—it’s a retirement issue.

When you ask most people why they invest, retirement is the number one answer given. There are many challenges associated with investing for retirement, including saving enough to fund the type of retirement they envision, developing a plan to meet long-term income needs, preparing for medical expenses and … financing education expenses?

For people without children, financing an education is not typically a primary investment focus. But for parents, financing college is often a top investment goal along with retirement—and can be a top source of stress.

Although saving for college is a top investment goal for many, it does not occur in isolation; financial goals are often intertwined. As such, financing education frequently has a direct and potentially negative effect on retirement. When asked to describe the impact of financing a college education on retirement planning, only 6% of those with children in Franklin Templeton’s 2015 College Savings Trends Survey said it would have no impact.1 So for the other 94%, what is the impact? You don’t need a master’s degree to figure out that answer!

College—Big Expense at the Wrong Time

As people are having children later in life, there is a greater chance that the college tuition bill for their kids will come due during their prime retirement savings years or, in an increasing number of cases, just as retirement approaches. This often leaves parents facing sticker shock and may lead to siphoning money from retirement savings.

If parents reallocate their savings from retirement to education, they are faced with the prospect of being unable to retire as planned due to a lack of savings. As a result, they often have to make the hard choice to retire later, or to retire as planned but with less money and perhaps a lower standard of living.

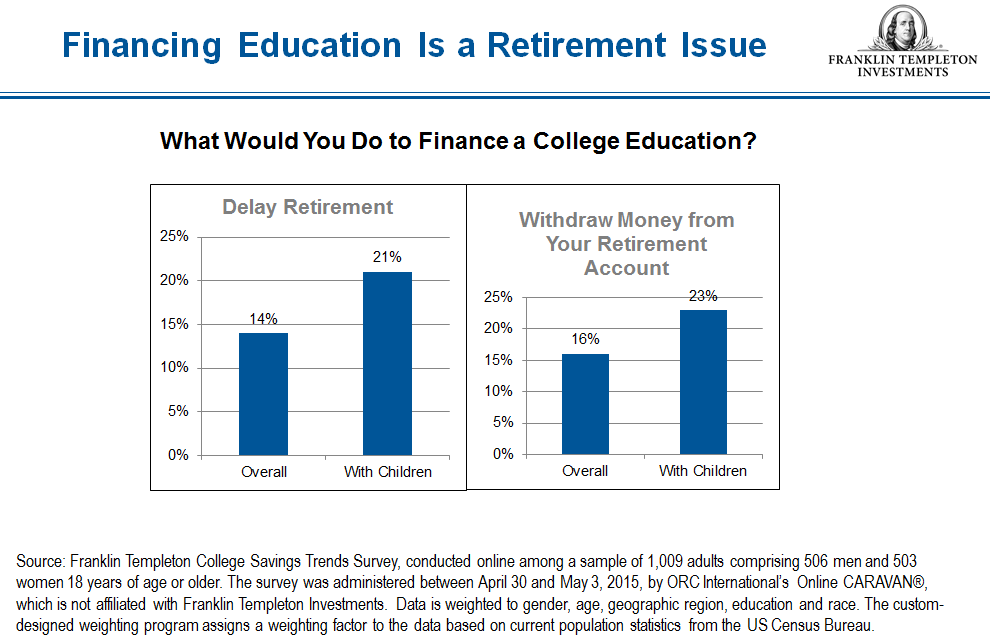

While the Franklin Templeton College Savings Trends Survey revealed 21% of those with children and 14% of all individuals said they would retire later to finance a college education, the Franklin Templeton 2016 Retirement Income Strategies and Expectations (RISE) Survey2 revealed delaying retirement is a common strategy that comes with a couple of pitfalls:

- As retirement draws near, people are less willing to delay retirement and more willing to reduce their retirement lifestyle.

- Nearly 25% of working individuals are unable to control when they retire because they are forced into retirement based on circumstances beyond their control.

Don’t Get Caught Stealing (from Yourself)

While delaying retirement may not be an optimal solution for those trying to finance education, I would argue it is much better than another common option—stealing! No, I don’t mean robbing a bank. I’m referring to those who withdraw from their retirement accounts to finance a college education. This should be done very cautiously. Taking money from a retirement account can fatally impact the ability to reach one’s retirement saving goals. Additionally, any withdrawal from a retirement account requires careful planning in order to understand the impact of penalties, fees, taxes and the impact on financial aid (since a withdrawal may be considered income).

According to a related survey from the College Savings Foundation, one-third of parents are still shouldering loan student debt from their own college days.3 That means these folks could be paying off (or defaulting on) debt well into retirement, and would therefore also have less funds available to help their children.

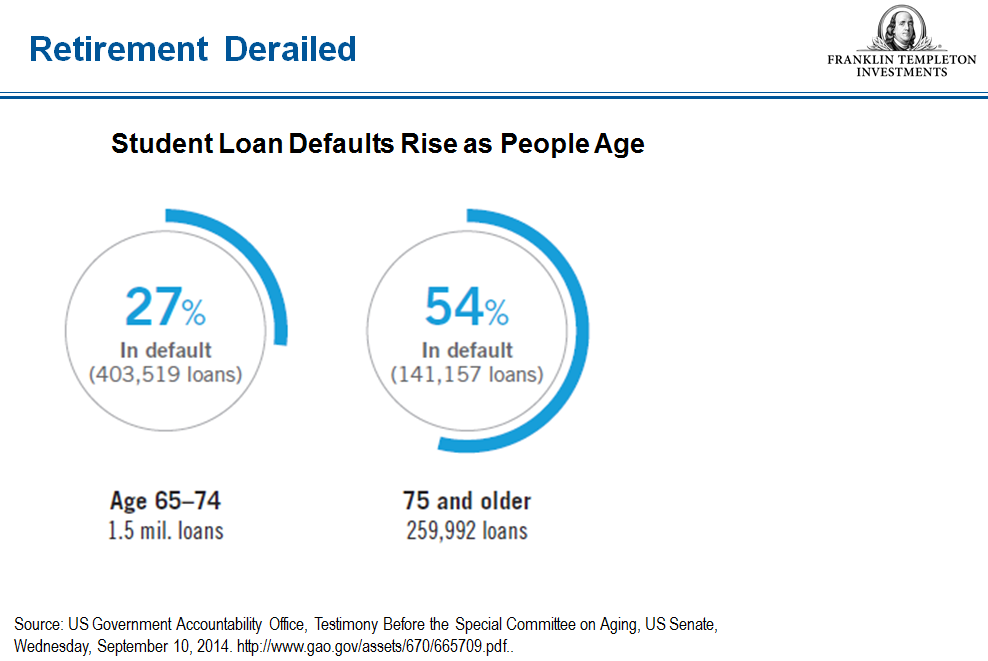

For older borrowers who rely on student loans to finance their own education, government statistics show their default rate is much higher than that of younger borrowers. For individuals aged 25–49 who held federal student loans, only 12% were in default, while 27% of loans held by individuals 65–74 were in default, and more than half of the loans held by individuals 75 or older were in default.4

This is affecting their retirement income as well. The number of people whose Social Security checks are garnished due to student loan defaults has skyrocketed in recent years, increasing fivefold since 2001.

Long-Term Effect of Student Loans and a Solution in Three Numbers

But there is some good news. According to the College Savings Foundation’s 9th annual survey, overall, there was an upswing in parental saving from the year prior: 53% of all parents reported they are saving; and nearly half (48%) reported saving at least $5,000 per child. And, for 33% of parents, a 529 college savings plan was part of their savings strategy.5

What’s a 529 plan? Legally known as a “qualified tuition plan,” these college savings vehicles can be sponsored by states, state agencies or educational institutions. These programs allow parents, grandparents and even other family members and friends to help a designated beneficiary (for example, a child) save for college costs. One of the appealing features of a 529 savings plan is that money invested grows free of federal income tax when withdrawn for qualified higher education expenses such as tuition, books, and room and board. Depending on where you live, you may be able to take advantage of state tax benefits, too.6

Tax benefits of 529 plans are conditioned on meeting certain requirements. Federal income tax, a 10% federal tax penalty and state income tax penalties apply to non-qualified withdrawals of earnings. Generation-skipping tax may apply to substantial transfers of assets to a beneficiary at least two generations below the contributor.

One Small Step for a Brighter Future

It seems like sage advice to save early, save often, and save consistently—what 71% of retirees polled in our RISE survey said they would advise someone who hadn’t yet retired.7 While that advice sounds very reasonable, only 56% of those with children in the home are currently saving for retirement.8 I think it’s crucial for families to make college planning part of their overall retirement savings and investment plans. Investors may want to consider striking a balance between saving for college and saving for retirement. Emphasizing one over the other could jeopardize both investment goals in the end.

You’ve probably heard dour statistics about rising tuition costs and rising student debt, which has exploded to more than $1.2 trillion.9 At the same time, there has been a decline the number of people saving for retirement—at least according to our RISE surveys over the past two years.

Don’t be overwhelmed. Consider taking small steps. Retirement planning varies from one individual to the next. There are many creative ways to finance a college education, from enlisting a family “crowd-funding” solution to pursuing community college for the first two years to exploring various scholarships and grants. Ideally, individuals should be able to plan and save for retirement and college at the same time. It should be possible, with some proper planning, creative solutions and perhaps a few sacrifices. Your children will thank you for their education, and you’ll be thankful for a more stress-free retirement!

Want More Information and Strategies?

Learn about the “$1 Solution,” an answer to the conundrum faced by families caught between needing money for both retirement and college. It can give information that may help you determine how to allocate funds, while also boosting college savings by $1 per day.

Whether you are just getting started or have been saving for years, watch our short video, “5 Strategies of Successful College Savers,” to see more strategies that can help in the quest.

Learn about 529 College Savings Plans at Franklin Templeton and talk to an advisor for savings ideas and strategies that are best for you and your family.

What Are the Risks?

All investments involve risks, including potential loss of principal.

Investors should carefully consider college savings plan investment goals, risks, charges and expenses before investing. To obtain a disclosure document, which contains this and other information, talk to your financial advisor or call Franklin Templeton Distributors, Inc., the manager and underwriter for a 529 plan at (800) DIAL BEN®/(800) 342-5236 or visit franklintempleton.com. You should read the disclosure document carefully before investing and consider whether your, or the beneficiary’s, home state offers any state tax or other benefits that are only available for investments in its qualified tuition program.

____________________________________________________

1 Source: Franklin Templeton College Savings Trends Survey. Conducted online among a sample of 1,009 adults comprising 506 men and 503 women 18 years of age and older. The survey was administered between April 30 and May 3, 2015, by ORC International’s Online CARAVAN, which is not affiliated with Franklin Templeton Investments. Data is weighted to gender, age, geographic region, education and race. The custom-designed weighting program assigns a weighting factor to the data based on current population statistics from the US Census Bureau.

2 Source: Franklin Templeton Retirement Income Strategies and Expectations (RISE) survey. Conducted online among a sample of 2,019 adults comprising 1,011 men and 1,008 women 18 years of age or older. The survey was administered between January 4 and 18, 2016, by ORC International’s Online CARAVAN®, which is not affiliated with Franklin Templeton Investments. Investors in the United States can visit www.franklintempleton.com/rise for more information.

3 Source: College Savings Foundation’s 9th Annual State of College Savings Survey, August 2015.

4 Source: US Government Accountability Office, Testimony Before the Special Committee on Aging, US Senate, Wednesday, September 10, 2014.

5 Source: College Savings Foundation’s 9th Annual State of College Savings Survey, August 2015.

6 It’s important to remember that, as with any investment, principal value may be lost, and investing in the plan does not guarantee admission to college or sufficient funds for college. There is no federal or state guarantee of investments in the plan.

7 In the United States, the Franklin Templeton Retirement Income Strategies and Expectations (RISE) survey was conducted online among a sample of 2,019 adults comprising 1,011 men and 1,008 women 18 years of age or older. The survey was administered between January 4 and 18, 2016, by ORC International’s Online CARAVAN®, which is not affiliated with Franklin Templeton Investments. Investors in the United States can visit www.franklintempleton.com/rise for more information.

8 Ibid.

9 Source: Federal Reserve Bank of New York, Quarterly Report on Household Debt and Credit, data as of December 2015.

© Franklin Templeton Investments

© Franklin Templeton Investments